|

|

|

|

|

| |

|

Vol. 9 - Issue 8

December 7, 2020

|

|

|

|

|

|

| |

Joe Lieberman spent 24 years in the United States Senate and in 2000 came thisclose to being Vice-President of the United States. Before that he spent over a decade as a lawyer in private practice. And he’s back at it. I spent an hour on the phone with Lieberman, for the ABA Journal, discussing a wide range of topics, including something that the former Senator did 60 years ago that offers a lesson for lawyers today.

https://www.abajournal.com/columns/article/joe-lieberman-reflects-on-50-years-in-law-and-politics-and-recounts-a-famous-supreme-court-case

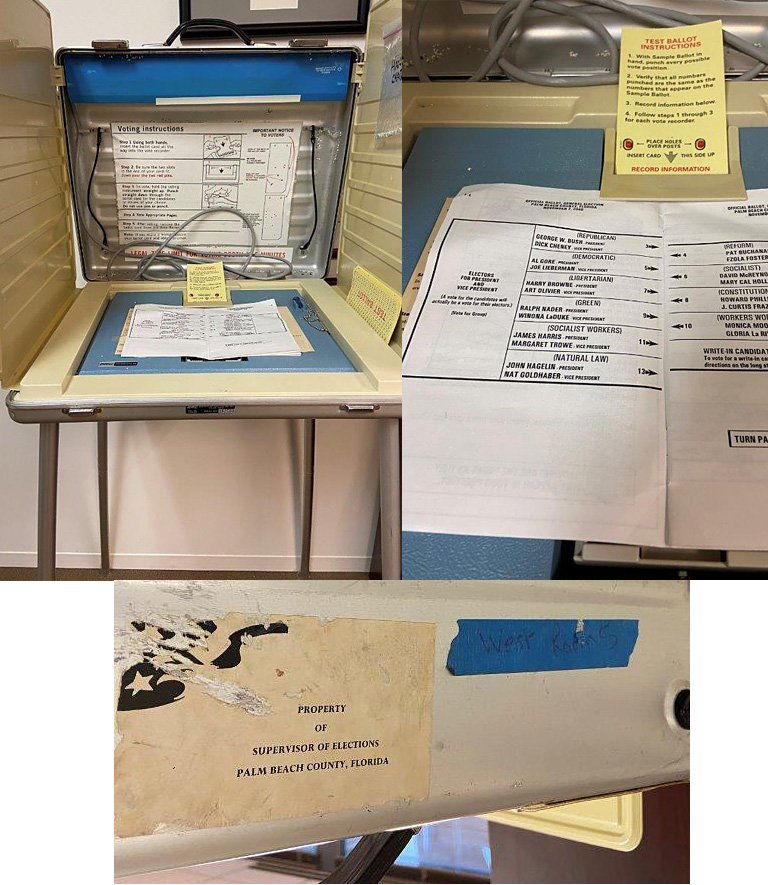

I’ve long been fascinated with the aftermath of the 2000 Presidential election, as evidenced by the BRC Votomatic III, used in Palm Beach County during the 2000 election, that I proudly own.

As my wife said when I got it – “That thing can live in your office.” |

| |

|

|

|

|

Vol. 9 - Issue 8

December 7, 2020

If Costco Were An Insurance Company

|

|

|

|

|

| |

I love going to Costco. Who doesn’t? It’s so much fun to marvel at the giant packages of the products. Whoa! Who knew Ritz Crackers came in a box of 5,000. And I like knowing that if I ever need a 55-gallon drum of Skippy, it’s there for me.

Now imagine if Costco were an insurance company. There’s no way it would function like a regular insurance company. It wouldn’t know how. It would only know how to be, well, Costco. You could expect to see Costco Property & Casualty Insurance Company operate like this:

- Insureds are not mailed a Declarations Page. Rather, they are given directions where to drive to see their Dec page on a billboard on the side of the highway.

- When a reservation of rights letter is sent, also included is a box of 50 copies.

- Claims are paid with those giant checks used to show off prizes and charitable contributions.

- Claim numbers are 64 digits.

- When the company has a duty to defend, it hires three law firms for the insured.

- When a mediation takes place in New York City, the Costco adjuster requires that his or her breakout room be Madison Square Garden.

- In cost sharing, adjusters pout when they don’t have the largest share.

- The company always takes a multiple occurrences position.

- Like Allstate, the company’s advertising spokesperson is also called Mayhem Man. It’s King Kong.

- Policies are drafted by Tolstoy.

|

| |

That’s my time. I’m Randy Spencer. Contact Randy Spencer at

Randy.Spencer@coverageopinions.info |

|

| |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Vol. 9 - Issue 8

December 7, 2020

Encore: Randy Spencer’s Open Mic

SkyMall And Insurance Coverage

|

|

|

|

|

|

| |

SkyMall, the catalogue that you used to see in the back of airplane seats, featuring all kinds of odd products that you don’t need, but can’t live without, is no more. The magazine of consumer curiosities no doubt failed because it didn’t have enough insurance coverage related items.

Randy Spencer looked closely at this situation in 2015:

https://www.coverageopinions.info/Vol4Issue9/RandySpencer.html

|

That’s my time. I’m Randy Spencer. Contact Randy Spencer at

Randy.Spencer@coverageopinions.info |

|

| |

|

| |

|

|

|

|

Vol. 9 - Issue 8

December 7, 2020

What Does An Insurance Company Taste Like?

For The 2nd Time: Coverage Opinions Discusses Alpha-Bits Cereal And Insurance

|

|

|

| |

Back in the November 11, 2015 issue of Coverage Opinions I responded to a lawyer’s billboard, claiming that he eats insurance companies for breakfast, by wondering what they taste like. Chicken no doubt. Actually, this is what insurance companies taste like:

|

| |

|

| |

I never imagined that I would discuss insurance and Alpha-Bits cereal again. But the opportunity has arisen.

In Post Holdings v. Liberty Mutual Fire Insurance Company, No. 18-1741 (E.D. Mo. Oct. 30, 2020), the Missouri federal court addressed coverage for Post Holdings, maker of numerous breakfast cereals, for a putative class action alleging – as described by the court -- that it “actively maintains a policy and practice of labeling high-sugar cereals . . . with various health and wellness claims that suggest the cereals are healthy, when they are not.” According to the court, the complaint alleges that, “when buying Post cereals, the plaintiffs were seeking to buy those that were ‘healthy to consume,’ but Post’s misrepresentations induced them to buy ‘products [that] are not healthy . . . instead their consumption increases the risk of CHD, stroke, and other morbidity.’” Again, according to the court: “The Complaint alleges that, as a result of Post’s practices, the named plaintiffs themselves ‘suffered bodily injury in the form of increased risk of CHD, stroke, and other morbidity.’”

At the heart of the coverage dispute was whether the underlying complaint seeks damages for “bodily injury,” to trigger coverage under the cereal maker’s commercial general liability policy. The court held that it did not. Rather, the court interpreted the underlying complaint as alleging that, eating Post’s cereals, could result in bodily injury in the future:

“Although the Krommenhock Suit contains references to ‘bodily injury,’ upon analysis, it is abundantly clear that no ‘bodily injury’ is alleged to have been sustained by the Krommenhock plaintiffs. The allegations in the underlying suit detail that there is a chance someone eating the sugary cereals may develop certain conditions as a result, but nowhere contained in the allegations do the Krommenhock plaintiffs claim they have actually suffered any of the potential conditions.”

Being a Curious George type, I wondered which cereals were at issue in the underlying litigation. So I got a copy of the complaint. There are many, including Bran Flakes, Honey-Comb and Raisin Bran [WHAT? Raisin Bran!]. And what do you know, right there at paragraph 225: Alpha-Bits in the plaintiff’s cross-hairs. Note to any plaintiff’s attorneys who eat insurance companies for breakfast: be careful.

|

| |

|

|

|

|

Vol. 9 - Issue 8

December 7, 2020

A Coverage Opinions Reader Brings Back A Fond Memory: My First Insurance Contest. No Mickey Mouse Affair

|

|

|

| |

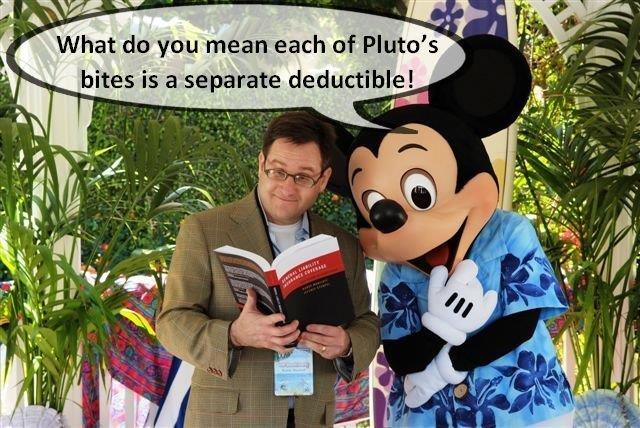

As readers of Coverage Opinions know, I’m a big fan of insurance contests and often give away copies of Insurance Key Issues as prizes. A long-time Coverage Opinions reader reminded me of one that I did eons ago. In fact, it was my first-ever contest. And, it even goes back so far that it pre-dates CO. Before CO I sent emails to insurance folks with write-ups of recent decisions of significance or interest. It was called “Binding Authority.” CO is a low-budget operation. This was a no-budget operation. But “Binding Authority” was fun to do and led me to aspire to something bigger – which was CO.

Tony Antonico, of Antonico Insurance Consulting in Manchester, NH, sent me this photo. I had completely forgotten about it. It was taken at the 2011 West Coast Casualty Construction Defect Seminar at Disneyworld in Anaheim. The first edition of Insurance Key Issues had just come out and West Coast Casualty bought a copy for each attendee. I was there to say thank you.

No surprise that the world’s most famous mouse was more interested in checking out Insurance Key Issues than the nearby cheese buffet at the seminar cocktail party. I was inspired by the photo to have a caption contest, which Tony won with this very clever entry. Thank you to Tony for bringing back a great memory.

|

|

| |

| |

|

|

|

|

Vol. 9 - Issue 8

December 7, 2020

University of Pennsylvania’s “Covid Coverage Litigation Tracker” Keeps Going Strong

|

|

|

| |

Given that decisions addressing business interruption coverage, for Covid-19 losses, can now be seen as often as Law & Order reruns, it is getting quite difficult to keep track of them all. But it does not need to be. Not at all.

As I mentioned in the last issue of Coverage Opinions, the “Covid Coverage Litigation Tracker,” run by Penn Law School’s Professor Tom Baker, is doing a tremendous job of keeping a running list of them and their outcomes. The tracker showed 80+ decisions as of Saturday morning. I’ve lost track of the number of publications that have used Tom’s statistics in reporting on Covid coverage litigation.

Click here to see the Covid-19 coverage litigation scorecard, as well as a slew of other statistics about the litigation and commentary.

|

|

| |

| |

|

|

|

|

Vol. 9 - Issue 8

December 7, 2020

What To Get The Insurance Coverage Fanatic On Your Holiday Gift List

|

|

|

| |

What else. www.InsuranceKeyIssues.com

Get the law in 50 states (and D.C.) on these issues and nearly 20 more:

Is faulty workmanship a Ho, Ho, Hoccurrence?

Number of occurrences: Does the claus test apply?

Insurability of naughty damages?

|

|

| |

| |

|

|

|

|

Vol. 9 - Issue 8

December 7, 2020

Crazy Case: But Not To Coverage Opinions Pen Owners

|

|

|

| |

|

| |

Well, I’m getting close to finishing sending out Coverage Opinions pens to all who requested one. It’s been a challenge. After that, I’ll send them to those who won one as a prize in the “Most Interesting Insurance Man or Woman in the World” contest. Then I’m done. And it may be a while before I do this again. It was a good idea. Until it wasn’t a good idea.

But something was reported in the media last week that made me think about CO pen recipients – much as I’ve been trying not to.

Several media outlets had the story of a New York lawyer who went to trial over a temporarily stolen pen and was awarded $2.00 by the jury [$1.00 for damages and $1.00 for attorney’s fees].

From the New York Post: “A civil rights lawyer who made a federal case out of a pen got a measly $2 after he sued the city because a cop snatched away his pen. ‘Once upon a time, we urged people not to make too much of real but petty grievances by saying, ‘Don’t make a federal case out of that,’ wrote US District Judge Colleen McMahon of Jeffrey Rothman’s lawsuit. ‘This lawsuit was a violation of that principle writ large.’”

Here is the full Post story:

https://nypost.com/2020/12/01/nyc-civil-rights-lawyer-wins-2-in-pen-snatching-lawsuit/

Who in the world would file suit, and have a jury trial, over a stolen pen (and one that was quickly returned)? It’s crazy. Wait, I know. CO pen owners would do this if their precious writing implement had been taken from them, even if just for a moment. They know what I’m talking about.

|

| |

| |

| |

|

|

|

|

Vol. 9 - Issue 8

December 7, 2020

Big Fight Brewin’: I’m Not Surprised That Someone Filed This Lawsuit

|

|

|

| |

For many years coffee in my house has been stored in a large plastic Folgers container, located in the cabinet above the coffee maker. It hasn’t had Folgers coffee in it for years [my wife had a Folgers stage]. Rather, whatever kind of coffee we buy – Starbucks, La Colombe, Trader Joes or some uber-organic offering from Whole Foods (grown in a region of the amazon where it rains Evian) -- gets poured into it.

We go though it very quickly. Which is why I’ve always marveled at the statement on the container that it makes up to 210 six ounce cups. I never did the math, but that number always seemed high to me. That’s a lot of cups of coffee. Maybe you get that many cups if you only use a super small amount of coffee per cup? Or maybe you get 210 cups, but they are the size of the ones we used when my daughter was 5 years old and we sat on the floor having tea parties?

In any event, imagine my surprise, or not, when I saw that a putative class action was filed, earlier this month in the Northern District of Illinois, against Folgers, alleging that it “grossly exaggerated the number of cups of coffee that the Folgers ground coffee products can make in order to induce consumer purchases and to charge consumers more for these products.” The complaint even includes pictures of the very coffee container in my kitchen. And it turns out that some Folgers containers claim to make up to 240 cups.

The complaint in Ellen Moser, individually and on behalf of all others similarly situation v. The J.M. Smucker Company, et al., United States District Court for the Northern District of Illinois, No. 20-7074, reads like a statistics textbook. It is filled with all sorts of calculations that allegedly reveal how many cups of coffee can come from various containers of Folgers coffee, versus how many are promised on the package. The plaintiff’s attorneys definitely followed the math class rule of showing their work.

For example, consider this explanation as set out in the complaint:

21. On the back of all the Products, Defendants instruct consumers that they should use 1 tablespoon of ground coffee to make 1 serving/cup of coffee.

22. One tablespoon of ground coffee weighs approximately 5 grams.

23. Based on these standard measurements, it is evident that Defendants grossly overstate the number of servings the Products can make.

24. By way of example, Defendants represent on the 30.5 oz. canister of the Folgers Classic Roast that it "MAKES UP TO 240 6 FL OZ CUPS."

25. As set forth above, one tablespoon of ground coffee is needed to make 1 serving. Therefore, 240 tablespoons of ground coffee are needed to make 240 servings.

26. As set forth above, one tablespoon of ground coffee = approximately 5 grams. Therefore, 1200 grams of ground coffee is needed to make 240 servings [240 tablespoons x 5 grams].

27. However, the 30.5 oz. canister has a net weight of 865 grams. Therefore, it contains only 72% of the amount of ground coffee required to make up to 240 cups of coffee [865 / 1200 x 100%]. This is equivalent to approximately 173 cups of coffee.

28. The same shortfall (i.e., only 173 cups of coffee) is calculated by dividing the total grams of coffee in the 30.5 oz. cannister by the number of grams required to make a single serving [865 grams / 5 grams].

This got me thinking. If a train leaves Chicago at 2 PM, with 139 six ounce cups of Folgers on board, and a train leaves Miami at 4 PM with 912 grams of coffee on board, how may eight ounce cups of coffee can there be when the trains cross paths in Indianapolis? Show your work.

The complaint sets out "promised versus actual" cup numbers for dozens of different types of Folgers coffee products, resulting in the following conclusion:

32. There are 40 varieties of the Products listed in the chart above. Each and every one of them contains substantially less ground coffee than is required to make the recommended number of "up to" servings promised on the packaging. On average, these Products contain enough ground coffee to make only 68.33% of the number of servings promised on the packaging, thus revealing a systematic course of unlawful conduct by Defendants to deceive and shortchange consumers.

I have no idea where this will go. But since we don’t put Folgers coffee in the Folgers container, I won’t be getting a coupon, for a free 6 ounce cup of Folgers coffee, if there is a settlement.

|

| |

| |

| |

|

|

|

|

Vol. 9 - Issue 8

December 7, 2020

Traditional Environmental Noise: Court Addresses Applicability Of Pollution Exclusion To Car Horn Honking [Real Case]

|

|

|

| |

Regular readers of Coverage Opinions have heard me say that I don’t address the pollution exclusion too often. Back in the day it was a great issue. There were so many interesting cases addressing the parameters of the exclusion – both as a matter of law [the traditional versus non-traditional scope issue] and factually [does the pollution exclusion apply to this hazardous substance or that]. But, as the number of cases has grown – like a weed – there are lesser opportunities for novel issues. There are probably some cases, with good facts, that are not being litigated, because existing case law dictates, with enough assurance for those involved, whether the pollution exclusion applies.

Early last month a California federal court gave pollution exclusion enthusiasts something to get excited about. The court addressed the novel issue of whether the pollution exclusion – admittedly, a unique one – applied to a claim for unwanted noise.

The decision in Crosby Estates at Rancho Santa Fe v. Ironshore Specialty Ins. Co., No. 19-2369 (S.D. Calif. Nov. 3, 2019) is somewhat lengthy. As I’m wont to do in these situations, I’ll focus on just the part what matters for purposes here.

The coverage issues arise out of the following scenario. The Crosby Estates at Rancho Santa Fe, a community association, was sued by a neighboring community association, Avaron Community Association. Wait till you see this. We’re talking some bad blood between these condos.

The court described the war between the condos as follows:

“Avaron alleged that in 2007, Avaron and The Crosby entered into a ‘Shared Use Maintenance Agreement’ giving The Crosby an easement for ingress and egress over Avaron’s property. Avaron alleged that The Crosby 1) breached the Shared Use Maintenance Agreement by removing speedbumps on Avaron’s property; 2) interfered with Avaron residents’ quiet use and enjoyment by instigating ‘Operation Honk,’ a coordinated effort in which residents of The Crosby repeatedly honked their car horns when they passed over speedbumps on Avaron’s property; and 3) intentionally destroyed and removed speedbumps on Avaron’s property to allow residents of The Crosby to ‘drive as fast as they can through the easement without regard for the safety or well being of the residents and guests in Avaron.’ Avaron sought compensatory damages, punitive damages, termination of The Crosby’s rights under the SUMA, and injunctive relief.”

The Crosby, insured under a D&O policy issued by Ironshore, sought coverage for the Avaron suit. Ironshore initially disclaimed coverage and then agreed to provide a defense to The Crosby as a courtesy. But then there were all kinds of issues concerning the role of a retention on the defense and choice of counsel. The opinion devotes numerous pages to these issues. I’ll skip all of that here.

At some point a coverage action was filed by The Crosby against Ironshore. Again, the ins and outs of this are not relevant for purposes here.

Here’s the part that matters. Ironshore maintained that it had no obligation to provide coverage to The Crosby on account of the policy’s pollution exclusion. Huh? The pollution exclusion? The Crosby had been sued because its residents honked their car horns when they passed over speedbumps on Avaron’s property. And they allegedly destroyed and removed speedbumps on Avaron’s property. What in the world does that have to do with the pollution exclusion?

It is tied to the policy’s definition of “pollutants:” “any substance located anywhere in the world exhibiting any hazardous characteristics as defined by, or identified on any list of hazardous substances issued by, the United States Environmental Protection Agency or any state, county, municipality or locality counterpart thereof. Such substances shall include, without limitation, solids, liquids, gaseous or thermal irritants, contaminants or smoke, vapor, soot, fumes, acids, alkalis, chemicals or waste materials. Pollutants shall also mean any other air emission, odor, waste water, oil or oil products, infectious or medical waste, asbestos or asbestos products and any noise.”

The pollution exclusion here, when you apply this definition of “pollutants,” is about as broad as you can get (especially when you consider its reference to that which every governmental entity in America -- from the United States, down to my township – may consider a hazardous substance).

At the very end of the definition is “any noise.”

Of course horn honking is “any noise.” But that wasn’t how the court went about addressing the potential applicability of the exclusion. Rather, the court stated that it was compelled to interpret “noise” in the context of how it is used in the policy – within the definition of “pollutant” – and not literally and in isolation.

By doing so, the court reached the following conclusion: “It is reasonable that a layperson may not consider someone honking their horn while they pass over a speedbump to be a pollutant or pollution. [MacKinnon] (‘[T]he interpretation of the pollution exclusion as limited to conventional environmental pollution is . . . reasonable.’). Based on the Policy provisions and the allegations in the Avaron Lawsuit complaint, the Court concludes that interpreting the pollution exclusion to include car horn honking is not the only reasonable interpretation.” (emphasis in original).

The court’s opinion does not say this specifically, but it seems that, for purposes of “noise,” it was limiting the pollution exclusion to noise related to an environmental or hazardous substance. In a way, the court is limiting the exclusion to “traditional environmental noise.” In that case, perhaps this pollution exclusion would apply to noise created by trash trucks, the operation of a waste disposal facility or a rock quarry.

But a claim against Aunt Gertrude, for injury caused by her constant talking about her bursitis, would not be precluded under the Crosby Estates court’s analysis. [Don’t worry Aunt Gert, we would never sue you. Then you wouldn’t stop talking about that.]

|

| |

| |

| |

|

|

|

|

Vol. 9 - Issue 8

December 7, 2020

Court Addresses Rate For Policyholder-Selected Defense Counsel -- And Takes Guidance From Judge Posner

|

|

|

| |

Many of us – on both sides -- deal with this issue regularly: the rate to be paid by an insurer to counsel chosen by the policyholder. The gap, between the amount that the insurer and insured each believe is reasonable, can be quite wide. Simply put, there are no easy answers here. And, for that matter, not even many answers. I’ve always found it curious that there is not more case law on the issue.

A New York federal court addressed the issue last month in Value Wholesale, Inc. v. KB Insurance Company, No. 18-5887 (E.D.N.Y. Nov. 2, 2020). To be clear, the court had found that the insurer breached its duty to defend and was now determining how much the insured was entitled to recover for its defense costs. That may not be the same as an insurer who affirmatively agrees to pay independent counsel, for its insured’s defense, and then a dispute arises over the rates. A policyholder can be expected to argue that a court should be less sympathetic to the insurer in the former case. So the argument may go - if the insurer is not happy with the defense costs, it should have defended the case. I’ve seen courts say just that.

In Value Wholesale, the court had earlier determined that the insurer beached the duty to defend its insured in an intellectual property case that had triggered commercial general liability coverage for advertising injury. The ins and out of that are not important for purposes here. I address here simply the court’s handling of the hourly rate issue that was part of the policyholder’s claim for reimbursement of its defense costs. [There are lots of other issues address by the court, concerning the attorney’s fees to be paid, that I do not discuss here.]

The insurer argued that the fees charged by the insured’s counsel were too high. To support its argument, the insurer cited to civil rights cases that involved fee shifting. But the court concluded that these decision were not directly on point. In civil rights cases, the court observed, the plaintiff’s attorney likely worked on a contingency fee basis. There, because the plaintiff paid no fees, the court’s job is to determine what a reasonable, paying client, would be willing to pay.

Here, when the breach of the duty to defend is at issue, “the court is not faced with a situation in which it must award fees, pursuant to a fee-shifting statute, to a plaintiff's lawyer who did not yet receive any fees. Rather, the question before this court is the amount of damages owed by KBIC as a result of its breach of its contractual duty to defend Value. In such a situation, the amount of damages is the attorneys’ fees and litigation expenses reasonably incurred by the insured in defending the underlying action. Though the fees must have been reasonably incurred, the reasonableness inquiry is slightly different than the one at issue in [the civil rights cases].”

The court concluded that the rates charged, for complex intellectual property litigation in Brooklyn federal court, involving a sophisticated medical device company -- $550/hr. for partners and $325 for associates, increasing to $600 and $400 after July 1, 2018 – were reasonable. In reaching this conclusion, the court had this to say: “Where an insurer has breached its duty to defend, the insured’s fees are presumed to be reasonable and the burden shifts to the insurer to establish that the fees are unreasonable.”

[It didn’t help the insurer’s case that its own expert charged $550/hr. to review and analyze the law firm’s invoices.]

In reaching its decision, that the time expended by the attorneys was reasonable, despite the insurer’s vocal protestations, the court quoted what it called a “persuasively written” observation from the Seventh Circuit’s Judge Richard Posner in Taco Bell Corp. v. Continental Casualty (2004): when there is “uncertainty about reimbursement, [an insured has] an incentive to minimize its legal expenses (for it might not be able to shift them); and where there are market incentives to economize, there is no occasion for a painstaking judicial review.”

|

| |

| |

| |

|

|

|

|

Vol. 9 - Issue 8

December 7, 2020

Car Crashes Through Restaurant Window. Result: Lesson In The History Of Additional Insured Coverage

|

|

|

| |

Back in the day, additional insureds were often-times afforded coverage for liability “arising out of” the named insured’s work for the additional insured. When confronted with such language, courts often concluded that it dictated “but for” causation. In other words, but for the named insured doing the work for the additional insured, the additional insured would not be in the liability-facing situation that it is. The result in some cases: additional insureds were entitled to coverage for their sole negligence. Decisions reaching such conclusion were generally not well-received by insurers. This was especially so when you consider that the premium received by insurers, for the AI coverage, may not have been enough to buy a package of Twizzlers.

Insurer frustration with such decisions -- which insurers did not believe expressed the intent of additional insured coverage -- led ISO to make revisions to additional insured forms in 2004 [and later revisions followed]. At the heart of these revisions was an attempt to require fault on the part of the named insured before coverage could be afforded to the additional insured. [This is a very brief and simple history of this complex issue.]

Given that the use of “arising out of”-type additional insured endorsements have been waning over the years, decisions addressing them have been fewer and fewer. But one came along not long ago. The insurer lost. No doubt it was not happy with the outcome -- and for the same reason why ISO changed the additional insured endorsements in 2004.

I am sure that some insurers are still using the form of endorsement that led to the insurer frustration here. Insurers have, in their own hands, the ability to avoid the outcome that befell the insurer here. As the old saying goes, those who do not learn history are doomed to repeat it.

The history lesson at issue in Truck Insurance Exchange v. Amco Insurance Co., No. B298798 (Ct. App. Cal. Oct. 26, 2020) [published] was coverage for the Awads, owners of a commercial property in Long Beach, as additional insureds under an Amco Insurance Company policy issued to their tenant, Scott Bascon, owner of Holé Molé Restaurant.

In 2013, the Smiths were dining in Holé Molé when two cars collided outside. One of them crashed into the restaurant, continued through the establishment and pinned the Smiths to a wall, causing injuries. Holy moly -- with a y.

The Smiths filed suit against Bascon/Holé Molé and the Awads. Holé Molé was dismissed on summary judgment on the basis that, from Bascon’s perspective, the accident was not foreseeable. But not so for the Awads, as the landlord, on the basis that an accident in 2007 made them liable for not taking any action to prevent the 2013 accident.

The Awads insurer, Truck Insurance Exchange, settled the matter for $785,000. Truck then filed an equitable subrogation action against Amco, Holé Molé’s insurer, alleging that the Awads were entitled to coverage, as additional insureds, under the Amco policy. There is nothing at all surprising about a landlord being an additional insured on a tenant’s policy.

The additional insured endorsement, at issue in the Amco policy, provided as follows:

“Any person or organization from whom you [Bascon] lease premises is an additional insured, but only with respect to their liability arising out of your use of that part of the premises leased to you.”

As Truck saw it, the Smiths’ claim arose out of Holé Molé’s use of the premises. So Truck’s argument went, the Smiths would not have been injured, but for Bascon’s use of the premises as a restaurant.

Amco had a much different take on how to interpret the additional insured endorsement. At its core, Amco’s argument was that, because the car accident was not casually connected to Bascon’s “use” of the leased premises, the Awads were not additional insureds. The undertone of Amco’s argument was that, because Bascon was not liable for the accident (which is true, as he was dismissed from the action), the Awads were not additional insureds. Thus, under this scenario, the Awads were seeking coverage, as additional insureds, for their sole negligence. How can that be?

However, the California Court of Appeal, like the trial court, found in favor of Truck and ordered Amco to pay Truck 50% of its settlement of the Smiths’ claim.

This is how. The appeals court relied extensively on its 1999 decision in Acceptance Insurance Co. v. Syufy, which may be the most frequently-cited case nationally on the broad interpretation of “arising out of” additional insured endorsements.

As the Syufy court explained it: “California courts have consistently given a broad interpretation to the terms ‘arising out of’ or ‘arising from’ in various kinds of insurance provisions. It is settled that this language does not import any particular standard of causation or theory of liability into an insurance policy. Rather, it broadly links a factual situation with the event creating liability, and connotes only a minimal causal connection or incidental relationship.”

The Syufy court also noted, importantly, “the policy language does not purport to allocate coverage according to fault.” (emphasis added). Further, “when an insurer grants coverage for liability ‘arising out of’ the named insured’s work, the additional insured is covered without regard to whether injury was caused by the named insured or the additional insured.”

Applying Syufy here, but for Bascon using the premises as a restaurant, the Smiths would not have been present there. In addition, the theory of liability, against the Awads, was that the property itself was dangerous, as the Awads knew that a car could crash into the building but failed to take steps to prevent it.

This, the court concluded, was all that was necessary to establish the causal connection to trigger additional insured coverage under an “arising out of” provision.

As I said, insurers have in their own hands the ability to avoid the outcome here. Many have. But as that old saying goes…

|

| |

| |

| |

|

|

|

| |

|

Vol. 9 - Issue 8

December 7, 2020

Insurer Liable For Bad Faith -- For Filing A Declaratory Judgment Action

|

|

|

| |

I’ve said for a long time that when insurers are found liable for bad faith, it is usually not because their coverage determination was erroneous. Courts generally give insurers wide latitude to get a coverage determination wrong – and conclude that it was not done in bad faith. The bad faith standard is usually quite high – too high to be satisfied because an insurer’s interpretation of the meaning of “mobile equipment” was not correct. All of this is notwithstanding how some policyholder counsel define “bad faith” -- anything the insurer does that he or she does not agree with.

Insurer liability, for bad faith, is usually tied to the manner in which the insurer handled a claim. In other words, it is not the coverage determination that was made in bad faith, but how it was reached. Often-times this has to do with the insurer’s investigation of a claim.

That’s what happened in Travelers Property Cas. Co. v. North American Terrazo Co., No. 19-1175 (W.D. Wash. Nov. 13, 2020), but in a different way. Travelers filed a declaratory judgment action, seeking a determination that it had no obligation to provide coverage for a construction defect claim. As Travelers saw it, the claim was excluded by the “your work” exclusion. On its face, this seems relatively straightforward. But it wasn’t. The court concluded that the insurer’s decision to file the DJ was made in bad faith, and the insurer was estopped to deny coverage.

The facts giving rise to the situation started in the kitchen of a restaurant. North American Terrazzo (“NAT”), as a subcontractor to SODO Builders, installed an epoxy flooring at the 13 Coins restaurant in Washington. The epoxy had been supplied by Terrazzo & Marble Supply Co. of Illinois (T&M). The work was completed in December 2017. In May 2018 and later, NAT began to notice damage to the flooring in various places.

Here’s the key to the case: T&M undertook a lab analysis, on a sample of the epoxy flooring, in an effort to find the cause of the damage. It identified five possible causes of the damage. Of note, three were related to work performed by NAT: preparation of the existing concrete floors, improper mixture of the epoxy and inadequate thickness of the application. But two other possible causes were not related to NAT’s work: exposure to heat above 140 degrees Fahrenheit and standing water.

To make a long story short, NAT reported a potential claim to Travelers. Travelers provided a defense, under a reservation of rights, even though no complaint had been filed. NAT replaced the epoxy flooring with tiles. A mediation to settle the underlying claims was not successful. A settlement was reached after a second mediation. It included no contribution from Travelers. SOTO was to receive $200,000 and 13 Coins was to receive $300,000.

Somewhere along the way, Travelers had filed a declaratory judgment action. The decision is a little complex. But it can be boiled down to this. The court observed that Travelers knew, within a month of getting the claim, that the “your work” exclusion or “your product” exclusion could preclude coverage.

The claim is clearly one involving “your [NAT’s] work.” There is no dispute about that. But that did not mean that the “your work” exclusion applied. The exclusion applies to property damage to the insured’s work, arising out of the insured’s work – and not some other source.

But, as noted above, T&M’s lab analysis identified five possible causes of the damage – three related to work performed by NAT and two other possible causes that were not related to NAT’s work. And, if they were not related to NAT’s work, then the property damage was not arising out of NAT’s work. Therefore, there were reasons why the “your work” exclusion may not have applied.

And, as the court observed, Travelers did not have a definitive answer on the cause of the damaged floor:

“Travelers knew that there was a limited window to investigate the epoxy flooring before it would be removed and replaced. But Travelers sent only one investigator before the flooring was replaced. And she simply made visual observations of the damage and took photographs. Travelers’ coverage adjuster did not visit the site, take a sample, or retain an expert before the repairs were made. And Travelers did not retain a flooring expert until after the damaged flooring was replaced. Over two months before Travelers filed this action, its flooring expert, Phillips, put Travelers on notice that only forensic testing of the damaged flooring could allow him to determine the flooring failure’s cause. Phillips stated: ‘[I] cannot determine the cause of the failure without analyzing a product sample to determine the laboratory results of the mixture of the product’ and ‘[a] forensic laboratory analysis will be able to determine what is the probable cause of failure.’ Travelers has not provided any forensic evidence or expert evidence as to the cause of the flooring's damage.”

Held: “Both exclusions require evidence that the property damage ‘arose out of’ the insured's work or product and not some other source. Travelers’ failure to investigate meant that it could not make a reasonable determination of coverage. This violated Travelers’ quasi-fiduciary responsibilities to investigate the claims. And the undisputed evidence demonstrates that Travelers filed this lawsuit knowing from its own expert that it could not prove the claims it has asserted. Travelers actions were ‘unreasonable’ and ‘unfounded’ and constitute bad faith.”

The court further concluded that the bad faith finding justified a “presumption of harm” and “coverage by estoppel.”

|

| |

| |

| |

|

|

|

|

Vol. 9 - Issue 8

December 7, 2020

Number Of Occurrences…And Kabobs

|

|

|

| |

I have not seen many decisions lately addressing number of occurrences. It is usually a frequently litigated issue. This I know from having followed it, for the past ten years, as part of writing Insurance Key Issues. And no surprise it is so popular. The number of occurrences at issue can make a big difference – a really big difference – in the amount of money available to satisfy a claim. If a policyholder or claimants can turn one occurrence into two or more, they have performed insurance alchemy.

I was happy to see that a number of occurrences decision came up last month, and an interesting one at that. And it involves kabobs. I love a good kabob.

At issue in Travelers Casualty Ins. Co. v. Mediterranean Grill & Kabob, Inc., No. 20-40 (W.D. Tex. Nov. 4, 2020) was coverage for nearly 200 cases of food poisoning, from salmonella, allegedly contracted at Pasha Mediterranean Grill in San Antonio.

The food poisoning led to seven lawsuits, all alleging that Pasha was negligent in the manufacture and preparation of food and such negligence was the proximate cause of the food poisoning.

Pasha was insured under a commercial general liability policy issued by Travelers. The limit of liability was $1 million each occurrence and $2 million. This is all you need to know that number of occurrences was going to be a big issue. It’s the difference between there being up to $1 million available for all of the claims or $2 million.

Travelers, treating all of the claims as arising out of a single occurrence, offered to pay $1 million is settlement. However, this was rejected by Pasha. It argued that each food poisoning was a separate occurrence. Therefore, for the remaining 124 claimants, Travelers must pay over $1.5 million.

As Pasha saw it, there were a multitude of causes of the food poisoning. Pasha pointed to pauses or interruptions in its business operations – opening and closing -- during the poisoning, as well as the preparation of different batches of food. A report of the San Antonio Health District was inconclusive as to the cause of the outbreak, but pointed to multiple contributing factors, such as the presence of unclean utensils and improper hand washing.

But despite all this, the court had little trouble concluding that, based on Texas’s “cause test” for determining number of occurrences, there was only one at issue:

“[O]nly one cause gave rise to Pasha’s liability, and that is Pasha’s allegedly contaminated food. Thus, under Texas’s ‘cause’ analysis it appears there was a single, continuous event that both allegedly caused the injuries in the underlying suits, and gave rise to Pasha's liability. Therefore, the food poisonings were a single ‘occurrence’ under the policy. Importantly, this conclusion comports with the language of the policy. Included in the definition of occurrence is ‘continuous or repeated exposure to the same general harmful conditions.’ The allegedly harmful condition here was food that had been contaminated with salmonella bacteria and, therefore increased the risk of illness and possibly death. Individual patrons were continuously exposed to this alleged condition while they ate Pasha’s food, and patrons, as a group, were repeatedly exposed to it. . . . There is no allegation or evidence that Pasha returned to preparing food safely, allowed the food to become contaminated again, and then, because of Pasha’s negligence, exposed more patrons to contaminated food. Thus, Pasha’s purported negligence is alleged to have caused one uninterrupted chain of events, meaning there was but one proximate, uninterrupted and continuing cause of the contamination for which it may be liable.”

It’s an old story: not enough limits? Find more occurrences.

|

| |

| |

| |

|

|

|

|

Vol. 9 - Issue 8

December 7, 2020

Insurer Fails To Provide Notice Of ROR To Claimant And Waives Strong Defense: No, This Was Not A New York Case

Guest Author

Margo Meta

White And Williams, LLP

|

|

|

| |

It is well-know that, under New York statutory law, an insurer that fails, in a timely manner, to advise a claimant of a disclaimer to its insured – for a bodily injury claim – can waive certain coverage defenses. This is a general statement of an aspect of New York Insurance Law § 3420.

In my experience, it is less-known that Virginia has a similar statutory provision – and not limited to bodily injury claims. And, as last week’s decision in National Casualty Ins. Co. v. Solomon, No. 20-699 (D.D.C. Nov. 24, 2020) teaches, an insurer’s failure to comply can lead to a harsh result. Here, on account of not providing notice to a claimant of a reservation of rights, National Casualty lost the ability to disclaim coverage, under a claim-made policy, where notice was late by 12 years. Not 12 months. Years. Insurers don’t lose too many “claims made” cases with facts like this. But enter Va. Code § 38.2-2226.

In Solomon, the court addressed coverage under the following circumstances.

In December 1999, Atlanta Channel Company, Inc.’s former attorney, Henry Solomon, allegedly committed legal malpractice following the submission of a defective application for a special broadcasting license with the Federal Communications Commission. Solomon did not report the allegedly defective application to National Casualty until November 2012. National Casualty sent Solomon a series of reservation of rights letters, in 2015, 2016 and 2019, stating that it would defend him in the malpractice action filed by Atlanta Channel, but it would not indemnify him for any judgment or settlement. This on account of his failure to provide timely notice of circumstances which could give rise to a claim. Significantly, National Casualty failed to copy Atlanta Channel on the letters.

Atlanta Channel did not receive copies any of the letters until late 2019. The company argued that National Casualty’s failure to copy it on the letters violated Virginia Code § 38.2-2226, and that as a result, National Casualty had waived its right to disclaim coverage to Solomon for his failure to comply with the policy’s notice provisions.

As cited by the court, Virginia Code § 38.2-2226 provides:

“Whenever any insurer on a policy of liability insurance discovers a breach of the terms or conditions of the insurance contract by the insured, the insurer shall notify the claimant or the claimant’s counsel of the breach. Notification shall be given within forty-five days after discovery by the insurer of the breach or of the claim, whichever is later. Whenever, on account of such breach, a nonwaiver of rights agreement is executed by the insurer and the insured, or a reservation of rights letter is sent by the insurer to the insured, notice of such action shall be given to the claimant or the claimant's counsel within forty-five days after that agreement is executed or the letter is sent, or after notice of the claim is received, whichever is later. Failure to give the notice within forty-five days will result in a waiver of the defense based on such breach to the extent of the claim by operation of law.”

While not cited by the court, § 38.2-2226 also provides:

“Notwithstanding the provisions of this section, in any claim in which a civil action has been filed by the claimant, the insurer shall give notice of reservation of rights in writing to the claimant, or if the claimant is represented by counsel, to claimant's counsel not less than thirty days prior to the date set for trial of the matter. The court, upon motion of the insurer and for good cause shown, may allow such notice to be given fewer than thirty days prior to the trial date. Failure to give the notice within thirty days of the trial date, or such shorter period as the court may have allowed, shall result in a waiver of the defense based on such breach to the extent of the claim by operation of law.”

The bulk of the court’s opinion addressed whether Virginia Code § 38.2-2226 is procedural or substantive in nature and its applicability to the clam.

After determining that the provision was substantive, and applicable, the court had no trouble quickly reaching a conclusion: National Casualty’s failure to provide timely notice of Solomon’s breach to Atlanta Channel was a violation of § 38.2-2226 and mandated a determination that National Casualty could not disclaim coverage for any judgment entered in favor of Atlanta Channel, against Solomon, in the malpractice lawsuit.

Of note, Va. Code § 38.2-2226 does not apply when an insurer is advising its insured of a defense, based on a claim not satisfying the requisite terms for coverage under a policy. This point was made not long ago by the Fourth Circuit in Gateway Residences at Exch., LLC v. Ill. Union Ins. Co., 917 F.3d 269, 274 (4th Cir. 2019): “The statute’s text makes two things clear: it covers denials based on the insured’s ‘breach’ of the terms and conditions of the policy and applies to arguments properly characterized as waivable ‘defenses.’ Courts have therefore rightly held that the statute (or its precursor) doesn’t apply when an insurer denies coverage because the claim falls outside the scope of policy coverage. (citations omitted) The argument that a claim is outside the scope of coverage is not about an insured’s ‘breach’ of contract. A ‘breach’ assumes a legal duty on the insured’s part, but the insured obviously has no legal duty to incur covered claims. Likewise, a denial based on scope of coverage is not a ‘defense,’ as a ‘defense’ presupposes the insurer’s existing obligation to provide coverage.”

If you’re going to Virginia, don’t miss Monticello, Mt. Vernon or Va. Code § 38.2-2226.

|

| |

| |

| |

|

|

|

|

| |

|

|

Arizona Federal Court Concludes That Covid-19 Is Not “Traditional Environmental Pollution”

In a decision that is hardly a finger in the socket, the court in London Bridge Resort LLC v. Ill. Union Ins. Co., No. 20-08109 (D. Ariz. Dec. 4, 2020) held that Covid-19 is not “traditional environmental pollution.” The issue arose in the context of a coverage grant in a pollution liability policy, but the court’s analysis was based on Arizona case law addressing the pollution exclusion and its breadth: “The Court has little trouble concluding that no plausible interpretation of ‘traditional environmental pollution’ includes a virus outbreak. . . .Plaintiff argues COVID-19 constitutes traditional environmental pollution because different government agencies include ‘virus’ in the definition of certain contaminants and pollutants. However, a virus being considered a ‘contaminant’ or ‘pollutant’ in certain instances does not render a COVID-19 outbreak ‘traditional environmental pollution.’ As the Keggi court explained, ‘[m]any courts that have considered the purpose of the standard pollution exclusion clause have concluded that the clause is intended to preclude coverage for environmental pollution, not for ‘all contact with substances that can be classified as pollutants.’ Furthermore, a virus outbreak does not closely resemble the enumerated examples provided in the Policy's definition.”

Citing Marge Simpson, Court Finds No Coverage For Covid-19 Business Interruption

In Toppers Salon & Health Spa, Inc. v. Travelers Prop. Cas., No. 20-03342 (E.D. Pa. Nov. 30, 2020), the Eastern District of Pennsylvania held that a spa was not entitled to coverage for business income losses on account of Covid-19: the policy’s Virus Exclusion applied and the spa did not sustain physical damage. In doing so, the court somehow managed to work in a reference to Marge Simpson: “There was a time not so long ago when someone seeking an escape from day-to-day pressures could count on a trip to a spa, like Marge Simpson at Rancho Relaxo. But like so many other things, the Covid-19 pandemic has upended that norm. Like so many other businesses, state and local governments have at times issued orders closing spas to prevent the virus’s spread. Those businesses have, in turn, looked to recoup their losses from insurers. This is one such case.”

Different Choice Of Law Analysis For Bad Faith

When it comes to a choice of law analysis for a coverage dispute, the state where the policy was issued is often a strong factor in the outcome – usually more so than where the claim arose or the underlying litigation is pending. But, as demonstrated by the court in Charter Realty Group v. James River Ins. Co., No. 20-22768 (S.D. Fla. Oct. 19, 2020), that may not be the case when choice of law is being determined for a bad faith claim. [In a recent issue of CO I addressed another case that reached this same conclusion]. The Charter Realty Group had this to say about choice of law for bad faith: “However, in bad faith failure to settle claims, the location of the insured risk should be given less weight in the choice of law analysis, and the location of the underlying litigation and the state whose laws were applied should bear heavier consideration. . . . Here, several factors favor applying Florida’s rule. The insured property is in Florida, the tragic shooting occurred in Florida, the settlement on behalf of MPG took place in Florida, the Judgment Creditors are citizens of Florida, and the Underlying Action was litigated in Florida. Critically, because Charter has brought a bad faith failure to settle claim, we give more weight to the fact that the Underlying Action occurred in Florida and applied Florida law.”

|

| |

|

|

|

| |

| |

|

|

|

|

|

|

|

|

|