|

|

|

|

|

| |

|

Vol. 9 - Issue 7

October 30, 2020

|

|

|

|

|

|

| |

October 6th was the 20th anniversary of the first episode of “CSI: Crime Scene Investigation.”

To mark the occasion, I did an interview, for the ABA Journal website, with Donald Shelton, a retired Michigan judge of 24 years, who is a leading researcher on the “CSI effect.”

Shelton’s extensive research has concluded that it is a myth that jurors come to court, expecting to see scientific evidence on account of watching CSI, and then wrongfully acquit because of the lack of such evidence.

I hope you can check it out here. |

| |

| |

|

|

|

Vol. 9 - Issue 7

October 30, 2020

Long Wait In A Doctor’s Waiting Room Leads To Interesting Coverage Decision

|

|

|

|

|

| |

| As I mentioned in the last issue, Randy Spencer has been in a slump. His last few columns just haven’t been very good. That’s being kind. I put him on probation. Unless things improved, I told him, I’d have to look for a replacement. |

*** |

| |

Philip Metcalf was a cardiologist in San Antonio. While he was known for being one of the best in the country, he was also obnoxiously boastful. Adding to his patients’ dislike -- Metcalf was always extraordinarily late for appointments. An appointment with Metcalf often required a three-hour wait. His overbooking was extraordinary and he then spent twenty minutes with every patient sharing stories of his most recent trip to this or that private island – where he told about reeling in an eleven foot marlin. While in the waiting room, Metcalf’s patients were treated to a sign showing the latest tally of the number of lives that he had saved. It resembled a billboard outside of McDonalds, announcing how many burgers the fast food giant had served. But Metcalf’s patients put up with it all because he really was one of the best of the best cardiologists.

James Roberts was a 65-year-old mergers and acquisitions lawyer in San Antonio. He needed a cardiologist. He knew all about Dr. Metcalf’s reputation as a superb physician. But he also knew about Metcalf’s other reputation. Nonetheless, Roberts made an appointment to see Metcalf on October 9, 2019 and 1:30 P.M. He knew what was in store, but told himself that he would bring a book and that the wait would be worth it.

Roberts arrived at Metcalf’s office at 1:20 P.M. on the day of his appointment and was greeted by the receptionist. He filled out the new patient forms and was told to have a seat and that Dr. Metcalf would be with him shortly.

The wait to see Dr. Metcalf was dramatically longer than Roberts expected. He was finally called back to an examination room at 6 P.M. Roberts’s blood was boiling. Metcalf walked in, introduced himself and informed Roberts that he would need to re-schedule. The stone crabs that Metcalf had had shipped in, from legendary Joe’s in Miami Beach, had arrived earlier than expected. Metcalf needed to get home to eat them while they were at their peak of freshness. With that, Metcalf turned and left, without even saying good-bye. The entire encounter was less than 60 seconds.

Roberts shared this story the next day with a colleague and the two agreed that Metcalf needed to be taught a lesson. They drafted a complaint against him, in small claims court, for breach of contract, alleging that Metcalf and Roberts had an oral contract for medical services. The complaint alleged that Metcalf breached the contract by making Roberts wait four-plus hours and then cancelling the appointment. The complaint stated that Roberts’s hourly rate, as a prominent M&A lawyer, was $1,100. Roberts sought damages of $4,400 for the time that he lost being taken away from his office. Roberts contemplated adding a misrepresentation count against the receptionist, for stating that Metcalf would be with him “shortly,” when she knew that that would not the case. But he decided that working for Metcalf was punishment enough.

Metcalf, incensed by the suit – “how dare he,” he told colleagues-- sent it to his insurer, Crockett Property & Casualty Insurance Co. He had a professional liability policy and commercial general liability policy with the company.

Crockett P&C disclaimed coverage under Metcalf’s professional liability policy – “how dare they,” he told colleagues -- on the basis that the suit alleged a fee dispute, which the insurer stated was not a “professional medical service,” as required to trigger coverage. Metcalf did not challenge this.

The company also disclaimed coverage under Metcalf’s commercial general liability policy on the basis that the suit did not allege an “occurrence,” nor seek damages because of “bodily injury,” “property damage” or “personal and advertising injury.”

Metcalf was forced to hire counsel to defend Roberts’s suit. He filed a declaratory judgment action against Crockett Property & Casualty, vowing to take the case all the way to the United States Supreme Court. Metcalf alleged that coverage was owed, under the commercial general liability policy, on the basis that the suit alleged an “occurrence” and sought damages because of “property damage.”

The court in Metcalf v. Crockett Property & Casualty Insurance Co., No. 19-1398 (Tex. Dist. Ct., Bexar Cty., Oct. 2, 2020) agreed with Metcalf, at least for purposes of a duty to defend.

First, the court concluded that the suit’s allegation, that Roberts was seeking damages for “the time that he lost being taken away from his office,” may have been alleging the loss of use of his office -- and the office was tangible property that had not been physically injured. Thus, the suit was alleging “property damage,” as that term is defined in the policy. The court in fact seemed skeptical of this premise for affording coverage, but noted that it was constrained in its consideration by the allegations in the complaint. What the complaint said controlled. Thus, the court concluded that, at least for a duty to defend, the suit alleged “property damage.”

The court also held, again, based on a duty to defend standard, that the “property damage” may have been caused by an “occurrence.” While the court stated that cancellation of an appointment is ordinarily intentional, and not an “occurrence” -- defined as an accident -- that may not have been the case here. Rather, if the cancellation was based on the earlier than expected arrival of Metcalf’s order from Joe’s Stone Crabs, that was something that Metcalf had no control over. Therefore, as the court saw it, the cancellation of the appointment may have been caused by an accident.

|

| |

That’s my time. I’m Randy Spencer. Contact Randy Spencer at

Randy.Spencer@coverageopinions.info |

|

| |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Vol. 9 - Issue 7

October 30, 2020

Encore: Randy Spencer’s Open Mic

Halloween Candy Lawsuit Leads To Coverage Litigation

|

|

|

|

|

|

| |

Halloween, and, in particular, candy, was at the heart of a recent fascinating underlying and companion coverage case.

On October 31, 2015, Sanford Grigsby, like millions of others, passed out candy to the ghosts and goblins who knocked on his door in suburban Cleveland. But there was something about a stop at Grigsby’s house that differed from most. Grigsby was a dentist. So, in addition to Gobstoppers, his trick or treaters each received a small zip-lock bag containing a toothbrush and travel-size tube of toothpaste. The toothbrush was imprinted with Sanford Grigsby, D.D.S. and his office phone number. Inside the bag was a folded piece of 8 ½ x 11 paper, with Dr. Grigsby’s offer letterhead, and the text: “Happy Halloween! Enjoy your candy and then come see Dr. Sandy!” Grigsby knew it made him look like Scrooge – but he believed in never missing a chance to promote good dental health. Plus, thanks to the overzealous marketing tactics of toothpaste manufacturers, he had 500 travel-size tubes of toothpaste in his office that he was desperate to unload.

Skip McMaster, age 10, and dressed as Harry Potter, knocked on Dr. Grigsby’s door and was handed Gobstoppers and one of Grigsby’s toothbrush/toothpaste bags.

Two days later, Skip’s father, Melvin, ate Skip’s Gobstoppers (with Skip’s permission). Melvin bit down on the candy and cracked two crowns in his mouth. The cost to remake them was $6,000 plus plain and suffering and hours of time out of Melvin’s life to deal with the numerous dentist’s office visits.

Melvin decided to file suit against Dr. Grigsby. It was easy to identify Grigsby as the Gobstopper-ghoul. Skip did not like Gobstoppers and had made a note to himself to avoid Grigsby’s house the following year. And Melvin was willing to testify that Skip had received no other Gobstoppers in his candy bag. Product ID was satisfied.

Melvin had a difficult time finding a lawyer to take the case. Several turned him down on the basis that, as a matter of law, he could not maintain an action against Dr. Grigsby. As these lawyers saw it, Grigsby simply had no liability for the incident. Prepared to give up, Melvin went to see one last lawyer. This time the attorney saw a cause of action – strict liability. As for the law’s requirement that Dr. Grigsby be a manufacturer, retailer or distributor of the product, they would argue that he was a distributor. By including the toothbrush with his name and office phone number, plus the note stating “Enjoy your candy and then come see Dr. Sandy!,” Grigsby was in fact selling Gobstoppers, through a deferred payment scheme -- fees for dental services arising out of Gobstopper-caused cavities.

Melvin McMaster filed suit against Sanford Grigsby, D.D.S. in state court in Cuyahoga County, Ohio. He sought payment of $6,000 for the replacement of the two crowns and damages for pain and suffering.

Grigsby did not have a homeowner’s policy, with liability insurance, as he was renting his house and also did not have a renter’s policy. So Grigsby tendered the McMaster suit to his dental malpractice insurer – Molar Property & Casualty Ins. Co. Molar declined to defend Grigsby on the basis that the policy’s insuring agreement was not satisfied. Specifically, as Molar saw it, the complaint did not allege that McMaster’s injury was caused by Grigsby “arising out of the performance of dental services.”

With nowhere to turn, Grigsby retained a lawyer and filed the Ohio equivalent of a 12(b)(6) motion to dismiss for failure to state a claim. The court, in Melvin McMaster vs. Sanford Grigsby, D.D.S., No. 17-2145 (Cuyahoga Cty. Jan. 3, 2017) acknowledged that McMaster’s cause of action was novel. However, based on the high burden required for granting a 12(b)(6) motion, the court could not say that McMaster had no claim. The court explained: “If all Dr. Grigsby had done was given away toothpaste and a toothbrush, even with his name and office phone number, this court would not hesitate to conclude that Dr. Grigsby was simply a concerned dentist and not a distributor of Gobstoppers for purposes of the state’s strict liability law. But Grigsby went further. This court cannot say, at this preliminary stage, that Dr. Grigsby, having included the note inviting people to see him, after getting a cavity from the Gobstoppers, was not selling the candy, through the deferred payment scheme alleged by plaintiff.” Id. at 3.

Grigsby, now faced with the prospect of the litigation going forward, and a six-figure estimate for defense costs, settled the action for $22,500.

Grigsby, now spitting mad, filed suit against Molar P&C, seeing recovery of his $9,000 in defense costs, the $22,500 settlement and damages for bad faith. Molar filed a motion for summary judgment, arguing that McMaster’s injury was not caused by Grigsby “arising out of the performance of dental services.” Grigsby cross-moved.

Brace yourself. The court, in Grigsby v. Molar Property & Casualty Ins. Co., No. 18-1387 (Cuyahoga Cty. Sept. 5, 2018) held that McMaster’s injury was caused by Grigsby “arising out of the performance of dental services.” The court explained: “By giving out a toothbrush and toothpaste to the trick or treaters, Dr. Grigsby was acknowledging that eating candy can be hazardous to a child’s teeth. He was promoting good dental hygiene to address the risk. Based on the broad meaning given to the term ‘arising out of’ as used in insurance policies, and this court’s mandate to interpret a coverage grant broadly, this court holds that Mr. McMaster’s injury was arising out of the performance of Dr. Grigsby’s dental services.”

Scary decision.

The molar of the story: It’s safer to give out Peeps.

|

That’s my time. I’m Randy Spencer. Contact Randy Spencer at

Randy.Spencer@coverageopinions.info |

|

| |

|

| |

|

|

|

|

Vol. 9 - Issue 7

October 30, 2020

|

|

|

|

|

|

| |

I am excited to report that this issue marks the 8th Anniversary of Coverage Opinions. That’s bronze if you are thinking about sending a gift.

Of course, there could be no eight-year anniversary to mark if it were not for you – the dear Coverage Opinions reader. I can’t thank CO readers enough for taking the time to do so, despite having such busy schedules and being inundated with other newsletters, and the like, competing for their time.

I appreciate all of the reader email that I receive – mostly positive, but sometimes taking me to task for something I said or didn’t say -- and that’s fine too. And people sometimes kindly send cases that they think I’ll enjoy or that might merit a write-up.

I am also lucky for the friendships that I have made with CO readers who reached out about something they saw.

Putting together CO is an extremely time-consuming endeavor. Hearing from people, that they read it and enjoy it, provides the mojo that I need to keep it going.

Again, thank you for your loyal readership.

-- Randy

maniloff@coverageopinions.info

|

| |

| |

|

|

|

|

Vol. 9 - Issue 7

October 30, 2020

My Wall Street Journal Op-Ed: 150th Anniversary Of A Legendary Closing Argument

Even Cat People Will Love This

|

|

|

| |

September 23rd was the 150th anniversary of one of the most famous and enduring closing arguments in history: George Vest’s “A Tribute to a Dog” delivered in a Missouri courtroom. It is a masterpiece of advocacy that has been enjoyed by lawyers and dog lovers for years.

I had the fun of commemorating Vest’s milestone anniversary by publishing an Op-ed about it in The Wall Street Journal.

I hope you can check it out here: https://www.coverageopinions.info/WSJ1TributetoaDog.pdf

|

| |

|

|

|

|

Vol. 9 - Issue 7

October 30, 2020

Contest: The Most Interesting Insurance Man Or Woman In The World

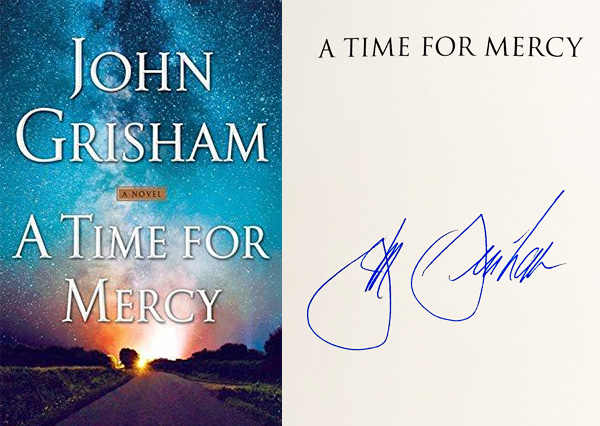

Win An Autographed Copy Of John Grisham’s Just-Released Book: “A Time For Mercy”

Most Popular Coverage Opinions Contest Ever!

|

|

|

| |

|

| |

|

| |

I have an autographed copy of “A Time For Mercy,” John Grisham’s just-released book [currently #1 on The New York Times best sellers list for fiction]. The story features the return of Jake Brigance, the lawyer who starred in Grisham’s first book “A Time to Kill” and then “Sycamore Row.”

I’d love to give it away as a prize in a Coverage Opinions contest.

Way back in November 2013 I did a column about the “Most Interesting Insurance Man in the World.” It was a take-off on the suave, handsome, smoking jacket-wearing bearded man in the Dos Equis beer commercials. At the end he provides his trademark line: stay thirsty, my friend.

In that column I explained that, if there were a “Most Interesting Insurance Man in the World,” these are some of the things he would do:

- He doesn’t consider notice to be late if it was only fashionably late.

- He thinks is would be tacky to seek reimbursement of defense costs.

- He goes to a bar to investigate a liquor liability claim and buys everyone a drink.

- Every party at a mediation wants him to be in their breakout room.

- He describes a duty to defend as a pleasure to defend.

- He disclaims coverage under the pollution exclusion and then goes to the site and cleans it up himself.

- His choice of law problem is between France and Monaco.

Contest: Tell me something insurance-related that the Most Interesting Insurance Woman or Man in the World would say or do.

Best answer will win the autographed copy of “A Time For Mercy.” And honorable mentions will get a Coverage Opinions pen. Better than nothing. Well, maybe. [And, as noted above, in light of the popularity of this contest, I am going to dig up a bunch a copies of Insurance Key Issues to give away as additional prizes.]

Deadline to enter – November 13. Send as many entries as you’d like.

Please note that there is no “link” to enter, as some people ask. Just reply to this email. CO is a one man band, low-budget operation. And you don’t pay for this fine publication, I’ll remind you. So there is nothing in the budget for a fancy, hi-tech contest-entry feature.

No purchase necessary. Employees of Coverage Opinions are not eligible. Void where prohibited (I love saying that).

|

| |

|

|

|

|

Vol. 9 - Issue 7

October 30, 2020

New State Law Accidentally Eliminates The Four Corners Rule

|

|

|

| |

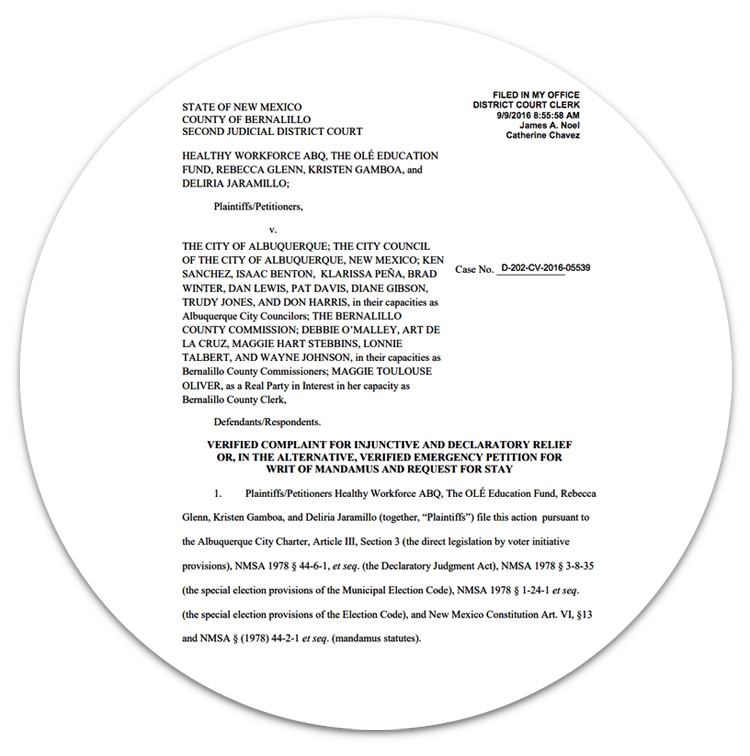

With all of the Covid-19 distractions these days it went largely unreported that New Mexico, in an effort to celebrate being the flying saucer capital of the nation, passed a new rule of civil procedure requiring that all complaints, filed in its District Court, must be on circular paper.

Lawyers interviewed about the change were generally in favor of it. As for needing to buy special printers that can handle circular paper, many said that, after working from home for so long, they didn’t know what a printer was.

But a coverage lawyer was quick to point out an unintended consequence of the new rule – the elimination of the “four corners” standard for purposes of determining an insurer’s duty to defend.

|

| |

|

[Note: I am aware that New Mexico’s duty to defend rule in fact allows for consideration of extrinsic evidence. But, if I said that, this bit wouldn’t work. So I took poetic-legal license. New Mexico readers (if there are any): no need to send an email pointing this out.] |

| |

|

|

|

|

Vol. 9 - Issue 7

October 30, 2020

|

|

|

|

|

|

| |

Who knows how Halloween will work this year for wanna-be Power Rangers, princesses and Hermione Grangers in search of candy But it’s still Halloween. My house is decorated – inside and out – and my daughter and I made a scarecrow (pictured here). Sure, it’s not going to win any scarecrow making contents, but it’s not bad for beginners – who complained the entire time that the hay was making their noses run.

Featured above is the Coverage Opinion pumpkin that my wife -- a very good pumpkin carver – produced a couple of years ago.

I have long been a fan of how the law and Halloween coincide. Yes, they do. Here are a couple of older pieces that I’ve published in USA Today and The Wall Street Journal on this interesting interaction.

https://www.coverageopinions.info/USAToday.pdf

https://www.coverageopinions.info/WallstreetHalloween2018.pdf |

| |

|

|

|

|

|

Vol. 9 - Issue 7

October 30, 2020

Covid-19 Coverage Litigation Scorecard

|

|

|

| |

When the first few Covid-19 coverage litigation decisions came down it was easy to keep track of them. Then an avalanche of decisions came tumbling down and the task became much more difficult. And that is only going to continue and the challenge grow. For those looking for effortless, one-stop shopping, to get the latest rundown on these judicial decisions, there is no better place than the “Covid Coverage Litigation Tracker,” run by Penn Law School’s Professor Tom Baker.

The Litigation Tracker started out keeping score of the Covid-19 coverage litigation filings, setting out a slew of statistics, including the number of filings on a weekly basis, types of claims being asserted, class action status, law firms bringing the cases, insurance companies named as defendants, the policy forms at issue and so on and so on.

Then, as judicial decisions were issued, the Litigation Tracker turned its attention to keeping a running list of them and their outcomes. To see the Covid-19 coverage litigation scorecard, check out this page on the University of Pennsylvania Law School’s “Covid Coverage Litigation Tracker:”

https://cclt.law.upenn.edu/judicial-rulings/

|

| |

|

|

|

|

Vol. 9 - Issue 7

October 30, 2020

They’re Back: Coverage Opinions Pens!! Free For The Asking

|

|

|

| |

|

| |

I have some new Coverage Opinions pens. More than once users of the CO pen have described the experience of owning one as life-altering. [Truth be told – they write really well and are comfortable to hold.]

I’d be happy to send a Coverage Opinions pen to the first 10 people who ask for one. If you like Coverage Opinions, what could be better than having CO swag.

|

| |

|

|

|

|

Vol. 9 - Issue 7

October 30, 2020

Thank You To Those Who Attended The “Coverage Opinions Greatest Hits” Virtual Presentation

|

|

|

| |

Thank you to all who attended my session on October 22nd at the 14th Annual White and Williams Coverage College. I presented “Coverage Opinions Greatest Hits.”

I’m very selective in the cases that I choose to address in CO. They generally need to provide a lesson for insurers or have the potential to influence other courts or have something novel about them. The overarching test is this -- I ask myself: Will the reader find this case interesting or useful?

In this W&W Coverage College session, I reviewed some of the best cases, over the past several years from Coverage Opinions, that satisfied this selection criteria. The cases were wide-ranging and included some of the most unique addressing all manner of issues, such as the following:

- Most Ridiculous Argument Ever Made For Coverage – Will Never Be Topped

- Solving The Dispute Over The Rate To Pay Independent Counsel

- One Insurer Settles A Claim. Can That Fact Be Used By A Different Insured, Against A Different (Non-Settling) Insurer, As Evidence Of Bad Faith?

- Insurer Has Right To Settle. But Insured Refuses To Sign The Settlement Agreement: Now What?

- Insurer Excludes Products Coverage And Pays $1,000,000 For Products Claim

- Coverage Counsel Authors Insurer’s Letters -- Leads To Waiver of Attorney-Client Privilege

- Choice of Law: Is the Answer Different for Bad Faith?

- and lots more….

The presentation was well-received. I’d like to reprise it one of these days as a stand-alone webinar.

Thanks again to all who attended.

|

| |

|

|

|

|

Vol. 9 - Issue 7

October 30, 2020

I’ve Always Wanted To Write This – Now I Have

|

|

|

| |

[This page left intentionally blank]

|

| |

|

|

|

| |

|

Vol. 9 - Issue 7

October 30, 2020

Perhaps The Most Blatant Example Of A Plaintiff “Pleading Into Coverage” That I’ve Ever Seen

|

|

|

| |

Courts tasked with addressing whether an insurer has a duty to defend are often required to consider only the allegations in the plaintiff’s complaint. Whatever the complaint says goes, the rule often dictates.

Knowing that the insurer must wear blinders when examining the complaint can give plaintiffs’ attorneys a powerful tool. Hoping to tap a liability insurance policy for any settlement or judgment, plaintiff’s attorneys have the opportunity to draft their complaint in a manner that is more likely to trigger an insurer-provided defense. Triggering a defense, even if under a reservation of rights, is the first step to reaching an insurer’s potential indemnity obligation -- or sometimes desire to settle. The fact is that, in most cases, the path of least resistance, for a plaintiff to recover money, runs through an insurance company.

There are times when a plaintiff’s effort to draft a complaint designed to trigger a defense – sometimes referred to as “pleading into coverage” – is so fantastical that courts do not let it stand. This is so, no matter what the law says about the duty to defend being tied solely to the allegations in the complaint.

For example, despite the plaintiff saying that the defendant negligently or accidently stabbed him 17 times, does not make it so. Therefore, the court will conclude that the bodily injury was not really caused by an “occurrence” to trigger a defense. In essence, the court is saying to the plaintiff: Look, we see what you are up to, but you can’t fool us. We’re not going to let you get away with it.

But that is not always the case. In fact, sometimes the court says to the plaintiff: “Look, we see what you are up to, but have no choice but to let you get away with it. That’s what happened in Liberty Mutual Fire Ins. Co. v. Lyons, No. 19-1053 (D.N.M. Sept. 25, 2020).

In January 2019, Lindsay Lyons filed a complaint against her father, Michael Lyons, in New Mexico state court. Lindsay alleged that she was “‘repeatedly sexually abused by [Mr. Lyons] at his home in Albuquerque and at his vacation home in Pagosa Springs, Colorado’ from the time she was five years old until her teenage years and that she suffered ‘severe emotional distress and serious mental and economic injuries and damages’ as a result of Mr. Lyons’ actions.”

Michael Lyons sought coverage under a Liberty Mutual homeowner’s policy. There is no specific discussion of what happened but coverage was seemingly denied.

Then, in August 2019, Lindsay filed an amended complaint against Michael, alleging that she was repeatedly sexually molested at his homes. HOWEVER, in the amended complaint, she removed the allegations that it was Michael, specifically, who molested her. Let me say that again. Lindsay’s objective was to sue her father, for alleging molesting her from age five until her teenage years, but she did not specifically mention that he molested her.

Instead, Lindsey alleged that Michael breached a duty of ordinary care, as a homeowner and parent, to keep the premises safe for her use. In other words, she alleged that Michael breached a duty of care to keep the premises safe -- from himself.

Liberty Mutual disclaimed a defense based on several grounds, including no “occurrence.”

The court concluded that this was not a basis to deny a defense. In essence, the court faulted the insurer for reading the two complaints together and treating Michael as the perpetrator for purposes of the amended complaint. However, the court observed:

“[W]hile true that the Original Complaint alleged that Lindsay was ‘sexually abused by [Mr. Lyons]’, the Amended Complaint does not allege that Mr. Lyons was the perpetrator of the sexual abuse. Rather, the Amended Complaint generally and passively alleges that Lindsay “was sexually molested” but identifies no specific perpetrator. Liberty Mutual fails to acknowledge this obvious and material difference between the Original and Amended Complaints. It incorrectly insists that ‘[t]he only acts described in the Complaints are acts of sexual abuse and/or molestation,’ and impermissibly reads into the Amended Complaint a fact that simply is not alleged: that Mr. Lyons sexually molested Lindsay.”

Most importantly, the court noted that, in reaching this duty to defend decision, its hands were tied by the allegations in the complaint. The court even acknowledged the obvious: “[I]t appears to the Court that the Amended Complaint may have been revised as it was ‘for the sole purpose of reaching the insurance policy proceeds[,],’” which the court called “an approach to drafting that [it] has previously found questionable.”

Nonetheless, “taking as true only the facts as pleaded,” the court concluded that “it is possible to read the Amended Complaint as claiming that Mr. Lyons breached a duty he owed to Lindsay by unintentionally and unknowingly—i.e., negligently, or accidentally—allowing her to be molested by a third party in his home.” (emphasis mine). The court concluded that the insurer “wrongly relies on facts not pleaded to support its contention that the Amended Complaint failed to state a claim for an ‘occurrence’ within the Policy’s coverage.”

In the end, the court went on to conclude that the insurer had no duty to defend Michael based on a sexual abuse exclusion.

However, the court’s willingness to allow a plaintiff to so blatantly plead into one aspect of coverage, and even admit that it knew what the plaintiff was doing, is breathtaking.

|

| |

|

|

|

|

Vol. 9 - Issue 7

October 30, 2020

Must Read: Important Primary-Excess Decision: When Excess Disagrees With Primary’s Determination That A Claim Is Covered

|

|

|

| |

When writing a newsletter with an aim to focus on unique cases, there is nothing better than a decision that states, in the first sentence, that the court will be addressing an issue of first impression. When this happens my eyes open wide and I begin to read with the anticipation of a child opening a box on Christmas morning. Unfortunately, sometimes the experience disappoints, like for the youngster who opens Aunt Mildred’s gift and finds a sweater. But usually the decision lives up to the pre-game hype.

This is what happened in Axis Reinsurance Co. v. Northrop Grumman Corp., No. 19-55135 (9th Cir. Sept. 14, 2020), where the court announced in its opening stanza that it was addressing an issue of first impression, at least in its circuit.

In simple terms, Northrop Grumman had a multi-layered Employee Benefit liability insurance program. National Union had the first $15 million. CNA had the next $15 million and AXIS had $15 million on top of that.

There was a settlement of two claims. The first was called the DOL Settlement. National Union determined that it was covered, paid a portion of it and its $15 million policy was now exhausted. CNA also believed that the settlement was covered and paid the remainder. AXIS had no involvement. The DOL Settlement did not reach its layer.

Next was the so-called Grabek Settlement. With National Union now exhausted, CNA paid part of it - $7 million -- with its remaining limits and was exhausted. AXIS was now up to the plate and called upon to pay the remainder of the Grabek Settlement -- $9.7 million.

Here’s the issue. AXIS did not dispute that the Grabek Settlement was covered and paid its portion. However, AXIS believed that the DOL settlement was not covered under the National Union and CNA policies, on the basis that it involved uncovered disgorgement. Therefore, as AXIS saw it, the erroneous decisions by National Union and CNA, to pay the DOL Settlement, resulted in the AXIS policy being prematurely triggered for the Grabek Settlement.

AXIS filed a coverage action against Northrup seeking reimbursement of the amount of its payment of the Grabek Settlement. The District Court found for AXIS, adopting its theory of “improper erosion.”

However, for various reasons, the Ninth Circuit reversed. To the appeals court, the insured should not have to bear “the risk that an excess insurer might disagree with payment decisions made by underlying insurers, and might withhold payment of valid claims it would otherwise cover to compensate itself for the exposure caused by those allegedly improper payments.” An exception exists, the court noted, if the exhaustion was motivated by fraud or bad faith. Not at issue here. Therefore, AXIS could not obtain reimbursement from Northrup of its payment for the Grabek Settlement.

Continuing its public policy-esque conclusion, the court stated: “We agree with Northrop that the district court’s alternative rule—that excess insurers generally may contest the soundness of underlying insurers’ payment decisions—would undermine the confidence of both insureds and insurers in the dependability of settlements, eliminating one of the primary incentives for obtaining insurance in the first place. Furthermore, such a rule would introduce a host of inefficiencies into the insurance industry, with no obvious countervailing benefits to insurers or policyholders.”

The case is certainly a win for policyholders, especially those insured under layered programs, with multiple claims, where the insurers in the tower may not agree with the coverage decisions made on certain ones. This is the scenario that can give rise to arguments, by higher layer insurers, that they were prematurely triggered.

I mention this scenario because the court noted that its rule did not apply where there was a dispute between insurers on a specific claim: “[A]n excess insurer remains free to contest claims submitted to it during the claims adjustment process, even when an underlying insurer has already determined that the same claim falls within the scope of coverage.”

But, despite the win here for insureds, the court also opened the door to insurers having the potential ability to contract for the right to argue improper erosion: “Of course,” the court observed, “excess insurers may contract around this general rule by including specific language in their policies reserving a right to challenge prior payments (so long as the provision is not prohibited by applicable law).”

On that last point, about the provision needing to not be prohibited by applicable law, the court made this observation: “We note that Northrop argued only that the inclusion of ‘improper erosion’ clauses in excess policies would be impractical and unwise, not that they would be per se illegal. Neither party has pointed to any public policy or provision of the California Insurance Code prohibiting such clauses as a matter of law, nor are we aware of any.”

Whether “improper erosion” clauses will be inserted in policies by excess insurers creates beaucoup issues, even if they are legally permissible. That’s an issue for down the road and well beyond the scope of discussion here. Until then, Northrup is an important win for policyholders that use certain types of layered insurance programs.

|

| |

|

|

|

|

Vol. 9 - Issue 7

October 30, 2020

Important Primary-Excess Decision II: Allocation Between Covered And Uncovered Damages:

|

|

|

| |

A frequent topic in CO is allocation between covered and uncovered claims. It is usually in the context of an insurer that must take steps, pre-trial, to secure a verdict that allows for a determination to be made between damages that are covered and those that are not. If an insurer’s failure to do so leads to a “general verdict,” the insurer’s inaction could make it liable for the entirety of such verdict, even it includes some surely uncovered damages.

But allocation between covered and uncovered claims also arises in the context of settlement. And since the vast majority of cases settle, the issue is of paramount importance here.

This is demonstrated in clear terms in Great American Ins. Co. v. Employers Mutual Casualty Co., No. 18-1819 (N.D. Tex. Oct. 15, 2020). The facts at issue are confusing and somewhat difficult to follow. The parties of course understand them but it would take a lot of effort for an outsider to. So let me get to the lesson here without getting bogged-down in this quagmire.

This case involves an insurance-coverage dispute, between two umbrella insurers, arising from a vehicle accident. Gerald Decker was performing tire collection services as an employee of Corona Management and on behalf of Liberty Tire Recycling. His vehicle collided with two other vehicles, killing one driver and injuring another.

Employers Mutual issued an auto policy and commercial umbrella policy to Corona. Great American issued an umbrella policy to Liberty Tire. Liberty Tire also had a primary auto policy from Liberty Mutual.

An underlying law suit resulted in a $7 million settlement agreement. The first $2,668,537.90 of the settlement was funded by the primary insurers. Great American and Employers Mutual disputed their respective liability for the remaining $4,331,462.10. Great American felt compelled to fully fund the remaining amount [although Employers Mutual offered to contribute to the remaining balance on a pro rata basis].

As Decker was performing services for one entity, while an employee of another, there was an issue concerning the extent to which policies applied to various insureds’ direct and vicarious liability. Trust me, it’s really complex and I had zero desire to figure out the nitty gritty.

Here’s the bottom line as the court put it: The settlement agreement contained “no language purporting to segregate covered from uncovered damages. In other words, the settlement agreement in the underlying lawsuit was a complete release[] of liability, but the agreement[] did not allocate the proceeds of the settlement[] to the damages/liabilities they covered.”

More specifically, the court explained that “Great American failed to offer any evidence allocating damages covered by the Employers Mutual umbrella policy (i.e., amounts paid for Liberty Tire’s vicarious liability for Corona or Decker/Corona’s liability) from damages not covered by the Employers Mutual umbrella policy (i.e., amounts paid for Liberty Tire’s direct liability).”

As a result of this failure to allocate the settlement, the court held that “[a]llowing Great American to recover the total value of the Employers Mutual umbrella policy when it cannot produce any evidence as to what Employers Mutual actually owes—if anything—lacks legal authority.”

In reaching this decision, the court rejected, as impermissible conclusory statements, affidavits from a defense attorney for Liberty Tire and Great American’s lead claim adjuster that addressed which claims the settlement encompassed.

Lesson: “While the Court agrees with Great American that allocation doesn’t require ‘mathematical certainty,’ there still needs to be some ‘reasonable, reliable, non-arbitrary basis’ for allocation of covered from uncovered losses.”

Given that settlement agreements often state that they are simply a release of everyone’s liability, with no description provided of what money is being paid for which claims, this decision offers a potentially sharp tool in some cases involving multiple insurers liable for a settlement.

|

| |

|

|

|

|

Vol. 9 - Issue 7

October 30, 2020

That Particular Case: Read This If You Deal With Exclusions (J)(5) and (J)(6)

|

|

|

| |

When it comes to cases involving CGL property damage exclusions (J)(5) and (J)(6), the issue is often whether the term “that particular part” should be interpreted narrowly or broadly. The court in Cincinnati Ins. Co. v. Charlotte Paint Co., No. 18-657 (D.S.C. Oct. 13, 2020) applied it to the specific work that the insured was hired to do and damages caused by the insured’s work. Policyholders will see this as a broad application. The court would describe it as narrow.

I’ll keep this brief and limit it to what’s needed to get to the lesson. Cases involving exclusions (J)(5) and (J)(6) are fact specific and anyone who finds the case to be of interest would need to read it.

Southeastern Wall Systems was hired for the replacement of the stucco cladding on buildings. After Southeastern substantially completed its work, cuts in the Blueskin membrane flashing around certain window openings were discovered. The cuts allegedly damaged the Blueskin waterproof membrane and the wall sheathing—a product called DensGlass. It was alleged that the cuts took place while Southeasten was completing its work. A repair plan involved removal of some stucco around the windows and sliding glass doors, repairing the Blueskin, replacing the stucco, and restoring sealants at all affected locations.

The project’s general contractor filed suit against Southeastern, which sought coverage from Cincinnati Insurance Company. At issue in the coverage action was the potential applicability of exclusions (J)(5) and (J)(6):

This insurance does not apply to:

j. Damage To Property

“Property damage” to:

(5) That particular part of real property on which you . . . are performing operations, if the “property damage” arises out of those operations; or

(6) That particular part of any property that must be restored, repaired, or replaced because “your work” was incorrectly performed on it.

As is often the case, the parties disputed how broadly these exclusions should be interpreted.

CIC contended that exclusion j.(5) was broad enough to include not only the specific work an insured is hired to do, but the area an insured damages while performing such work. The GC, pursuing coverage, saw it differently, focusing on the language “that particular part” in exclusion j.(5) and asserting that “the use of the word ‘particular’ suggests the exclusion should only apply to the smallest unit of division available to the work in question. The ‘particular part’ language is too limiting to allow the entire property to fall within the exclusion.” If so, according to the GC, the exclusion should apply to the component parts of the stucco and nothing else.

The court sided with CIC. As I said, if you are involved with this issue you’ll want to read the case, but here is an excerpt from the court’s explanation of its decision:

“If Southeastern caused the damage, then it happened while Southeastern was performing operations on ‘that particular part’ of the Shipwatch property on which Southeastern was contractually engaged to install stucco. It would strain credulity to divorce the DensGlass and Blueskin from ‘that particular part’ of the property on which Southeastern was performing work. Without the DensGlass there would be no walls on which to install the stucco. The door and window openings were not considered complete without the Blueskin lining being installed to ensure waterproofing. . . . Moreover, CIC is not seeking to apply the "particular part" language to exclude damage to unrelated parts of the entire property and it is hyperbole for Pro-Tec to suggest as much. . . . Some of the case law cited by Pro-Tec shows courts wrestling with delineating the boundaries of the phrase ‘that particular part,’ and the extent to which it limits the scope of the exclusion. But the facts of this case do not require the Court to grapple with those boundaries. This case does not involve alleged damage to the whole property, to neighboring property, or to unrelated building components. Rather, Pro-Tec’s claims in the Underlying Action are for damage to the very building components on which Southeastern performed its stucco installation, and which Southeastern was contractually bound to protect while performing that installation—to wit, the exterior walls, which were composed of DensGlass sheathing and Blueskin borders around door and window openings.”

The court here would tell you that it was not interpreting “that particular part” broadly. Policyholders would likely disagree.

|

| |

|

|

|

|

Vol. 9 - Issue 7

October 30, 2020

Court Provides A Pollution Exclusion Reminder

|

|

|

| |

There was a time when the pollution exclusion was my favorite coverage issue and I discussed it with regularity in CO. While I still follow the issue closely while wearing my coverage lawyer hat, I do not have the same gusto for it when it comes to reporting on decisions here. The problem is that the provision has been litigated to death. So decisions involving novel and interesting issues – what I look for when selecting cases for CO – are hard to come by.

The Texas federal court’s pollution exclusion decision in Canal Indemnity Co. v. Caljet, No. 19-2945 (S.D. Tex. Sept. 8, 2020) is far from unique. But it addresses an important issue, one that comes up less frequently than others and provides a reminder about the clause that is sometimes forgotten.

At issue in Caljet was coverage for Phillips 66, as an additional insured under Auto and CGL policies issued to Coastal Transport Company, for a suit filed against Phillips as follows.

From approximately 1985 to 2016, Elwin Webb worked as a gasoline truck driver for Calzona Tankways and later Coastal Transport Company, Inc. He loaded benzene-containing gasoline at various terminals and loading racks owned and/or operated by the defendants, including Conoco [predecessor to Phillips 66]. A complaint alleged that: “In the course of his work at the defendants’ premises, [Mr. Webb] was exposed to benzene through inhalation and dermal absorption of the defendants’ gasoline. As a direct and proximate result of his exposure to benzene, [Mr. Webb] contracted Myelodysplastic Syndrome (MDS), a benzene-induced blood and bone marrow cancer.” Mr. Webb was diagnosed with MDS in January 2016 and shortly thereafter.

Phillips tendered the suit to Coastal. Canal, Coastal’s insurer, disclaimed coverage to Phillips under both the Auto and CGL policies. Canal filed an action seeking a determination that it did not owe coverage to Phillips.

After addressing some issues surrounding Philips’s status as an additional insured, the court turned to the applicability of the pollution exclusion in the Auto and CGL policies. The court noted that the pollution exclusion generally precluded coverage for bodily injury arising out of the “discharge, dispersal, release or escape” of pollutants.

As Canal saw it, the pollution exclusion applied because the complaint alleged that Mr. Webb suffered bodily injury through exposure to benzene, a pollutant. Eeasy peasy lemon squeezy, right? No.

The court pointed out that the cases cited by Canal – and, as I see it, Texas law supports benzene being a pollutant under the pollution exclusion – involved “the alleged movement of a pollutant.” This, the court noted, is a requirement for the applicability of the pollution.

Here, the “movement requirement” had not been satisfied: “[T]he complaint in the Underlying Lawsuit alleges that Mr. Webb was ‘exposed to benzene through inhalation and dermal absorption of . . . gasoline.’ In other words, even if the Court were to assume that benzene is a pollutant in this situation, the bodily injury was allegedly caused by direct exposure to gasoline, not by the discharge, dispersal, seepage, migration, release, or escape of benzene—as required by the Pollution Exclusions. Therefore, the Pollution Exclusions are inapplicable.”

Again, while far from unique, Caljet provides a reminder about an aspect of the pollution exclusion that is sometimes forgotten.

|

| |

|

|

|

|

Vol. 9 - Issue 7

October 30, 2020

When Bodily Injury At A Water Park Is Not “Because Of ‘Bodily Injury’”

|

|

|

| |

It’s ironic that a claim against an insurance and risk advisor, that it failed to procure adequate insurance for a client, resulted in a coverage action focusing on whether the insurance and risk advisor procured a policy that covered its own alleged negligence.

The story in Bliss Sequoia Ins. & Risk Advisors, Inc. v. Allied Prop. & Cas. Ins. Co., No. 20-00256 (D. Or. Oct. 5, 2020) started this way.

Bliss Sequoia was an insurance and risk advisor. A waterpark client sought professional advice on how to adequately insure itself. After a young boy was seriously injured at the waterpark, and suit was filed, it was determined that Bliss Sequoia had sold the waterpark “woefully inadequate insurance.”

The waterpark sued Bliss Sequoia for misrepresentation and professional negligence. In the injury suit, the waterpark assigned its claims against Bliss Sequoia to the child’s family. The family brought a third-party complaint against Bliss Sequioa.

Here’s the interesting part. The court addressed coverage for Bliss Sequioa under its commercial general liability policy. There is no discussion whether Bliss Sequioa had an insurance agents errors and omissions policy. Maybe it did and the family was trying to get proceeds under both policies. Or maybe it didn’t and this was the only coverage avenue that could be pursued. Also, one wonders about the professional services exclusion was in the CGL policy.

In any event, the policy provided coverage for any sums that the insured becomes legally obligated to pay “because of ‘bodily injury.’”

On its face, you could say that Bliss Sequioa would be legally obligated to pay sums “because of ‘bodily injury.’” The young boy suffered a bodily injury. It was because of that, that Bliss Sequioa was facing potential liability. Indeed, the court noted that the parties agreed that “because of” means “by reason of” or “on account of.”

However, the parties disagreed over “the object of the phrase.” As Bliss Sequoia saw it, it faces liability “by reason of” a child’s injuries. The insurer’s take was that Bliss Sequoia was facing liability not “by reason of” a child’s injuries, but “by reason” of its professional conduct in recommending inadequate insurance coverage.

The court agreed with the insurer, focusing on the “legally obligated” to pay damages aspect of the insuring agreement. The court explained that “the damages sought from Bliss Sequoia are not because of bodily injury but are sought because of Bliss Sequoia’s poor performance of its contract. After all, the complaints allege the boy’s injuries were ‘caused by a lack of adequate lifeguards at the water park at the time of the near drowning of [the boy].’ Bliss Sequoia, however, was not involved in the waterpark’s daily operations. As Bliss Sequoia was not involved in the decisions regarding the appropriate number of lifeguards, it cannot be ‘legally obligated’ to pay damages for any bodily injury caused by inadequate staffing of lifeguards. Instead, Bliss Sequoia’s liability arises solely from its own negligence in providing professional services to the waterpark.”

Not a surprising decision.

|

| |

|

|

|

|

| |

|

|

Case of First Impression: PFAS And The Pollution Exclusion

I believe that last week’s North Carolina federal court decision in Colony Insurance Company v. Buckeye Fire Equipment Company, No. 19-534 (W.D.N.C. Oct. 19, 2020) is the first case addressing the pollution exclusion and the white hot issue of PFAS. Check out this White and Williams Alert on the decision:

New Jersey Legislature Introduces Bill Regarding The Virus Exclusion And Policy Renewals

On October 8th the New Jersey Assembly introduced Bill no. 4805 the includes the following requirement (as well as the same for policies already in effect): “An insurer shall disclose, in a form and manner prescribed by the Commissioner of Banking and Insurance, to any potential purchaser of or any policyholder seeking renewal of a policy insuring against loss or damage to property that includes the loss of use and occupancy and business interruption in this State whether the policy provides coverage for global virus transmission or pandemic coverage.” I’m just a bill, sittin’ on Capitol Hill….

Insurer Being Wrong ≠ Bad Faith. No Brown Bag Required For Policyholders.

Some policyholder lawyers like to maintain that an insurer commits bad faith when its coverage determination is found to have been wrong. But courts frequently show that such hyperventilation is not justified. This conclusion by the court, in Nationwide Mut. Ins. Co. v. Ozark Mt. Poultry, No. 20-CV-5014 (D. Ark. Sept. 21, 2020), resembles many other judicial observations: “Having reviewed the policy language out of which the dispute arises and the ‘controlling authority’ Ozark cites regarding lost profits, the Court cannot reasonably infer ‘dishonest, malicious, or oppressive conduct’ by either Plaintiff in denying coverage. A disagreement as to the facts or the applicable law, even if the insurance company is mistaken in its position, does not rise to the level of bad faith. The Court cannot, even by reasonable inference, conclude that a plausible claim has been made that Nationwide and Great American acted with malice in denying coverage to Ozark under the CGL policies.’”

|

| |

|

|

|

| |

| |

|

|

|

|

|

|

|

|

|