|

|

|

|

|

| |

|

Vol. 8 - Issue 6

July 10, 2019

|

|

|

|

|

|

| |

“Destroy everything segregated I could find.” This, Fred Gray told me, was the reason he went to law school. Gray wasted no time. In 1955 -- remarkably, just one year out -- he represented Rosa Parks, on trial for her legendary act of defiance on a bus in Montgomery, Alabama. Parks was found guilty. But Gray got the last word. Less than one year later, he convinced the Supreme Court to declare racial segregation of Montgomery’s buses unconstitutional. Gray had another iconic civil rights figure as a long-time client – Dr. Martin Luther King, Jr.

If Fred Gray’s goal was to destroy everything segregated he could find, he was blessed with good timing. Just weeks before Gray graduated from law school, the Supreme Court decided Brown v. Board of Education, striking down the “separate but equal” doctrine in public education. Of this extraordinary alignment of the stars, Gray, also a long-time preacher, said he could not rule out “divine intervention.”

Last month was the 65th anniversary of Brown. For nearly an hourly, the 88-year-old Gray, by phone from his law firm’s office on Fred Gray Street in Tuskegee, Alabama, shared with me a range of experiences over his lifetime as a civil rights lawyer, including building on Brown to achieve what he set out to accomplish.

|

| |

|

| |

Fred Gray with Rosa Parks |

| |

Rosa Parks And The Role Of The Community

Brown gave lawyers the “tools and the legal basis” to fight segregation, Gray told me. However, he was quick to add that you could not have desegregated the buses without having the Montgomery bus boycott. Gray gives all of the credit for it to the involvement of the community.

The 382-day boycott, by African Americans, of the buses in Montgomery – and considered by many scholars to be the beginning of the civil rights movement -- began the day Rosa Parks was found guilty. Gray “vigorously defended” her, he said. But his constitutional challenges were summarily denied and it was all over in 30 minutes.

The boycott finally ended in conjunction with Gray’s 1956 victory in Browder v. Gayle, where the Supreme Court held that segregation of the races, on Montgomery’s buses, violated the Due Process and Equal Protection clauses of the Constitution.

“The real issue that we get from the bus boycott,” Gray said, “is the fact that other people realized, if we could see what they did there, use that, add something else to it, and we’ll be able to solve our problems, whatever they are, where people are being mistreated and being denied their constitutional rights.”

Gray knows of what he speaks when he tells me that a judicial decision alone could not have ended segregation. Gray desegregated his own elementary school in Carr v. Montgomery County Board of Education. In this 1964 Alabama federal court opinion, the court observed that, although it had been ten years since Brown, the Montgomery Board of Education had done virtually nothing to comply with it.

The Impact Of Buses

On account of Rosa Parks, and what followed in Montgomery, buses have long had a powerful association with the civil rights movement. For Gray, this public transportation was also life altering. He originally set out to be both a preacher and a teacher, calling these two professions the only options available to an African American male from the parts of Montgomery “where nothing good is supposed to come.”

Gray attended Alabama State College for Negroes to prepare for a career as an educator. But, following graduation, he abandoned those plans. “It was because of the conditions I saw in having to ride the buses,” he told me, “and seeing how people were treated, that I made the commitment that I would not only be a preacher, but I would become a lawyer. And not just a lawyer but a civil rights lawyer.”

It was then that Gray made the personal commitment to use his degree to destroy segregation. Ironically, to do so, he had to be victimized in the process. On account of the University of Alabama Law School not accepting African Americans, Gray attended Western Reserve University School of Law in Cleveland.

It is a lawyer’s job to serve his or her clients without distraction that could come from having a personal stake. For Gray, where his clients’ causes were often his own, this seems like it may have been a challenge. Gray, not unmindful of my observation, told me that he “didn’t take this as a personal matter.” He kept his personal feelings, of why he became a lawyer, separate and distinct from the issues. There was a strategic reason for such objectivity, wanting to “present to the court that . . . it’s not a personal matter but it’s what the Constitution requires and it’s not being followed and that’s what I want to see corrected.” |

| |

|

|

| |

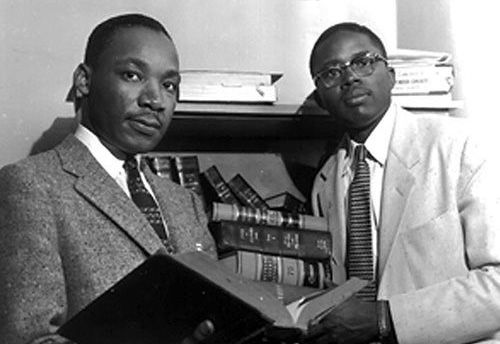

Dr. Martin Luther King, Jr. and Fred Gray |

| |

Martin Luther King, Jr. And The Fight Of His Life

In 1960, Martin Luther King, Jr., now living in Atlanta, was indicted and put on trial in Alabama for perjury -- a novel charge -- in connection with the filing of his Alabama state tax returns. Gray called it politically motivated. “At this point [King] has become an icon and the voice of the movement,” he explained. “I think they believed that if we can get him convicted, then this will stop what he’s doing.”

For King, facing a felony charge, the stakes could not have been higher. In addition to possible prison, “a conviction would have seriously weakened his credibility,” Gray said. “At the same time that he’s talking about civil rights, he’s cheating the state and doesn’t want to pay his state income tax.” Gray, along with others, represented King, who was found not guilty by an all white jury after a four day trial. It was just one of several instances in which Gray served as counsel to King in connection with his civil rights activities.

In an interesting judicial confluence, the King perjury trial is directly related to New York Times v. Sullivan, the Supreme Court’s landmark 1964 decision setting out the standard for a public official to bring a defamation claim. The New York Times advertisement at issue in Sullivan, that allegedly libeled a Montgomery public safety officer, had, as one of its purposes, raising funds for King’s defense in his tax case. Here too Gray was involved -- representing four ministers accused of libel in connection with the ad. They lost – until the Supreme Court had its say, following its adoption of an “actual malice” standard for a public official to bring an action for defamation.

Gray pointed to Sullivan as evidence that the civil rights movement was about more than just securing rights for African Americans. As he explained it, what it accomplished, with respect to obtaining rights under the Equal Protection and Due Process clauses of the Fourteenth Amendment, “now serves more white people than it does blacks, because there is more of them.”

King’s defense team in his tax case had challenged, without success, an all white jury. Later, the exclusion of African Americans from juries was another of Fred Gray’s accomplishments in destroying everything segregated he could find. In 1966, in Mitchell v. Johnson, Gray argued to an Alabama federal court that the process for selecting juries, in Macon County, Alabama, was rigged to exclude African Americans. A dramatically lower percentage of African Americans were called for jury services than their overall county population. The court ordered the County to take immediate corrective action.

The Most Important Case

With a career like Fred Gray’s, the obvious question is whether one case stands out as most significant. Gray said yes. It is Gomillion v. Lightfoot, a case that laid the foundation for the concept of “one man, one vote.” In 1960, Gray convinced the Supreme Court that the city limits of Tuskegee had been gerrymandered for the purpose of excluding African Americans from voting in municipal elections.

Gray had been concerned about getting Justice Frankfurter’s vote. He shared with me that, during oral argument, Frankfurter was shocked to learn something about the new boundaries of Tuskegee that had been drawn. “You mean to tell me,” Frankfurter asked Gray, incredulously, “that Tuskegee Institute is outside the city limits of the City of Tuskegee?” Frankfurter authored the court’s unanimous decision.

The Bus Ride To 1600

Gray told me that be believed that was done in Montgomery, and what other groups did, “all contributed to the election and re-election of President Obama.” And Gray is sure that Obama recognizes this. Leading the former President’s 2009 inauguration parade was a replica of the bus on which Rosa Parks said no. Inscribed on the side: “It All Started on a Bus.”

For Fred Gray it has been a long ride. “A bus, he said,” can take you from where you are, to where you want to go.”

|

| |

|

|

|

Vol. 8 - Issue 6

July 10, 2019

ISO’s Data Breach Exclusion Does Not Apply To Your Cappuccino Order

|

|

|

|

|

| |

There has been lots of litigation over the potential availability of coverage, for invasion of privacy, under a commercial general liability policy. This is no surprise, as “personal and advertising injury” is almost always defined to include “injury, including consequential ‘bodily injury’, arising out of one or more of the following offenses: . . . [o]ral or written publication, in any manner, of material that violates a person’s right of privacy.”

Of recent vintage has been litigation specifically over the availability of CGL coverage, for invasion of privacy, on account of an insured’s data breach. In other words, an insured’s computer system is hacked, or, for some other reason, customers’ personal information is no longer within the insured’s control and is revealed to the public at large or a hacker.

ISO does not intend for injury and damage from data braches to be covered under its standard CGL policy. A few years back the policy language gang added an endorsement that precludes, in part, “‘personal and advertising injury’ arising out of any access to or disclosure of any person’s or organization’s confidential or personal information, including patents, trade secrets, processing methods, customer lists, financial information, credit card information, health information or any other type of nonpublic information.”

The scope of this exclusion was recently put to the test in Iheartcoffee, LLC v. Pacific Salmon Property & Casualty Co., No. 18-347 (Ore. Cir. Ct. (Marion Cty.) May 3, 2019).

The coverage case arose out of the following facts. Iheartcoffee, in Salem, Oregon, installed ordering kiosks. Hadley Anderson used a kiosk to place an order, selecting a variety of options for her beverage. She was prompted to enter her first name so that the barista could call out her order when ready for pick-up. In addition, she was given the option to enter her email address and birthday (month and day only). If so, just before her birthday, Iheartcoffee promised to send her a coupon for a free coffee. Hadley provided this information.

In December 2017 hackers breached Iheartcoffee’s computer network. As a result, information about its customers was available on the internet. This included their first name and related coffee order. But, for those who opted to get a free birthday coffee, the hacked data included their email address and birthday.

Jeff Boyd, a frequent patron of Iheartcoffee, has his curiosity piqued about the breach and found the customer data on the internet. In scrolling through it he saw the name Hadley. He only knew one person named Hadley – a woman who worked out quite seriously at his gym and who Boyd always noticed, to his dismay, did not clean off the equipment after she used it. Wondering if it could be her, given the unusual name, Boyd looked closer. Indeed it was. This Boyd knew as Hadley’s email address was included in the leaked information and it contained the domain of her employer. Boyd knew Hadley’s employer as she had mentioned it to him once, during a chat, while he waited, endlessly, for her to fill up a 64-ounce bottle of water at the fountain.

Boyd saw that Hadley frequently ordered a Venti Half-Soy Nonfat Decaf Organic Chocolate Brownie Iced Vanilla Double-Shot Gingerbread Cappuccino Extra Hot With Foam Whipped. And one Nutrasweet.

Boyd was amused by Hadley’s highly unusual coffee drink. He knew that others at the gym would be too. He shared the information with other members. And they sure were. Within days Hadley had been dubbed “The Queen Bean.” It didn’t take long for Hadley to learn that she was being called this name. After two weeks, Hadley began to believe that her workouts were less effective, as she was preoccupied by the idea of gym members calling her “The Queen Bean.”

Hadley filed suit against Iheartcoffee in Oregon Circuit Court in Marion County, alleging that, on account of the data breach, Iheartcoffee had violated her right to privacy. Hadley alleged that, as a result of being called “The Queen Bean,” she sustained emotional distress and, as a result of less effective workouts, the loss of muscle tone in her triceps.

Iheartcoffee sought coverage for the suit from its general liability insurer, Pacific Salmon Property & Casualty Co. Pacific Salmon disclaimed coverage for a defense and any liability on the basis of the data breach exclusion contained in its policy. While Pacific Salmon acknowledged that there had been oral or written publication, in any manner, of material that violated Hadley’s right of privacy, any “personal and advertising injury” was, the insurer maintained, “arising out of any access to or disclosure of any person’s or organization’s confidential or personal information, including patents, trade secrets, processing methods, customer lists, financial information, credit card information, health information or any other type of nonpublic information.” [Iheartcoffee did not dispute that loss of muscle tone was not “bodily injury.”]

Iheartcoffee undertook its own defense and filed an action, seeking a declaratory judgment, that Pacific Salmon had an obligation to provide coverage to it for a defense and any liability in the Anderson action.

The court in Iheartcoffee, LLC v. Pacific Salmon Property & Casualty Co. agreed that coverage was owed: “We reject the insurer’s argument that a person’s coffee preference, even if it is as unique as a fingerprint -- Venti Half-Soy Nonfat Decaf Organic Chocolate Brownie Iced Vanilla Double-Shot Gingerbread Cappuccino Extra Hot With Foam Whipped. And one Nutrasweet. – qualifies as their “confidential or personal information.” Id. at 5. “It is clearly not of the same type of non-public information described in the exclusion. The exclusion addresses information that has value to its owner, such as trade secrets, customer lists and financial information. That cannot be said of one’s coffee preference. Words are interpreted by the company they keep. In addition, a person’s coffee order is not nonpublic information, even if they’d like it to be.” Id at 6.

The court explained that “[t]he flaw in Pacific Salmon’s argument is that, simply because a person has information that, personally, they’d prefer to keep private -- as clearly evidenced by the fact that its disclosure caused emotional injury -- does not make it per se confidential or personal, as that term is used in the exclusion. Pacific Salmon mistakenly equates the two. It should now be wide awake.” Id. at 7.

|

That’s my time. I’m Randy Spencer. Contact Randy Spencer at

Randy.Spencer@coverageopinions.info |

|

| |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Vol. 8 - Issue 6

July 10, 2019

Encore: Randy Spencer’s Open Mic

Texting While Driving: Court Says  To Homeowners Coverage To Homeowners Coverage

|

|

|

|

|

|

| |

Texting while driving is outrageously dangerously. And even more foolhardy when you consider the unimportant subject matter that people are risking life and limb to communicate. Even people who can agree on nothing, such as political foes or acrimonious opposing lawyers who could disagree on what day of the week it is, would surely at least find common ground on the texting while driving issue. While the statistics vary on the extent that texting while driving plays in motor vehicle accidents, they have one thing in common. It’s staggering.

A Vermont trial court’s recent decision is as unusual of a texting while driving coverage case as you’ll ever see. Richard Downey and Carl Pressman were both texting when Pressman rear-ended Downey. But here’s the even crazier part, they were texting each other. And they weren’t sending smiley face emojis.

Downey and Pressman had arrived at a four-way intersection in Burlington, Vermont at almost the exact time. Downey believed he got there first and made a left hand turn. However, Pressman was of the opinion that he had, and was outraged when Downey made the turn before Pressman could proceed straight. Pressman now turned and began to follow Downey.

Downey and Pressman actually knew each other. Their five year old sons had just been on the same t-ball team – the Polar Bears. And there had been bad blood between the fathers. Pressman believed that Downey’s son, Justin, cost the Polar Bears the league championship. The bases were loaded with one out in the bottom of the last inning with the Polar Bears holding a one run lead. An easy ground ball was hit to Justin at second base. But he had been opening a bag of M&Ms at the time and the ball went through his legs. He missed an easy double play opportunity and two runs scored. Squirrels 9. Polar Bears 8. Both teams got a trophy and ice cream. But only the Squirrels were allowed to get jimmies.

As Pressman proceeded to follow Downey’s vehicle he sent him a text – “Nice move back at that stop sign. You pay as much attention to driving as your kid does at second base.” Downey responded: “You are insane. It was t-ball. They are five years old.” Pressman back to Downey: “Make sure your kid knows in which direction to run on the football field this season.” Downey’s response: “You need help man.” And back and forth it went -- Pressman insulting Downey’s five year old son and Downey telling Pressman that he was pathetic.

After ten minutes of texting, with Pressman still following Downey, Downey stopped at a red light. Pressman, with his attention focused on his phone, plowed into the rear of Downey’s car. Downey was seriously injured. Needless to say, he couldn’t file suit fast enough.

Downey settled with Pressman’s insurer, Maple Syrup Mutual, for policy limits of $100,000. However, this was not adequate for the injuries sustained and Downey did not have a UIM policy. So Downey took an assignment of Pressman’s rights under Pressman’s homeowner’s policy with Maple Syrup Mutual. Needless to say, Maple Syrup denied liability coverage on the basis of the homeowner’s policy’s “Motor Vehicle” exclusion.

But here’s where it got interesting. Downey argued that coverage was not excluded because his injuries were not “arising out of” Pressman’s use of a motor vehicle, as stated in the exclusion, but, rather, Pressman being distracted by texting at the time of the accident.

And the court in Downey v. Maple Syrup Mutual, No. 16-823 (Vt. Super. Ct., Chittenden, April 28, 2017) agreed with Downey’s argument. And the court didn’t seem to think it was even a close call. The court relied on the Vermont’s doctrine of concurrent causation: “Under that doctrine, if the liability of an insured arises from concurrent but separate nonvehicle-related and vehicle-related negligent acts, and the nonvehicle-related act is an included risk under the insured’s homeowner’s policy, coverage exists even though the policy contains an automobile exclusion. In other words, if an occurrence is caused by a risk included within the policy, coverage may not be denied merely because a separate excluded risk was an additional cause of the accident.”

As the Downey court saw it, the texting, even foolishly and inappropriately – and this “takes the cake,” the court added -- was as occurrence (accident) under the Maple Syrup policy. Thus, because a “nonvehicle-related act was an included risk under [Downey’s] homeowner’s policy, coverage exist[ed] even though the policy contain[ed] an automobile exclusion.”

Maple Syrup Mutual is a sticky decision for homeowner’s insurers as texting plays a greater role in automobile accidents.

|

That’s my time. I’m Randy Spencer. Contact Randy Spencer at

Randy.Spencer@coverageopinions.info |

|

| |

|

| |

|

|

|

|

Vol. 8 - Issue 6

July 10, 2019

Do The Insurance Coverage Crossword Puzzle

|

|

|

| |

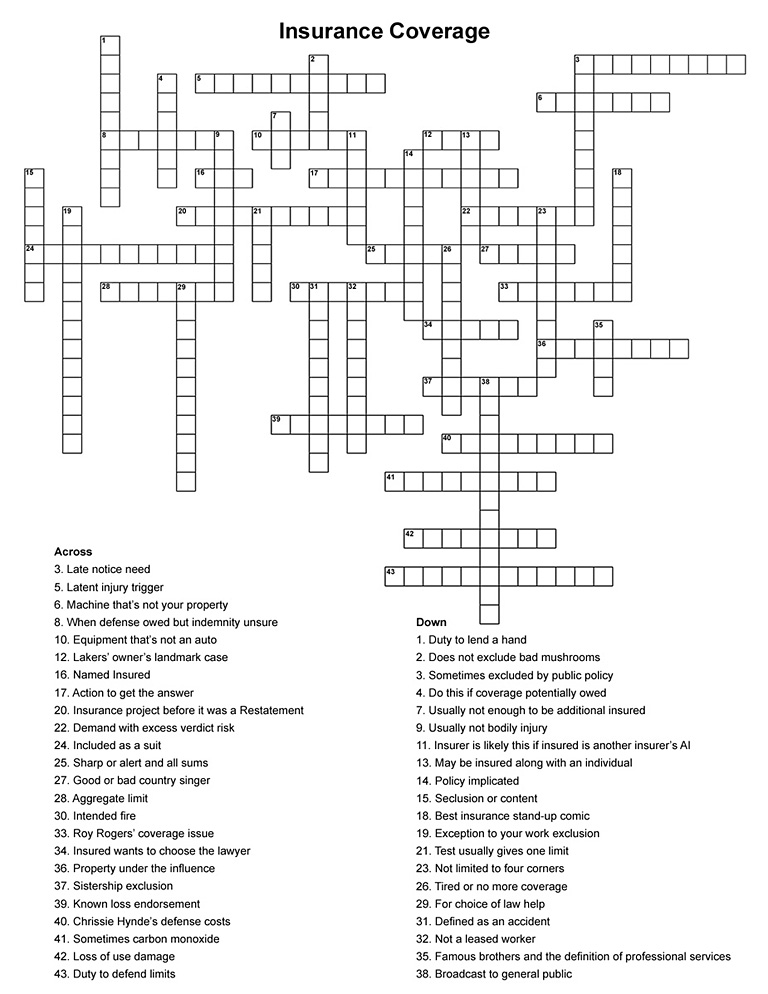

Back in the July 18, 2018 issue of Coverage Opinions I had an Insurance Coverage Seek and Find. I am now stepping it up. I hope you enjoy this Insurance Coverage Crossword Puzzle. Maybe an Insurance Coverage Jumble will be next!

|

|

|

| |

|

|

|

|

Vol. 8 - Issue 6

July 10, 2019

Roadside America: Lawyer Style

Don’t Miss The World’s Largest Warning Sign

|

|

|

| |

Summer is here. And that means family road trips. And no road trip would be complete without stops along the way to see the best of America’s quirks and curiosities. Often these are things boasted to be the world’s largest of something. There is the always-popular world’s largest ball of twine in Cawker, Kansas. If you’ll be in Montana, don’t miss the world’s largest frying pan in Libby. Bealeton, Virginia offers the world’s largest roller skate. And, for you sports fans, a trip to Casey, Illinois will bring you face to face with the world’s largest golf tee.

If you stop by Ishpeming, Michigan you can see for yourself the world’s largest working chainsaw: “Big Gus,” which is 23 feet long and powered by a V-8 engine. According to Roadside America, the experts on all things quirky sightseeing, the “large chain cycles with a terrifying rumble,” even when held back from being revved it up to “forest hewing velocity.” Roadside America reports that the owner of the attraction worries about the chain flying off onto the highway.

That sure seems like a valid concern. That’s why I suggest that another Roadside America-worthy attraction be added next to “Big Gus” – the world’s largest warning sign. So, if that chain ever does fly across Highway 41, and causes all manner of injury and destruction, those responsible for “Big Gus” can maintain that its 9 foot tall warning sign protects them from liability. And, of course, for an added protection, they can always get a 14 foot tall CGL policy.

Here is “Big Gus” with an artist’s rendering of the world’s largest affirmative defense:

|

|

|

| |

|

|

|

|

Vol. 8 - Issue 6

July 10, 2019

Wagging Tail Coverage: Meet The Newest Four-Legged Reader Of Coverage Opinions

|

|

|

| |

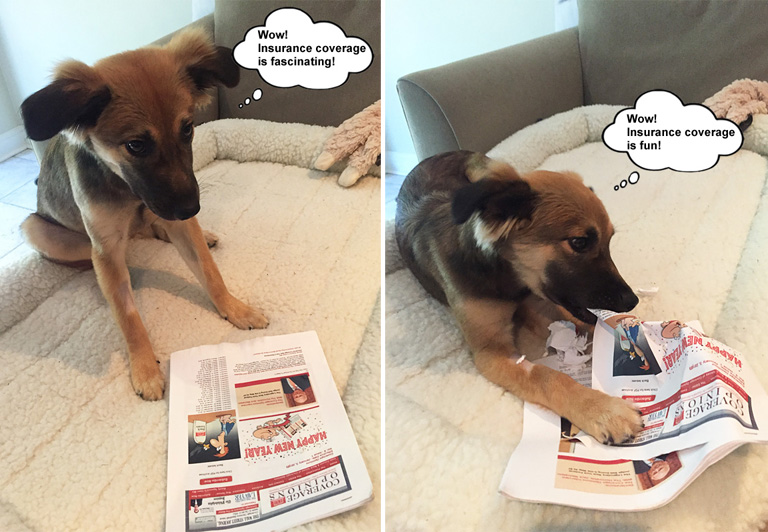

I know. There should be a law against using a dog as click bait. Well, at least I didn’t say “puppy” in the title. I could have. That would be double the punishment.

Meet five-month old Gracie Jane, my family’s newest addition. Not long ago Gracie was roaming the streets of the Caribbean island of Anguilla. Now she is chewing slippers in the suburbs of Philadelphia. She loves it here. But let’s see how her Caribbean lineage does when it’s 9-degrees outside. Should have read the fine print, she’ll no doubt be thinking.

Of course I introduced her to insurance coverage. She had two reactions.

|

|

|

| |

|

| |

|

|

|

|

Vol. 8 - Issue 6

July 10, 2019

Coming Soon (Finally): Insurance Key Issues Half-Price Sale

|

|

|

| |

|

| |

Sales of Insurance Key Issues have been humming along so the price has been full retail for a long time.

I am pleased to report that Key Issues will soon be having a half-price sale. Not sure when. But soon. So, if you’ve been on the fence about making a purchase, or would like an extra copy, to avoid having to share with someone you don’t like, this will be your chance.

Stay tuned.

|

|

|

| |

|

|

|

|

Vol. 8 - Issue 6

July 10, 2019

Introducing The New Coverage Opinions Logo

|

|

|

| |

Last month, The Wall Street Journal reported that Europe’s second highest court ruled that Adidas’s three stripes are not a trademark. The court ruled that Adidas had not offered sufficient evidence that its parallel stipes were a mark of “distinctive character” worthy of protection. The court concluded that the three stripes were too basic a pattern to be considered a trademark.

I was surprised by the decision. Granted, I know nothing about European trademark law. But Adidas’s three stripes sure seem like a trademark to me. That’s my test for a trademark – does it seem like one?

I’ve always been a big fan of Adidas sneakers. Stop by my house and you’ll see Sambas and Stan Smiths in my closet. So, with the thee stripes now being fair game, I’ve decided to update the Coverage Opinions logo.

|

|

|

| |

|

|

|

|

Vol. 8 - Issue 6

July 10, 2019

Smokey And The Bandit And Insurance Coverage

|

|

|

|

|

| |

|

|

|

|

Vol. 8 - Issue 6

July 10, 2019

WSJ: Great Pull-Out Section On Cybersecurity

|

|

|

| |

There was great pull-out section in the June 5th Wall Street Journal addressing many cybersecurity topics, ranging from a quiz on how much do you know about cyber, a list of the most damaging data breaches over the years, competing articles on whether the U.S. needs a cabinet level Department of Cybersecurity, or how about a National Cybersecurity Safety Board, ala the NTSB for transportation accidents, cyber insurance and much more. My favorite article – the psychological reasons why people choose weak passwords.

If you are involved in any way in cyber issues, the WSJ’s pullout section is worth tracking down.

|

|

|

| |

|

|

|

| |

|

Vol. 8 - Issue 6

July 10, 2019

Allocation Between Covered And Uncovered Claims

|

|

|

| |

At its core, Horn v. Liberty Ins. Underwriters, Inc., No. 18-80762 (S.D. Fla. May 30, 2019), is a case about coverage for a consent judgement for a TCPA claim that included an assignment of the insured’s rights under its policy. [The consent judgment was a whopper -- $60 million and change].

As the claim arose under a professional liability policy, the coverage issues were different from those usually on the table under a CGL policy. Here, the question whether there was invasion of privacy went to the applicability of an Invasion of Privacy exclusion. In a TCPA claim, under a CGL policy, whether there was invasion of privacy goes to whether the definition of “personal and advertising injury” has been satisfied.

The insurer here argued that the TCPA action arose out of an invasion of privacy and, therefore, excluded under the policy. Following a lengthy analysis, with resort to lots of case law, the court held that coverage for the TCPA violations was precluded by the TCPA exclusion. Then the court went further, concluding that coverage for the entire action was precluded and not just those aspects that involve invasion of privacy.

If the case had ended there, I would not be writing about it here. Yes, it involved a lot of money. And, yes, it addressed a TCPA claim from a different angle than a CGL policy. But, at its core, it’s a straightforward TCPA claim and not one I’d get excited about.

But then the court went on, stating that “even assuming that coverage is available under the Liberty Policy for the other, non-invasion of privacy harms identified in the iCan Action, Plaintiffs still cannot recover under the Liberty Policy because of their failure to allocate the lump sum settlement between covered and non-covered losses.”

The Plaintiffs (assignees) sought to get around this problem by asserting that the insurer “waived the allocation issue by failing to raise it as a coverage defense in its denial of coverage letters to the iCan plaintiffs, in violation of the Claims Administration Statute, §627.426, Fla. Stat.” But the court concluded that the statute does not apply to the allocation/apportionment issue: “The CAS provides that an insurer can be estopped from denying coverage based on the non-disclosure of a ‘coverage defense’ Both federal and state cases, including the Florida Supreme Court, have narrowly construed the term ‘coverage defense’ to include defenses to coverage where coverage would otherwise exist, such as the insured’s breach of a contractual policy condition. . . . However, the CAS does not apply to on-point policy exclusions or issues that result in a complete lack of coverage. Here, the burden of an insured to allocate/apportion a settlement is established by the common law and is not a ‘coverage defense’ under the CAS.”

Admittedly, given that the allocation issue arose in the context of a Florida statute, it could be said that the decision is not strong support for a wider rule that an insurer, by failing to include it in its reservation of rights letter, does not waive the insured’s obligation to allocate a settlement between covered and uncovered claims.

However, the basis for the court’s conclusion was that “waiver and estoppel may not be used to create coverage beyond the terms of the policy.” This is a general rule nationally. Therefore, while the allocation issue arose in the context of a Florida statute, the decision, based on its reasoning, has the opportunity to provide wider support for a rule that an insurer does not waive the insured’s obligation to allocate a settlement, between covered and uncovered claims, by not including this requirement in its reservation of rights letter.

|

|

|

| |

|

|

|

|

Vol. 8 - Issue 6

July 10, 2019

Court Writes Rx For Defense Coverage For Sexual Misconduct Under Med Mal Polices

|

|

|

| |

I don’t have any statistic on this this. But, anecdotally, reading a lot of cases, I would say that those in the medical field, seeking coverage for sexual misconduct, in the course of treating a patient, have an uphill battle. Sexual misconduct exclusions are usually broad and, in general, courts seem disinclined to reward perpetrators, of such conduct, with the luxury of someone else paying for its consequences.

But, in NCMIC Insurance Co. v. Smith, No. 18-533 (S.D. Ohio May 30, 2019), the Ohio federal court was not prepared to rule out coverage, under a medical malpractice policy, for a chiropractor who allegedly sexually assaulted over 40 female patients during the course of chiropractic treatment. The chiropractor, Smith, facing a class action, sought coverage from NCMIC Insurance Co. under a Professional Liability Policy.

NCMIC Insurance Co. filed an action seeking a declaratory judgment that it had no obligation to provide coverage to Smith, for defense or any liability, in connection with the suit.

The policy at issue contained the type of insuring agreement provisions that you would expect to see in a medical malpractice liability policy. This was followed by various exclusions, including one for “[s]exual impropriety, sexual intimacy, sexual assault, sexual harassment or any other similarly defined act.”

Addressing a motion for summary judgment, the court concluded that the intentional tort claims were not a “negligent omission, act or error” to trigger the insuring agreement. In addition, the intentional tort claims were excluded from coverage by various exclusions, including the sexual impropriety, sexual assault, etc. exclusion. Not surprisingly, the court stated: “[T]he actions underlying the claims of assault and battery are rooted in sexual misconduct—including allegations that Defendant Smith exposed patients’ breasts, touched their breasts, and placed his genitals in contact with patients while performing chiropractic procedures. Consequently, the Court agrees with Plaintiff that the underlying complaints unquestionably allege a pattern of sexual assault and impropriety, therefore triggering exclusion C.”

The court next turned to the negligence claims. Here it was a different story. The court focused on the claim for failure to obtain informed consent and concluded that the negligence requirement, to trigger the insuring agreement, was satisfied. The court stated that “Defendant Smith ‘failed to disclose ... [the] material risks and dangers inherent in the procedures [Defendant] Smith proposed to perform on her. Specifically, [he] failed to disclose to [Defendant Doe] the risk that the treatment ran the risk of [her] breasts being touched or exposed, as well as the risk that her hand would be pressed against his genitals.’ Defendant Homer similarly alleges that Defendant Smith fell below the standard of reasonable chiropractic care by failing ‘to disclose to [Defendant Homer] the risk that her breasts would be touched or exposed, as well as the risk that her hand would be in contact with his penis.’ Construing the evidence in the light most favorable to the nonmovants, these alleged facts support a cause of action that Defendant Smith negligently failed to obtain informed consent concerning ‘inadverten[t] or accidenta[l] touch[ing]’ during treatment.”

Turning to the potential duty to indemnify, here too the court could not rule out the possibility of the chiropractor having acted negligently, despite his conviction for numerous counts of sexual imposition: “[A] genuine dispute of material fact exists as to whether Defendant Smith committed intentional torts against Defendants Doe and Homer. [NCMIC] states, ‘it is clear from [Defendant] Smith’s conviction for 66 counts of sexual imposition as well as the nearly identical allegations made by [Defendants] Doe and Homer against [Defendant] Smith in their respective complaints that [Defendant] Smith committed unauthorized touching.’ Yet Defendant Smith avers that ‘[a]ll physical contact [he] made with [Defendant Doe] was either for the purpose of providing chiropractic treatment or incidental to the provision of chiropractic treatment.’ Defendant Smith denies that he intentionally touched Defendant Doe’s breasts, or intentionally caused his genitals to come in contact with her hand. At this stage in the litigation, no jury has resolved whether Defendant Smith acted intentionally, negligently, both, or neither. Because an insurer’s duty to indemnify is fact dependent, the Court cannot conclude that [NCMIC] has no duty to indemnify Defendant Smith as a matter of law.”

For plaintiffs seeking to plead into coverage for sexual assault, alleged in the course of medical treatment (or, at least a defense for the insured, opening the door to possible coverage), the Rx from Smith is to allege that the medical provider failed to get informed consent that he or she could come into contact with the patient’s private areas.

I suspect that not every court would buy into this. Some courts ignore labels on complaints and apply a common sense approach to what’s really at issue. That argument was rejected here. And, presumably, not every type of medical procedure, where sexual impropriety allegedly took place in the process, could give rise to an allegation that, as part of the procedure, a patient’s private areas could come into contact with the medical provider. Thus, the medical provider should have obtained informed consent. Of course, even if such a lack of informed consent claim is groundless, well, you know what a groundless claim means for purposes of duty to defend…

|

|

|

| |

|

|

|

|

Vol. 8 - Issue 6

July 10, 2019

Significant Decision On “Any Insured” And “Separation Of Insureds”

|

|

|

| |

In general, the law concerning “separation is insureds” is pretty clear. In just about all states, the terms “any insured” and “an insured” are interpreted just as they say. Any means any. An means an. But, after this initial interpretation, states depart.

In some states, an exclusion that applies to certain conduct by “any insured” or “an insured” precludes coverage even for an insured who did not, himself or herself, commit the excluded conduct. Think of an exclusion for the “criminal act of any insured.” So long as “any insured” committed a criminal act, the exclusion is satisfied, and it applies to all insureds. Thus, it excludes coverage for an insured, who did not commit the criminal conduct, but is alleged to have been negligent for not preventing their insured-spouse or insured-child from doing so.

But courts in some states say “whoa, not so fast.” As they see it, despite what “any insured” and “an insured” mean on their face, in the abstract, the exclusion applies only to the insured that actually committed the excluded conduct. Therefore, in the case of an exclusion for the “criminal act of any insured,” a spouse who did not commit the criminal conduct, but is alleged to have been negligent for not preventing it, is not subject to the exclusion. In essence, an exclusion for the “criminal act of any insured” is read as the “criminal act of the insured.”

Courts in this latter camp tie their conclusion to the policy’s “separation of insureds” clause, which is intended to provide each insured with separate coverage – but not separate limits -- as if each were separately insured with a distinct policy. As these courts see it, to preclude coverage to one insured, for the conduct of another insured, is incompatible with the purpose of the “separation of insureds” clause.

California is considered to be in the latter camp. At least that’s what I would have said. In Minkler v. Safeco Ins. Co., 232 P.3d. 612 (Cal. 2010), the Supreme Court of California held that coverage was owed under the liability section of homeowner’s policies to an insured-mother for failing to take reasonable steps to prevent her insured-son from sexually molesting a minor over the course of several years. The policies contained exclusions for “Personal Liability [coverage] … do[es] not apply to bodily injury or property damage: (a) which is expected or intended by an insured or which is the foreseeable result of an act or omission intended by an insured.”

The Minkler court held “that, in light of the severability clause, Betty would reasonably have expected Safeco’s policies, whose general purpose was to provide coverage for each insured’s ‘legal[] liab[ility]’ for ‘injury or … damage’ to others, to cover her separately for her independent acts or omissions causing such injury or damage, so long as her conduct did not fall within the policies’ intentional acts exclusion, even if the acts of another insured contributing to the same injury or damage were intentional. Especially when informed by the policies that ‘[t]his insurance applies separately to each insured,’ it is unlikely Betty understood that by allowing David to reside in her home, and thus to become an additional insured on her homeowners policies, [she was] narrowing [her] own coverage for claims arising from his [intentional] torts. In light of the severability provision, Safeco’s intent to achieve that result was not clearly expressed, and the ambiguity must be resolved in the [insured’s] favor.”

In reaching its decision, the California high court observed that courts nationally are “split on the general issue whether a severability-of-interests provision in a policy covering multiple insureds alters the otherwise collective effect of an exclusion for the acts of ‘an’ or ‘any’ insured.”

Based on Minkler, it seems like a court addressing California law would limit an “any insured” exclusion to only the insured who actually committed the excluded conduct. In other words, if the policy contains a separation of insured’s clause, coverage is not precluded for an innocent co-insured, whose only alleged liability is for failing to prevent the excluded conduct from taking place.

For this reason, I suspect that many will find the Ninth Circuit’s decision in Bayes v. State Farm, No. 17-56035 (9th Cir. June 10, 2019) to be surprising. At issue was coverage for Susan Potter, under a Renter’s policy issued by State Farm, for claims that her adult son molested a child in Ms. Potter’s home day care. To be clear, it was alleged that the molestation was committed by Ms. Potter’s son. The action, brought by the parent of a molested child, was solely against Ms. Potter for negligent supervision of her son.

The State Farm policy contained the following exclusion:

Sexual Molestation Exclusion. We do not cover bodily injury, property damage, or medical expense arising out of or resulting from the actual, alleged or threatened sexual molestation of a minor by:

a. any insured;

* * *

We have no duty to defend or settle any sexual molestation claim or suit against any insured. . . (emphasis added)

The State Farm policy also contained a separation of insureds clause.

Based on the Sexual Molestation Exclusion, State Farm disclaimed coverage to Ms. Potter, who then assigned her claims against State Farm to Holy Bayes, the mother of the molested child. Bayes filed suit against State Farm.

Putting aside what happened at the district court, the Ninth Circuit, following a detailed discussion of Minkler, held that no coverage was owed to Bayes on account of the Sexual Molestation exclusion. But doesn’t this seem inconsistent with Minkler, where the court held that, in light of the separation of insureds clause, the policy’s intentional acts exclusion [bodily injury or property damage “which is expected or intended by an insured”] did not apply to the insured who did commit an intentional act, even if another insured did.

The Bayes court reached the decision is did by pointing to one sentence in the Minkler opinion: “Significantly, the California Supreme Court observed that because ‘Betty’s policies did not contain a specific exclusion for claims arising from sexual molestation . . . nothing we hold in this case concerns how an exclusion framed in those terms should be construed.”

This was the basis for the Bayes court to distinguish Minkler, namely, that the California Supreme Court had stated that its decision may not apply to a specific exclusion for claims arising from sexual molestation. The court stated: “In this case, Susan and Cooper Potter’s Renters Policy expressly excluded injury or damage ‘arising out of or resulting from the actual, alleged or threatened sexual molestation of a minor by [] any insured . . .We have no duty to defend or settle any sexual molestation claim or suit against any insured . . .’ Applying the severability-of-interests or ‘separate insurance’ clause to each, Susan and Cooper Potter, alongside the Sexual Molestation Exclusion does not result in any ambiguity. State Farm expressly excluded coverage for this type of damage or injury, regardless of the theory for liability.”

Basically, the Bayes court had before it the situation that the Minkler court specifically noted it did not.

Not surprisingly, there was a dissenting opinion that would have followed Minkler, based on its reasoning, notwithstanding the Minkler court’s attempt to limit its holding: “Were we deciding this case on a blank slate, I would likely agree with my colleagues that the State Farm Policy’s Sexual Molestation Exclusion unambiguously excludes Susan Potter from coverage for claims arising from acts of sexual molestation committed by her adult son Cooper. But this case does not come to us on a blank slate. In my view, notwithstanding the California Supreme Court’s attempt to limit its holding in Minkler (citation omitted), Minkler's reasoning forecloses the facile conclusion the majority reaches today.”

The dissent acknowledged the Minkler court’s possible limitation on its holding, but was not persuaded by it: “I recognize it would be odd to reach a result seemingly compelled by the reasoning of a case that carefully stated it was saying ‘nothing’ about this very circumstance. But neither the majority nor any other court to consider the same question has explained how a contrary result can be squared with Minkler’s basic premise: A severability clause requires us to apply the Policy’s exclusions to each insured as if she were the only insured.”

|

|

|

| |

|

|

|

|

Vol. 8 - Issue 6

July 10, 2019

Nevada High Court To Address Reimbursement Of Defense Costs

|

|

|

| |

Just as this issue of CO was going to print, the Ninth Circuit handed down Nautilus Ins. Co. v. Access Medical, LLC, No. 17-16265 (9th Cir. July 2, 2019). The court had before it an insurer’s claim for reimbursement of defense costs, following a judicial determination that the insurer, which undertook its insured’s defense, had no such duty. On several occasions, the insurer asserted a reservation of rights to seek recovery of its defense costs.

The district court held that, under Nevada law, the insurer was not entitled to reimbursement. However, the Ninth Circuit was not so convinced. The appeals court noted that courts nationally have gone both ways on the issue and discussed the rationales for these two schools of thought.

Concluding that there was no Nevada law on the issue, the appeals court made the decision to seek guidance from the Nevada Supreme Court. Interestingly, in doing so, the court observed that, when Nevada law is lacking, courts have looked to the law of other jurisdictions for guidance – “particularly California.” But the court declined to do so here. Perhaps the Ninth Circuit didn’t like what it saw when it turned to such guidance – California’s Buss decision, which allows an insurer to reserve the right to reimbursement of defense costs, without the insured’s agreement.

Instead, the Ninth Circuit certified the following question to the Nevada Supreme Court: “Is an insurer entitled to reimbursement of costs already expended in defense of its insureds where a determination has been made that the insurer owed no duty to defend and the insurer expressly reserved its right to seek reimbursement in writing after defense has been tendered but where the insurance policy contains no reservation of rights?”

No doubt the insurer here will argue that the Nevada high should follow California law, just at is did so closely in State Farm v. Hansen (2015), where it adopted California’s Cumis rule for purposes of determining if an insured is entitled to independent counsel (and specifically speaking the name Cumis fifteen times in the decision). |

|

|

| |

|

|

|

|

Vol. 8 - Issue 6

July 10, 2019

Trigger Of Coverage And Funeral Home Malpractice

|

|

|

| |

The question whether “bodily injury” or “property damage” has occurred during the policy period, to implicate a general liability policy, is usually not hard to figure out. There should be plenty of evidence of the date that the limb went missing of the building went kaboom. Of course, that wasn’t the case with bodily injury caused by asbestos and property damage caused by hazardous waste and other injuries that lay dormant, for a period of time, before being discovered. For those situations, years of litigation ensued, culminating in the continuous trigger or other methods for figuring it out. Since the advent of the continuous trigger, efforts have been made to apply it to all manner of injuries or damages.

At issue in Zack v. Clock Funeral Home, No. 343732 (Mich. Ct. App. June 11, 2019) was trigger of coverage for a unique scenario. An infant passed away in February 2015. The parents arranged for funeral and burial services with Clock Funeral Home of White Lake. The visitation and funeral services were conducted on February 16 and 17, 2015. Burial was delayed due to a required autopsy. The parents requested that their son be cremated and that his ashes be buried in an urn they provided to Clock. Clock conducted a burial service interring the urn on April 18, 2015. In January 2016, an employee of the funeral home discovered a box labeled as the ashes of the infant. The employee delivered the box to the parents. During an investigation, in March 2016, their son’s grave was exhumed and the urn was empty.

At the time of the funeral and burial, the funeral home was an insured under a commercial general liability policy issued by Westfield. The policy included an additional coverage part for acts and omissions arising out of services rendered or the failure to render services as a funeral director. The policy was cancelled on December 19, 2015 for nonpayment of premium.

At issue was the potential for coverage under the policy for a claim against the funeral home. The overarching question was whether “bodily injury” took place during the policy period, as required to trigger coverage.

To summarize, the policy was on the risk at the time of the funeral and burial. However, it was no longer on the risk at the time that the grave was exhumed.

The court concluded that “bodily injury” did not take place during the policy period: “Because plaintiffs did not learn that their son’s ashes were not, in fact, buried until after the policy coverage had ended, they did not suffer their emotional, mental and physical injuries resulting from that negligent act until after the policy had terminated.”

The court rejected the argument that the policy was triggered on the basis that, it was during the policy period, that the empty urn was buried. They argued that “interference with their right to control the final disposition of their son’s remains” was the injury, and such injury was incurred when the empty urn was buried. “However,” the court held that “the interference was simply the wrongful action Clock engaged in that resulted in injuries to plaintiffs.”

Not surprisingly, as often happens in cases involving trigger of coverage, the court turned to its environmental case law on the subject, to see what that has to say about it. The court addressed the Michigan Supreme Court’s 1998 decision in Gelman Sciences, in which the court addressed four theories for when gradual property damage, caused by pollution, takes place.

Gelman Sciences did not help the parents here in their pursuit of coverage: “Our Supreme Court held that the policy language concerning when coverage was triggered was unambiguous and, according to the policies’ explicit terms, actual injury must occur during the time the policy is in effect in order to be indemnifiable, i.e., the policies dictate an injury-in-fact approach. The Gelman Court acknowledged that determining the precise timing of actual property damage is sometime difficult and while it appreciate[s] the difficulty of proof in this regard, this difficulty cannot justify redrafting unambiguous policy terms in the guise of judicial interpretation.”

Even outside of traditional latent injuries, courts sometimes use trigger theories to conclude that “bodily injury” or “property damage” took place during a certain policy period. The court in Clock did not. And I don’t think the case was even a close call. I’m surprised it got this far. But it demonstrates efforts made to make the timing of “bodily injury” and “property damage” malleable to fit a necessary calendar.

|

|

| |

|

|

|

|

Vol. 8 - Issue 6

July 10, 2019

No Failure To Cooperate:

Insured’s No Show At Trial Helps -- And Does Not Prejudice -- Insurer

|

|

|

| |

While insureds are obligated to cooperate with their insurers in their defense, a failure to do so does not always mean a loss of coverage. Often times, to be able to disclaim coverage, the insurer must prove that it was prejudiced by the insured’s lack of cooperation. In general [putting aside specific tests], the insurer must demonstrate that, because the insured did not cooperate in its defense, the outcome of the case was different than it would have been, if the insured had helped out.

There are varying degrees of failure to cooperate. What about when the insured does not participate at all in its defense? As in -- he or she just doesn’t show up, including at trial. If the insurer loses the insured’s case, or the verdict is higher than it should have been, presumably this was because the insured was not there to tell his or her side of the story. That seems like a logical argument. But, as demonstrated by Mora v. Lancet Indemnity Risk Retention Group, No. 18-1566 (4th Cir. May 7, 2019), this may not be so. In fact, as the Mora court saw it, the insured’s lack of participation at trial was to the insurer’s advantage.

The failure to cooperate issues in Mora arose this way.

“In January 2015, Dr. Ishtiaq Malik treated Juan Castillo for his complaints of chest pains and shortness of breath. After administering a treadmill stress test and an EKG, Dr. Malik prescribed a beta blocker but did not refer Castillo to a cardiologist or instruct him to seek any other immediate medical attention. Eight days later, Castillo died from a cardiac event.”

In July 2015, Mr. Castillo’s wife and children filed a medical malpractice action against Dr. Malik, and others, in Maryland state court. Lancet, Dr. Malik’s medical malpractice insurer, informed the insureds that it had retained defense counsel and required Dr. Malik’s assistance in discussing the allegations against the Insureds. The attorney retained by Lancet, despite many attempts, using various forms of communications, was never able to reach Dr. Malik. Lancet learned that Dr. Malik had moved to Pakistan and had no plans to return to the United States.

I’ll let the court tell the rest of the story: “Unable to reach Dr. Malik, Kelly [the attorney retained by Lancet] advised Lancet that because he had not obtained Dr. Malik’s consent to representation, the Maryland Rules of Professional Conduct barred him from appearing in the malpractice action. After Kelly advised Lancet that he believed he was ethically barred from appearing on Dr. Malik’s behalf, Lancet elected not to participate in the malpractice action—it did not investigate the malpractice claim, it did not obtain Castillo’s medical records, and it did not answer Plaintiffs’ complaint. Several months later, in October 2015, Lancet sent a letter to Dr. Malik’s last known address informing him that it was disclaiming coverage because of his failure to cooperate in defense of the malpractice suit. Lancet sent two similar letters to Pakistani addresses thought to be where Dr. Malik might be residing. In February 2016, Plaintiffs moved for Entry of an Order of Default against the Insureds, which the state court granted on March 11, 2016. The attorney for the Plaintiffs notified Lancet that it had thirty days to move to vacate the order. Three days before a state-court scheduled hearing on damages, Lancet filed a motion to intervene—its first effort to participate in the case—which the court granted. Thereafter, Lancet unsuccessfully moved to delay the damages hearing. The state court then entered judgment in the Plaintiffs' favor in the amount of $2.56 million.”

Mr. Castillo’s family filed an action against Lancet seeking a declaration that the insurer was obligated to pay the judgment. Lancet filed a counterclaim seeking a declaration that it had no such obligation because of Dr. Malik’s failure to cooperate.

Following a two-day bench trial, the court declared that Lancet was liable. The court held that “neither ethical rules, nor Maryland law, nor the terms of the Policy prevented counsel for Lancet from entering an appearance and defending the malpractice action.” On the failure to cooperate issue, the court “concluded that Lancet had failed to meet its burden to establish that it had been actually prejudiced by Dr. Malik’s refusal to participate because, even in Dr. Malik’s absence, Lancet had several viable paths to defending the malpractice action, which it elected not to pursue.”

The federal court of appeals affirmed, including on the issue that counsel for Lancet was not precluded from entering an appearance on behalf of Dr. Malik. This was an important issue in the case, but not important for purposes of the points to be made here.

In affirming the trial court, that Mr. Malik’s refusal to participate in his defense did not prejudice Lancet, the court described the necessary prejudice this way: “[A]lthough the insurer does not have to overcome the almost insurmountable burden of proving that the verdict was the direct result of a lack of cooperation, it must show that the insured’s failure to cooperate has, in a significant way, precluded or hampered it from presenting a credible defense to the claim. Under this standard, possible, theoretical, conjectural, or hypothetical prejudice does not suffice.”

The court rejected Lancet’s argument that Dr. Malik’s absence hamstrung Lancet in defending against Malik’s violation of the standard of care. Here, the court saw Dr. Malik’s absence as a benefit to Lancet’s defense: “Lancet vigorously pressed, through its medical expert, cardiologist Dr. Richard Schwartz, that the state of the evidence absent Malik would be insufficient to establish one way or the other whether Malik violated the standard of care. The district court explained that ‘this is itself a credible defense to the Malpractice Lawsuit’ because it demonstrated that, in Dr. Malik’s absence, ‘precious little’ evidence was available for Plaintiffs to meet their burden to show ‘that Malik’s conduct violated the standard of care.’”

But, as a general take-away, the opinion demonstrates that, simply because the insured is not present in his or her defense, prejudice may not be established: “The district court also found credible testimony by Plaintiffs’ expert on emergency medicine, Dr. Alec Anders, that ‘the medical records alone provided sufficient evidence for medical experts to opine on [the] standard of care’ because Dr. Malik’s ‘contemporaneous notes reflect[ed] his diagnostic impressions, course of care, and follow-up plan.’ According to Dr. Anders, such notes are not only used by other physicians administering additional treatment, but also are used by experts at trials testifying as to whether a defendant physician met the standard of care. Plaintiffs’ medical malpractice defense expert, Brault, likewise testified that it would have been possible for Lancet to mount a defense that Dr. Malik’s conduct met the standard of care primarily, if not exclusively, from his consultation notes[.]”

|

|

|

| |

|

|

|

|

| |

|

|

What Could Have Been: Can You Send A ROR Via E-Mail?

Sometimes a coverage case is poised to address some really interesting or unique issue. But then comes the buzz kill – the court never reaches the issue because of some pesky procedural issue, such as it lacks jurisdiction or abstention. That was the situation in Twin City Fire Ins. Co. v. Uland, No. 18-124 (W.D. Ky. May 14, 2019). At issue was the appropriateness of an ROR sent to an attorney making a claim under a professional liability policy. The underlying plaintiffs had lots of reasons for challenging the ROR sent to the insured-attorney, including, that it was improper to send the reservation of rights via email. Instead, they argued that the letter should have been sent certified mail, return receipt requested to the insured as well as defense counsel. Wow, I’ve never seen either of those issues addressed before. It would have been great to see the court’s discussion of them. But, alas, it was not meant to be. The court, for various reasons, held that it did not have jurisdiction.

When Does The Statute Of Limitations Begin To Run For a Coverage Dispute?

Over the years courts have grappled with the question when does the statute of limitations begin to run for a coverage dispute? The answer has not always been the same. If you are addressing this issue, it is worth checking out Baltimore Scrap Corp v. Executive Risk Specialty Ins. Co., No. 18-2743 (D. Md. June 17, 2019). It is a fairly detailed decision. Here is the Tapas version: “Plaintiff’s cause of action for breach of contract accrued on May 1, 2015, when Executive Risk notified plaintiff of the denial of coverage. Limitations was not tolled merely because the insurer indicated that the insured should contact the insurer with ‘additional or new information . . . .’ Refusal to pay a benefit ‘when due is sufficient to constitute a breach.’ The insurer’s assertion that it might reconsider if additional information were presented did not deprive plaintiff of its right to sue to enforce the contract based on the denial of the claim.”

|

| |

|

|

|

| |

|

|

|

|

|

|

|

|

|