|

|

|

|

|

|

Vol. 8 - Issue 4

April 30, 2019

|

|

|

|

|

|

| |

The rules are only a part of the story,” Preet Bharara tells me. “There are oceans of discretion in between those rules.” The former United States Attorney, for the Southern District of New York, is describing the enormous role that the human element plays in the administration of justice. It is a running theme throughout his new book, “Doing Justice – A Prosecutor’s Thoughts On Crime, Punishment, And The Rule Of Law.”

Bharara, curiously fired by President Donald Trump in 2017, is in Philadelphia – a stop on a book tour to promote his New York Times best seller. We’re sitting comfortably in the lobby of his hotel, a chip-shot field goal from Independence Hall. Two hours later Bharara would take the stage at the National Constitution Center where nearly 600 people gave him a rock-star reception.

Dressed in a suit and no tie, Preet Bharara is as relaxed as he looks. As he should be. Besides the success of his inaugural literary effort, his podcast, “Stay Tuned with Preet,” is wildly popular. He has a million followers on Twitter and is teaching at NYU School of Law.

While Bharara won’t tell me what comes next – he provides a possibility -- it’s anything he wants. Preet Bharara is a free agent. And, as lawyers go, they don’t get much bigger. Bharara’s landing will be like LeBron James going to The Miami Heat in 2010, but without all the negative stuff.

Over the course of nearly an hour, the affable and quick-witted, one-time most powerful prosecutor in America, covered a lot of ground, including his time on the job, the “Trump effect” and how not to get hired at the SDNY.

|

| |

|

Bad Chemistry

Bharara, 50, was born in Firozpur, a city in Punjab, India. He moved with his parents to Monmouth County, New Jersey at age two.

That Bharara ended up as a lawyer is the product of both fiction and harsh reality. Among other books, Bharara tells me that “To Kill a Mockingbird” introduced him to the legal profession. “Early on I wanted to be a lawyer, because I felt from these books I’d read – it may be over-sensationalizing the profession -- but I thought it was a pretty noble thing to pursue. Especially if you were doing something in public service.”

But if there was still any chance of Bharara following in his father’s footsteps as a physician, high school chemistry shut that door, he tells me. He’s not alone. I share my long-held observation: “Show me a lawyer and I’ll show you someone who wasn’t smart enough to go to medical school.” Bharara laughs and raises his hand. “Yep, here we go.”

That Bharara did not pursue medicine was not inconsequential in his household. Referring to his parents’ generation: “I don’t know if this is still true,” Bharara says, “but at that point in India, if you were the brightest kid in the class, you became an engineer or a doctor.” Bharara says, humorously, that he and his brother [a lawyer turned successful entrepreneur] disappointed his parents. “They’re very proud of us. They wanted us to be happy. . . I think, had they had their druthers, they would have preferred medical school to law school.”

But whatever shortcomings Bharara may have had with the periodic table of elements, it did not keep him out of Harvard University. This was followed by a degree from Columbia Law School in 1993.

Bharara knew early-on the path he wanted to take. “I realized the only thing that I wanted to be was a federal prosecutor. A prosecutor of some sort. Ideally a federal prosecutor. . . . I realized [that] the most thrilling couple of hours I spent every week in law school was in trial practice and the idea of getting on your feet. I didn’t have an interest in being a lawyer to sit behind a desk, no offense to people. I didn’t become a lawyer to do transactional work. I didn’t become a lawyer to litigate. I became a lawyer because I wanted to do criminal work. But I did other stuff for six years until I felt I had an adequate application to the U.S. Attorney’s office.”

Stints at Gibson, Dunn & Crutcher and Shereff, Friedman, Hoffman & Goodman were the steps Bharara took to get his application in shape. In 2000, he joined the SDNY as an Assistant United States Attorney. Five years later he moved to the role of chief counsel to Senator Chuck Schumer (D – N.Y.).

In 2009, President Barack Obama tapped Bharara to serve as United States Attorney for the Southern District of New York. His tenure was marked by an aggressive pursuit of public corruption and insider trading cases. Indeed, that later effort landed Bharara on the cover of Time magazine in 2012. The headline screamed: “This Man Is Busting Wall St.”

Bharara stayed as the man at the top of the SDNY until 2017, when President Trump fired him under peculiar circumstances.

Bharara had initially been asked, by then President-elect Trump, to stay on in his position at the SDNY. Then Trump continued to call Bharara, leading the prosecutor to believe that the President might have been trying to cultivate a relationship and compromise his independence. When a third call came from Trump, Bharara didn’t return it. He was fired less than a day later. |

|

| |

“Doing Justice”

Many came to know Preet Bharara from the media-storm following his termination. But, despite this, the first thing you notice about “Doing Justice” is what it is not about -- Donald Trump. The President’s name appears on just a handful of pages.

Even before page one, Bharara sets the stage for what’s to follow. He recounts the story of Henry Sweet, a black man, on trial in 1926, for the murder of a white man. Sweet’s life was in the hands of Clarence Darrow. In his closing argument, the legendary lawyer declared that “freedom comes from human beings, rather than from laws and institutions.” These are words that Bharara says he has lived by.

Bharara brings these words to life: “Nothing in law school, in any class,” Bharara tells me, “taught me how I might persuade a frightened, undocumented, Chinese immigrant, in the Fifth Precinct in New York, to come and testify as a robbery victim. Nobody taught me that. Nobody could teach you that. You have to rely on your discretion, your judgment and your understanding of people, your own character, your personality.” |

|

|

|

| |

“Doing Justice” takes the reader on a chronological walk through the federal criminal justice process, covering such topics as interrogation, the use of cooperating witnesses, indictment (including a prosecutor’s decision to walk away from a case), trial and punishment. By taking this vignette approach, Bharara tells me that you can “pick up this book to any of the chapters and begin reading. You can start at the middle, you can start at the end or the beginning.”

But “Doing Justice” is no text book. It makes its points through Bharara’s observations, experiences and discussions of moral and ethical dilemmas, all of which are illustrated by fascinating accounts of cases handled by the SDNY. What makes it all so compelling are the closed doors that Bharara unseals. You are taken to places you never thought you could go.

And nobody can accuse the former prosecutor of wearing rose-colored glasses. He does not hesitate to point out mistakes made by his office and shortcomings in the system.

The book’s strength is in its main characters – the accusers and accused. At the stops along the tour, Bharara focuses on the human aspect. Those involved in the investigation process are subject to the risk of “confirmation bias” – once someone credible comes to a conclusion, subsequent examiners may be prone to agree with it. Interrogation is a course in psychology – the approach the interrogator takes and what makes the subject open up and provide information. Prosecutors face moral concerns when using cooperating witnesses. And for the cooperators, they must confront the decision to dime-out a friend or colleague for their own benefit.

All of this goes back to the lesson he learned from Darrow’s summation. “Justice is served, or thwarted, by human beings,” Bharara says. “Mercy is bestowed, or refused, by human beings.”

Bharara “did not set out to write a book for lawyers. This would have been a much easier task if I was writing a book for lawyers,” he tells me. “I could use jargon and I could assume knowledge and I didn’t have to explain cooperation, the grand jury. . . . I could have written that book in half the time. It also would have been an easier book to write if I didn’t care about being thoughtful about issues of decision making and ethical dilemmas and I just wanted to tell stories.”

While the book may not have been written for lawyers, not once in its 300-plus pages did I feel overqualified to read it. Hardly. Until now, everything I knew about the criminal justice system I’d learned from Law & Order reruns. “Doing Justice” is an eye-opening and riveting insider’s account of the criminal justice system.

Don’t Be Fooled

My conversation with Bharara is frequently interrupted by laughter. He is easy-going and quick with a witticism. It is easy to forget that this laid back guy was known for being unrelenting in the pursuit of justice.

Bharara says in “Doing Justice” that there is Justice Department guidance that a prosecutor brings a charge if he or she is more likely than not to obtain a conviction. But Bharara isn’t convinced that it should always be based on statistics. “It depends on the case and the circumstances.” Bharara explains: “If fifty witnesses tell me someone is guilty of a crime, and they all die in an earthquake, it’s still a righteous case and if I have a chance of convicting, I should bring it.” Of course, he is quick to point out that the prosecutor must not proceed, even in a winnable case, if he or she has a legitimate qualm about guilt -- “period.”

“You might have two cooperating witnesses who are kind of gross, and you have some concern, based on how unseemly they are, that they might not be welcomed warmly by the jury. But you believe that they are corroborated and you believe they are telling the truth in good faith. If it lowers your chances of prevailing do you not bring the case? I think you do.”

As head of the SDNY, Bharara was unafraid to be out-spoken. In “Doing Justice,” he defended his actions, as U.S. Attorney, in drawing attention to the problems of opioids, gangs, insider trading and public corruption. But he acknowledges that he can also see the argument for being quieter. Which path to take, Bharara concludes, “depends a bit on how ones sees the job and its potential impact. Is it purely to prosecute or also to prevent? Also to educate? Also to warn? Also to deter? The important thing was not to affect any particular defendant’s right to a fair trial. Which I made sure I never did.”

Bharara doesn’t hide that a federal judge took him to task for what she described as his “media blitz,” on account of a fired-up speech he gave in 2015, about the conduct of New York State Assembly Speaker Sheldon Silver, the day after the powerful New York politico was charged by Bharara’s office with public corruption. While rejecting the defense’s motion, to dismiss the indictment on grounds of pre-trial publicity, Bharara admits that the judge “slapp[ed] [him] hard.”

But Bharara is unapologetic when I ask him about it. It was a warning shot, he explains. “You . . . can’t get at every crime, so, yes, I wanted the other politicians who were corrupt, who were going to commit crimes, I wanted them to know.”

Landing A Job At The SDNY

The job of Assistant United States Attorney – for any district, and especially the SDNY -- can be a large stepping-stone to even greater things. Did Bharara seek to minimize turn-over in the office by attempting to hire career-minded prosecutors?

I hit a nerve with the terminology I used: “The way you ask the question, I didn’t like it if I got a sense that people viewed it as a ‘stepping-stone.’” Bharara explains that he sought out prosecutors who “respected the idea that it was an inherently valuable service that they had done. If it looked like someone [for whom it] was a way-stop for them to run for office, or get a partnership or some other thing, I tried not to hire those people.”

“Look,” Bharara admits, “it happens to be a catapult to greater things -- it was for me -- it is for a lot of people. But I would like to think that we made sure that we brought people in for whom that was an incidental consequence of taking the job.”

Bharara had other criteria for making hiring decisions. “Harvard doesn’t teach you how to speak to a Blood or a Crip. They should have a class,” he says, smiling. “Young prosecutors . . . haven’t lived a lot of life. They are really smart. We tried to make a great effort not to hire just people who are really smart. A lot of people are really smart. But hire people who are not only smart, but thoughtful, have perspective, because they are going to have so much power.” Being smart, Bharara tells me, doesn’t mean that you “know how to talk to regular folks, . . . how to talk to victims. You learn by doing and you try to find people who are not just at the top of their class at Harvard Law School.”

Bharara has the statistics to demonstrate the unparalleled demand for a prosecutor’s job in the SDNY. “I think I made 180 offers,” Bharara tells me. “I think 179 [accepted on the phone]. Nobody needed a day to think about it. Nobody needed to talk it over with a spouse. Nobody needed to say ‘well let me see if this other offer comes in.’”

Bharara shares with me the story of a billionaire who once asked him who his competition was for labor? “This is going to sound to readers who live in other districts as very arrogant,” Bharara warns, “but it’s a fact. We don’t have any. Because if they get an offer from us, they take it on the spot.”

“The Trump Effect”

What about the “CSI effect?” Did Bharara’s office see any impact of that? So the theory goes, jurors, accustomed to seeing forensic evidence used to solve crimes on television, will not be satisfied of a defendant’s guilt if the same quantum of physical evidence is not presented to them.

Bharara’s short answer -- yes. But he pivots and prefers to discuss a different challenge faced by prosecutors these days: “You didn’t ask this, but I am going to answer it anyway. A more insidious issue we are having now is not the ‘CSI effect’ but sort of the ‘Trump effect.’ It matters when the person with the largest microphone on earth decides that he is going to indiscriminately say ‘the FBI is terrible,’ ‘the intelligence agencies are terrible.’ It undermines people’s faith in the rule of law. It undermines people’s faith in how the justice system operates. Other people have said it, I think FBI directors have said it, if you spend a lot of time with the biggest megaphone on the planet, telling everyone that the FBI is terrible, . . . [it] undermine[s] the credibility of the entire institution. And that has an affect too on juries. They are more skeptical when they walk in the courtroom too.”

The Next Chapter

United States Attorneys frequently transition to the defense side. But can Preet Bharara, a man whose name is synonymous with law and order, see himself arguing to a jury that the government hasn’t met its burden of proof?

“I think people deserve representation, even if they have a lot of money,” Bharara tells me. “At this particular moment in my life, I don’t have an interest -- because I have other options -- in representing individuals or institutions who have been charged with crimes. Other people can do that. They deserve the best representation they can find.”

While Bharara has no immediate plans to spend his days in the Daniel Patrick Moynihan United States Courthouse in lower Manhattan, he gives me a clue as to what may be next-up: “If I were to go into that area [private practice], my preference would be a practice in which I could help companies reform after they admitted to doing conduct that is improper or less than ideal or doing internal investigative work with an eye towards ferreting out bad actors and bad conduct.”

But, for now, Preet Bharara is clearly enjoying the opportunity that his firing, and the resulting media storm surrounding it, have given him. “People maybe read the things I write. You can have some civic impact that way, which I think is good,” Bharara explains. “That’s why I’m doing it. That’s why I’m not doing what a lot people who may read this are doing. I’m taking a pause, from the traditional practice of law, to do this, and speak to people, and to pursue things that I care about and believe in and I think people can be educated on.”

“I’m very fortunate that I have a platform from which I can speak and teach and write and more than four people will listen and read. Maybe I won’t have that in five years,” Bharara considers. “Not everyone gets that chance. So I decided to seize it.” |

| |

|

| |

[Elizabeth Vandenberg, a student at the University of Iowa College of Law, assisted with this article.] |

| |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Vol. 8 - Issue 4

April 30, 2019

Elvis, E-Mail Spoofing And Crime Coverage

Thank You To Cincinnati’s Go Bananas Comedy Club For Its Hospitality

|

|

|

|

|

| |

|

|

Thank You To Cincinnati’s Go Bananas Comedy Club For Its Hospitality

I found myself in Cincinnati last week for reasons of business. Thank you so much to Go Bananas Comedy Club for finding a spot for this out-of-towner on its Pro-Am Showcase. What a great club! It combines audience intimacy, low ceilings (so the laughs don’t float away), a great sound system, really neat décor and super nice people to make for a wonderful experience. If you are in Cincy, do yourself a favor and check out Go Bananas.

****

Elvis, E-Mail Spoofing And Crime Coverage

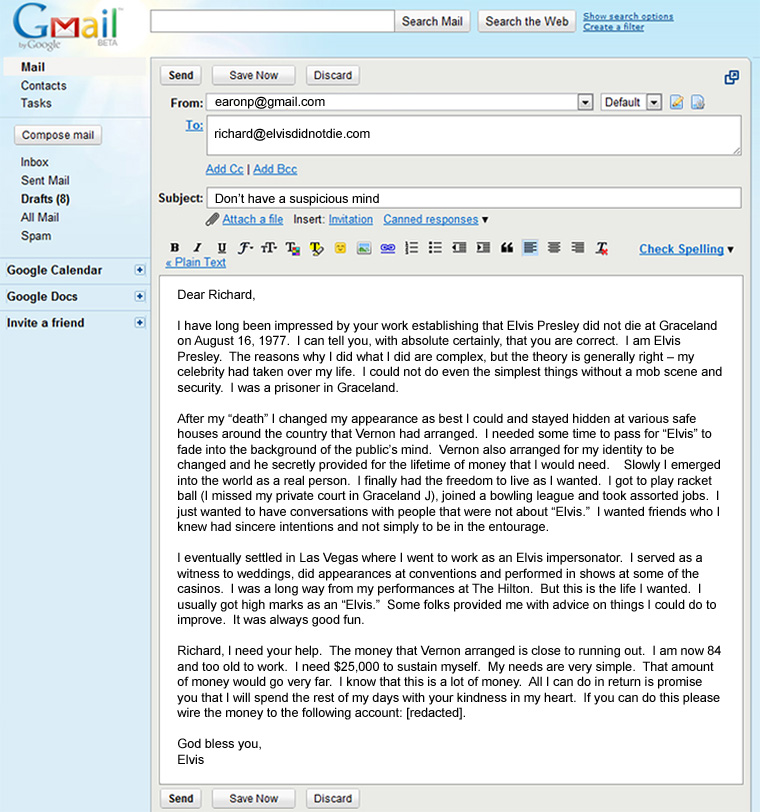

Richard Billings, of Minot, North Dakota, was considered, by those who considered such things, the nation’s leading expert on proof that Elvis Presley was still alive. Billings had spent decades unearthing evidence that he believed established that the King faked his own death on August 16, 1977. Billings had a website that contained photos, voice recordings (with voice analysis experts), DNA evidence, witnesses accounts to Elvis sightings and other information that he believed established that Elvis did not leave this earth in 1977. Billings also had confidential information, from those very close to Elvis, that the star was burned out, felt trapped by his celebrity and simply wanted a simpler life. The only solution was to lead the world to believe that he had forever left the building.

On January 17, 2018, Billings received an email from earonp@gmail.com that read as follows: |

|

|

| |

Richard Billings read the e-mail dozens of times. While he understood that it could be a fraud, he could not get out of his mind that the sender's email address was earonp@gmail.com. Elvis considered his middle name to be Aron, spelled with one "a" only. This, Elvis did, as a tribute to his twin brother, Jesse Garon, who died stillborn. Despite this, the public spelled Aaron the Biblical way. Even Elvis's tombstone is spelled Aaron.

Richard could not believe that a scammer would know to spell Aron with a single "a." Based on this, he wired $25,000 to Elvis. Richard eventually came to believe that he had been scammed.

Richard, seeking to recover the money lost, made a claim for coverage under his Crime policy with Bismark Mutual Insurance Company. The policy provided coverage as follows: "The Company will pay the Insured for the Insured's direct loss of, or direct loss from damage to, Money, Securities and Other Property directly caused by Computer Fraud." The policy defined "Computer Fraud" to mean: "The use of any computer to fraudulently cause a transfer of Money, Securities or Other Property from inside the Premises or Financial Institution Premises: 1. to a person (other than a Messenger) outside the Premises or Financial Institution Premises; or 2. to a place outside the Premises or Financial Institution Premises."

Bismark Mutual disclaimed coverage, arguing that Billings could not prove that his loss had been caused by a fraudulent transfer of money. Bismark maintained that, because Billings had spent decades, and substantial money, in asserting that Elvis Presley was alive, he could not have believed that he had been fraudulently induced into sending money to the sender identified as "earonp."

Richard filed suit against Bismark Mutual Insurance Company. In a recent decision in Billings v. Bismark Mutual Insurance Company, No. 18-2365 (Ward Cty. N.D. Apr. 9, 2017), the court found in favor of the insurer. The court held as follows:

"The content of plaintiff's website demonstrates an individual as confident that Elvis Presley is alive as that the sun rises in the east. It was on this basis that plaintiff wired $25,000 to "earonp." In return, Plaintiff was to receive knowledge that, for the rest of Elvis's days, the legendary singer would have plaintiff's kindness in his heart. Simply put, plaintiff, having spent so long believing that Elvis is alive, cannot prove that he was fraudulently induced to wire the money. Nothing from this transaction changes the mountain of evidence that plaintiff purports proves that Elvis is alive. Therefore, plaintiff cannot now change course, for the benefit of his claim, and maintain that the sender of the e-mail was not Elvis Aron Presley." Billings at 4.

|

That’s my time. I’m Randy Spencer. Contact Randy Spencer at

Randy.Spencer@coverageopinions.info |

|

| |

|

| |

|

|

|

|

Vol. 8 - Issue 4

April 30, 2019

Encore: Randy Spencer’s Open Mic

Cheese Wheel: The Strangest Auto Insurer You’ve Ever Seen

|

|

|

|

|

|

| |

Some insurance companies have interesting names. And taking notice of them is something that I’ve long done. In fact, the very first “Open Mic” column, way back in 2012, was about interesting insurance company names. So when I recently came across the Wisconsin Supreme Court’s old decision in Pouwels v. Cheese Makers Mutual Insurance Company, 37 N.W.2d 869 (Wis. 1949) my first reaction was brie whiz that’s a goudumb name for an insurance company. Stilton stranger, the case was about an automobile policy issued by Cheese Makers Mutual.

Cheese Makers Mutual seems like a munsterrible place to asiago when you need automobile insurance. You would think they don’t know jack about cars – except maybe the wheels.

But I thought about it and then the babybel went off. Insuring cheese must have made them board – especially since they were probably all provalone doing it. Queso instead of being bleu they decided to manchego into cars.

I couldn’t find anything on the internet even remotely current about Cheese Makers Mutual. Apparently they couldn’t cut it.

|

That’s my time. I’m Randy Spencer. Contact Randy Spencer at

Randy.Spencer@coverageopinions.info |

|

| |

|

| |

|

|

|

|

Vol. 8 - Issue 4

April 30, 2019

Thank You To Doug Widin of Reed Smith

Distinguished Policyholder Lawyer Visits My Class At Temple Law School: Gives The Students A Sage Lesson In Coverage |

|

|

| |

|

|

Last week was the final class for my students in Insurance Law 549 at Temple University Law School. They begged me – pleaded, really --to continue it into the summer. Believe me. I thought they were going to riot if I didn’t. And I told them I would, if it were up to me, but my hands were tied by pesky school rules.

For the final class it was my honor to have Doug Widin, of Reed Smith’s Philadelphia office, as a guest speaker. Doug has been practicing coverage law for nearly 35 years – representing, initially, insurers and then, later, policyholders, in all manner of claims involving multiple types of policies, including property, crime, general liability, professional and managed care errors and omissions, directors and officers and numerous specialty liability policies. Doug also counsels organizations with respect to the scope and terms and conditions of coverage for existing and proposed insurance programs.

Doug was a big hit with the students, discussing numerous practical issues, such as the importance of insurance in litigation, how policyholders approach coverage, the role of bad faith in a coverage disputes and independent counsel issues.

Doug told the students that the two most important things that a coverage lawyer can do are, first, read the policy. Second, read the policy again. |

|

| |

It sounds obvious, but Doug’s point was this: No matter how familiar you are with the terms and conditions of a policy, there is a world of difference between reading it in the abstract and reading it with an eye toward coverage for a particular set of facts before you. When an actual claim is at hand, your mind may read and analyze the provisions in ways not otherwise considered in the past, no matter how many times you’ve read them. That sure is the truth.

My thanks to Doug for taking the time to stop by the class and share with the students some of his experiences and observations over the years.

|

|

|

|

|

|

| |

|

Vol. 8 - Issue 4

April 30, 2019

Get A Complimentary Copy Of The 4th Edition Of Insurance Key Issues

|

|

|

|

|

| |

The 26th Annual West Coast Casualty Construction Defect Seminar is being held from May 9-10, 2019 at the Disneyland Hotel in Anaheim. Yes, 26th annual! There are CD claims that were going on at the first seminar that have still not been resolved two and a half decades later.

With 1,500 attendees, this is the must-attend construction defect seminar for all those involved with construction defect litigation and claims -- insurers, coverage lawyers, plaintiff’s counsel, defense counsel and those on the science and technology side of CD. This is the Davos of construction defect seminars.

I am delighted to announce that attendees of this year’s West Coast Casualty Construction Defect Seminar will receive a complimentary copy of the 4th edition of General Liability Insurance Coverage – Key Issues In Every State!! How exciting is that!

I’ll be there at Disney and I know I’ll see some CO subscribers. It’s a small world, after all.

More information about the 26th Annual West Coast Casualty Construction Defect Seminar is here:

http://www.cvent.com

|

|

|

|

|

|

|

Vol. 8 - Issue 4

April 30, 2019

Houston Astros Sued: Its Mascot, Orbit, Broke A Fan’s Finger With A Flying T-Shirt

|

|

|

| |

According to an April 11th Associated Press story, Jennifer Harughty has sued the Houston Astros, alleging that, during a game last season, her index finger was shattered after being stuck by a t-shirt that had been launched into the stands – from a “bazooka style” cannon -- by the team’s mascot, Orbit. It allegedly required two surgeries to repair her fractured finger. Ms. Harughty alleged such things as negligence by the Astros in not using reasonable care in the firing of the T-shirt cannon and failure to warn.

The Astros said in a statement that the team is “aware of the lawsuit with allegations regarding Orbit’s T-shirt launcher. We do not agree with the allegations. The Astros will continue to use fan popular T-shirt launchers during games. As this is an ongoing legal matter, we will have no further comment on this matter.”

Man I love cases like this. Last season the lovable Phillie Phanatic allegedly injured a fan’s face when she was struck by a hot dog, wrapped in duct tape, that the adorable fury green thing had launched into the crowd using a similar bazooka style device.

Shortly after the Phanatic incident I wrote, for The Wall Street Journal, about the legal liability of sports teams for their mascots that cause injuries to fans. You can check it out here:

http://www.coverageopinions.info/FlyingHotDogs.pdf

|

|

|

|

|

|

|

Vol. 8 - Issue 4

April 30, 2019

Wanted: Texas Policyholder Lawyer

|

|

|

| |

When it comes to Texas policyholder counsel, I think very highly of the gang at Shidlofsky Law Firm in Austin. I was recently on the phone with Lee Shidlofsky and he mentioned that his firm needs two coverage lawyers. He joked about putting an announcement in Coverage Opinions. I said, wait, why not? So here is a Coverage Opinions first – a want ad:

Shidlofsky Law Firm PLLC is looking for an experienced insurance coverage lawyer (or two) to join our commercial policyholder practice in Austin, Texas. While we handle most types of commercial insurance cases, our practice is heavily focused on the construction industry—CGL, E&O, CPPI, Builders Risk, etc. Accordingly, experience in that area is a plus. And, who wouldn’t want to live in Austin? Please contact me if you are interested.

Lee H. Shidlofsky

7200 North Mopac Expwy., Suite 430

Austin, Texas 78731

512-685-1400 (Phone)

866-232-8709 (Direct Fax)

lee@shidlofskylaw.com

www.shidlofskylaw.com

|

|

|

|

|

|

|

Vol. 8 - Issue 4

April 30, 2019

Contest Winners:

Obscure Claims Under A CGL Policy

NCAA Tournament “Final Four” Challenge

|

|

|

| |

Obscure Claims Under A CGL Policy

In the last issue of Coverage Opinions I noted that, in the course of my teaching duties at Temple Law School this semester, I have gone through many important provisions of a commercial general liability policy with the students. Doing so caused me to notice some terms that I have never even remotely thought about in all these years. And I’m sure that’s the case for many long-time insurance professionals.

For example, I’ve never even come close to having a claim that involved any of the following provisions in a CGL policy:

- The vending machine exception to the definition of “your product”

- An “insured contract” on the basis of a sidetrack agreement

- The exception to the aircraft exclusion for liability assumed under an “insured contract” for the ownership, maintenance or use of the aircraft.

- Coverage for a bail bond, as a supplementary payment, for a “traffic law violation”

- The “war exclusion” for purposes of a claim for “personal and advertising injury”

I offered to send a copy of the 4th edition of Insurance Key Issues to the first two people who could tell me the details of a claim, in which they were involved, where one of the above policy provisions was in play.

I really expected no winners. But, alas, there was one. Vivian Harrington wrote to tell me that just a few years ago she had a claim involving a sidetrack agreement -- her first since getting involved with claims in 1981. At issue, a demand for indemnity in connection with a claim by an engineer, for a railroad, who allegedly sustained injury when a coal company failed to properly maintain the land upon which the tracks were situated. Well there you go.

Vivian will be sent a copy of the 4th edition of Insurance Key Issues.

NCAA Tournament “Final Four” Challenge

Congratulations to Jeff Purcell of Willis Re in Philadelphia and Gretchen Fitzer on winning the Coverage Opinions NCAA Tournament “Final Four” Challenge. Both beat out an onslaught of entries and correctly picked Virginia and Texas Tech to play in the final game and that Virginia would be the team to cut down the net. The total points scored were 162. Gretchen and Jeff came closest to the number: 174 and 149 respectively.

Each will be sent a copy of the 4th edition of Insurance Key Issues.

Thanks to the everyone who entered.

|

|

|

|

|

|

| |

|

Vol. 8 - Issue 4

April 30, 2019

That Crazy Cosgrove Case Is Still Going (9th Circuit Oral Argument)

|

|

|

| |

In April 2017 an Arizona federal district court issued Cosgrove v. National Fire & Marine Insurance Company. The court held that insurer-appointed defense counsel, in a reservation of rights-defended case, used the attorney-client relationship to learn that his client did not use subcontractors on a project. When defense counsel did so, he knew, or had reason to know, that his client’s policy contained a Subcontractors Exclusion and that the insurer may attempt to deny coverage based on the exclusion. Thus, the court held that the insurer was estopped from asserting the Subcontractor Exclusion as a coverage defense. The court reached this decision despite the existence, or not, of subcontractors being a pretty routine, and obvious, and not secret, fact in a construction dispute.

Needless to say, this was a very troubling decision for insurers (and appointed defense counsel). Very shortly after the court’s decision the parties settled. As part of the settlement, the court agreed that it would vacate and seal the summary judgment decision. Sure enough, you can’t get the decision on Pacer and the insurer arranged for the decision to be 86ed from Lexis and Westlaw. I have a copy of the decision, which is now a collector’s item and I keep it in my special shoe box with my autographed picture of Gopher from The Love Boat and every $2 bill I’ve ever gotten in change. [But, despite being vacated and sealed, the opinion is not exactly a state secret buried at Langley. You can find it on the internet in less time than it takes to put cream cheese on a bagel.]

In November 2017 – many months after the case was over -- United Policyholders, a policyholder advocacy group, filed a Motion to Intervene to unseal and reinstate the decision. UP said in its brief that what the insurer did is an “impermissible tactic” – one “commonly employed by insurers in an attempt to reshape case law in their favor after an adverse ruling.” UP said that the insurer, faced with an adverse decision, is “seek[ing] to hide the court’s opinion.” The insurer filed a response, providing many reasons for denial of intervention, including UP has no standing; the case is over; the judge agreed to vacate and seal the decision as a condition of settlement; and the various requirements of the Intervention rule have not been satisfied.

On January 18, 2018, the court, in a five and a bit page opinion, denied UP’s motion to intervene, citing such reasons as lack of jurisdiction, it is not a party to litigation that shares questions of law or fact to the case, untimeliness and prejudice to the parties.

Notably, in denying UP’s motion to intervene, the District Court stated: “Allowing United Policyholders to intervene in this case would be prejudicial to the parties. While allowing United Policyholders to intervene might not affect the outcome of this case, intervention could potentially affect a material term of the parties’ settlement. United Policyholders wants to essentially un-do a settlement reached by the parties. As part of their settlement, the parties agreed that the partial summary judgment orders would be sealed and vacated. Whatever reason the parties had for reaching this agreement, they were entitled to make that agreement and a ‘potential prejudice to the parties is the possibility that modification [of the court’s partial summary judgment orders] would ‘unravel’ the original settlement.’”

UP filed a notice of appeal to the Ninth Circuit. Oral argument was held on April 16, 2019.

I reviewed the parties’ briefs and listened to the oral argument on the Ninth Circuit website. It makes for interesting listening. It is also available in video format. But I couldn’t get that to work. I’ll try Netflix.

In general terms, the competing positions, during the argument, were between the public’s right to have access to judicial documents versus, as maintained by the insurer, upsetting the benefit of the bargain that was struck between the settling parties. Mixed in were lots of technical issues about intervention and a possible difference between unsealing the decision and reinstating it.

But despite these public policy-esque arguments before the panel, the real issue here is simple -- a fight over reinstating a decision that policyholders view favorably and might want to cite in the future. This is clear from UP’s motion to intervene. UP’s Ninth Circuit brief: “The Insurance Company Buys and Buries the Adverse Ruling.”

Admittedly, UP’s counsel stated during the argument that he knew of no specific plans of UP to do so. But anyone could do so, including UP in a future case. Given how anomalistic the Cosgrove decision is, I’m not sure it has a lot of value going forward. But I could certainly be wrong. Even if I’m not, the Ninth decision may address, generally, the use of sealing and vacating decisions as part of a settlement. Perhaps that is UP’s real objective here and not just bringing Cosgrove back from the witness protection program.

The potential use of the decision, in future cases, was discussed during the argument, but it took a back seat to the more lofty arguments of the public’s right to access versus the parties’ benefit of the bargain. To this listener, the panel showed a willingness to rule either way.

|

|

|

|

|

|

|

Vol. 8 - Issue 4

April 30, 2019

WSJ: Insurers Creating a Consumer Ratings Service for Cybersecurity Industry

|

|

|

| |

There was an interesting article in the March 27th Wall Street Journal: “Insurers Creating a Consumer Ratings Service for Cybersecurity Industry” (Leslie Scism).

According to Momentum Cyber, which tracks such things, there are 3,500 firms world-wide in the cybersecurity business. Under a new program developed by Marsh (the brokerage unit of Marsh & McLennan) – called “Cyber Catalyst” -- cyber vendors can apply to have their offerings evaluated by certain insurers. Marsh will collate the scores and identify the products and services considered effective at reducing cyber risk. Then, a policyholder that uses an approved vendor may qualify for improved terms and conditions on a cyber policy with a participating insurer. These include Allianz SE, AXA SA, Axis Capital Holdings Ltd., Beazley PLC, CFC Underwriting Ltd., Munich Re, Sompo International and Zurich Insurance Group AG.

Needless to say, if this program takes hold, it could make some cyber vendors very successful and it may be control, alt, delete for others. I wonder how those cyber vendors, that don’t make the cut, may react. If you are involved in cyber-related matters it is worth checking out the Journal article.

|

|

|

|

|

|

|

Vol. 8 - Issue 4

April 30, 2019

Wow: Another Court Addresses A “Fall From Heights” Exclusion

|

|

|

| |

In the last issue of Coverage Opinions I addressed United Specialty Ins. Co. v. Everest Construction, No. 18-45 (D. Utah Feb. 28, 2019), where the court held that a “Fall From Heights” exclusion did not apply to preclude coverage for a claim against a construction company, brought by a building inspector, who was seriously injured by an eighty-five pound package of roofing shingles that had been thrown, by an insured’s employee, off the roof of a building at a construction project. The court agreed with the insured that the “Fall From Heights” exclusion did not apply because the bag of shingles did not “fall” off the roof, but, rather, it was thrown.

A case involving a “Fall From Heights” exclusion seems unique. At least you would think. Right? Nope. Less than two weeks later the “Fall From Heights” exclusion was back. This time in Porch v. Preferred Contractors Ins. Co., RRG, No. 18-102 (D. Mont. Mar. 11, 2019). One more “Fall From Heights” exclusion case and they’ll be calling this the “next asbestos.” Law firms will start forming “Fall From Heights” exclusion practice groups.

Kelly Porch, a seller of roofing contracts, went on the roof of a residential building to show a foreman for Ochoa Construction how roofing materials should be applied. While he was on the roof, an employee of Ochoa moved the ladder and placed it against a rain gutter. As Mr. Porch was climbing down the ladder the rain gutter broke. The ladder and Mr. Porch fell 10-15 feet and Mr. Porch was seriously injured.

Suit was brought against Ochoa, which was insured under a CGL policy issued by Preferred Contractors Ins. Co., RRG. PCIC disclaimed coverage. Ochoa entered into with Porch a stipulated consent judgment and covenant not to execute. A judgment was entered in favor of Porch for $4.7 million. Ochoa assigned to Porch its rights under the PCIC policy.

At issue before the court was the applicability of the “Fall From Heights” exclusion in the PCIC policy, which provided as follows: “‘Bodily injury’ sustained by any person at the location of the incident, whether working or not, arising out of, resulting from, caused by, contributed to by, or in any way related to, in whole or in part, from a fall from heights. For purposes of this exclusion, a fall from heights shall include, but not be limited to, a fall from scaffolding, hoists, stays, ladders, slings, hangers, blocks, or any temporary or moveable platform where there is a height differential to the ground.”

The court rejected Mr. Porch’s argument, that the “Fall From Heights” exclusion did not apply, because he did not fall from the ladder, but, rather, with the ladder: “Under the plain language of the first sentence, Mr. Porch’s injuries were clearly excluded. Regardless of whether Mr. Porch rode the ladder to the ground or was separated from the ladder during the fall, the underlying Complaint alleged Mr. Porch’s injuries resulted from a fall from a height of 10-15 feet. As such, the allegations in the underlying Complaint unequivocally demonstrated Mr. Porch’s claim was excluded because his injuries ‘ar[ose] out of, result[ed] from, [were] caused by, contributed to by, or [were] in any way related to, in whole or in part, from a fall from heights.”

Further, the fact that Mr. Porch sustained an injury in a fall with a ladder, rather than in a fall from a ladder, was a “distinction without any discernable difference.” “It would,” the court explained “distort the contractual language to create an ambiguity where none exists” if the policy were interpreted as “excluding coverage for a fall where the injured party loses contact with the ladder, but providing coverage if the injured party is able hang on to the ladder throughout the fall[.]”

|

|

|

|

|

|

|

| |

|

|

Over the course of nearly seven years writing and publishing Coverage Opinions I have tried various new things when it comes to presenting information. Some worked out as I had hoped. Some didn’t – leaving me to wonder: what in the heck was I thinking.

I’ve decided it’s time for a “try something new” moment: The “Tapas in the Spotlight” issue of Coverage Opinions. Regular readers of CO know that every issue features a column: “Tapas: Small Dishes Of Insurance Coverage.” It provides just a brief summary of a few cases. These are cases where there is a point to be made – but not enough about the decision to justify a full-blown article with analysis.

This issue of CO is going to written in all tapas style. Here’s why. I am insanely choosy about which cases are discussed in CO as full articles. To be selected, the case has to make an important point or offer a lesson or involve an emerging or not-often-discussed issue or have a surprising outcome or go in a different direction on an issue or be just plain interesting. So if a court finds that an insurer does not owe coverage to an insured, who shot and killed someone in cold blood, because the bodily injury was not caused by an “occurrence,” the case is unlikely to make it onto these pages.

Normally I can find five or six cases per issue that meet the CO criteria. However, this time around, there are many, many more available. Too many. Rather than choose just five or six, and leave so many worthwhile cases on the proverbial editing room floor -- as I wouldn’t have time to address them -- I decided to include them all, but do so in time-saving Tapas style. And so was born the “Tapas in the Spotlight” issue of Coverage Opinions.

I hit just the high points of the decision, made the important points and kept the analysis and commentary brief (or just skipped it). Admittedly, I did so, in some instances, in a longer fashion that traditional Tapas write-ups – old habits; you know what they say -- but the concept was the same. Anyone interested in leaning more about the case can simply read it.

So that’s the story behind this “Tapas in the Spotlight” issue of Coverage Opinions.

[In case you are wondering, I wrote the above article on Porch v. Preferred Contractors Ins. Co., RRG before coming up with the “Tapas in the Spotlight” idea.].

Insurer Offered Independent Counsel – And Breached The Duty To Defend

Starr Indemnity & Liability Co. v. Young, No. 14-239 (D. Nev. Mar. 31, 2019) involved a situation where an insurer undertook its insured’s defense for a claim alleging that, as an employee of a massage parlor, he performed inappropriate sexual acts while performing a message on a patron. The insurer undertook the defense under a reservation of rights. The coverage issues asserted were as you may expect – “expected or intended” exclusion, “abuse or molestation” exclusion and “assault and battery” exclusion. The insurer retained counsel. However, based on the policy provisions asserted in the reservation of rights, the insurer offered its insured independent counsel, to be paid for by the insured.

Despite this offer, the Nevada federal court held that the insurer breached its duty to defend “by not obtaining an explicit waiver from Young as to his right for independent counsel since Starr understood that an actual conflict of interest existed between itself and Young. The Court finds that Nevada law requires that an insurer obtain an explicit waiver of the right to independent counsel from an insured before it can proceed with dual or concurrent representation in an action in which an actual conflict of interest between the insurer and insured exists or has arisen.”

The attorney retained by the insurer discussed with the insured his right to independent counsel. However, as the court saw it, this was not enough: “[T]he insured at the time a conflict arises will be in the confusing position, for one unversed in the law, with trying to understand a.) what it actually means to have an actual conflict with the insurer, b.) how they may not have actually received advice from the shared attorney if such advice conflicted with the interests of the insurer, c.) what it means to have an attorney who is not representing the insurer in the context of settlement negotiations, discovery and trial, and d.) how an independent attorney’s fees and expenses will be paid by the insurer while the attorney’s loyalty is only to the insured. This complex yet quite substantive-possibly dispositive-set of considerations does not lend itself to written notice or explication from the very attorney who has the actual conflict.”

Further, the reservation of rights letter purporting to inform Young of his right to independent counsel did not fully explain important aspects of his right to independent counsel, including but not limited to a.) the nature of the conflict that arose between Starr and Young and b.) the fact that Young would have the right to ‘independent’ counsel who would have no duty to report to or protect the interests of Starr.”

Court Uses ALI Restatement To Insurer’s Advantage

In Marus v. Allied World Ins. Co., No. 18-253 (D. Me. Apr. 23, 2019), the Maine federal court addressed coverage for claims under a lawyer’s professional liability policy. Putting aside how it got there, an argument was made that the insurer acted in bad faith by seeking recoupment of its defense costs. The court was unconvinced.

In reaching its conclusion, in favor of the insurer, the court found support in the ALI’s Restatement of the Law, Liability Insurance: “At oral argument the plaintiffs’ lawyer argued that the reservation-of-rights provision for recoupment of claims expenses in the Endicott lawsuit and Allied World’s attempt to enforce it are actionable bad faith under the Count II claim. I do not find any Maine case that so holds, and the Restatement of the Law, Liability Insurance § 21, cmt. a (2018) states: ‘When an insurer’s claim to recoupment is based on a contractual right to reimbursement—whether because of a provision of the insurance policy or a subsequent agreement with the insured—it presents no legal difficulty.’ Here, Allied World’s reservation-of-rights letter had a recoupment provision and the plaintiffs did not reject it.”

North Dakota Enacts Legislation: Gives Chilly Reception To The ALI Restatement

On March 20, North Dakota Governor Doug Burgum signed into law H.B. 1142 which provides as follows concerning the state's rejection of the ALI's Restatement of the Law, Liability Insurance:

"Rules of interpretation. In addition to the rules of interpretation under chapters 1-01 and 1-02, in interpreting this title, a person, including the courts of this state, shall apply the Constitution of the United States of America and the Constitution of North Dakota, this code, and the common law of this state. A person may not apply, give weight to, or afford recognition to, the American Law Institute's 'Restatement of the Law, Liability Insurance' as an authoritative reference regarding interpretation of North Dakota laws, rules, and principles of insurance law."

Yikes: Insurer Bitten By Failure To Put A Defined Term In Bold

This is my kind of case. First, it involves coverage for a dog bite. Right there I love it. Then it involves an issue that the court says has “scare authority.” This is a one-two punch for choosing a case for CO.

At issue in Auto Owners Ins. Co. v. Kammerer, No. 18-02143 (D. Minn. Apr. 26, 2019) was coverage for the Kammerers, after their dog bit J.M., who had been watching the Kammerers’ dogs while they were away. The policy defined “insured” to include any person legally responsible for animals owned by the Kammerers. It was agreed that J.M. was responsible for the dog that bit her. Thus, J.M. was an insured as that term was defined.

The policy stated that defined terms appear in bold face type whenever used in the policy. Here’s where the problem started for the insurer. The insurer did not believe that personal liability coverage was owed based on the policy’s “intra-insured” exclusion, which precluded coverage for bodily injury to any insured.

However, as used in the “intra-insured” exclusion, the term “insured” was not in bold face text. The insured seized on this and argued that, as used in the exclusion, “insured” has a different meaning than the bold face type meaning.

For several reasons, the court sided with the Kammerers - rejecting the insurer’s notion that this was simply an inadvertent typographical error: “Perhaps some policyholders would conclude that words assigned special meaning in the DEFINITIONS section but appearing in plain text reflect typographical mistakes by Auto-Owners. Under this interpretation, a hypothetical policyholder might conclude that the word ‘insured’ in the policy’s intra-insured exclusion should be interpreted as if it appeared in bold text, and that would mean J.M.’s claim is not covered. That is not, however, the only reasonable interpretation of the phrase ‘[t]hese words appear in bold face type whenever used in this policy.’ The point of the two sentences preceding the DEFINITIONS is to alert policyholders to the fact that ‘words appear[ing] in bold face type,’ have special meaning. With that qualifier, a policyholder might reasonably think that the two sentences and the DEFINITIONS section as a whole do not say anything about the meaning of words not in bold text. Also, the word ‘used’ in the second sentence need not-and really should not-be understood to mean ‘appear.’ The words have different meanings. Relevant to interpreting the policy, ‘use’ means ‘[t]o put into service or apply for a purpose; employ.’” (bold and all caps in original).

But the court was not done with its work. It had to address what “insured” means when it is not the policy’s defined term? The court concluded that “it is at least reasonable to understand the word insured appearing in plain text to mean just that: the named insured or policyholder.”

The moral of the story here for insurers is obvious.

Insurer Can Withdraw From Insured’s Asbestos Defense After Learning In Discovery That BI Was After Its Policies Expired

I’ll keep this really brief. If you have this issue you’ll want to check out the case.

In Fireman’s Fund Ins. Co. v. Hyster-Yale Grp., Inc, No. 106937 (Ohio Ct. App. Apr. 25, 2019), the insured argued as follows: “[T]he duty is determined solely with reference to the policy language and the allegations of the injury set forth in the plaintiffs’ complaints. Because the policies require Fireman’s Fund to defend even ‘groundless, false, and fraudulent’ claims, and the complaints allege liability against Hyster-Yale, the duty to defend is ‘absolute.’ Therefore, according to Hyster-Yale, the duty continues until the asbestos plaintiffs amend their complaints, or there are judicial determinations of the actual dates of asbestos exposure due to Hyster-Yale.”

The court rejected this, holding as follows: “[T]he trial court properly concluded that Ohio law permits Fireman’s Fund to withdraw its defense of Hyster-Yale in asbestos lawsuits in cases in which there is indisputable, reliable evidence that the date of an underlying asbestos injury clearly occurred outside of the effective ‘policy period.’” [The court reached the same conclusion with respect to Oregon law.]

It is not uncommon for this issue to arise in the context of asbestos complaints, where there is sometimes, at the outset, little said about the plaintiff’s dates of alleged exposure to the insured’s asbestos containing products or operations. Query, can the case be stretched to contexts outside of asbestos-trigger? And what qualifies as “indisputable, reliable evidence” to take the claim outside of the duty to defend?

Insurer’s “Easy Button” To Avoid All Coverage For Construction Defects

The extent of coverage litigation, for construction defects, has reached the point of nuts. You begin to wonder if anything gets built in America without a law suit filed for construction defects, followed by claims for coverage and sometimes followed by litigation on the subject. So much of the litigation revolves around what’s an “occurrence,” exclusions J(5) and J(6), the “you work” exclusion and its “subcontractor exception,” trigger, Montrose issues, what’s “property damage” and other random issues.

Well, Mt. Hawley Ins. Co. found a Staples-like “Easy Button” way out of construction defect problems. It added a Breach of Contract exclusion to its general liability policy issued to a contractor. When its insured, a general contractor for the construction of an apartment complex, was sued by the owner with whom it had contracted, for various construction defects, Mt. Hawley was relieved of all obligations – defense and indemnity.

The court rejected the insured’s argument that the “your work” exclusion’s “subcontractor exception” trumped the Breach of Contract exclusion: “While Schaffer and other subcontractors on the EHP Project may be partially responsible for the property damage claimed in the Underlying Action, the Breach of Contract Exclusion still negates Mt. Hawley’s duty to defend. There is no evidence to suggest, as Huser argues, that the subcontractor exception contained within the ‘Your Work’ Exclusion preserves coverage. . . . The subcontractor exception contained within the ‘Your Work’ Exclusion expressly modifies only the ‘Your Work’ Exclusion, not the other exclusions contained in the Mt. Hawley Policies. Just because the ‘Your Work’ Exclusion preserves coverage for damage caused by subcontractors does not mean that other policy exclusions must do the same.”

Most importantly, for the Breach of Contract exclusion to serve as a walk-away for CD claims, the court held that the exclusion applied to claims that were not labeled “breach of contract.” In other words, the court held that the exclusion applied to negligence claims: “In the Underlying Action EHP sued both Schaffer and Huser alleging they were at fault for construction defects in the EHP Project. EHP’s Petition clearly states separate claims against Huser and Schaffer: EHP’s Petition contains a section labeled ‘Huser's Breach of Contract and Negligence’ and another, separate section labeled ‘Schaffer's Breach of Contract, Negligence, Violations of the DTPA and Fraudulent Misrepresentations.’ The Underlying Action alleges that ‘HUSER has breached its contract or, in the alternative, has negligently supervised and staffed the project in question all proximately causing damages or producing damages which have far exceeded the minimum jurisdictional limits of this Court.’ Huser's contract with EHP imposed upon Huser a duty to supervise and staff the EHP Project with adequate subcontractors. EHP alleges that Huser’s failure to hire and supervise qualified contractors directly resulted in the ‘property damage’ claimed in the Underlying Action. In other words, EHP alleges that Huser was a ‘but for’ cause of the property damage claimed. The facts and allegations in the Underlying Action therefore make clear that the ‘property damage’ at issue ‘ar[ose] directly or indirectly’ from Huser’s alleged breach of its contract with EHP.”

Well that was easy.

No Bacon For Insured For Hog Odor Claim (Shhh. Don’t Tell Your Neighbors -- Or Risk Losing Coverage)

I’ve read a lot of “what’s an accident/occurrence” cases. I’m not sure I’ve ever seen one, with the factors here, on which the decision turned.

At issue in Geidel v. De Smet Farm Mutual Ins. Co., No. 28627 (S.D. Apr. 10, 2019) was liability coverage for an insured, the former owner of farmland, in connection with land he sold for use as a hog confinement facility. Specifically, claims brought by neighbors of the facility, for nuisance and trespass, on account of hog smell that emanated from it.

This is not the first claim of this type. Nor is it the second. Not even the third. These claims often involve the potential applicability of the pollution exclusion. But forgot exclusions. In Geidel, the claim never got past the insuring agreement. The court held that no coverage was owed on account of the failure to satisfy the policy’s “occurrence” requirement, defined as “an accident, including loss from continuous or repeated exposure to similar conditions, which results during the policy period, in bodily injury or property damage, neither expected nor intended from the standpoint of the insured.”

In reaching this conclusion, the court rejected the insured’s argument that the relevant inquiry was whether the injury to the neighbors was expected or intended. Instead the court held: “While the record demonstrates Geidel [insured] may not have expected to get sued by the Finks [neighbor] because of Cedar Creek’s operation of the hog confinement facility, the allegations and record establish Geidel knew his neighbors would see, hear, and smell the facility on the property sold by Geidel. Moreover, even if Geidel did not expect the Finks to object to hog confinement facility because they had previously raised hogs and Karl and Alene lived in Minnesota (away from their South Dakota property), the Finks’ complaint sets forth that prior to construction, they informed Geidel and Cedar Creek of their concerns. Therefore, the Finks’ claims do not allege an ‘occurrence’ as it is defined by the policy.”

The fact that the neighbors objected to the placement of the facility, and the insured knew this, was the driver here. The court further observed: “[A]ccording to the Finks, Cedar Creek and Geidel knew or had reason to know the Finks would object to the facility ‘due to the close proximity of the barn to Plaintiffs’ residential properties.’ The Finks asserted that despite this knowledge, Geidel did not consult with the Finks in determining whether the location of the hog facility ‘would be objectionable.’ Geidel also did not respond when the Finks sent Geidel and Cedar Creek a letter expressing their concerns before the facility was built.”

9th Circuit (Not A Typo): Insurer Being Wrong On Coverage Is Not Bad Faith

Some policyholder lawyers argue that the definition of bad faith is simple: the insurer’s disagreement with anything he or she says. But, in fact, bad faith (first-party) is hard to prove, given how high the standard is. And no amount of policyholder counsel hyperventilation to the contrary will change this. Courts consistently hold that, even when an insurer is determined to have been incorrect on its coverage determination, and, thus, now has a previously disclaimed obligation under its policy, it is not liable for bad faith damages as well.

You know that’s a solid rule when the Ninth Circuit Court of Appeals so holds. In Berns v. Sentry Select Ins. Co., No. 17-56264 (9th Cir. Mar. 29, 2019), the Court of Appeals held that Sentry Select Insurance Company got it wrong in its interpretation of the word “intentional” as used in the definition of “act” in its policy. The policy provided coverage for an “act” of “wrongful termination” or “harassment” committed in the course of employment. However, there was an exception of any “dishonest, malicious, fraudulent, criminal or intentional ‘act.’”

While the insurer was now obligated to pay its insured’s defense costs, the court, in a familiar sounding opinion, concluded that the insurer was not liable for bad faith damages. The standard for proving bad faith was just too high: “In order to constitute ‘bad faith,’ there must be more than just an insurer’s contractual breach or mistaken judgment. (citation omitted) Berns has shown merely that the insurance company incorrectly denied him policy benefits, not that it acted in bad faith. Berns had to show that Sentry was guilty of more than a mere ‘honest mistake, bad judgment or negligence.’ Because Berns has not shown a ‘conscious and deliberate act, which unfairly frustrates the agreed common purposes and disappoints the reasonable expectations of the other party thereby depriving that party of the benefits of the agreement,’ he has not shown bad faith. Although an insurer’s denial must be reasonable under all the circumstances, here, Sentry did not act unreasonably in interpreting the term ‘intentional’ to mean ‘voluntary.’ California law was then mixed as to the definition of ‘intentional.’ Some California cases interpreted the term ‘intentional’ broadly.”

Educational Decision: Pollution Exclusion Not Judged By Its State’s School Of Though

When it comes to the pollution exclusion, there are generally two schools of thought. Some states apply the Pollution Exclusion broadly, to all hazardous substances, and not simply so-called “traditional environmental pollution.” Others apply the Pollution Exclusion narrowly, limiting its application to traditional environmental pollution.

It is fair to say that, based on its case law, Georgia is in the camp that applies the Pollution Exclusion broadly, to all hazardous substances. Despite this, the court in Evanston Insurance Co. v. Xytex Tissue Services, No. 117-140 (S.D. Ga. Mar. 27, 2019) held that the pollution exclusion did not preclude coverage for fatal injuries caused by the discharge of nitrogen in a warehouse.

In general, exposure to nitrogen would clearly be precluded from coverage in a state that applies the Pollution Exclusion broadly. But not so in Xytex Tissue Services – because the facts mattered.

The court’s decision was based on the fact that air is not considered unclear or impure because it contains nitrogen. What killed the individuals was not exposure to nitrogen, but, rather, that nitrogen displaced the oxygen in the air.

The court explained its decision this way: “When read as a whole, the provision is susceptible to multiple meanings. Plaintiff [insurer] reasons that because nitrogen displaces oxygen in the air, it is an ‘irritant’ to persons attempting to breathe the air and is a ‘contaminant’ to the breathable air; the resulting bodily injury arose from that pollution. Defendant Xytex responds that the Underlying Lawsuit alleges that lack of oxygen caused the injury and there is no contamination or irritation of the body in the way carbon monoxide and lead contaminate and irritate the body or water run-off contaminates a lake. Finally, the Court cannot ignore the mandate to construe ambiguities against the insurer and that insurance exclusions are to be strictly construed.”

It is a very interesting decision and demonstrates that there can be more to a pollution exclusion decision than simply knowing in which camp a state is.

Employment Practices Exclusion And Post-Employment Defamation

It is not unusual for the termination of an employee to go badly, resulting in post-employment disputes between the employer and former-employee. Sometimes this arises when the former employee goes to work for a competitor of the former employer. This can give rise to defamation claims, between the parties, on account of bad mouthing.

When a defamation claim is brought by the former employee, against the former employer, the question often arises whether it is excluded by the employment-related practices exclusion in the employer’s general liability policy. After all, the conduct took place after the employment relationship had ended.

This was the issue in Technical Security Integration, Inc. v. Philadelphia Indemnity Ins. Co., No. 14-1895 (D. Ore. March 18, 2019), which the court noted was a case of first impression under Washington law. The employment-related practices exclusion provided, in pertinent part: “This insurance does not apply to: ‘personal and advertising injury’ to: (1) A person arising out of any: (c) Employment-related practices, policies, acts or omissions, such as . . . defamation. . . .”

Here, a defamation claim was brought by a former employee, against his former employer, for allegedly telling others that he had been terminated for a variety of bad conduct, some of which was criminal. Of note, the former employee had gone to work for a competitor of his former employer.

Addressing whether an employment-related practices exclusion precluded coverage for a former employee’s defamation claim, the court held that the magistrate judge got it right when he “concluded that the survey of out-of-state law suggested that courts: (1) apply a context-based evaluation to determine whether an employment-related practices exclusion bars coverage of a former employee’s defamation claim; and (2) draw a distinction between employment-related defamation allegations and competition or business-related defamation allegations.”

Here, the court concluded that, even though the underlying plaintiff’s employment with the insured was the “but-for” cause of the defamation, the defamation was caused by his actions and statements as a competitor in the marketplace. Thus, the court concluded that the employment-related practices exclusion did not apply.

The exclusion stated that it applied “whether the injury-causing event . . . occurs before employment, during employment or after employment of that person.” The court did not address this aspect of the exclusion. Presumably, this simply means that the exclusion is not inapplicable simply because the injury-causing event – defamation -- occurred after employment. But it still needs to satisfy the requirement of being employment-related defamation and not competition or business-related defamation.

Court’s Narrow Interpretation Of The Business Pursuits Exclusion

Insurers generally have success when it comes to excluding liability claims, under a homeowner’s policy, based on the “business pursuits” exclusion. But that was not the case in Ill. Farmers Ins. Co. v. Modory, No. 1-18-0721 (Ill. Ct. App. Mar. 15, 2019), despite the fact that the insured’s alleged conduct, that gave rise to his liability, took place at his place of employment.

Putting aside all of the details, as to how this fellow-employee tiff reached this point, the insured, Gerald Modory, was sued for defamation, for allegedly doing the following, after Joan Nebel was allegedly terminated as a Sergeant, in Public Safety, at a college: “Following her termination, Mr. Modory posted copies of a flyer in the patrol, sergeant’s, and interview rooms advertising a one-day workshop for ‘Problem Employees and the Games They Play.’ Mr. Modory altered the flyer to include a photograph of Ms. Nebel next to the title. According to the flyer, the workshop would help attendees ‘learn what games are actually being played and why problem employees are motivated to play these games,’ with a special emphasis on ‘addressing gossip and rumors.’ Ms. Nebel alleged that her photograph juxtaposed with the workshop’s title ‘intentionally created the impression that Ms. Nebel was herself a ‘problem employee’ who engaged in these actions.’”

At issue before the court was the potential applicability of the “business pursuits” exclusion contained in Mr. Modory’s homeowner’s policy, which provided as follows: personal injury that ‘arises from or during the course of business pursuits of an insured.’ An activity is a ‘business pursuit’ if it ‘is a continuous or regular activity done for the purpose of earning a profit.’”

The court concluded that the “business pursuits” exclusion did not preclude a duty to defend:

“To fall within the business pursuits exclusion, the injury-causing act must be within the scope of employment and be employment-related activity. Thus, for Mr. Modory’s allegedly defamatory conduct to fall within the business pursuits exclusion, so as to preclude Farmers’ duty to defend, the allegations in the underlying complaint must show, free and clear from doubt, that such conduct was a continuous or regular employment-related activity he performed during the scope of his employment as a training officer in the Department of Public Safety at OCC. Farmers bears the burden of proof.

Review of the underlying complaint shows that it is not at all clear and free from doubt that Mr. Modory’s allegedly defamatory conduct fell within the business pursuits exclusion. The complaint alleged that Mr. Modory was a training officer in the Department of Public Safety at OCC, but it did not allege that his altering and posting of the flyer advertising a one-day workshop for problem employees, with Ms. Nebel’s photograph next to the title, was done at his employer’s request or direction, or that he altered or posted it during working hours. There was no allegation that the altering and posting of such a flyer was the type of activity that Mr. Modory was regularly called on to perform pursuant to his employment or that it in any way fell within the scope of his employment. Rather, a reading of the entire complaint reveals that Mr. Modory’s altering and posting of the flyer, indicating that Ms. Nebel was a problem employee, was done due to his personal animosity toward her, as demonstrated by his calling her a derogatory name, hanging up on her, and stating that he did not like or respect her, and was not an employment-related activity that was performed in his capacity as a training officer or on behalf of OCC.”

Insurers Ask Court To Define What The Term “Trigger” Means

The term “trigger of coverage” is a funny thing. Not funny ha-ha, but funny interesting. Despite being such a common term when discussing the availability of coverage -- or not -- under a liability policy, “trigger” appears nowhere in such policies. [At least not in any standard form policies and I’ve never seen it used in any non-standard form.] In King County v. Travelers Indemnity Co., No. 14-1957 (W.D. Wash. Mar. 26, 2019), the insurers (a lot of them; 3 ½ pages needed to list them) asked the court to define “trigger of coverage” in the context of an environmental coverage case.

It’s a very short opinion – except for the list of lawyers -- but the issue was this. All parties seem to agreed that “trigger” means the existence of property damage during the policy period. But the insurers wanted a ruling that, simply because a policy is triggered, that does not mean it’s game-over. In other words, coverage under a “triggered policy” must still be established. The court complied with the insurers’ request: noting that “trigger is a necessary – but not sufficient – element of establishing entitlement to coverage under the polices at issue[.]” Further, the court held that “the term ‘trigger of coverage’ means ‘what event must occur for potential coverage to commence under the terms of the insurance policy’ and ‘what must take place within the policy’s effective dates for the potential of coverage to be ‘triggered.’”

Tingly Fingers Are Not “Bodily Injury”

As general rules (and everything has exceptions), emotional injury does not qualify as “bodily injury” under a general liability policy that defines “bodily injury” as “bodily injury, sickness or disease.” [I know. I know. Lavanant in New York.] But, emotional injury, that results in physical manifestation, does qualify as “bodily injury” under this definition. In those states that apply this rule, a follow-on question often arises: So just what is physical manifestation of emotional injury? Courts have been confronted with a wide-range of offerings, including: feelings of paranoia, anxiety, dazed confusion, lack of safety, embarrassment, crying, shaking, sleep difficulties, weight loss, hair loss, fragile fingernails, headaches, stomach pains, muscle aches, dry throat, rise in body temperature and a knot in one’s stomach.

Thanks to Knutsen v. State Farm, No. 2-88 (D. Vt. Mar. 25, 2019), we can now add tingly fingers and trouble sleeping: “Even looking beyond the facts alleged in the Complaint, as the Knutsens urge this Court to do, there is only a small basis for supporting a claim of bodily injury: Cegalis testified at trial to tingly fingers and trouble sleeping. These slight, physical manifestations may offer insight into the severity or extent of Cegalis’ emotional harm, but they are thin facts upon which to rest a duty to defend. Since these minor symptoms all stem from her emotional distress, which is explicitly excluded from the State Farm policy, State Farm is not obligated to indemnify or defend the Knutsens in the Cegalis lawsuit.” [While the issue in Knutsen arises in a different context than whether emotional injury is “bodily injury, sickness or disease,” the impact is the same.]

Florida Supreme Court To Address Whether Insurer Can Bring Malpractice Claim Against Defense Counsel

In late January, the Court of Appeal of Florida held in Arch Ins. Co. v. Kubicki Draper LLP that an insurer lacked standing, to sue a law firm that it retained to represent an insured, for malpractice. The insurer maintained that the law firm’s delayed filing of a defense resulted in a settlement, using the insurer’s funds, which would have been avoided, in whole or in part, if the law firm had raised the defense earlier. The court concluded that the insurer had no standing to sue as it lacked privity with the law firm.

The insurer filed a motion requesting the appeals court to certify the question to the Florida Supreme Court. The appeals court granted the motion and sent the following “question of great public importance” to Florida’s top court: “Whether an insurer has standing to maintain a malpractice action against counsel hired to represent the insured where the insurer has a duty to defend.” Arch Ins. Co. v. Kubicki Draper LLP, No. 4D17-2889 (Fla. Ct. App. Mar. 20, 2019).

|

| |

|

|

|

| |

| |

|

|

|

|

|

|

|

|

|