|

|

|

|

|

| |

|

Vol. 10 - Issue 2

March 8, 2021

|

|

|

|

|

|

| |

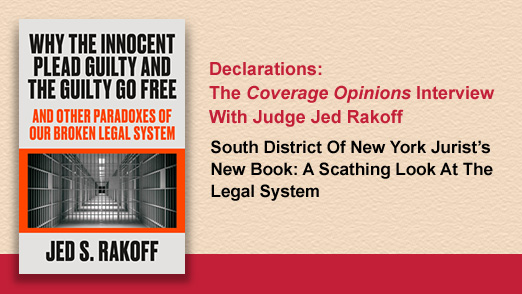

Jed Rakoff, the well-known jurist from the Southern District of New York, just published “Why the Innocent Plead Guilty and the Guilty Go Free -- And Other Paradoxes of our Broken Legal System.” The book is brutal in its criticism. Wait. Can a sitting federal judge really say such things? Yes, Rakoff told me during an hour-long interview that I did with him for The ABA Journal. Lots of books have been written about the legal system’s maladies. But when its 200 pages, from a nationally-known sitting federal judge, it’s not like all the others.

You can check out the interview here.

|

|

|

|

Vol. 10 - Issue 2

March 8, 2021

|

|

|

|

|

|

| |

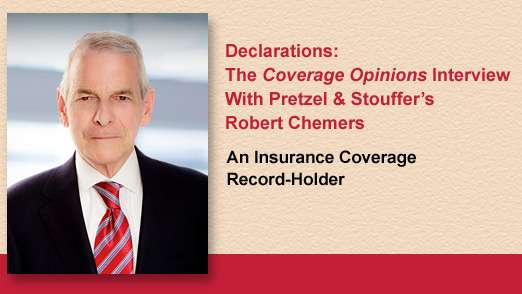

I read a lot of coverage cases. And when I do, I always take note of the lawyers involved. For years, I have been seeing the name Robert Chemers, of Chicago’s Pretzel & Stouffer, over and over and over listed as counsel for the insurer. Out of curiosity, I did a Lexis search and discovered that Chemers represented a party in a staggering 650 or so opinions (not all coverage, but mostly). I don’t believe that there is a coverage lawyer in America credited with so many. I was delighted, and flattered, to learn that the Second City lawyer (Cubs over Sox) is a long-time Coverage Opinions reader.

I reached out to Chemers to ask him to do an interview for CO. He graciously agreed. I had to get to the bottom of how he’s been involved in all those cases.

Chemers’s remarkable stats read like the back of an Ernie Banks baseball card. He has handled over 900 appeals, including over 150 in the Supreme Court of Illinois, of which 52 involve opinions (20 involving coverage), 65 in the Seventh Circuit Court of Appeals and hundreds in the Appellate Court of Illinois, with the majority being coverage-related. He has astonishingly handled coverage cases in 71 of Illinois’s 102 counties. And Chemers plays in away games too, having handled cases in the Supreme Courts of Wisconsin, Ohio, Maine, Mississippi and Indiana, as well as in numerus states’ intermediate appellate courts and federal courts of appeal.

For the 69-year old coverage lawyer, it all started at Pretzel & Stouffer in 1976. “I was 24 and right out of Indiana University School of Law,” Chemers tells me. “I initially worked with Joseph B. Lederleitner, then a senior partner, who was my mentor. He was a renowned coverage and appeals practitioner.”

Lederleitner took the reins off his mentee early. In less than a year, the nascent lawyer found himself arguing before the Appellate Court of Illinois in Kaiserman v. Bright, a case involving the standard for recovery for emotional injuries caused by negligent conduct.

Chemers recalls his debut and the comment from one of the three panel members: “This must not be a tough appeal if Mr. Lederleitner isn’t arguing.” Chemers won the case.

Lederleitner was a tough critic. “I submitted my first brief to Joe for review,” Chemers reminiscences. “The plaintiff had appealed a $600 verdict, in an auto case, claiming that it was inadequate. That’s how it was in 1976.”

“Joe looked at the document and told me that the only aspect that could be salvaged was the title -- Brief of Appellee. He pulled off the cover page, dropped the rest in the trashcan and told me to focus and do it again. For years I saved that first page, however, I no longer have it. I won that appeal.”

“Joe was strictly business,” Chemers says. “I worked with him for three years before I knew he had eight children. I greatly respected him, and, in fact, my oldest son has Joseph for his middle name.”

With an experience like that, I ask Chemers what he was like as a mentor when that time came. “I told myself that I would never treat associates the way I was treated,” Chemers explains. “And I have adhered to that approach.” Chemers says that his own style is to mark up a brief in red ink and then discuss the reasons for his edits. “The more briefs prepared by the associate, the less red ink, as style sets in. My style not only prevails, but is required.”

So what’s behind Chemers being involved in so-many cases? Does he specialize in representing litigious insurers?, I joke.

The answer is quite simple, he explains: “Illinois is a litigious state and insurance coverage issues are a big part of litigation. The focus of the firm has always been on litigation, and litigation begets coverage work and coverage work and litigation beget appeals.”

He also gives credit to the Land of Lincoln’s appellate court rules. “In Illinois,” Chemers explains, “our appellate court is not bound by its own decisions, and often a panel issues a decision which conflicts with another panel’s decision. It is up to the Supreme Court of Illinois, if it decides to exercise its discretionary jurisdiction, to resolve the conflict. If the Supreme Court does not allow leave to appeal, the conflict continues and litigants continue to appeal and attempt to chip away at the conflict by arguing that one line of cases is better reasoned than the other. And so on and so on, and decisions proliferate. Not just in the coverage arena, but in the full spectrum of appealable issues.”

Having handled so many appeals, especially before the Illinois Supreme Court, Chemers has of course had a hand in many significant cases, including Waste Mgt. Inc. v. International Surplus Lines Ins. Co. (1991), which recognized the common interest doctrine; Pekin Ins. Co. v. Wilson (2010), adopting a narrow exception to the four-corners doctrine; Cincinnati Cos. v. West Am. Ins. Co. (1998), concluding that a tender is not required where the insurer has knowledge of the suit; Standard Mutual Ins. Co. v. Lay (2013), involving the sufficiency of a reservation of rights letter; ISBA Mutual Ins. Co. v. Tuzzolino & Terpinas (2015), addressing rescission and the innocent insured rule; and Kakos v. Butler (2016), which struck an amendment to the Code of Civil Procedure as unconstitutional which mandated 6-person juries in civil trials.

“These cases have significantly changed Illinois law,” Chemers says, “and it is rewarding to have been involved in these frequently cited decisions.”

Chemers can’t help chuckling about the client who refused to pay for legal research: “We will not pay your firm to review your own cases.”

Chemers’s coverage practice evolved over the years, coming to include all issues imaginable under a long list of property and casualty policies. “Whatever was the coverage issue du jour,” Chemers says, “we handled it.”

“The approach to an appeal, coverage or non-coverage, is the same,” Chemers says. “A thorough review of the record and framing the issues in a cogent and convincing manner so that the desired result may be obtained.”

Chemers recalls a two-week period in 1987 when he argued two insurance coverage appeals in the 7th Circuit. “During the first argument, Judge Posner commented that the policy was ‘the most ambiguous policy I ever read.’ Two weeks later, during my argument, Judge Posner commented that the policy was ‘the most ambiguous policy I ever read.’ This caused me to state that the policy was clear and unambiguous, and, further, at worst it would be tied with another as the most ambiguous. I reminded His Honor about his comment two weeks earlier and then I named that appeal. The clerks told me after the argument that it was the first time they saw Judge Posner laugh on the bench. I lost the first appeal, but won the second.”

Chemers observes that he is one of very few attorneys who can state that they argued the same appeal twice. “I argued an appeal to the Supreme Court of Illinois in January 1978. Then, one of the seven Justices died. The Court must have been tied 3 to 3. After a new Justice was named, I argued the case again.” Chemers tells me that he lost that one 4-3.

There is an occupational hazard of handling cases outside of Chicago, Chemers says. “There are a number of counties in Illinois that have fewer than ten registered attorneys,” Chemers tells me. “The first question that a Chicago attorney gets is a tough one – ‘what’s wrong with the local bar?’ When we lose in those venues, we have frequently prevailed on appeal.”

Chemers says that he has no retirement plans in his future so long as he continues to enjoy good health and the challenges provided on a daily basis by a busy coverage, coverage litigation and appellate practice. “I thrive on those challenges,” he says, “and look forward to further success in my field. I work at a pace which would cause a younger person to grow weary, but I have always maintained a strong work ethic.”

Chemers calls himself an “avid but not very good golfer.” Nonetheless, he has two holes-in-one to his credit. Proof, he says, of the adage that “even a blind squirrel can find an acorn.” The aces came in 1996 and 1998. “I thought they would occur every two years, but I’m now working on a 23-year dry spell.”

After 45 years Robert Chemers has seen a lot. But he tells me that the basic practice of law has not changed for his firm: “Our clients still want quality work for a reasonable price. Some still want to win and others want resolution if it can be achieved reasonably to get the file closed.”

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Vol. 10 - Issue 2

March 8, 2021

Encore: Randy Spencer’s Open Mic

I’m Not Lion: The Coverage Case Involving Cats That You Must Read

|

|

|

|

|

| |

This “Open Mic” column originally appeared in the March 5, 2014 issue of Coverage Opinions. With all the attention given recently to the Texas lawyer, who appeared as a cat on a video hearing, this seemed like a good time to reprise this Spencer column. This one is a real case. No kitten.

|

| |

I really dislike cats. It has got to be one of the worst musicals ever. That it came from Lloyd Webber just serves as evidence that even the greatest are entitled to an off day now and then. That it is one of the most successful Broadway and West End musicals ever just serves as evidence that P.T. Barnum was right. Thankfully “Memory” was performed in Act I so I could leave before Act II.

As for cats and coverage, there are very few cases involving this combination – as in, almost none. Dogs on the other hand – you can’t even count them all. There are no doubt lots of reasons for this disparity owing to the many differences between the two.

The last issue of Coverage Opinions looked at some coverage cases involving dogs. In particular, claims involving show dogs that bite. In the amazing coincidence category, just as that issue of CO was being put together, the California Court of Appeal issued an opinion addressing liability coverage for an incident involving cats. And not just any opinion, but one with wacky facts that makes for very interesting reading. You’ll see. While Coverage Opinions is not bound by any sort of equal time requirements, like television networks, it only seemed fair to follow up last issue’s dog article with one involving cats.

Abrahams v. Allstate Ins. Co., No. B244642 (Cal. Ct. App. Feb. 6, 2014) goes like this. Leslie Abrahams and Hal Gosling, husband and wife, undertook to protect the feral cat population at California State University, Long Beach by maintaining feeding stations around the campus. Scott Miller lived adjacent to CSULB and frequently walked, jogged and rode his bicycle through the campus with his dog and young children. Allegedly, one day in 2005, Abrahams stopped Miller on campus and demanded that he not walk his dog. Miller ignored the demand and four years later Abrahams confronted Miller and his son as they walked their dog on the campus. She berated Miller, told him she represented CSULB and he was not welcome on the campus with his dog. Abrahams threatened that “the campus cat club was going to ‘take care of him.’”

Let me repeat that line here because I don’t tire of hearing it: The campus cat club is going to take care of you.

Wait, it gets better. The court put it this way. “Over the next year, on multiple occasions, Abrahams and Gosling drove their car toward Miller and his sons in a threatening manner as they walked or biked with their dog on the CSULB campus. Abrahams and Gosling repeatedly followed and stared down Miller and his sons and videotaped Miller and his family at their home and at CSULB. Abrahams also charged up to Miller in a post office parking lot, berated Miller’s wife and son as they exited a local Sears store, and contacted Miller’s son’s daycare provider to report that Miller was emotionally unstable, a danger to the community, and a threat to the daycare provider’s cats.” Someone was getting into the catnip.

Miller sued the cat duo alleging causes of action for invasion of privacy, stalking, intentional infliction of emotional distress and assault. The couple sought coverage from Allstate, their homeowner’s insurer. Allstate disclaimed coverage and litigation ensued. The trial court granted Allstate’s motion for summary judgment on the basis that Abrahams and Gosling’s alleged conduct was deliberate and no accident that triggered Allstate’s duty to defend. The case went to the Court of Appeal, where the cat lovers coughed up a fur ball.

The couple argued that they did not intend to threaten, frighten or intimidate Miller. They described their motivations as benign and that they lacked knowledge that Miller was emotionally hypersensitive. They also asserted that others would have perceived their behavior to be innocuous. However, the court held that their peaceable motivation did not transform their actions into accidental conduct: “[A]ppellants essentially argue their mistaken belief about Miller’s receptiveness to their deliberate behavior rendered their conduct accidental because they did not anticipate or intend its result. They are incorrect. Miller alleged appellants confronted, berated and threatened him on multiple occasions; drove their car toward him in a threatening manner several times; followed, stared at and videotaped him; and made a negative report about him to his son’s daycare provider. Appellants might not have anticipated this conduct would injure Miller, but their miscalculation did not transform the conduct from deliberate to accidental.”

The campus cat club is going to take care of you.

|

That’s my time. I’m Randy Spencer. Contact Randy Spencer at

Randy.Spencer@coverageopinions.info |

|

| |

|

| |

|

|

|

|

Vol. 10 - Issue 2

March 8, 2021

Meet the New Insurance Key Issues Spokes-cat

|

|

|

| |

Not long ago, Zurich’s Carrie Von Hoff sent me a picture of her cat, Legolas, hanging out with her at-home copy of Insurance Key Issues. We had a good laugh about it.

But then it hit me. Legolas, perched next to Key Issues, could be the official spokes-cat for the book. There has never been an official spokes-cat for Key Issues. [Actually, it is possible that there has never been an official spokes-cat for any book since Johannes Gutenberg invented the printing press in Germany in around 1440.]

After some negotiations, the deal was inked. Legolas, named for the Lord of the Rings character, held out for an extra ball of yarn. It got a little ugly. The whole thing nearly fell apart over it.

Meet Legolas, an almost 2-year-old male cat. The feline resident of Evanston, Illinois enjoys sleeping on heating vents, pouncing his brother Gimli, climbing into laundry baskets, and attacking house slippers to get to the insoles. His favorite toys include a tiny cat-sized soccer ball, a mouse-shaped laser pointer, ribbons, and pretty much any toy with a feather. His favorite meal is canned chicken dinner with gravy. [Carrie doesn’t like to brag, but Legolas also sings a killer rendition of Memory.]

A Key Issues spokes-cat! Why didn’t I think of this sooner? It opens up a whole new avenue for sophomoric book plugs. The potential is limitless. Do any Key Issues readers have a parrot looking for a job? Nominate your pet to be the Key Issues spokes-fill in the blank!

|

| |

|

| |

|

|

|

Vol. 10 - Issue 2

March 8, 2021

RIP Vernon Jordan: My 2019 Interview With The Civil Rights Icon

|

|

|

| |

|

| |

I was saddened by last week’s passing of Vernon Jordan. I had the privilege of interviewing the civil rights icon in October 2019 in his Washington, D.C. office.

I focused on Jordan’s role as a civil rights leader and lawyer at Akin Gump. Nothing political. Nothing about his close relationship to Bill Clinton. But I did ask him about being considered “the most connected person in America.” His response was perfect.

Jordan knew that many people didn’t know that he was a civil rights leader. He said to me: “Some people believe I was born on January 20, 1993” – referring to the date of Bill Clinton’s inauguration.

The interview is reprised here.

https://www.coverageopinions.info/Vol8Issue9/Declarations.html

|

| |

|

| |

|

|

Vol. 10 - Issue 2

March 8, 2021

Policyholder Counsels’ Favorite Song: Stairway To Heaven

|

|

|

| |

This year marks the 50th anniversary of the release of Stairway to Heaven.

Few – more like nobody, I’m sure – realize this, but the Led Zeppelin song, that some call the greatest in rock & roll history, is no doubt the favorite of policyholder counsel.

Take a look at the 2nd verse:

There’s a sign on the wall, but she wants to be sure

‘Cause you know sometimes words have two meanings

There is absolutely no tune that policyholder counsel enjoy singing more than that!

In 8+ years of Coverage Opinions, that may be the most inane thing that I have ever written. And that’s saying a lot.

But, it also conclusively proves that there is absolutely no limit to what you can learn about insurance coverage from this fine – and, as I like to remind you, free – publication.

|

| |

|

| |

|

|

|

Vol. 10 - Issue 2

March 8, 2021

What Do You See?: Insurance Coverage Rorschach Test

|

|

|

| |

When I see a new house being built, I do not think of the lucky family who will soon be making a lifetime of memories inside. And when I see a building going up, I do not think about the business soon to be occupying it.

Rather, in both cases, the image that appears before me is a future construction defect suit, followed by a dispute, between a builder and insurer, whether faulty workmanship is an “occurrence.” This is my insurance coverage Rorschach test.

A couple of weeks back, while walking early-morning to the train station, I spotted the below.

A snow plow hard at work, you say?

Not me. I see a future additional insured coverage dispute. [If you do additional insured work, you get it.]

What’s your insurance coverage Rorschach test?

|

| |

|

| |

|

|

Vol. 10 - Issue 2

March 8, 2021

3 Courts, In 3 Days, Seek Guidance From The ALI Restatement Of Liability Insurance

|

|

|

| |

May will mark the third anniversary of the American Law Institute’s vote to approve the organization’s Restatement of the Law, Liability Insurance.

For the most part, while the RLLI has been cited by courts in several dozen cases, the ALI’s work had a substantive role in only a handful. This is why I was so surprised by what I saw in late February. Over the course of just three days, three courts discussed the RLLI as part of their analysis in reaching a decision. The RLLI was right there, playing a part in the court’s decision-making process. And, I was pleased to see that the courts used the RLLI in exactly the manner that I have been predicting for the past eight or so years. [I get lots of predictions wrong-- so when I get one right, I like to make a big deal about it.]

Throughout its long and contentious drafting process there were numerous concerns raised by insurers, and their counsel, that the ALI was seeking to adopt positions in the RLLI that would lead to all manner of detrimental outcomes for insurers in coverage disputes. After nearly three years, and several dozen decisions having something to say about the RLLI, to various degreees, that has not come to pass.

Yes, there have been a few cases that an insurer lost and the RLLI was included in the court’s analysis. But, in some of those cases, it is clear that the court would have found against the insurer anyway – for other reasons. Importantly for insurers, courts have not undone any pro-insurer precedent in favor of adopting a different rule pronounced in the RLLI. Insurers have also prevailed in cases where the RLLI was included in the discussion.

None of this is to say that insurers are out of the woods on the RLLI. For sure, there are some aspects that offer courts an opportunity to adopt a novel approach on an issue that could be very detrimental to insurers. And then that approach could take hold and be adopted widely.

Overall, when it comes to courts citing to the RLLI, is has mainly been to state a general principle of coverage law or the ALI’s work was mentioned but it played no part in the decision making. For example, one court cited the RLLI to state that the insurer has the burden to prove an exclusion. In another, the court turned to the RLLI to tell us that the insurer “must defend any legal action brought against an insured that is based in whole or in part on any allegations that, if proved, would be covered by the policy, without regard to the merits of those allegations.” Insurers will lose no sleep over these decisions – nor most others, as they cite to the RLLI for fairly innocuous reasons.

So with courts having mainly cited the RLLI for benign purposes, I was surprised by the February trifecta. Are courts’ use of the RLLI changing?

In Burka v. Garrison Prop. & Cas. Co., No. 20-172 (D. Me. Feb. 22, 2021) the court addressed when the duty to defend ends. In reaching its decision, the court noted that no Maine Law Court had addressed the issue. However, the court noted that the RLLI has, and cited the rule set out in section 18 as well as a comment. The court looked favorably to the RLLI’s position: “Adjudication eliminating the covered cause from the action, so that the only remaining cause of action is not covered, ends the insurer’s duty to defend the action, provided that the time for taking an appeal from that adjudication has expired, any appeals have been resolved, or the claimant has relinquished its appeal rights.”

But it doesn’t end there. The court noted that, in reaching its decision, it was going against another Maine District Court, where Judge Singal held that a trial court dismissal ends the duty to defend before appeal rights are exhausted. But, as the court noted, it had reasons for reaching a contrary result. Drum roll: “[Judge Singal] did not have the benefit of the later Restatement analysis,” as well as the fact that he based his conclusion on Massachusetts law.

In Inn One Home v. Colony Specialty Ins. Co., No. 19-141 (D. Vt. Feb. 23, 2021), the court addressed whether an insurer was required to prove that it was prejudiced before it could disclaim coverage on account of an insured’s failure to satisfy the notice provision in a claims made policy.

The court stated that the majority of courts nationally have held that no prejudice is required. This is not a contentious conclusion. In predicting that the Vermont Supreme Court would not require prejudice, the court took guidance from the RLLI: “The Restatement of Liability Insurance endorses this same approach and notes ‘[w]ith respect to claims first reported after the conclusion of the claim-reporting period in a claims-made-and-reported policy, the failure of the insured to satisfy the claim-reporting condition in the policy excuses an insurer from performance under the policy without regard to prejudice’. Restatement of the Law of Liability Insurance § 35(2) (2019). Because the Vermont Supreme Court often looks to the Restatement for guidance, . . . the court predicts that Vermont’s highest state court will not require a showing of prejudice before coverage may be denied for failure to make and report a claim within the applicable policy period.” (emphasis added).

In Cincinnati Ins. Co. v. Selective Ins. Co., No. 18-956 (S.D. Ind. Feb. 25, 2021) the court addressed whether to certify, to the Indiana Supreme Court, the question whether the state recognizes a cause of action for negligent failure to settle. In deciding if certification was appropriate, the court addressed several factors, including the absence of a consensus view among state courts.

In concluding that there was an absence of a consensus view, the court stated: “Although ‘a duty to settle is a firmly entrenched aspect of an insurer’s obligation to an insured,’ states’ ‘views as to the source of the obligation, the precise extent of an insurer’s obligations, and the remedies for breach diverge[,] and there is a wide-ranging spectrum of approaches as to each.’”

The source for this statement: a Rutgers Law Review article, by Leo Martinez, titled: “The Restatement of the Law of Liability Insurance and the Duty to Settle.”

***

My take on the RLLI has not changed since the beginning. I have said the following many times: “Liability insurance coverage is an extremely well-developed body of law. On many of the RLLI subjects, the vast majority of states have already spoken. I do not believe that courts will eschew their own precedent in favor of adopting a contrary rule contained in the RLLI. Rather, as I see it, the RLLI’s impact will be felt by courts using it to fill voids and crevices in their own state’s law. Faced with an issue on which there is no home-state law (or the law is not clear), and there is a divergence of positions nationally, the court, looking for a place to land, may be inclined to adopt the RLLI’s position. In this situation, insurers have more to fear than policyholders.”

My frequently cited prediction has come true in the courts’ use of the RLLI in all three of the decisions from February. Once in a while my crystal ball is right. But never with my NCAA tournament bracket.

|

| |

|

| |

|

|

|

|

Vol. 10 - Issue 2

March 8, 2021

Boxing World Loses A Champion (And Coverage Opinions Good Sport)

|

|

|

| |

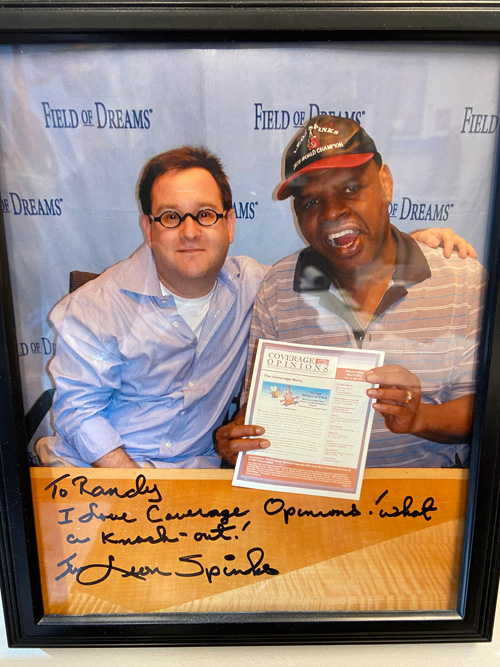

In 1978, Leon Spinks shocked the world by beating Muhammed Ali and becoming boxing’s heavyweight champion. Spinks died last month at age 67.

I had the opportunity to meet Spinks in 2013 at a personal appearance he did in Las Vegas. Of course, I had to ask him to hold up a copy of Coverage Opinions and write something about it. And the former champ was a great sport and happily obliged.

|

| |

|

| |

|

|

|

|

Vol. 10 - Issue 2

March 8, 2021

The Crazy Coincidence: Judge Rakoff’s Great Opening Paragraph In Olin

|

|

|

| |

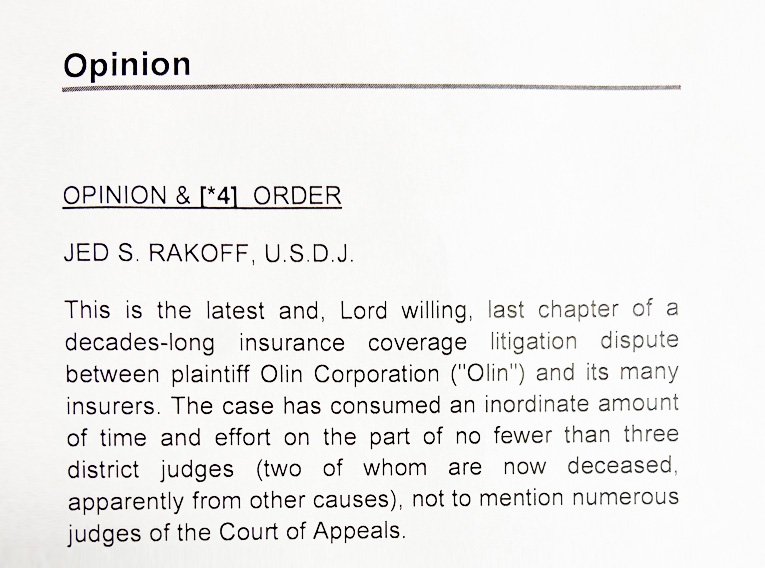

It was the craziest of coincidences. At the very same time that I was writing this issue’s interview with Judge Jed Rakoff, and emailing with him back and forth on some follow-ups to our phone conversation, the Southern District of New York judge issued an opinion in Olin Corp. v. Lamorak Ins. Co.

Olin involves coverage for environmental contamination. The case has been around for a long-time. A reallly long time. The docket number indicates that it was filed in 1984. “16 Candles” came out that year. Member’s Only jackets were cool.

That Olin is Methuselah-like was certainly not lost on Judge Rakoff, a point His Honor makes humorously clear in the opening paragraph of his opinion:

|

| |

|

OK, I had a Member’s Only jacket. [But I’ll deny I said that.] |

| |

| |

|

|

|

|

Vol. 10 - Issue 2

March 8, 2021

Tom Baker On The Latest From The Penn Law School Covid Coverage Litigation Tracker

|

|

|

| |

Penn Law Professor Tom Baker is still going full-tilt with his Covid Coverage Litigation Tracker. It is the single-best source to get the latest -- and constantly changing – statistics on Covid coverage litigation decisions. Given that decisions are now coming down swarm-like, this has to be a huge undertaking for Tom to keep it up.

I asked him. “It IS a huge undertaking,” Tom told me by email, “but lots of people are helping, especially at UConn’s Insurance Law Center. The weak link is state court decisions, because there isn’t any unified docket system. If you’re involved in a state court case, please send a copy of any judicial rulings to cclt@law.upenn.edu.”

Check out the current scoreboard and latest statistics here:

https://cclt.law.upenn.edu/judicial-rulings/

|

| |

|

|

|

|

| |

|

|

There were a lot of cases of late that met the high standards for being included in Coverage Opinions. It was too many for me to do a lengthy write-up of each. So, instead, I am resorting to Tapas-style case write-ups.

Exclusion Not Applicable: Not “Conspicuously Placed” In The Policy

At issue in HDI Global Ins. Co. v. San Fernando Realty, No. 20-6468 (C.D. Calif. Dec. 28, 2020) was coverage, under a Real Estate Errors & Omissions Liability policy, for a deal gone bad. In particular, the court focused on the potential applicability of a policy exclusion, contained in an endorsement, called the “Other Source Exclusion.” What it says, and its relevance here, is not important for purposes of this discussion.

The court held that the exclusion could not be enforced – assuming that it was otherwise applicable, which, it turns out it was not – because it was not “conspicuously placed” in the policy, as required by California case law. The court had much to say – none good -- about where the exclusion fit into the policy document.

In general, the court took issue with the exclusion on several bases.

“It appears only after many long and complicated pages, separated from the beginning of the Policy’s exclusions section by 11 pages.”

“There is no language on the endorsement that would alert a reader that the list contains limitations on coverage. . . . This silence stands in contrast to other sections of the Policy limiting coverage, which are introduced as ‘Exclusions’ and ‘Limit of Liability’ in explicit terms.”

“The heading, ‘Mortgage Brokering Amendatory Endorsement,’ suggests that its provisions are limited in scope to mortgage brokering services, which is only one of six Insured Services on the declarations page.”

But the court wasn’t done with its criticism: “While the Policy defines 11 terms, it does not define ‘mortgage brokering’ or ‘escrow agent services,’ and does not contain any other language that would clarify how the term ‘mortgage brokering’ is used in the heading of the endorsement containing the Other Source Exclusion.”

Other than that, how was the play Mrs. Lincoln?

Federal Judge To Plaintiff: You Gotta Be Kidding! That’s Not Negligence.

I love cases where plaintiffs try to plead into coverage: “Defendant negligently stabbed plaintiff 17 times.” Then: “Defendant should have known that stabbing plaintiff 17 times would cause injury.” Sometimes plaintiffs can get away with it and trigger a defense, for the defendant-insured, for what is clearly an uncovered/intentional conduct claim. But courts are usually wise to it and the judge says not on my watch – even if the duty to defend determination must be limited solely to the four corners of the complaint.

In State Farm v. Simone, No. 20-908 (W.D. Pa. Jan. 28, 2021) the judge made it clear what he thought of this plaintiff drafting tactic: No way, no how, is anybody pleading into coverage in my courtroom.

At issue in Simone was coverage for Charles Simone, under a State Farm homeowner’s policy, for injuries that he allegedly caused to Michael Wain, after Simone and Wain’s friend, as the court put it, “bumped into” each other at a crowded concert. As is often the case in assault-type situations, State Farm argued that it had no obligation to provide coverage because the claims against Simone did not allege an occurrence/accident.

Simone argued that the complaint filed against him did allege negligent conduct (in addition to intentional conduct). Number 3 is as good as it gets when it comes to pleading into pleading.

The complaint alleged that Simone breached the duty to act reasonably and avoid injuring Michael Wain by: (1) “[n]egligently striking [Michael Wain] and causing him to suffer personal injuries”; (2) “[f]ailing to observe [Michael Wain] and avoid striking him”; and (3) “[f]ailing to stop his arm before striking Michael Wain.” The complaint also alleged that Simone was negligent in: “[p]ermitting himself to either (sic) become intoxicated which caused him to strike Michael Wain”; “[a]llowing his emotions to control his actions which caused him to strike Michael Wain”; and “[l]osing control of his emotions which caused him to strike Michael Wain.”

But the judge wasn’t buyin’ it, no matter what the complaint said: “There is no allegation in the Underlying Complaint, however, that Simone lacked control over his arm at the time he allegedly struck Michael Wain, nor are there allegations which would indicate that Simone, in allegedly punching Michael Wain with enough force to break seven bones in his face, did not intend the ‘natural and expected’ consequences of his actions.”

As Maxwell Smart would have said: “The oooold failing to stop your arm trick.”

Can You Hear Me Now?: In Re: Verizon Marches On

In late-2019, the Delaware Supreme Court decided In re: Verizon Insurance Coverage Appeals. In a unanimous decision, the high court of the first state held that the term “securities claims” was unambiguous and reached only laws and regulations typically understood to apply to the purchase and sale of securities (e.g., the 1934 Act; Rule 13A; and state equivalents) and applied only to laws, regulations or rules that had the primary purpose of regulating securities. As a decision that defined a term that goes to the heart of a specific category of D&O coverage, I included it as a Top 10 case of 2019.

Verizon is back in Delaware – this time serving as the basis for Travelers’s win in Calamos Asset Management v. Travelers Casualty & Surety Co., No. 18-1510 (D. Del. Feb. 19, 2021). At issue was coverage for Calamos, under a D&O policy, for two suits arising following a merger – one seeking appraisal of Calamos’ stock and the other alleging that Calamos’ officers and directors breached their fiduciary duties.

The court’s decision was all Verizon in putting the kibosh on the insured’s pursuit of coverage for the fiduciary claims, noting the “Delaware Supreme Court’s holding that fiduciary-based claims are not specific to any rule, regulation or law ‘regulating securities.’ This holding is relevant here — and indeed is fatal to Plaintiff's claims. As the Verizon court explained, the phrase ‘regulating securities’ imposes its own limitation. The court elaborated: ‘regulations, rules, or statutes that regulate securities are those specifically directed towards securities, such as the sale, or offer for sale, of securities.’ Fiduciary duty claims ‘are not specifically directed towards securities.’ They ‘do not depend on a security being involved.’ Instead, fiduciary duty claims ‘include a variety of claims when ‘one person reposes special trust in another’ or when ‘a special duty exists on the part of one person to protect the interests of another.’ Reading the phrase ‘regulating securities’ to cover fiduciary duty claims would be inconsistent with the plain meaning of the term.”

Also for reasons related to Verizon, the policyholder fared no better with its other claim.

Who Doesn’t Love A Good “Use Of An Auto” Case

I love “use of an auto” cases – be they in the context of coverage under an auto policy or the auto exclusion in a general liability or homeowner’s policy. The cases have a way of involving peculiar facts. And there’s a reason for that. After all, since automobiles are designed with a clear purpose in mind, getting to Point B, what’s a “use of an auto” shouldn’t be all that hard to figure out. So, if “use of an auto” is being litigated, then, by definition, it’s probably because the claim involves something more than a person simply sitting behind the wheel and motoring down the road.

Atain Specialty Ins. Co. v. Davester, LLC, No. 19-11634 (D. Mass. Feb. 11, 2021) is an interesting “use of an auto” case. Technically, it’s not a “use of an auto” case, as it involves different policy language. But, in my book, it’s a “use of an auto” case for purposes of auto-related cases being interesting.

I’ve never seen facts like this: “[O]n March 17, 2018, [Newman] Galati was a patron at Embargo, a restaurant, where he was ‘highly and visibly’ intoxicated. The complaint further alleges that when Galati sought to leave the restaurant, Embargo employees looked in his wallet for identification, determined his home address, called him a Town Taxi cab, and instructed the cab driver to take Galati home. Instead, according to the complaint, the cab driver let Galati exit the cab somewhere other than his home and left him lying in the street, and Aguiar then struck Galati with his car, causing Galati substantial injuries. The state court complaint alleges counts of negligence against Aguiar, Embargo, and Town Taxi.”

At issue was coverage for Embargo under a commercial general liability policy. Specifically, the applicability of an exclusion for bodily injury arising out of or in connection with any auto.

Embargo, the insured-restaurant, argued that the claims had nothing to do with an auto, as it alleges that “Embargo should have called the police or for medical assistance, rather than assist [Galati] into a Town Taxi cab.”

The court concluded that the auto exclusion applied, but not because of the role of the taxi, but, rather, the car that hit Mr. Galati: “In the underlying complaint, the source of Galati’s bodily injuries is the car, and the damages Galati suffered are connected with the car. While Embargo’s relationship to Galati’s injury would be the same whether Galati was injured by falling in a ditch or by being hit by a car, it is the car’s relationship to Galati’s injuries that controls this dispute.”

It’s Still Covered: Insured Settles Claim Without Insurer’s Consent

When an insured settles a claim without its insurer’s consent, the insurer will often be reluctant to provide coverage, on the basis that the insured made an impermissible voluntary payment. But it’s not always that simple, as we see in TSL Transportation Solutions, Inc. v. Cruz, No. 17-2158 (D.P.R. Feb. 9, 2021).

The insured gave notice of a claim to its insurer, but then settled with the claimant while the claim was still pending. The nature of the claim is not important for purposes here. What is important is that the claimant, Costco, was the insured’s biggest customer – making up 80% of its business. Costco was placing tremendous pressure on the insured to resolve the matter. The insured made the payment in an effort to save its business.

The insurer denied the claim on the basis that the insured breached the policy’s voluntary payments provision. When this happens, the issue of coverage sometimes turns on whether the insurer must prove that it was prejudiced by the voluntary payment, and, if so, was it?

The Puerto Rico court noted that U.S. states are “unsurprisingly split” as to whether prejudice is required. After taking a look at how some states handle the issue, the court concluded that, as far as Puerto Rico law was concerned, prejudice was required -- and the insurer could not prove that it had suffered any.

Key to the court’s decision was that the insured’s liability for the claim was clear and it involved liquidated damages. In that situation, the court concluded that prejudice was not satisfied based on the insurer’s “metaphysical claims of interference with its investigation and its rights that amount to nothing more than tautological claims of prejudice. There is simply no evidence that MAPFRE has been materially prejudiced at all in its ability to investigate, defend or recoup the Loss from others.”

The court was also persuaded by the District of Massachusetts’s 1995 decision in New England Extrusion v. American Alliance Ins. Co.: “‘[I]t would have been grossly unfair to [the insured] to require it to delay resolution of the claim and jeopardize its relationship with an important customer to satisfy a technicality in the policy with no risk of prejudice to the insurer.’ The Court recognizes, of course, that, had MAPFRE been able to demonstrate prejudice, the business reason for TSL’s payment would not save the day for TSL -- at least from a prejudice perspective. The apparent reason TSL chose to make reparations to its biggest client as to what it believed was an undisputed and indisputable loss was to preserve that relationship, and, by extension, its own business. These facts are not necessary to decide the issue, but merely illustrate the hard business realities that undergird ‘considerations of sound public policy’ that this Court rules would also be persuasive to the Puerto Rico Supreme Court.”

Insurer’s ROR Silent On A Limits Issue: Was It Waived?

In Stacy v. Bar Plan Mutual Ins. Co., No. ED108576 (Ct. App. Mo. Jan. 26, 2021), the court addressed whether an insurer waived the right to assert a coverage issue on account of having not included it in its reservation of rights letter. The issue involved whether the coverage situation was a single claim versus multiple claims.

The court set out the general rule, which, ordinarily, may have doomed the insurer: “[A]n insurer must effectively inform the insured if the insurer believes it may not be required to extend the coverage provided under the policy. Defending an action with knowledge of noncoverage under a policy of liability insurance without a proper and effective reservation of rights in place will preclude the insurer from later denying liability due to non-coverage.” (emphasis in original).

But, here, the insurer caught a break. The court concluded that the general rule did not apply to an issue concerning the extent of an insurer’s limit of liability: “In contrast, the limit of the insured’s liability under an insurance policy is generally not considered a defense to coverage. Missouri law recognizes a critical distinction between the assessment of what conduct is covered under the policy and the assessment of the financial limit of the insurer’s liability for conduct that is covered under the Policy. In other words, a question of what is covered is distinct from a question of how much is covered. . . . It is well settled that an insurers communication to the insured of the limits of liability is not a statement denying coverage. Thus, an insurer’s failure to communicate the limits of liability neither constitutes a breach of the policy nor waives the applicable limits of liability.”

Supreme Court Addresses When A D&O Insurer Can Withhold Consent Of A Settlement

In Apollo Education Group, Inc. v. National Union, No. 19-0229 (Ariz. Feb. 17, 2021) the Supreme Court of Arizona answered the following question from the 9th Circuit Court of Appeals:

“What is the standard for determining whether National Union unreasonably withheld consent to Apollo’s settlement with shareholders in breach of contract under a policy where the insurer has no duty to defend?”

The Arizona high court clarified the question by asking: “Should the federal district court assess the objective reasonableness of National Union’s decision to withhold consent from the perspective of an insurer or an insured?”

Held: “[U]nder a policy without a contractual duty to defend, the objective reasonableness of the insurer’s decision to withhold consent is assessed from the perspective of the insurer, not the insured. The insurer must independently assess and value the claim, giving fair consideration to the settlement offer, but need not approve a settlement simply because the insured believes it is reasonable.”

The court’s explanation, of what the insurer must do, to act reasonably, is lengthy. I set it out here in full. Of note, the court stated that considerations of coverage are in play, as well as adding this: “The insurer may, however, discount considerations that matter only or mainly to the insured—for example, the insured’s financial status, public image, and policy limits—in entering into settlement negotiations.” The Arizona Supreme Court’s full explanation (citations omitted):

“To act reasonably, the insurer is obligated to conduct a full investigation into the claim. The Court has described the insurer’s role as an almost adjudicatory responsibility. To carry out this responsibility, the insurer evaluates the claim, determines whether it falls within the coverage provided, assesses its monetary value, decides on its validity and passes on payment. The company may not refuse to pay the settlement simply because the settlement amount is at or near the policy limits. Rather, the insurer must fairly value the claim. The insurer may, however, discount considerations that matter only or mainly to the insured—for example, the insured’s financial status, public image, and policy limits—in entering into settlement negotiations. The insurer may also choose not to consent to the settlement if it exceeds the insurer’s reasonable determination of the value of the claim, including the merits of plaintiff’s theory of liability, defenses to the claim, and any comparative fault. In turn, the court should sustain the insurer’s determination if, under the totality of the circumstances, it protects the insured’s benefit of the bargain, so that the insurer is not refusing, without justification, to pay a valid claim.”

Owner of LLC Not An Insured Under Policy Issued To: His LLC

You own a company. You expect to an insured under a liability policy issued to it. Right? So what happened in Whiting v. Kulhanek, No. 2019AP1568 (Ct. App. Wis. Feb. 2, 2021)? The case is an important one. I have seen insurers overlook this defense when addressing coverage for individual defendants – especially, as here, when the individual is the owner of the named insured.

Wayne Kulhanek owned a building in Rhinelander, Wisconsin. He leased space in the building to NOW Equipment LLC, which sold and reconditioned restaurant equipment. Kulhanek was the sole member of NOW Equipment LLC. Another portion of the building contained a garage, which Kulhanek leased to Kevin Mathison for a transmission repair business. Mathison went to jail for a few months during the lease period. At the time, he was several months behind on his rent.

While Mathison was locked up, Kulhanek went looking for another tenant for the garage space. In doing so, Kulhanek contacted a junk dealer who came and removed property from the garage. The junk dealer did not pay for the property removed. After Mathison was released from jail, Kulhanek allowed him access to the garage to remove his property. Mathison discovered that some of his personal property was missing, as well as automobile parts owned by a customer. Mathison and the customer sued Kulhanek for negligent bailment and conversion.

Auto Owners issued a commercial general liability policy to NOW Equipment LLC. As a limited liability company, insured status was also afforded to the LLC’s members, but only respect to the conduct of NOW Equipment LLC’s business.

The court concluded that, while Kulhanek was a member of NOW Equipment LLC, it was not an “insured” for purposes of the Mathison suit. The court explained its decision:

“We conclude Kulhanek was not an insured under the unambiguous language of the policy. He was not named as an insured—rather, the policy clearly designated NOW Equipment LLC as the named insured. Kulhanek was a member of the LLC, but as a member, Kulhanek could receive coverage only while engaged in the conduct of the LLC. According to the unambiguous language of the insurance policy, Kulhanek could therefore only be an insured as a member of the LLC with respect to the conduct of NOW Equipment LLC’s business.

Under the policy, property management cannot reasonably be considered part of the conduct of NOW Equipment LLC. Kulhanek testified at his deposition that NOW Equipment LLC was in the business of refurbishing and selling restaurant equipment. The business description on the policy's declarations page listed the LLC’s business as ‘Refrigerator Refurb.’ Under either description, NOW Equipment LLC was not in the business of commercial property rental, and any actions Kulhanek took in his role as Mathison’s landlord were therefore not part of the conduct of NOW Equipment LLC's business.”

Indiana Supreme Court To Decide Bad Faith Failure To Settle Between Primary And Excess

At issue in Cincinnati Ins. Co. v. Selective Ins. Co., No. 18-956 (S.D. Ind. Feb. 25, 2021) is a dispute between Cincinnati, a primary insurer, and Selective, an excess insurer, where the two settled an auto claim involving serious injuries.

Cincinnati alleged that Selective acted negligently and in bad faith in refusing to settle the case sooner.

Normally the situation is the other way around -- The excess insurer argues that, on account of the manner in which the primary insurer handed the settlement, the excess insurer suffered damages. The court’s opinion does not explain the nature of the dispute between the two insurers.The Indiana federal court, on the basis that the Indiana Supreme Court has never held whether there is a cause of action for negligent failure to settle, and for other reasons, certified the following questions to Indiana’s top court: (1) Does Indiana law recognize a cause of action against an insurance company for the negligent failure to settle a claim within policy limits?; and (2) Does Indiana law recognize the doctrine of equitable subrogation, thus permitting an excess insurance carrier to directly sue a primary carrier for the negligent and/or bad faith failure to settle a claim within policy limits?”

|

| |

|

|

|

| |

| |

|

|

|

|

|

|

|

|

|