|

|

|

|

|

| |

|

Vol. 11 - Issue 5

October 15, 2022

|

|

|

|

|

|

| |

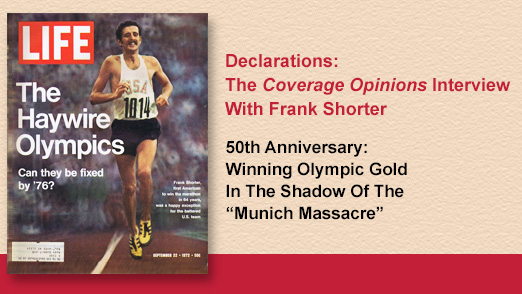

September 10th was the 50th anniversary of Frank Shorter winning the gold medal in the marathon at the Munich Olympics. Five days earlier, 11 members of the Israeli Olympic team were taken hostage by a faction of the PLO and killed. Frank was awakened by the pre-dawn gun fire just 150 yards away in the Olympic village.

In a brief interview for Letsrun.com, I spoke to Frank about his remembrances of the “Munich Massacre” and its impact on his marathon performance.

[Interesting fact - Frank was a student at the University of Florida Law School when he won the gold medal in the marathon.]

I hope you can check it out:

https://www.letsrun.com/news/2022/09/on-50th-anniversary-of-marathon-gold-frank-shorter-reflects-on-impact-of-munich-massacre

|

|

|

|

Vol. 11 - Issue 5

October 15, 2022

Encore: Randy Spencer’s Open Mic

Cheese Wheel: The Strangest Auto Insurer You’ve Ever Seen

|

|

|

|

|

| |

This “Open Mic” Column appeared in the June 4, 2014 issue of Coverage Opinions. |

| |

Some insurance companies have interesting names. And taking notice of them is something that I’ve long done. In fact, the very first “Open Mic” column was about insurance company names. So when I recently came across the Wisconsin Supreme Court’s old decision in Pouwels v. Cheese Makers Mutual Insurance Company, 37 N.W.2d 869 (Wis. 1949) my first reaction was brie whiz that’s a goudumb name for an insurance company. Stilton stranger, the case was about an automobile policy issued by Cheese Makers Mutual.

Cheese Makers Mutual seems like a munsterrible place to asiago when you need automobile insurance. You would think they don’t know jack about cars – except maybe the wheels.

But I thought about it and then the babybel went off. Insuring cheese must have made them board – especially since they were probably all provalone doing it. Queso instead of being bleu they decided to manchego into cars.

I couldn’t find anything on the internet even remotely current about Cheese Makers Mutual. Apparently they couldn’t cut it.

|

That’s my time. I’m Randy Spencer.

|

|

| |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

| |

|

| |

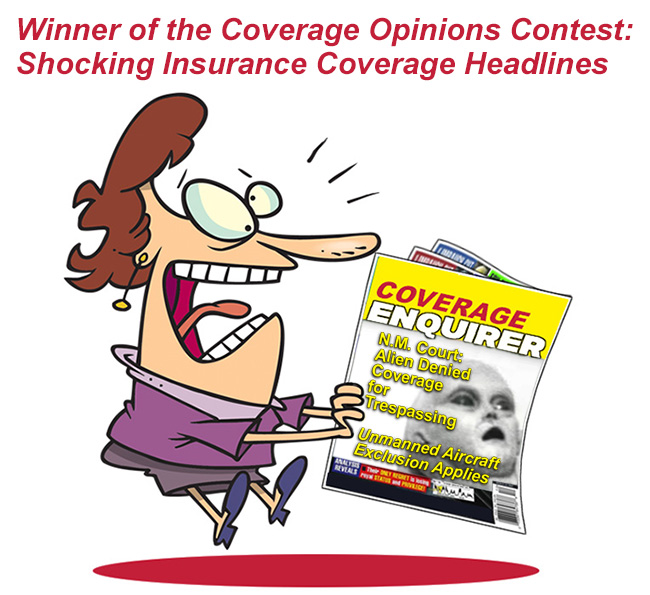

For this first-time contest, I asked readers to send in outlandish insurance coverage headlines that you would see on the cover of the Coverage Enquirer, an insurance coverage supermarket tabloid.

There were some really great entries. The winner is Peter Tyrrell, Assistant Director, MLC General Liability Team, at Hartford. Here is Pete’s very funny and clever headline above. I’ll send Pete an autographed copy of The Boys from Biloxi, John Grisham’s book to be released later this month.

Thank you to everyone who entered.

|

| |

|

|

|

|

|

|

Vol. 11 - Issue 5

October 15, 2022

Coverage Opinions Turns 10!: Thank You Dear Readers

|

|

|

| |

|

| |

I am excited to report that this issue marks the 10th Anniversary of Coverage Opinions!

Here is the thank you that I’ve provided for prior anniversaries. I know it’s redundant, but I can’t think of any other way to say it.

There could be no ten-year anniversary to mark if it were not for you – the dear Coverage Opinions reader. I can’t thank CO readers enough for taking the time to do so, despite having such busy schedules and being inundated with other newsletters, and the like, competing for their time.

I appreciate all of the reader email that I receive – mostly positive, but sometimes taking me to task for something I said or didn’t say -- and that’s fine too. And people sometimes kindly send cases that they think I’ll enjoy or that might merit a write-up.

I am also lucky for the friendships that I have made with CO readers who reached out about something they saw. And, of course, I sincerely appreciate the many client relationships that have grown out of CO.

Putting together Coverage Opinions is an extremely time-consuming endeavor. Hearing from people, that they read it and enjoy it, provides the mojo that I need to keep it going.

Again, thank you for your loyal readership.

-- Randy

maniloff@coverageopinions.info

|

| |

|

|

|

|

|

|

Vol. 11 - Issue 5

October 15, 2022

Take The “Supreme Court Emoji Challenge”

|

|

|

| |

With the new Supreme Court term getting underway, I thought you might like to try my “Supreme Court Emoji Challenge.” Name the landmark SCOTUS case based on it being written in emojis.

I put this together in 2016. Remarkably, it was actually picked up by The Wall Street Journal Law Blog and SCOTUSblog. Answers below.

https://www.coverageopinions.info/TheWllaStreetJournalEmojis.pdf

|

| |

|

|

|

|

|

|

Vol. 11 - Issue 5

October 15, 2022

White And Williams Client Alert Mentioned In Front Page Wall Street Journal Story

|

|

|

| |

About ten days ago I wrote a White and Williams Client Alert about looming litigation over the cause of Hurricane Ian property damage – wind vs. water – on account of the low take-up rate for flood insurance in the badly affected counties. This will cause an incentive, when feasible, for some to argue that damage was caused by wind, which is covered under homeowner’s policies. I sent the Client Alert to CO subscribers.

Anyway, cut to a week later and The Wall Street Journal did a front-page story on the “wind vs. water” issue and mentioned the firm’s Client Alert. It was great to see the things that we produce for clients getting such a wide distribution.

You can check out the WSJ story here:

https://coverageopinions.info/WALLSTREETJOURNAL10-7-22.pdf

You can check out the WW Client Alert here:

https://www.whiteandwilliams.com/resources-alerts-Hurricane-Ian-Discussing-Wind-Water-Disputes

|

| |

|

|

|

|

|

|

Vol. 11 - Issue 5

October 15, 2022

Queen Elizabeth II And Insurance Coverage

|

|

|

| |

With Queen Elizabeth’s death getting ’round the clock news coverage, it was inevitable that, at some point, I would wonder if Her Majesty had ever found her way into a coverage decision. I did. And she has.

In Northwest Steel Erection Co. v. Zurich American Ins. Co., No. 07CV3184 (D. Neb. Jan. 18, 2018), the parties duked it out (no pun intended; well, actually, that was intended) over coverage under a builder’s risk policy. And, ironically, the court called upon the legendary royal for assistance in interpreting the English language. At issue was the following policy provision:

“Any action or proceeding against the Company for recovery of any loss under this policy will not be barred if commenced within (12) twelve months after the OCCURRENCE becomes known to the Named Insured unless a longer period of time is provided by applicable statute.”

The court describe the insurer’s argument as follows:

“Under the plain wording of the policy, an action will not be barred if brought within 12 months after the occurrence becomes known. Zurich’s contention that this language supersedes the applicable statute of limitations, by providing that an action will be barred if not brought within 12 months of a known occurrence, is fallacious.” (emphasis in original).

And here’s where the court crossed the Atlantic for guidance:

“Zurich’s argument is a logical fallacy known as ‘denying the antecedent.’ (For example: If Queen Elizabeth is an American citizen, then she is a human being. Queen Elizabeth is not an American citizen. Therefore, she is not a human being.).”

God bless the Queen, who will forever be in our lives – or at least our pockets -- each time we get one of those pesky Canadian pennies in change.

|

| |

|

|

|

|

|

|

| |

Philadelphia Coverage Lawyer’s Dream: Coverage Case About Soft Pretzels |

|

| |

As a Philadelphia native, my love for soft pretzels knows no bounds. And the finest that the city has to offer, hands down, come from Philadelphia Pretzel Factory. And there is one located just a 9-iron away from the While and Williams office. In fact, the Coverage Opinions website has long included a picture, courtesy of Philadelphia Pretzel Factory, that demonstrates just how knotty some coverage issues can be.

So imagine my surprise, and sheer glee, when I saw a coverage decision involving Philadelphia Pretzel Factory!

At issue in Soft Pretzel Franchise Systems v. Twin City Fire Ins. Co., 22-1277 (E.D. Pa. Aug. 4, 2022) was coverage for the franchisor of Philadelphia Pretzel Factory as an additional insured under a policy issued to a Philadelphia Pretzel Factory franchisee. An employee of the franchisee was injured by an allegedly defective pretzel rolling machine.

The court concluded that the franchisor was not entitled to coverage, as AI status was limited to the franchisor’s role as grantor of the franchise. And that’s not what was alleged in the complaint:

“The claims in the underlying lawsuit against Pretzel Franchise are for strict liability, breach of warranty, and negligence related to injuries suffered by Jackiw and caused by an allegedly defective and unreasonably dangerous pretzel rolling machine. The amended complaint avers that Pretzel Franchise had responsibility for the implementation and enforcement of safety procedures at Philly Pretzel Factory facilities. Included are other allegations that it designed and placed in commerce the defective machine and failed to inspect, repair, and maintain it. The Twin City policy specifically limits coverage for Pretzel Franchise to its role as grantor of the franchise to Pretzel Factory. Jackiw’s pleading does not predicate liability against Pretzel Franchise as a franchisor.”

So Philadelphia Pretzel Factory will not be getting any dough.

|

| |

|

|

|

|

|

|

Vol. 11 - Issue 5

October 15, 2022

Two Policyholder Hail Mary’s For Coverage

|

|

|

| |

I get it. Sometimes policyholders [or underlying plaintiffs] must make arguments in support of coverage that have no real chance of winning. But, if the only way to secure compensation, for injury or damage, is liability insurance coverage, they have no choice but to try. Here are two recent cases in the hail Mary category that predictably ended in favor of the insurer:

Based on Texas law, and the interpretation of the absolute pollution exclusion, a win for the insurer in Peleus Ins. Co. v. Ron Sparks, Inc., No. 21-251 (N.D. Tex. Sept. 8, 2022) was far from a shocker on these facts:

On account of demolishing a building next door to O’Reilly Auto Parts, “the restroom in the O’Reilly store experienced a highly pressurized reverse sewage flow incident that ultimately forcibly projected raw sewage out of the toilet [and] an O’Reilly employee who was inside the restroom at the time, was covered by and directly exposed to the raw sewage, which ultimately led to bacterial infection, sepsis, massive organ failure, resultant neurologic injuries, and other ongoing debilitating injuries and damages.”

***

In B.E. v. Blood, No. 2021AP1377 (Wis. Ct. App. Sept. 15, 2022), the policyholder had a tall task to avoid application of an intentional act exclusion, even with the insurer needing to prove intent to harm: “Erie argues that we can infer intent to injure or harm as a matter of law because harm was substantially certain to result from Blood’s conduct. For the following reasons, we agree. It is manifest that placement of a camera in a person’s bedroom is nearly certain to record that person in various stages of undress and is likely, in some circumstances, to record that person engaging in intimate acts with another. Indeed, Blood was aware of this likelihood because he stated that the point of installing the camera was to monitor E.K.’s sexual activity with B.E. This is recognized in B.E.’s complaint, which alleges that Blood’s conduct was done for Blood’s sexual gratification. As well, E.K.’s complaint alleges that Blood acted ‘with an intentional disregard for the rights of’ E.K. Reasonable persons are aware that the surreptitious recording of a person’s bedroom activity is substantially certain to cause harm by violating that person’s reasonable expectations of privacy.”

|

| |

|

|

|

|

|

|

Vol. 11 - Issue 5

October 15, 2022

Policyholder Head Exploding-Decision On “Insured” Status

|

|

|

| |

There are some cases where the court finds an absence of coverage and policyholder attorneys are apoplectic. I imagine them reading the case, the anger building up and then boom -- their heads explode. The court’s opinion in Discover Property & Casualty Co. v. Blue Bell Creameries, No. 21-487 (W.D. Tex. Aug. 22, 2022) is once such opinion. Attention policyholder attorneys – I warned you. The case involves insured status. This is usually a deadly dull issue, but not here.

At issue in Blue Bell Creameries was coverage for certain officers and directors of the ice cream concern for shareholder suits filed against them. The company experienced a Listeria outbreak in its factories and it resulted in a nationwide recall of its ice cream. [As an aside, ice cream seems like a challenging product to recall.]

The shareholder suit set out, six ways from Sunday, why the officers’ and directors’ conduct, that caused the outbreak, was particularly egregious. This is an important part of the decision, so I’ll set out several of the allegations here in full:

“That suit alleged the Officers and Directors breached their fiduciary duty to Blue Bell when they ‘knowingly disregarded Listeria contamination risk and continued the Company's production and distribution of ice cream,’ and when the Board of Directors ‘willfully failed to exercise its fundamental authority and duty to govern Company management and establish standards and controls for Company compliance.’”

“The Complaint states the Defendant Directors ‘willfully failed to exercise [their] fundamental authority to govern management and institute a system of controls for legal compliance and safe operations of the Company.’ Further, it claims the Directors supported the Officers ‘despite the obvious existential threat to the Company due to management’s failure to operate the Company safely and the blatantly evident lack of adequate oversight and reporting of the known Listeria problems.’” (Id. at 48).

The officers and directors sought coverage for the shareholder suits under the company’s commercial general liability policies.

[I know. Where’s the “bodily injury?” What about no “occurrence?” The court addressed these issues, but I’ll skip them here. It’s not what makes the case interesting.]

The insurers argued that the officers and directors were not “insureds.” Under the policy, “executive officers” and directors are insureds, “but only with respect to their duties as [the corporation’s] officers or directors.”

As the insurers saw it, the only cause of action against the officers and directors was for breach of fiduciary duty, which means that they were not acting “‘with respect to their duties as [Blue Bell's] officers or directors’ when they breached those very duties.”

The court agreed, concluding that the officers and directors were not insureds, as they were not properly carrying out their duties, which was to advance the business of the corporation and not act “in a manner that is antagonistic toward the corporation’s business interests.”

The court rejected the officers’ and directors’ argument that they should be insureds as the shareholder suits did not allege that they were “acting in some other capacity or were pursuing the interests of some other entity.”

I can see this same argument applying to deny routine employees “insured” status, for on-the-job conduct that is alleged to have been wrongful – i.e., job-related (and not assault or other criminal conduct) -- on the basis that their liability is not – as required by a standard CGL policy – “for acts within the scope of their employment by you [named insured] or while performing duties related to the conduct of your [named insured] business.”

|

| |

|

|

|

|

|

|

Vol. 11 - Issue 5

October 15, 2022

Insured Can Bind Excess Insurer To “High-Low” Settlement When The “High” Is In Its Layer

|

|

|

| |

Even when there are no coverage issues – which can add a whole other dynamic – settlements of underlying cases can be challenging. And this can be even more so when the settlement, or potential verdict exposure, can reach an excess layer. And what about when a third layer is potentially in play – which was the situation in North American Elite Ins. Co. v. Menard, Inc., No. 21-1813 (7th Cir. Aug. 4, 2022), a published opinion by Judge Easterbrook.

At issue was coverage for a claim involving injury to a customer of Menards, a home improvement store, who was hit by an employee driving a forklift. Menards had a $2 million self insured retention, a $1 million primary policy with Greenwich Insurance Company and a $25 million umbrella policy on top of the $3 million with North American Elite Ins. Co.

The case went to trial and on the first day the plaintiff offered to settle for $1.985 million, a hair under the SIR. Menards did not respond to it. North American, not surprisingly, urged Menards to settle. Just before the verdict, the parties entered into a high-low settlement – with a range between $500,000 and $6 million. The verdict came in at $13 million. It was reduced to $6 million pursuant to the high-low arrangement. North American paid its $3 million share and then sought to recover this amount from Menards, arguing that the retailer violated duties by rejecting the $1.985 million settlement offer.

The Illinois district court dismissed North American’s claims. The Seventh Circuit affirmed. First, it concluded that Menards’ SIR is not insurance. Therefore, Menards owed no special responsibilities regarding settlement to North American.

The appeals court also approached it from a policy language standpoint. Specifically, the court cited provisions from the Greenwich policy and North American policy to demonstrate how they differ.

Under the North American policy, the insurer “will have no duty to defend any ‘suit’ against [Menard]. [North American] will, however, have the right, but not the duty, to participate in the defense of any ‘suit’ and the investigation of any claim to which this policy may apply.”

Then the court pointed out the “more expansive duties” that Menards took on in the policy with Greenwich: “[Menard] shall exercise utmost good faith, diligence and prudence to settle all claims and ‘suits’ within the Self-Insured Retention ... . In the event of a claim or ‘suit’ which in our reasonable judgment may result in payments ... in excess of the Self-Insured Retention, we [Greenwich] shall have the right and the duty to defend and may, at our sole discretion, assume control of the defense or settlement of such claim or ‘suit.’”

Comparing these provisions, the court concluded that Menards only owed Greenwich – and not North American -- a duty to act in good faith to try to reach settlements below $2 million: “Contracts are usually enforceable only by the parties who agreed to them.”

The court concluded with this observation on the high-low settlement

“There is more we could say. North American did not exercise its right to participate in the defense, which exposed it to the risk that Menard would make litigating choices that it did not like. Menard's negotiation of a high-low settlement agreement with the plaintiff in the underlying trial shows that it took some steps to limit its insurers’ eventual liability rather than gambling with their money. Nor do we doubt that Menard's own payment obligations were ample motivation to minimize any prospective damage

|

| |

|

|

|

|

|

|

Vol. 11 - Issue 5

October 15, 2022

What Is A “Claim?”

Deals Sour Over Playboy-Branded Beer And Cigarettes

|

|

|

| |

When it comes to litigation over “claims made” policies, two issues get the vast majority of the attention – what is a “claim” and when was it made? And often times these issues overlap.

That’s what happened in Playboy Enterprises v. Indian Harbor Ins. Co., No. B315763 (Ct. App. Calif. Oct. 4, 2022). Elliott Friedman had licensing deals with Playboy to sell Playboy-branded beer and Playboy-branded cigarettes. The deals soured. Friedman sent some lengthy emails to Playboy’s general counsel to address the situation and express his anger about it.

One of the emails [May 10, 2016] is the focus of the case. Thus, it is necessary to set it out verbatim:

“Hi Rachel: [¶] I agree that all business has potential risks. [¶] Unfortunately, the inexcusable actions of Michael McNabb and Matt Nordby while working as senior executives at [Playboy], killed two businesses which were well underway and widely acknowledged to be extremely valuable. Their negligent behavior caused significant damage to [Playboy] but also to myself. [¶] I spoke with my long time lawyer, Robert O’Brien (Larsonobrienlaw.com), and he suggests you and I sit down alone to see if we can come to a meeting of the minds. While working with Robert is great, and a billion dollar damages trial is interesting, challenging and should be successful, I would rather focus at this point of my life on settling the issues and just getting compensated for my investment (cash and time) in Playboy Breweries and Playboy Lifestyle (cigarettes with HH). [¶] Let[‘]s just the two of us meet for now—I am available Thursday /Friday at your office in West LA or Larson O’Brien offices downtown.”

There was a subsequent meeting but no settlement was reached.

In March 2017 and December 2017, Friedman’s lawyer, the aforementioned Mr. O’Brien, sent letters to Playboy that demanded $95 million and $90 million, respectively, to settle the matter.

Playboy notified Indian Harbor of the letters and sought coverage under a professional liability policy. [The specific type of policy, and any coverage issues (other than “claim”), are not relevant here.] Indian Harbor paid close to $5 million to settle the matter. Playboy paid $159,000 toward the settlement and the remainder of its SIR. Playboy filed a coverage action and Indian Harbor filed a cross-complaint seeking to recoup the nearly $5 million settlement payment.

Indian Harbor later learned of the May 10, 2016 email and argued that no coverage was owed for the settlement as the email was a “clam,” as defined under the policy, and, thus, not first made during the policy period of November 30, 2106 to July 1, 2018.

The policy defined “claim,” in pertinent part, as follows: “[a] written demand for monetary damages, services, or injunctive or other non-monetary relief.”

The trial court concluded that the email was not a “claim.” The California appeals court agreed. The decision, following a dissection of the email, and examination of case law, was based on three rationales:

“The subject email does not contain a ‘demand.’ Rather, it contains a description of Friedman’s ‘grievance’ and an ‘expression of [Friedman’s] dissatisfaction’ with the behavior of certain Playboy executives—each of which, under the guidance in [citation omitted] is ‘not a demand.’ The subject email does go on to make a request based on this grievance; specifically, it suggests, ‘Let[‘]s just the two of us meet for now.’ But it neither insists on any course of action, nor expresses an entitlement to any course of action.”

***

“Even assuming, for the sake of argument, that the letter contained a ‘demand,’ the email still would not constitute a claim, because it still would not contain a demand ‘for monetary damages, services, or injunctive or other non-monetary relief.’”

***

“Unlike the letter in [citation omitted], there is no additional context in the subject email that would allow us to interpret the email requesting a meeting as even an indirect request for settlement compensation. For example, the [citation omitted] letter, unlike the subject email, expressly states that litigation may become necessary, and describes affirmative steps, including jurisdictional exhaustion of administrative remedies, the employee had already taken towards being able to file suit. The subject email’s opaque reference to litigation—specifically, how Friedman does not want to pursue it, even though he believes he would prevail—is distinguishable from the discussion of litigation in the [citation omitted] letter in this and other respects.”

There is no shortage of case law addressing what is a “clam” for various purposes under a “claims made” policy. But Playboy Enterprises v. Indian Harbor Ins. Co. provides some detailed discussion of interesting aspects of a communication that is in dispute.

|

| |

|

|

|

|

|

|

Vol. 11 - Issue 5

October 15, 2022

Coverage For Bat Guano Not Precluded By The Pollution Exclusion [And Bat Faith Denial]

|

|

|

| |

I used to get excited by cases involving the applicability of the pollution exclusion to damages to a home caused by bat guano. But now that there have been a few of them, not so much. So I might have ignored Auto-Owners Ins. Co. v. Bank, 2022 U.S. Dist. LEXIS 156056 (D.S.C. Aug. 29, 2022). [But I address it here as the decision includes a twist.]

The court concluded that the pollution exclusion did not preclude coverage. Among other reasons for its decision: “Finally, as the court continues to consider the Policy in its entirety, as the court is bound to do, mention must be made that the Policy addresses exclusions for damages caused by animals in provisions separate from the provision addressing pollutants. The Policy specifically bars coverage for damage caused by ‘birds, vermin, rodents or insects.’ An additional provision also excludes coverage for damage caused by ‘animals owned or kept by any insured.’ And not to belabor the obvious, but we are dealing with damage caused by an animal here. Yet Auto-Owners resorts to the section on pollutants to argue coverage is excluded. This court agrees with Nicholson. The existence of two exclusions specifically covering damage caused by animals creates doubt regarding whether the pollutant exclusion was intended to cover animal waste. See Nicholson, 979 F. Supp. 2d at 1067. While the existence of these animal provisions is not dispositive on the interpretive issue, it further adds to the ambiguity of the terms pollutant and waste.”

The court also denied the insurer’s motion to dismiss the insured’s bad faith claim: “Auto-Owners’ denial of coverage letter provides a sparse basis for its decision other than its conclusory statement: ‘the homeowner's policy does not provide coverage for this as bat guano is considered a pollutant under the policy.’ Auto-Owners did not provide a detailed justification for this decision until it responded to the South Carolina Department of Insurance’s inquiry regarding Bank’s administrative complaint. Auto-Owners asserted that a ‘supreme court case (Hirschhorn v. Auto-Owners Insurance Co.)’ supported its determination. However, as Bank points out, Auto-Owners failed to specify the Wisconsin Supreme Court authored this decision and not the South Carolina Supreme Court. Further, the record suggests that Auto-Owners failed to recognize contrary precedent (Nicholson) until the present litigation.”

|

| |

|

|

|

|

|

|

Vol. 11 - Issue 5

October 15, 2022

From The “Coverage Opinions Blasts” Archives

|

|

|

| |

In case you missed them, here are a few articles that were sent to subscribers as Coverage Opinions “Blasts” last month:

Insurer’s Deficient ROR Turns Win Into Possible Loss

Between the work that I do for insurer clients, and writing about this and that coverage case, I have a few favorite issues. How could you not? At the top of the list is the effectiveness, or not, of reservation of rights letters. I have followed these judicial decisions very closely for many years, not to mention having done a “50 Item ROR Checklist” seminar/webinar dozens of times for insurers.

The issue is so important as ROR letters apply across the board. In other words, they are relevant to duty to defend cases regardless of the type of liability policy at issue or facts of the claim.

So I took particular note of last week’s decision in Penn National Mutual Casualty Company v. Beach Mart, Inc., No. 14-08 (E.D. Pa. Sept. 30, 2022). The court was critical of the manner in which the insurer’s ROR was drafted. While it did not lead to a waiver of the insurer’s defenses – I suspect that it would have in some states -- the court left open the possibility that the ROR violated North Carolina’s “Unfair Claim Settlement Practices” statute, which gives rise to a private cause of action under the state’s Unfair and Deceptive Trade Practices Act. Many states have statutes that looks like North Carolina’s.

At issue in Penn National v. Beach Mart was coverage for a counterclaim filed against the insured, Beach Mart, for trademark infringement-related claims. Penn National agreed to defend Beach Mart.

[As an aside, there was a hubbub about who defense counsel would be and whether the counsel chosen by Penn National was qualified to handle an intellectual property claim. This is not relevant to the ROR issue, but it’s an interesting issue, as the court concluded that counsel may not have been qualified for this type of case, and, therefore, it may be a breach of the duty to defend.]

For reasons not relevant here, the court concluded that at some point Penn National no longer had a duty to defend. However, Beach Mart argued that the insurer did, in fact, have a duty to defend, on the basis that it waived its coverage defenses by sending a reservation of rights letter that did not “fairly inform” Beach Mart of the coverage issues that were being reserved.

In support, Beach Mart cited what I call the “big three” – Harleysville v. Heritage Communities (S.C. 2017); Advantage Buildings v. Mid-Continent (Mo. Ct. App. 2014); and Hoover v. Maxum (Ga. 2012) -- which are the cases most commonly cited by insureds to argue that coverage defenses are waived because the ROR did not “fairly inform” the insured of the coverage issues being reserved. [The big three have all been “Top 10” coverage cases of the year in my annual coverage hit parade; once in a while I get those right.]

The Beach Mart court declined to follow any of these three cases on the basis that they are not North Carolina law and the federal court was not going to do so as a matter of first impression.

So while the court concluded that Penn National did not waive its coverage defenses, that was not the end of it. The court went on to hold that the ROR letter, based on the manner in which it was drafted, may have violated North Carolina’s “Unfair Claim Settlement Practices” statute, which gives rise to a private cause of action under the state’s Unfair and Deceptive Trade Practices Act.

Specifically, Beach Mart argued that the insurer violated, among other sections, 58-63-15(11)(a) of the N.C. “Unfair Claim Settlement Practices” statute, on the basis that the reservation of rights letters “misrepresent[] pertinent facts or insurance policy provisions relating to coverages at issue.”

The court concluded that, “construed in the light most favorable to defendant [the insured], such a misrepresentation may be inferred from certain language in the reservation of rights letters.”

As for what that possible misrepresentation in the ROR may be, the court explained it as follows:

“In particular, while these letters communicate clearly a reservation of rights sufficient to overcome defendant’s waiver argument, addressed previously, those that include excerpts from the policies omit reference to the breach of contract exclusion of the umbrella policy, and they include other exclusions that are unrelated to the L&L counterclaims.

“None of the letters include discussion of plaintiff’s position as the various provisions [sic], nor do they explain how the allegations in L&L’s counterclaims might create coverage issues. Thus, it is reasonable to infer in this respect that they ‘[m]isrepresent[] pertinent facts or insurance policy provisions relating to coverages at issue.’”

Thus, the insurer’s motion for summary judgment on this issue was denied.

When courts conclude that an ROR letter is ineffective, it is usually for the reasons cited by the Beach Mart court -- the letter is cut and pasted [the court described it that way in another part of the opinion], it cites provisions unrelated to the claim and does not “fairly inform” the insured how the allegations in the complaint might create coverage issues. In other words, the letter may set out facts and policy provisions, but does not marry the two and specifically explain how the cited policy provisions, based on the facts at hand, may in fact serve to preclude coverage.

Beach Mart is an interesting and unique decision as these cases generally involve efforts by insureds to argue that an ineffective ROR leads to a waiver of coverage defenses. While Penn National beat back the waiver argument – and it may not have, if the court had been willing to consider Heritage Communities, Advantage Buildings and/or Hoover – the decision gives insureds a second bite at the apple.

A Trend: Insurers Losing “Professional Services” Exclusion Cases

I’ve been following a trend over the past couple of years: insurers losing cases where they assert that no coverage is owed, under a general liability policy, on account of a “professional services” exclusion. The insurer asserts that the injury or damage was caused by the insurer’s professional skill – and the argument sure looks strong -- but the court disagrees and treats it as a general liability exposure. As discussed below, earlier this summer another court handed an insurer a loss on the issue.

I’ll be discussing this trend at the 16th annual White and Williams Coverage College on October 13th – attend in person in Philadelphia or join remotely. So no need to fret if you are in the South Pole. I will discuss why courts have been ruling against insurers on the “professional services” exclusion. I will do so by examining cases where the insurer lost and explaining why. Then, by looking at cases where insurers have succeeded in enforcing their “professional services” exclusion, the program will address ways that insurers can make changes to their policies to achieve their desired intent regarding professionals and CGL policies.

For more information about Coverage College and to register, go here.

https://www.whiteandwilliams.com/resources-events-Coverage-College-2022-1

CLE and CE is offered for a host of jurisdictions. [But I’m not so sure for the South Pole people.]

There is no cost to attend Coverage College except for attorneys in private practice and non-sponsor vendors for whom tuition is $249.

Now, back to that case from earlier this summer where the court held that a “professional services” exclusion did not apply to a claim for property damage caused by an insured engaging in conduct that certainly looks professional to me.

In Stonegate Ins. Co. v. Smith, No. 1-21-0931 (Ill. Ct. App. June 22, 2022), the Appellate Court of Illinois addressed coverage for John Smith, a carpenter by trade, who was performing plumbing work at a townhouse. The court described Smith’s work this way: “Smith attempted to remove the old copper fittings from the shower valve. He did this by heating the copper fittings with a torch, thereby melting the lead that fused the fitting and the valve together, which, according to Smith, would allow the fitting to slip off. However, as Smith was using the torch to heat the fittings, the fiberglass insulation behind the bathroom wall caught fire. That fire spread upward to the neighboring unit, causing substantial damage to that unit.” Smith was not paid for his work. He was replacing a shower valve as a favor for a friend.

A subrogation action was brought against Smith by property insurers that paid for damage caused by the fire. Smith sought coverage under his homeowner’s policy for the damage he caused. His insurer denied coverage, asserting that the “professional services” exclusion applied. [While the case arises under a homeowner’s policy, the issue is exactly the same under a “professional services” exclusion contained in a CGL policy.]

In determining whether the “professional services” exclusion applied – the term was not defined in the policy -- the court stated that “‘professional services’ encompass any business activity conducted by the insured that involves specialized knowledge, labor, or skill, and is predominantly mental or intellectual as opposed to physical or manual in nature.”

The court held that the “professional services” exclusion did not apply:

“Stonegate [the insurer] ignores the established standard and fails to assert that the activity at hand is predominantly mental or intellectual. Nor could it make such an assertion. It would defy common sense to contend that using a flame to heat pipes is a predominantly mental or intellectual endeavor. To be clear, we do not hold that every type of work that could broadly be categorized as plumbing is per se outside the scope of ‘professional services’; rather, we take the narrower position that the particular activity of heating pipes with a torch is neither predominantly mental nor intellectual and, therefore, not a ‘professional service.’ In the case at bar, Smith was not a plumber and was to receive no money for his work, and as a result, the ‘professional services’ exclusion does not apply here.”

I am struggling to see how using a torch to melt the lead that fused a fitting and valve together is not a “professional service.” Yes, it is a physical/manual act. But surely it takes experience and intellect to do so safely. This isn’t exactly using a snake to clean the hair out of the shower drain.

Indeed, by definition, if what Smith did were so easy, he would not have allowed the fiberglass insulation behind the bathroom wall to catch fire. As you are reading this, I bet you are saying to yourself – gee, I know I would not have done this in my bathroom.

For more on this coverage issue, and numerus more, please join me and my W&W colleagues on October 13th for the firm’s Coverage College.

Pollution Exclusion: The Chapter Is Full! [Last Holdout Makes A Noisy Entrance]

Chapter 15 of the 5th edition of Insurance Key Issues – Absolute Pollution Exclusion – provides case law addressing the issue in 49 states and the District of Columbia. As of last month, the final holdout to be devoid of pollution exclusion case law – New Mexico – is no more. And while it took a long time to get there, the Land of Enchantment made a noisy entrance.

In an incredibly long opinion – 60 printed Lexis pages – the New Mexico district court held in Chisholm’s Village Plaza, LLC v. Travelers, No. 20-920 (N.M.D.C. Aug. 16, 2022) that the absolute pollution exclusion did not serve to preclude coverage for a CERCLA suit alleging that land and groundwater were contaminated by historic dry cleaning operations. When the pollution exclusion does not preclude coverage to those facts, you know something unusual is going on.

Given the extent of the court’s analysis, I could spend pages explaining this decision. But here’s the bottom line. The court adopted the Indiana approach to the interpretation of the pollution exclusion. Which is to say that it adopted the strictest standard in the country for the applicability of the pollution exclusion.

Before getting to what the Indiana approach means, it is useful to see the two other approaches that the court considered and declined to adopt. These are the two methods that generally apply to the entire pollution exclusion landscape nationally. But neither approach was considered adequate for the New Mexico court.

First, the Chisholm’s Village court rejected the “literal approach” to the applicability of the pollution exclusion. Under this approach, because the pollution exclusion is defined broadly, the exclusion applies when a substance is acting in any manner as an irritant or contaminant. This leads to a broad applicability of the exclusion.

The court also rejected the “situational approach” to the applicability of the pollution exclusion. Here, the court generally limits the pollution exclusion to situations involving “traditional environmental pollution.” There is little doubt that the contamination of land and groundwater, by historic dry cleaning operations, is “traditional environmental pollution.”

But the New Mexico federal court noted that, while the “situational approach” provides “more coverage and greater protections for the insured,” it declined to adopt it, explaining that it is “still problematic because the concept of what is a traditional environmental contaminant may vary over time and has no inherent defining characteristics, which leaves courts in the awkward and inefficient position of making case-by-case determinations as to the application of the pollution exclusion.”

After rejecting the literal and situation approaches, the court settled upon the approach that has been adopted by the Indiana Supreme Court: the insurer must specify the substances that come within the pollution exclusion.

This approach grows out of the Supreme Court of Indiana’s decision in Am. States Ins. Co. v. Kiger, 662 N.E.2d 945 (Ind. 1996), holding that the pollution exclusion did not preclude coverage for claims for damages caused by the discharge of petroleum from an underground storage tank at a gas station. As the Kiger court put it, “[S]ince the term ‘pollutant’ does not obviously include gasoline and, accordingly, is ambiguous, we once again must construe the language against the insurer who drafted it.”

To see how challenging it can be for the pollution exclusion to apply under this specificity of pollutants test, the New Mexico federal court quoted the following from the Indiana federal court’s 2015 decision in St. Paul v. City of Kokomo: “The City argued, and Judge Magnus-Stinson agreed, that, ‘even though it is undisputed that silver and selenium are types of inorganic contaminants, an ordinary policyholder of average intelligence would not know that from the 2011-2013 Policies.’ Consequently, Judge Magnus-Stinson concluded that the third set of policies ‘is not sufficiently specific such that Travelers has no duty to defend the City as a matter of law for testing for the substances silver and selenium’ and denied Travelers Indemnity’s request for summary judgment on the duty to defend.”) (emphasis added).

A review of Indiana case law on the pollution exclusion demonstrates the challenges that insurers have had in applying it under Indiana law, even to substances that are no doubt traditional environmental pollution. Such a review also shows the efforts by insurers to try to draft a pollution exclusion that meets Indiana’s specificity of pollutants requirement.

Chisholm’s Village is the first word in New Mexico on the pollution exclusion, but probably not the last.

ISO’s Flood Exclusion Amendments And Hurricane Ian Claims; Wind-Water Disputes

It seems inevitable that disputes over coverage for property damage caused by Hurricane Ian will arise. The take-up rate for flood insurance policies is too low, the water is too much and the stakes are too high.

And then throw this into the mix: The Washington Post recently reported that, according to Florida’s insurance regulator: “In the last half of the 2010s, Florida accounted for about 8% of all homeowners’ claims in the U.S. but almost 80% of all homeowners’ lawsuits against insurers in the U.S.”

Since wind is generally covered under a homeowner’s policy, and flood is not, this would seemingly create an incentive for those affected by Ian to argue, when feasible, that their property damage, despite appearing to have been caused by flood, was also caused by wind.

Below are links to two articles that I published on the White and Williams website that look at ways in which policyholders may try to navigate around the flood exclusion -- one legally and one factually -- and insurers’ counter-arguments that preclude such efforts.

ISO’S FLOOD EXCLUSION AMENDMENTS AND HURRICANE IAN CLAIMS

HURRICANE IAN: DISCUSSING WIND-WATER DISPUTES

|

| |

|

|

|

|

|

| |

|

| |

|

|

Guilty Plea Does Not Establish Intent To Defeat Coverage

At issue in Safeco Inc. Co. v. Dooms, No. 21-5034 (W.D. Ark. Mar. 23, 2022) was the availability of coverage for Dillon Dooms, a photographer, for claims brought against him by models who were surreptitiously video-taped as they were changing outfits in his studio. Despite the fact that Mr. Dooms plead guilty to video voyeurism, the court concluded that this was not dispositive of his intent for purposes of applying a criminal act exclusion. I thought that the court’s rationale for this was interesting:

“Safeco asserts the guilty plea serves as an admission that the tortious conduct—recording State-Court Plaintiffs without first providing notice or obtaining consent—was purposeful, not accidental, and Defendants are precluded from arguing otherwise. However, under controlling Arkansas law, Mr. Dooms’ guilty plea does not establish his intent for collateral estoppel purposes. *** Mr. Dooms’ plea is not dispositive of his intent. Mr. Dooms had incentive to enter a guilty plea when he was faced with 13 counts of voyeurism that could total a sentence of 78 years of incarceration. Mr. Dooms agreed to a term of incarceration of five years in his plea agreement. Under Bradley Ventures, this reduction in sentence provided alternative motivation for Mr. Dooms to plead guilty. The record does not supply sufficient facts to establish Mr. Dooms’ failure to warn was intentional, and the Court cannot grant summary judgment based on the Criminal Acts Exclusion.”

|

| |

|

|

|

| |

| |

| |

| |

| |

|

|

|

|

|

|

|

|

|