|

|

|

|

|

| |

|

Vol. 8 - Issue 7

August 21, 2019

|

|

|

|

|

|

| |

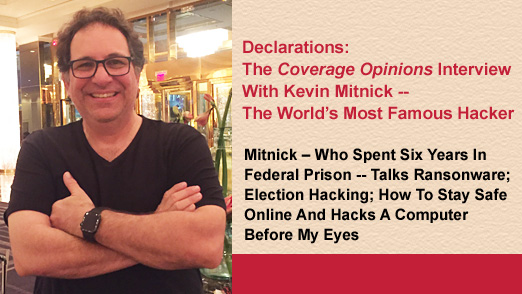

This issue's interview has a special twist – it first appeared as "The Weekend Interview" in The Wall Street Journal. For someone who loves to interview interesting people, the opportunity to do it for the WSJ's editorial page was a really neat experience.

For this I traveled to Las Vegas (man it was hot) to interview Kevin Mitnick, the world's most famous hacker. Mitnick spent six years in federal prison for various computer and phone hacking crimes. He now works as a "white hat," a hacker who is paid to break into companies' systems to find vulnerabilities that the real bad guys could exploit. Mitnick shared with me his thoughts on the recent surge in ransomware attacks, election hacking and how to stay safe online. Oh, and he hacked a computer in front of my eyes!

You can check it out here:

http://coverageopinions.info/WallstreetMitnick.pdf

|

|

|

|

| |

| |

| |

|

|

|

Vol. 8 - Issue 7

August 21, 2019

Insurance For Life's Petty Problems

|

|

|

|

|

| |

If I made the effort, I could find all kinds of technical definitions of insurance. But the best definition of insurance is the simplest – paying to get paid when something goes wrong. What these things-that-could-go-wrong could be are extraordinarily diverse and practically endless. But, for the most part, they have one thing in common: when one happens, it's pretty bad – disease, death, catastrophic injury, all manner of property losses, financial losses, and on and on and on.

Thankfully, despite paying for the chance to get paid, when something goes wrong, you usually don't see any money. And that's a really good thing. But, of course, sometimes it leaves you feeling like you haven't gotten your money's worth. Like -- Good news, I didn't die. Bad news, that pesky life insurance company took my money – again -- and did nothing for it. Nothing. They are stealing my money. Robbing me blind, I tell you.

Recognizing that most things that go wrong in life are not catastrophic, but that buying insurance, and not using it, feels like a bad deal, Irritated Insurance Company has set out to solve this problem. The company has introduced a new policy – The Peeved Insurance Plan. It provides insurance for life's petty problems. These are problems that are, of course, extraordinarily insignificant. But, at the time they are happening, leave you believing that the world is conspiring against you. Now, with the Peeved Insurance Plan, you can be compensated for having to face life's little annoyances.

Here's the real selling point of IIC's policy. Unlike that term life policy or umbrella policy, where you'll likely never get any dough back, with the Peeved Insurance Plan, the insurer expects to send some of your money back.

For a $60 annual premium, IIC will pay you $10 per petty problem, up to a $100 annual petty problem aggregate, in the event you are forced to confront a petty problem. Sure, $10 won't solve it, but at least you'll know that someone out there recognizes your suffering and feels your pain, as it's costing them money. IIC also boasts the policy's simplicity – just one page and a two-page nuclear exclusion (always gotta have that nuclear exclusion).

The Peeved Insurance Plan provides coverage for the following "specified petty problems:"

· Look at this! I ordered Diet Coke. This is Diet Pepsi.

· This is outrageous! They forgot to give me a little cup for my soy sauce.

· Six minutes? Huh? The app just said that the car will be here in four minutes! What, is the guy driving in reverse?

· Oh come on! Do you really need to include every country on the planet in the drop down menu? Just how many toasters did you send to Papua New Guinea last year?

· Hellooo! You're out of napkins. How hard is it to keep an eye on this?

· I can't sit here! This table is wobbly. Look at this ( ( ( shaking ) ) )!

· Would it kill businesses in NYC to include the cross street in their address? Sorry, my bad, I don't know where 320 Broadway is.

· I can't believe this. The barista spelled my name wrong on my cup. It's Alan. One l. If you weren't sure, you should have asked.

· Would you look at that! He has twelve items in his basket! Twelve! One, two, three, four . . . Hey buddy, last I checked, twelve is greater than ten. Twelve has the big fish mouth facing it.

· You call this water pressure? I've seen water pistols stronger than this. Don't tell me this is just a $59 a night hotel. The little sign on the back of the door says it's $700.

· Are you kidding me? Another preview? Will this movie ever start? I'm paying them for their advertisements. This is ridiculous.

· No, don't tell me! Please! Please! This can't be happening. My Mike and Ikes are stuck on the second coil. I'm going to shake this machine. If I break it, it's their fault.

|

That’s my time. I’m Randy Spencer. Contact Randy Spencer at

Randy.Spencer@coverageopinions.info |

|

| |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Vol. 8 - Issue 7

August 21, 2019

Encore: Randy Spencer’s Open Mic

Man Sues Dog: Court Finds That Insurer Has Duty To Defend German Shorthaired Pointer

|

|

|

|

|

|

| |

Frequent readers of Coverage Opinions know that I have a soft spot for coverage cases involving dogs. Sadly, they often involve dog bites. There’s just not much litigation over dogs licking faces. In general, the story is similar. Dog bits man. Man sues dog’s owner. Dog’s owner sues his insurance company.

The recent decision in Morrison v. Sioux Falls Mutual, No. 2014-2469 (So. Central Dist. Ct., N.D. Mar. 23, 2015) takes a different route. A really different route. Dog hurts man. Man sues dog. Yes, you read that right -- Man sues dog. Dog’s owners sue their insurance company. Court holds that insurer had a duty to defend -- the dog.

Believe me. I know. It sounds like one of those cases that people like to point to as evidence that the legal system is broken. The ones that tort-reformers discuss and then immediately need a paper bag to breath into. But as crazy as it sounds, the court’s decision actually followed well-established coverage law.

Morrison involves coverage for an unfortunate canine incident. Tom Robertson purchased some furniture from Rick and Sharon Morrison that he found on Craig’s List. Robertson’s car wasn’t big enough to enable him to transport all of the furniture in one trip. And since he lived about 75 miles away from the Morrisons’ home in Bismark, North Dakota, Robertson completed the purchase by making trips on three consecutive Saturdays.

The Morrisons had a dog – a German Shorthaired Pointer named Felix. Robertson was a life-long dog lover but did not own one on account of his wife’s allergy to pet dander. On all three trips to the Morrison’s house, once the furniture was loaded into Robertson’s car, Robertson spent time talking to the Morrisons and playing with Felix. By the third visit, Robertson and the Morrisons had become friendly and Robertson couldn’t get enough of Felix. At one point Felix walked into the room with his leash in his mouth -- indicating that he wanted to go for a walk. Rick Morrison suggested that Robertson take Felix on his walk. Robertson agreed without hesitation. Morrison showed Robertson the route that Felix like to take and off they went.

Robertson and Felix got about a block from the house when Felix spotted a squirrel. He bolted. Hard. Robertson had no warning and the force of the 60 pound dog pulled him down. Robertson suffered bumps and bruises and a badly sprained wrist.

Robertson sued the Morrisons in small claims court. Perhaps because his injuries were not too serious, he acted pro se. Robertson alleged that the Morrisons failed to warn him that Felix, being a German Shorthaired Pointer, was a hunter. Thus, having owned Felix for two years, the Morrisons surely knew that if Robertson didn’t hold the leash tightly, with minimal slack, he would be pulled down if Felix saw a squirrel or rabbit and went after it. Robertson named as defendants Rick and Sharon Morrison. Then, in a very odd move, Robertson named “Felix Morrison” as a defendant.

The Morrisons sent the complaint to Sioux Falls Mutual, their homeowner’s insurer. The insurer denied coverage, including a defense, on the basis that Robertson’s injuries were not caused by an “occurrence,” defined as an accident. The insurer relied on the statement in the complaint that, having owned Felix for two years, the Morrisons knew that if Robertson didn’t hold the leash tightly, he would be injured if Felix’s hunting instincts took over. The disclaimer letter made no mention of potential coverage for Felix.

The Morrisons and Robertson settled the matter for $1,500. The Morrisons then filed suit against Sioux Falls Mutual. A small amount, but the Morrisons’ counsel included a count for bad faith.

The court held that coverage was not owed to the Morrisons for a defense nor its $1,500 settlement. The analysis was brief. The court essentially adopted Sioux Falls’s argument that, because the Morrisons owned Felix for two years, they must have known that if Robertson didn’t hold the leash tightly, he would be injured if Felix saw a squirrel.

But that was not the end of the case. The court observed that Sioux Falls’s disclaimer letter made no mention of any potential coverage owed to defendant “Felix Morrison.” The court acknowledged that it was an absurdity that a dog could be named as a defendant in a law suit – and then have rights to a defense under its owner’s insurance policy. But the court focused on the black letter insurance rule that an insurer is obligated to defend complaints even if they are “groundless, false or fraudulent.” As the court saw it: “It that rule is to have any meaning, then an insurer is obligated to defend a dog that is named in a lawsuit.”

Of course, the obligation to defend Felix only existed if Felix were an “insured” under his owner’s homeowner’s policy. And the court had little troubling concluding that he was. The policy’s definition of insured was: “The named insured and, if residents of your household: your relatives; and any person under the age of 21 who is in the care of the Named Insured.” The court cited to the Supreme Court of Texas’s decision in Strickland v. Medlen, 397 S.W.3d 184 (Tex. 2013), where the Texas high court observed that: “America is home to 308 million humans and 377 million pets. In fact, American pets now outnumber American children by more than four to one. In a nation where roughly 62% of households own a pet—with about 78 million dogs and 86 million cats (and 160 million fish)—it is unsurprising that many animal owners view their pets not as mere personal property but as full-fledged family members, and treat them as such.” Id. at 187 (citations and internal quotes omitted). “A study found that 70% of pet owners thought of their pets as family members.” Id. (citation omitted).

Thus, having concluded that Felix was a resident “relative” of the named insured, he qualified as an “insured” under the Sioux Falls policy. And since there was no allegation in the Robertson complaint that Felix, unlike his owners, breached any duty to warn, the court held that a defense was owed to Felix. The court also observed that “insured” included a person under the age of 21 who is in the care of the Named Insured, but the policy did not require a resident “relative” to be a person. Thus, at a minimum, the policy was ambiguous and was required to be interpreted in favor of coverage.

Lastly, the court took issue with the fact that Sioux Falls’s disclaimer letter made no mention of potential coverage for Felix. The court cited to a North Dakota insurance reg. that required Sioux Falls to respond to claims of all insureds it in a timely manner. Having failed to do so for Felix, the court refused to dismiss the bad faith count filed against Sioux Falls.

As ridiculous as the opinion is, it is hard to say that it is not supported by the policy language and case law. A ruff decision for Sioux Falls Mutual.

|

That’s my time. I’m Randy Spencer. Contact Randy Spencer at

Randy.Spencer@coverageopinions.info |

|

| |

|

| |

|

|

|

|

Vol. 8 - Issue 7

August 21, 2019

Coming Soon (Finally): Insurance Key Issues Half-Price Sale

|

|

|

| |

|

| |

Sales of Insurance Key Issues have been humming along so the price has been full retail for a long time.

I am pleased to report that Key Issues will soon be having a half-price sale. I know I said this in the last issue but it really is going to happen. Soon.

So, if you’ve been on the fence about making a purchase, or would like an extra copy, to avoid having to share with someone you don’t like, this will be your chance.

Stay tuned.

|

|

|

| |

|

|

|

Vol. 8 - Issue 7

August 21, 2019

I Just Never Get Tired Of Saying This

|

|

|

|

|

| |

I have been saying this for years: Elvis Loves To Tender.

And legendary Elvis impersonator, Pete “Big Elvis” Vallee, is no exception.

I recently had the chance to see the “Big Elvis” show in Vegas. Close your eyes and you’d think The King was in the room. It is easy to see why Time magazine called Pete “Big Elvis” Vallee one of the top ten tribute artists of all time. In February 2017, Pete was inducted into The Las Vegas walk of Stars!

Pete takes requests. I hit him with “Bossa Nova Baby” from Elvis’s 1963 film Fun in Acapulco. Pete nailed it, even doing Elvis’s dance steps that went with the song.

If you are going to be in Vegas you must check out the (free) Big Elvis show at Harrah’s!

Pete was a good sport and happily posed with the current issue of Coverage Opinions. |

| |

|

| |

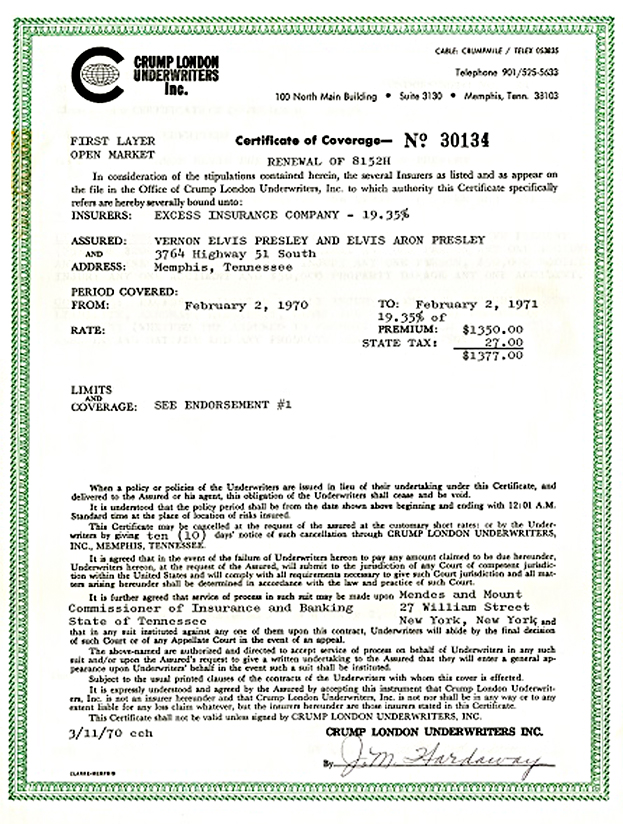

By the way, here is a picture of a renewal certificate from some sort of 1970 excess policy issued to Elvis at his Graceland address [3764 Highway 51 South, before it became 3764 Elvis Presley Boulevard.] This appeared in the July 18, 2018 issue of Coverage Opinions. Elvis Presley Enterprises, Inc. kindly licensed the picture to me to share with CO readers. |

| |

|

| |

| |

| |

|

|

Vol. 8 - Issue 7

August 21, 2019

|

|

|

|

|

|

| |

July 31st was the 50th anniversary of Elvis Presley’s seven-year run of 636 sold-old shows at The International Hotel and The Hilton in Las Vegas. August 16th was the 42nd anniversary of The King’s death.

Given Elvis’s place not only in music, but American culture at large, it is not surprising that he appears in many judicial decisions, in several forms. These include disputes over intellectual property rights, references to his songs and simply his place as a cultural icon.

Here are some of the many decisions where The King went to court:

Gentry v. Carnival Corp., 2012 U.S. Dist. LEXIS 64269 (S.D. Fla. May 8, 2012): Addressing a motion to compel discovery, Judge Jonathan Goodman, of the Southern District of Florida, made this observation: “Counsel often assume that when opponents withhold documents upon a claim of privilege, that they do so because they are in fact sitting on a smoking gun. Consequently, counsel propounding discovery often suspect automatically that the opponent is asserting the work product doctrine because the adversary is trying to hide significant, adverse evidence.” Judge Goodman, as he is wont to do*, compared this situation to a rock song, here, Elvis’s 1969 chart-topping “Suspicious Minds,” which Judge Goodman noted includes this lyric: “We can’t go on together with suspicious minds, and we can’t build our dreams on suspicious minds.”

*Judge Goodman’s use of rock music references in his opinions -- including Bruce Springsteen and Tom Petty -- has been discussed in prior issues of Coverage Opinions. In the October 11, 2017 issue of CO I declared him the “Hippest Federal Judge in America.”

Curtin v. Star Editorial, Inc., 2 F. Supp. 2d 670 (E.D. Pa. 1998): The court, addressing a copyright dispute over certain photographs of Elvis, had these parting words: “We realize that this opinion is not likely to be music to the ears of either side. While we cannot stand in anyone's shoes, blue suede or otherwise, it is possible that the parties, as Elvis devotees, are lamenting ‘Don't Be Cruel’ and ‘you ain’t no friend of mine.’ It is not totally farfetched that they may be feeling ‘All Shook Up,’ or agonizing that this court is nothing but a ‘Heartbreak Hotel.’ The parties may even wish that this opinion be ‘Returned to Sender.’ Nonetheless, we, like a hound dog, must follow the law.”

Zoe v. Zoe, 2014 N.J. Super. Unpub LEXIS 3078 (N.J. Super. Ct. Chancery Div. Jan. 23, 2014): In a custody case, a plaintiff-father alleged that the defendant-mother abused her parental discretion by taking their eleven year old daughter to a Pink concert. The father argued that the show was age-inappropriate due to alleged profanities in some of Pink’s songs and sexually suggestive themes and dance performances during the show. The court, six ways to Sunday, concluded otherwise.

The court noted: “Some of the most famous and time-honored names in rock music history were, in the 1950’s and 60’s, the subject of parental and cultural concern, social disapproval, and even direct censorship. Perhaps the most notorious example concerned Elvis Presley, now universally known as the King of Rock and Roll. As chronicled in Parental Advisory, Presley’s live performances and on-stage gyrations were in their early days considered highly controversial, and caused a great deal of consternation among adults convinced that he, his music, and his performances were obscene. Numerous concert promoters ‘washed their hands of the young King of Rock and Roll, fearing the repercussions of presenting the singer and his music.’ . . . [I]n 1955, Presley was threatened with arrest in Florida on obscenity charges if he gyrated onstage while performing his music. In 1956, officials in San Diego issued a warning to Presley that he would not be allowed to perform in the city unless he removed all dancing and gestures from his performance. In Presley’s 1957 television appearance on the Ed Sullivan Show, cameramen were reportedly instructed to show the performer only from the waist up so that television audiences could not see Elvis’ gyrating hips.”

Patel v. Tex. Dep’t of Licensing & Regulation, 469 S.W.3d 69 (Tex. 2015): In a decision addressing Texas cosmetology licensing, the Texas Supreme Court discussed the licensing distinction between cutting hair and shaving a beard: “Even the Attorney General of Texas got all shook up wondering whether Elvis’s famous sideburns ‘were hair which a cosmetologist might trim, or a partial beard which could be serviced only [by] a barber.” In a footnote: “(Tex. Att’y Gen. Op. No. JC-0211 (2000) ‘We think it likely that most observers would consider the sideburns worn by the late Elvis Presley at the time of his early success in 1956 as part of his hair. On the other hand, whether the muttonchops which adorned his face at the time of his death were hair which a cosmetologist might trim, or a partial beard which could be serviced only by a barber, is a question which in the absence of any articulated standard might well present difficulties to a cosmetologist who wished to remain within his or her licensed practice.’”).

Gibbons v. Arpaio, No. 07-1456 (D. Ariz. Oct. 11, 2017): A pre-trial detainee of a Maricopa County jail filed suit against Maricopa County Sheriff Joe Arpaio, alleging that his constitutional rights were violated in several ways, including his Eighth Amendment rights, on account of Arpaio’s policy of playing such songs as “I Fought the Law and Law Won,” and “Jailhouse Rock” at a loud volume over the public address system. The court denied the claim, concluding that “the broadcasting of music over the public address system might be deemed petty or insulting, but such actions also do not rise to the level of constitutional violations.”

Elvis Presley Enterprises v. Capece, 141 F.3d 188 (5th Cir. 1998): In an opinion by, eh, Judge King, the court addressed whether The Velvet Elvis, a nightclub, infringed certain intellectual property rights owned by Elvis Presley Enterprises, Inc. The club décor included a velvet painting of Elvis. The bar’s menu included “Love Me Blenders,” a type of frozen drink; Elvis’s favorite, peanut butter and banana sandwiches and a hot dog called “Your Football Hound Dog.” In addition, The Velvet Elvis’ advertisements included such phrases as “The King Lives,” “Viva la Elvis,” “Hunka-Hunka Happy Hour” and “Elvis has not left the building.”

|

| |

|

| |

|

|

|

|

Vol. 8 - Issue 7

August 21, 2019

The Theory Of Evolution And The Practice Of Law

|

|

|

| |

|

| |

Sorry for the shameless plug for Insurance Key Issues.

|

|

|

| |

|

|

|

|

Vol. 8 - Issue 7

August 21, 2019

Answer To The Insurance Coverage Crossword Puzzle

|

|

|

| |

|

|

|

| |

|

|

|

|

Vol. 8 - Issue 7

August 21, 2019

Proof That Insurance Is Amazing!

|

|

|

| |

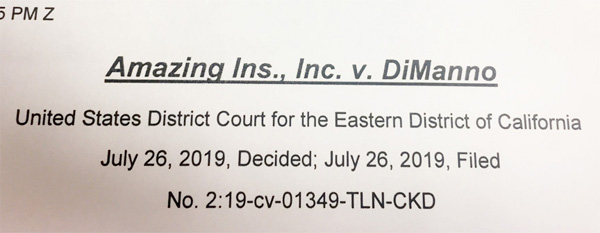

I certainly couldn’t let this go by without comment. Late last month the Eastern District of California issued a decision in Amazing Insurance, Inc. v. DiManno.

|

|

|

| |

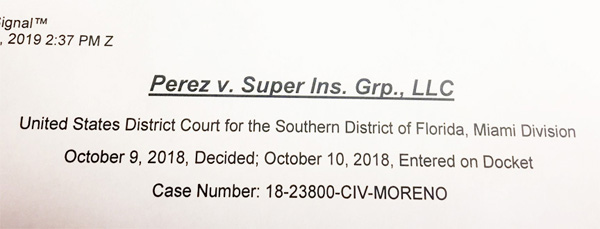

Here is Amazing Insurance Inc.’s biggest competitor: |

| |

|

| |

| |

| |

| |

| |

|

|

|

|

Vol. 8 - Issue 7

August 21, 2019

New Coverage Opinions Series: Roadside America: Lawyer Style

See The World’s Largest Warning Signs

|

|

|

| |

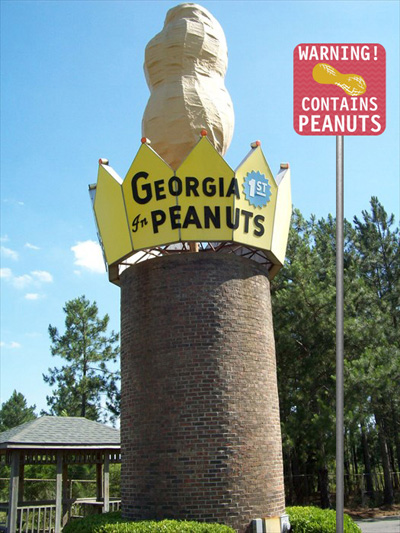

In the last issue of Coverage Opinions I pointed out that Ishpeming, Michigan is the home of “Big Gus,” the world’s largest working chainsaw at 23 feet long.

I also pointed out that visitors to “Big Gus” will now get the added bonus of seeing the world’s largest warning sign. Click here in case you missed it.

I had so much fun with the “Big Gus” piece in the last issue that I have decided to make this a series. Until I get tired of it, each issue of CO will feature a world’s largest object and a massive warning sign to keep visitors safe and lawyers at bay.

If your summer road trip will have you in the vicinity of Ashburn, Georgia, you can see the world’s largest peanut and massive warning sign. [In fact, sadly, the world’s largest peanut was severely damage in 2018 by Hurricane Michael. One estimate to fix it was $20,000. Not sure if that happened. If not, just pretend it was repaired.]

|

| |

|

|

|

| |

|

|

|

| |

|

Vol. 8 - Issue 7

August 21, 2019

Court Addresses The “Confusion Doctrine” And It’s – You Guessed It…

|

|

|

| |

The law loves doctrines. There’s the Erie Doctrine, the Reasonable Expectations Doctrine, the Doctrine of Last Clear Chance and the list goes on and on. As I see it, a doctrine is just a rule that had a good P.R. department, that was able to elevate it to a more important sounding “doctrine.”

Add this to this list. I recently came across the “Confusion Doctrine.” Really.

“Under the well-named confusion doctrine, ‘[w]hen the qualities of obligee and obligor are united in the same person, the obligation is extinguished by exhaustion.’ La. Civ. Code Ann. art. 1903. ‘[A]n obligation is said to be extinguished by confusion when a person is placed in the position of owing the obligation to himself.’ Langley v. Police Jury of Calcasieu Parish, 201 So. 2d 300, 304 (La. App. 3d Cir. 1967) (en banc) (quotation omitted); see, e.g., Matter of Dibert, Bancroft & Ross Co., Ltd., 117 F.3d 160, 170-71 (5th Cir. 1997) (confusion arises, for example, when a ‘promissory note that is secured by [a] mortgage is acquired by its maker’ or ‘an encumbered building is acquired by the mortgagee’ (emphasis omitted)). ‘For confusion to occur the same person must acquire the full and perfect ownership of both sides of the obligation.’” Lloyd’s Syndicate 457 v. Am. Global Mar. Inc., 346 F. Supp. 3d 908 (S.D. Tex. 2018).

So, if the “confusion doctrine” means that, when the qualities of obligee and obligor are united in the same person, the obligation is extinguished by exhaustion, how do you explain this definition provided by the North Dakota Supreme Court in City of Bismarck v. King, 2019 ND 74 (2019): “The ‘confusion doctrine’ provides that when an arresting officer introduces the question of a drunken-driving suspect’s right to counsel by giving a Miranda warning prior to requesting a chemical test, the suspect’s subsequent refusal to take a test until an attorney is consulted may not constitute a ‘refusal to submit’ to a chemical test.’ We further explained the confusion doctrine does not apply when the officer explicitly informs the driver that the Miranda rights do not apply to the taking of a chemical test pursuant to the implied consent law.”

But wait, it gets even more, well, you know….

There is also a Reverse Confusion Doctrine in the trademark context, where a “large junior user saturates the market with a trademark similar or identical to that of a smaller, senior user such that the public comes to assume that the senior user’s products are really the junior user’s or that the former has become somehow connected to the latter.” Fortres Grand Corp. v. Warner Bros. Entm’t, Inc., 947 F. Supp. 2d 922 (N.D. Ind. 2013).

|

|

|

| |

|

|

|

|

Vol. 8 - Issue 7

August 21, 2019

Court Provides Rate Warning To Independent Counsel

|

|

|

| |

We've all seen this in a reservation of rights letter. And, if you are on the insurer-side of things, you've probably written it yourself.

An insurer receives a new claim, the clock is ticking for the defendant-insured to respond, but the insurer has not yet determined if it owes a defense. So it sends a letter to the insured saying something along the lines – although perhaps not exactly (as discussed below) -- of what Hartford did as described in Hartford Casualty Ins. v. Swapp Law, PLLC, No. 17-1130 (D. Utah Aug. 1, 2019).

The insurer stated: "At this time . . . Hartford has not yet made a determination as to whether [Swapp Law] is entitled to coverage in connection with the [Underlying Action]. In the interim, we suggest that you retain your own attorney to protect your interests in this matter. In the event we determine that coverage may exist and we agree to defend this suit, we will reimburse you only for those reasonable legal costs and fees incurred by you for the defense of this action . . . While the issue of what constitutes 'reasonable legal costs and fees' may not be apparent to you, the legal community doing defense work in this area is well aware of the acceptable scale. You may wish to contact the undersigned prior to hiring an attorney since charges considered to be above the acceptable scale could result in our not covering your legal costs and fees in their entirety."

The Swapp Law firm was seeking coverage for a claim that it violated the federal Driver's Privacy Protection Act (18 U.S.C. § 2721 et seq.) "by purchasing accident reports from the Washington State Patrol and using the personal information gleaned from the reports to mail motorists unsolicited Swapp Law advertisements."

Two days after getting Hartford's letter, Swapp retained the Lane Powell law firm to defend the action. Swapp's coverage counsel provided Hartford with the hourly rates for the Lane Powell lawyers: Barbara Duffy ($645), Ryan McBride ($540) and Aaron Schaer ($310).

A representative of Hartford responded that the company would make "an accommodation on this one case only to accept" the rates charged by Duffy and McBride. Hartford advised that all other timekeepers would be paid at $195 per hour for associates and $100 for paralegals.

One week after agreeing to defend, under a reservation of rights, Hartford filed an action seeking a declaration that it had no duty to defend or indemnify Swapp Law in the Underlying Action. The court granted Hartford's motion for judgment on the pleadings, finding that the claims against Swapp Law were excluded from coverage and Hartford had no duty to defend.

At issue before the court now -- Swapp Law seeking payment for the full amounts billed by Lane Powell.

The court's decision did not require it to address the extent of Hartford's obligation for any Lane Powell fees over $195 per hour for associates and $100 for paralegals. The court held that, because Hartford had no duty to defend, it had no obligation to pay Swapp's legal fees – even those incurred up until the court's no duty to defend decision was made. This gets to a separate issue in the case of Hartford's right to reimbursement of defense costs.

However, the court also explained that, even if Hartford did have a duty to pay Swapp Law's legal fees prior to the determination that it had no duty to defend, "Swapp Law acted unreasonably by hiring Lane Powell and failing to confirm with Hartford that Lane Powell's rates would be reimbursed."

I'll let the court describe it from here. It is worth hearing it in full as well as with the court's tone:

"In Hartford's August 15, 2017 letter to Swapp Law acknowledging Hartford's notice of the Underlying Action, Hartford stated that Swapp Law would be reimbursed only for 'reasonable' legal costs and fees. That letter further stated that 'the legal community doing defense work in this area is well aware of the acceptable scale' of legal costs and fees. Finally, the letter warned Swapp Law that, in order to ensure reimbursement, Swapp Law may wish to confirm before hiring an attorney what rates Hartford will consider to be reasonable. And, as evidenced by attorney Humphery's February 2, 2018 email, Swapp Law was clearly aware of the precise rates Hartford considered to be reasonable.

On the basis of Hartford's August 15, 2017 letter, and Swapp Law's knowledge of Hartford-approved rates, Swapp Law knew, or should have known, it would not be reimbursed for any and all attorneys' fees it incurred. In its August 15, 2017 letter, Hartford indicated that it considered a particular spectrum of legal fees and costs to be reasonable and therefore, eligible for reimbursement. Thus, Swapp Law was on notice that, to ensure it would not be saddled with unreimbursable attorneys' fees, it had an obligation to determine that range, whether by contacting Hartford directly or seeking the opinion of lawyers who perform this kind of defense work in the relevant area. Even without Hartford's warning about reimbursable attorneys' fees, Swapp Law—no stranger to the mechanics of insurance defense—would have been well aware that insurance companies don't merely write blank checks to fund the defense of potentially covered claims.

Only two days after receiving Hartford's letter, Swapp Law hired Lane Powell, under an engagement letter agreeing to pay multiple lawyers more than $500 per hour. Swapp Law may well have concluded that its potential liability flowing from the Underlying Action was so great that it needed lawyers who charged nearly three times what Hartford deemed reasonable, and further that it was willing to assume the difference between Lane Powell's rates and Hartford's reimbursement. Or Swapp Law may have merely overlooked Hartford's clear warnings about the rates it would reimburse. In any event, in light of these facts, Swapp Law incurred these attorneys' fees at its own risk, knowing that Hartford would not merely rubber stamp any attorneys' invoice it received. In sum, Hartford had no duty under the Policy to defend against the Underlying Action and Swapp Law incurred exorbitant attorneys' fees at its own risk. Thus, Hartford has no obligation to reimburse Swapp Law for the difference between the rates charged by Lane Powell and those approved by Hartford."

It is easy to see how policyholders would likely respond to this: Simply because Hartford stated that the "reasonable legal costs and fees" are $195 per hour for associates and $100 for paralegals does not make it so. Policyholders would likely say, as they invariably do in cases of this type, that the fees paid by insurers, to panel counsel, are not "market rates," but, rather, are agreed to by lawyers in exchange for a steady flow of work from an insurer, etc. You know the drill. And some courts have said that panel counsel rates are not market rates when determining the rate to be paid to independent counsel.

But putting that aside, what makes the situation here unique is the explicit warning that was included in Hartford's reservation of rights letter when addressing the fact that Harford's rates may be lower than the rates of the lawyers retained by Swapp Law. Granted, it may not have mattered if Swapp Law addressed the rate issue with Hartford, as it seems that Hartford had already told the law firm what its maximum rates were. But if Swapp Law had addressed the rate issue with Hartford, and been refused anything higher than $195, perhaps the court would have been more sympathetic to Swapp.

It's all a little confusing. Nonetheless, the take-away is that, by having this explicit warning, Hartford won over the court and may have kept the court from concluding that the reasonable rate is somewhere between $195 per hour and the Lane Powell rates. Of course, this is all a non-issue, as the court held that Hartford had no obligation to pay Swapp's legal fees, even those incurred up until the court's no duty to defend decision was made.

Again, it's confusing. But there is little doubt that Hartford, with the strong warning in its reservation of rights letter, put itself in the catbird seat for dealing with an insured that paid no heed to the Stag's warning.

|

|

| |

|

|

|

|

Vol. 8 - Issue 7

August 21, 2019

Montrose Endorsement Does Not Apply: Injury And Damage Not Same Enough

|

|

|

| |

As I’ve discussed lots of times in the past, in general, insurers have had mixed results in construction defect cases when it comes to enforcing the Montrose (known loss) endorsement (which, of course, hasn’t been an endorsement for years, but it hasn’t shed that label). Some courts have interpreted the Montrose provision narrowly and required a strict “sameness” (my term) between the “property damage” that existed pre-policy inception date and that which took place during the policy period, for which coverage was being sought. Further, it is the “property damage” itself that must be known by the insured prior to the policy period and not the cause of the “property damage.”

In Mesa Underwriters Specialty Ins. Co. v. Blackboard Insurance Specialty Co., No. 18-4410 (N.D. Cal. July 15, 2019), the California federal court declined to preclude coverage on the basis of a Montrose endorsement. Again, the pre- and post-policy period injury and damage was not sufficiently the same to trigger the applicability of the Montrose/known loss provision.

As is often the case when it comes to litigation over the Montrose endorsement, the decision is “insurer vs. insurer.”

NDO Group acquired a “single room occupancy,” long-term residential hotel located in Oakland. A number of low-income tenants resided there. NDO group began renovations on common areas and some units in the Hotel.

Over time, various tenants began to file suit against NDO, alleging a variety of claims in connection with the habitability of their units on account of the NDO construction work. The first complaint was filed on July 8, 2016. A first amended complaint, filed on July 21, 2016, alleged: “NDO Group directed ongoing construction and renovation activities that disrupted the quiet enjoyment of the plaintiffs’ homes and resulted in the constructive and wrongful evictions of tenants. The tenants were no longer being supplied heat, garbage pickup, or secure mail delivery. The apartments all around them were gutted to the studs, large holes were created in the ceilings of apartments (including apartment of a tenant-plaintiff), and construction debris was dumped down the holes. Some of the tenants were forced to vacate their units due to water leaks, failure to repair habitability defects, ongoing wrongful entries to their apartments, noise, dust, and a continuing nuisance resulting from the construction activities.”

A second amended complaint was filed on May 1, 2017 and a third amended complaint was filed on May 22, 2018. These amended complaints contained further allegations concerning an alleged lack of habitability of the units.

Mesa Underwriters undertook NDO’s defense. However, Mesa tendered the defense to Blackboard Insurance, which issued two one-year general liability policies to NDO covering the period from November 18, 2016 to November 16, 2018.

Blackboard argued that it had no duty to defend based on “no occurrence” and no “bodily injury” or “property damage” during the policy period. The court rejected both of these arguments.

Turning to the issue relevant here, Blackboard also argued that it had no duty to defend based on the Montrose endorsement. As Blackboard saw it, NDO knew, prior to its policy periods, that the “bodily injury” or “property damage” had occurred, in whole or in part” including any “continuation, change or resumption of such ‘bodily injury’ or ‘property damage’”

It is easy to see why Blackboard made this argument. The first complaint was filed on July 8, 2016. A first amended complaint was filed on July 21, 2016. These were both before the inception of the first Blackboard policy issued to NDO, which was November 18, 2016. Then, the complaints filed after November 18, 2016 contained further – and similar -- allegations concerning an alleged lack of habitability of the units.

But Mesa disagreed, arguing that each discrete injury claimed must be evaluated separately for this purpose. The court agreed with Mesa, concluding that the Montrose endorsement did not preclude coverage, as there was not enough sameness between the “bodily injury” and “property damage” that existed prior to inception of the Blackboard policies and that which took place during the policy period.

The court explained: “Here, while NDO Group may have been aware of some of the bodily injuries and property damage alleged before Blackboard’s coverage began on November 18, 2016, many of the alleged injuries and property damage occurred after the policy’s inception, including loss of electricity, bathroom facilities, damage to property due to water leaks in unit’s closet, a slip-and-fall injury to one tenant navigating an unlit stairwell, and a physical attack on another tenant by a construction worker on the Hotel project. These allegations raised a potential for coverage of new, distinct injuries and property damage not alleged to have been known to NDO Group prior to Blackboard’s policy period.”

The court pointed to a single, simple, word in the policy language to support this conclusion: The known-loss provision bars coverage of ‘property damage’ if the insured “knew that the “property damage” had occurred.” The court stated that “the use of the definite article [the] particularizes the subject which it precedes and indicates that the claimed damage must be the same as the known damage.”

Or, as I call it, the strict “sameness” test.

|

|

| |

|

|

|

|

Vol. 8 - Issue 7

August 21, 2019

Personal And Advertising Injury: Disparagement Of A Product Without Mentioning It

|

|

|

| |

I’ve always found this to be an interesting issue. Is coverage owed, for “personal and advertising injury,” if the insured says something about its own product and makes no mention of the claimant’s product. One theory is that, if a company touts its own product in a way that is not true, then its competitor’s product is, by implication, disparaged, if it does not also have the same supposed positive trait as the insured’s.

The facts that gave rise to the coverage issues in Albion Engineering Company v. Hartford Fire Insurance Co., No. 18-1756 (July 10, 2019) are not spelled out in detail. But, in general, the case involves coverage for “personal and advertising injury,” for disparagement, where the insured made no mention of the claimant’s product.

Albion Engineering sells products such as caulking guns and dispensing accessories. Albion’s competitor, Newborn, believed Albion had claimed its products were made in the United States when they were really made in Taiwan. Newborn sued Albion in the District of New Jersey, bringing claims for false advertising and product marking in violation of the Lanham Act and New Jersey tortious unfair competition through false statements and material omissions.

Albion sought coverage for the Newborn action under a commercial general liability policy issued by Hartford. The insurer refused to defend. Albion sued Hartford.

At issue was whether the Newborn action alleged “personal and advertising injury,” specifically, “oral, written or electronic publication of material that slanders or libels a person or organization or disparages a person’s or organization’s goods, products or services.”

The district court found in favor of Hartford and the Third Circuit affirmed. At the heart of the court’s decision was that, under New Jersey law, Newborn’s causes of action require publication of a false statement concerning another.

Here, the court concluded that Albion did not publish a false statement about Newborn: “For its Lanham Act claim, Newborn alleged that Albion made ‘false statements of facts, misrepresentations, and material omissions of facts of the geographic origin of the subject merchandise and the commercial activity of Albion in violation of . . . the Lanham Act.’ Newborn made materially similar allegations for its claim of unfair competition. The gravamen of Newborn’s suit, in other words, is that Albion lied about Albion’s products, not Newborn’s. Newborn never claims that Albion published false statements about Newborn’s products. Newborn’s suit therefore does not meet the requirements for coverage under the Hartford policy.” (emphasis in original).

The court also declined to conclude that Albion had “implicitly” defamed Newborn, concluding that New Jersey law did not recognize such a claim.

It is an interesting issue, as well as involving an interplay between coverage and the elements of the law controlling the underlying action. And how does that fit in with the issue of whether extrinsic evidence can be considered for purposes of determining an insurer’s duty to defend?

|

|

| |

|

|

|

|

Vol. 8 - Issue 7

August 21, 2019

Appeals Court Says Coverage Counsel Cannot Be Adverse To Former Insurer Client

|

|

|

| |

Plein v. USAA Casualty Insurance Company is not a coverage case per se. However, it is likely to be of interest to CO readers. It involves the ability of a lawyer to be adverse to a former client, specifically, an insurer client. As a general rule, this is permitted under rules of professional conduct, so long as the current case, where the lawyer is adverse to the former client, is not “substantially related” to the lawyer’s prior representation.

The issue arose this way. Attorney Joel Hanson filed a first party bad faith action, on behalf of the Pleins, against USAA. It had to do with USAA’s handling of a fire claim. The ins and outs of the bad faith claim are not important here.

A few months later, attorneys William Smart and Ian Birk, from the law firm Keller Rohrback LLP, associated with Attorney Hanson in the case against USAA. To be clear, Smart and Birk were still working at Keller Rohrback. They simply joined the Pleins’ team.

Here’s the rub. Keller Rohrback had had a long relationship with USAA. Over a decade, ending in 2017, at least eight attorneys at Keller Rohrback had represented USAA in at least 165 cases, including approximately 12 that involved bad faith. Keller Rohrback was USAA’s primary law firm in Washington for bad faith. The firm billed over 8,000 hours of work for USAA during the last two years of the representation.

USAA objected to Keller Rohrback’s participation in the litigation based on this prior representation. However, the Keller firm’s past work for USAA had not involved the Pleins and attorneys Smart and Birk had never been involved in Keller’s relationship with USAA. The lawyers did not have any knowledge of attorney-client communications with USAA.

USAA sought disqualification of the attorneys. The trial court said no: “The Plein matter is factually distinct from and not substantially related to [Keller]’s prior representation of USAA, and as a result, the firm’s representation of the Pleins is not a conflict under RPC [Rule of Professional Conduct] 1.9.”

[Rule 1.9 provides: “A lawyer who has formerly represented a client in a matter shall not thereafter represent another person in the same or a substantially related matter in which that person’s interests are materially adverse to the interests of the former client unless the former client gives informed consent, confirmed in writing.”]

The Washington appeals court reversed. The court’s decision was guided by a comment to RPC 1.9: “Matters are ‘substantially related’ for purposes of this Rule if they involve the same transaction or legal dispute or if there otherwise is a substantial risk that confidential factual information as would normally have been obtained in the prior representation would materially advance the client’s position in the subsequent matter.”

For a host of reasons, the court concluded that the Plein matter was substantially related to the Keller firm’s prior representation of USAA. Some of these are as follows:

- “Keller learned significant confidential information about USAA's strategies for bad faith litigation.”

- “According to USAA, it trusted Keller attorneys ‘with direct access to confidential and proprietary business information of USAA CIC and its affiliated companies’ including, confidential claims handling materials, thought processes of adjusters and in-house attorneys, business and litigation philosophies, and strategies such as ‘approaches to settlement discussions, motion practice, case analysis, defenses, witness meetings, witness preparation, trial preparation, and discovery both on a case-by-case and institutional, company-wide level.”

- Keller also participated in seminars as part of enterprise-wide strategic discussions where attorneys became privy to ‘proprietary information including litigation approach and strategies that has only been shared with a limited group of all of the law firms nationally representing USAA CIC and its affiliate companies in alleged bad faith litigation across the United States.’ And Keller attorneys had electronic login credentials to certain internal proprietary and confidential documents concerning insurance bad faith litigation, ‘including document repositories holding attorney-client information and electronic claim databases.’”

- “[T]he temporal proximity of the prior representation affects the analysis of risk to the former client. ‘Information acquired in a prior representation may have been rendered obsolete by the passage of time.’ RPC 1.9 cmt. 3. Here, Keller agreed to represent the Pleins within three months of the end of its relationship with USAA. This short time frame provides scant opportunity for obsolescence, particularly given the extent—in substance and duration—of the prior representation.”

Thus, the court concluded that the Keller firm’s representation of the Pleins generated “a substantial risk that USAA’s confidential information would materially advance the Pleins’ position.” The court held that there was a conflict of interest under RPC 1.9(a) and attorneys Smart and Birk and the Keller Rohrback firm were disqualified from representing the Pleins.

|

|

| |

|

|

|

|

Vol. 8 - Issue 7

August 21, 2019

Dog Doody To Defend: Pooch Day Care Bites Landlord

|

|

|

| |

Ok, Cam-Sam Real Estate Holding, LLC v. Merchants Mutual Insurance Co., No. 18-433 (D.N.H. July 8, 2019) is not a duty to defend case. But I just couldn’t help myself. Shocking.

Cam-Sam is a property coverage case. Property cases rarely get discussed in CO. But, when a property coverage case involves all manner of things gone awry at a doggie day care, I’ll write about a property case.

Cam-Sam Real Estate Holding rented a commercial building, in Hooksett, New Hampshire, to D La Pooch Hotel, LLC for its use as a pet day care and grooming business. The deal went to the dogs for Cam-Sam.

Cam-Sam initiated eviction proceedings against D La Pooch and discovered that the space “was severely contaminated by pet urine and feces, and substantial damage had been caused by spillage/seepage from overflowing toilets. Substantial repairs were required including: removal of all building materials from Unit 1 down to the shell; remediation of odor, mold, and bacteria in the air and duct systems; and shot blasting the concrete floor to remove embedded odors.”

Did you hear that - shot blasting the concrete floor to remove embedded odors. I have no idea what that is. But, obviously, the odor was pretty intense, and required much more than a few squirts of Fabreze.

Cam-Sam sought coverage for the damage from Merchants Mutual under a property policy. Merchants Mutual told Cam-Sam to heel. Among other reasons, Merchants asserted that no coverage was owed on account of the old “Animal Waste exclusion,” which provided that no coverage was owed for loss or damage resulting from or caused by “nesting or infestation, or discharge or release of waste products or secretions by insects, birds, rodents or other animals.”

As Merchants saw it, dog urine and feces “unquestionably” fall within the definition of “waste products or secretions by . . . other animals,” as dogs are animals and urine and feces are animal waste products.

Cam-Sam barked back, taking the position that Merchants reads the Policy’s exclusion too broadly and inconsistent with the Policy’s purpose: “The Policy is intended, Cam-Sam argues, to provide coverage for damage done to property that is not within the landlord’s control, including, without limitation, damage done by tenants. Consistent with that purpose, Cam-Sam contends, the Animal Waste exclusion applies only when damages are caused by pest or wildlife infestations, not domestic animals, and not animal related damage brought about by human negligence and failure to manage animals under human control and care. Here, Cam-Sam says, the damage was plainly not caused by pests infesting the property, rodents leaving droppings, or insects destroying building materials, all of which would fall within the exclusion. Instead, the damage was caused by D La Pooch’s employees’ negligent operation of the business: ‘Dog feces merely happened to be involved in those business operations.’ At the least, Cam-Sam contends, the Animal Waste exclusion is ambiguous, and ought to be construed in the insured’s favor to provide coverage.”

All things considered, given that Cam-Sam had a steep climb here, it did the best it could with that argument.

The court did not bite, noting that “the Policy language provides, categorically, that damages resulting from animal waste and secretions are excluded from coverage. Dogs are animals. Given the Policy’s broadly worded exclusion, Cam-Sam could not have reasonably understood the Policy to insure against damages to the premises resulting from dog urine and feces. Cam-Sam’s argument that the animal waste was not the direct and immediate cause of the damages (but rather the damage was caused by negligent D La Pooch employees) does not alter the analysis. The Policy unambiguously provides that Merchants ‘will not pay for loss or damage caused directly or indirectly by any of the following. Such loss or damage is excluded regardless of any other cause or event that contributes concurrently or in any sequence to the loss.’ So, to the extent the damage alleged by Cam-Sam was caused, even indirectly, by dog ‘discharge or release of waste products or secretions,’ that damage is not covered by the Policy.”

|

|

| |

|

|

|

|

Vol. 8 - Issue 7

August 21, 2019

Court Addresses Coverage For A Bank Robbery Gone Wrong

|

|

|

| |

Cases involving tragic and unusual facts are de rigueur in the world of coverage. This is how I explain to my students why they read about so much misery in coverage cases – when things go right, there is no need for insurance. By definition, at the heart of every coverage case, is something that went awry.

Tragic and unusual facts were on display in Great Lakes Insurance v. 1 Bank of Eufaula, No. 18-055 (E.D. Okla. Aug. 5, 2019). The court described them like this: “[O]n January 21, 2016, while Julie Huff was a business invitee at the Bank [of Eufaula], an armed robber entered the Bank. He shot and killed the Bank’s president and then shot a teller who resisted his demand for money. He then took Mrs. Huff hostage at gunpoint. The robber ordered Mrs. Huff to drive him in a stolen vehicle and forced her to take him several miles as he sat in the passenger seat with a gun pointed at her. Law enforcement chasing the stolen vehicle were informed that Mrs. Huff was a hostage. After law enforcement stopped the vehicle, Mrs. Huff ran, but the robber caught up to her, put his arm around her neck and used her as a human shield. Law enforcement and the robber exchanged fire, during which law enforcement bullets struck Mrs. Huff approximately nine (9) times.”

The Huffs filed suit against the Bank, alleging that they owed a duty to Mrs. Huff, as a business invitee, and failed to follow industry standards to protect its customers from such a foreseeable situation. Great Lakes insurance undertook the bank’s defense, under a general liability policy, pursuant to a reservation of rights. Great Lakes filed an action seeking a declaration that it owed no duty to defend or indemnify the bank for the Huff action. At issue before the court were cross motions for summary judgment.

First the court found that there was no “occurrence” as there was no accident: “The injuries to the Huffs at issue in the state court action were caused by the bank robber shooting and killing the Bank president, shooting the Bank teller, taking Mrs. Huff hostage at gunpoint, and using her as a human shield. These were all acts that constitute battery. Acts that are intended to and do, in fact, cause offensive contact constitute the intentional tort of battery and are not ‘an accident. Mrs. Huff's injuries were not caused by an ‘occurrence’ under the Policy.”

I can certainly see policyholders taking issue with this conclusion since the bank did not shoot the Bank president or Bank teller or take Mrs. Huff hostage at gunpoint. The Bank is alleged to have failed to follow industry standards to protect its customers from such a foreseeable situation.

The court also concluded that coverage was precluded by an Assault or Battery Exclusion: “The ‘assault’ or ‘battery’ exclusion is not ambiguous on its face. The Bank argues, however, that it is ambiguous because it ‘fails to distinguish and determine what, if any, effect the intentional or negligent nature of an act has on its terms.’ The Bank argues further that ‘[w]here intentionality is not present in the acts resulting in Ms. Huff’s injuries, this ambiguity should be construed in favor of the insured Bank.’ The court does not agree that there is any ambiguity. The Policy clearly excludes coverage for any claims ‘arising out of assault or battery, or out of any act or omission in connection with assault or battery, or with the prevention or suppression of an assault or battery’ and any claims ‘arising out of charges or allegations of negligent hiring, training, placement or supervision with respect [thereto].’ Mrs. Huff's injuries clearly were caused by the intentional battery by the bank robber and by the intentional acts of law enforcement trying to prevent or suppress the bank robber from further intentional battery. To the extent that the Bank could be found negligent for not hiring enough security to prevent such an event, that is also excluded. To the extent that the Bank could also be found negligent for having too many entrances, that does not change the fact that Mrs. Huff's injuries were caused by an assault and battery, coverage for which is excluded under the Policy. Accordingly, as the Policy excludes coverage for the Huffs' claims, Great Lakes has no duty to defend or indemnify the Bank.”

|

|

| |

|

|

|

|

| |

|

|

No Latin Love: Court Declines To Apply Contra Proferentem

I’ve been saying forever that all policyholders speak Latin. And this is no surprise. They sometimes argue that contra proferentem supports their pursuit of coverage. This is the Latin maxim, meaning against the offeror, that generally provides (putting aside some other issues) that, if policy language is ambiguous, it is construed against the insurer and in favor of the insured. So, as policyholders sometimes see it, they do not have to prove what the policy language means, only that it has two different reasonable interpretations. If so, it is construed in favor of coverage. In Universal Cable Products, LLC v. Atlantic Specialty Insurance Co., No. 17-56672 (9th Cir. July 12, 2019), the appeals court addressed whether contra proferentem applies when the policy language at issue was proposed by the insured and the insured is a sophisticated entity. The court held, under this scenario, contra proferentem did not apply as a factor to be considered in the determination of coverage. If you have this issue – an insured that proposed the policy language at issue – it is worth looking at the ins and outs of the decision.

Billy Wilder’s “Double Indemnity” Turns 75!

The Wall Street Journal recently had a story about the 75th anniversary of “Double Indemnity,” Billy Wilder’s classic film about an insurance salesman, who helps a housewife murder her husband for insurance money. In 1998, the film was ranked No. 38 on the American Film Institute’s list of the 100 best American films of all time. There are a bunch of movies with ties to insurance. Here is one person’s list of the 25 best insurance movies of all time (proof that you can find anything on the internet). No surprise, “Double Indemnity” is number one.

|

| |

|

|

|

| |

|

|

|

|

|

|

|

|

|