|

|

|

|

|

|

Vol. 8 - Issue 3

March 20, 2019

|

|

|

|

|

|

| |

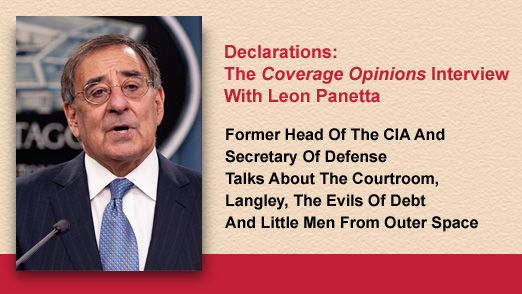

At some point in your career, Leon Panetta tells me, you are going to face a “fundamental decision of conscience.” It will be a choice between “doing what [you] think is right and doing what might enhance [your] career.” For Panetta, reckoning day came long before his eight terms in the House of Representatives and service as President Bill Clinton’s Chief of Staff and President Barack Obama’s Director of the CIA and Secretary of Defense.

It was 1970. Panetta was a young lawyer in a very big position. Faced with a fundamental decision of conscience, he chose to do what he thought was right. For his reward, he was sacked. The man who gave him the ax was Richard Nixon. I tell Panetta that when you are fired by the President of the United States at age 31, it’s a sign that your career has tremendous promise. He lets out a long laugh.

I’m on the phone with Leon Panetta, from his office at the Panetta Institute for Public Policy in Monterey, California, to discuss his remarkable career. While it only included a few years as a lawyer – military and private practice – I tell him that I have some questions about the experience. He’s game. The lessons he learned as a lawyer, Panetta tells me, served him well in Washington.

Panetta was also well-served in D.C. by a lesson he learned from his Italian-immigrant father. I share with him my theory that a man who came to America in 1921 – at 23 years old and with 25 dollars in his pocket -- deserves credit for one of the most remarkable legislative accomplishments of the 20th century.

The 80-year-old Panetta is soft-spoken and thoughtful in his responses. I’d read somewhere – I can’t remember where – that he has a wonderful belly laugh. I got to experience it first-hand a few times. But none louder than when I asked the nation’s former chief spy if there are aliens at Area 51.

|

| |

|

| |

Gotta Call Panetta

Leon Panetta didn’t just stumble upon Monterey as a nice place to live. He was born there. And in all his travels, to the farthest-flung places on the globe, he always kept his watch set to California time -- as a reminder of home.

Panetta graduated from Santa Clara University School of Law in 1963. What made him go, I ask. It was a “combination of elements,” he tells me. In high school he developed an interest in student politics and “help[ing] others and try[ing] to make a difference was important to me.” And his brother, who Panetta called “a model for me” had gone too. “I thought maybe I would like to do the same thing because in the end, law can give me the opportunity not only to practice if I want but also to take those credentials and bring them to government service.”

Panetta’s first stop as a lawyer was the Army, coincidentally serving as an intelligence officer, getting early experience for what was to come. But he was also called upon to represent servicemen in court martials. And he was good at it. Panetta tells me that the calls for his services were so frequent that his wife joked that his name must have been written on the stockade wall.

“I enjoyed the challenge of going into special court martials and general court martials with people who had some very difficult cases,” Panetta says. It was a difficult system for the accused, the former Army lawyer explains, “but if you studied, if you read the law, if you read what you could try and accomplish on behalf of your client, it was amazing that I could really make a difference in terms of their legal cases.”

A Rough Start In Politics

Following the Army, the still-nascent lawyer got his first taste of politics. Panetta served as a legislative aide to California Republican Senator Tom Kuchel. But it was a short stay. Kuchel was the victim of false allegations about his sexual orientation. He lost re-election not long after Panetta arrived.

Panetta landed as a special assistant to Robert Finch, Secretary of the Department of Health, Education and Welfare. Despite being just 30 years old, Panetta quickly rose to Director of HEW’s Office of Civil Rights – overseeing nearly 300 lawyers.

Here again things ended quickly. The Office was responsible for implementing the law on school desegregation. And following the Supreme Court’s decision in Brown v. Board of Education, and subsequently enacted federal statutes, that mandate was clear. It offered no options. But President Nixon, seeking to maintain his support in the South, was in no rush to enforce the law. Of course only one of them could get their way. And, of course, it’s clear who that would be. Panetta woke up one day in 1970 to a headline in The Washington Daily News that read “Nixon Seeks to Fire HEW’s Rights Chief for Liberal Views.” Panetta quickly resigned.

Panetta was now 0-2 in Washington – having been victimized by the ruthlessness that can be politics. He had gone to Washington to do good. Following these initial experiences, I suggest to Panetta that nobody could have faulted him for throwing in the towel. But he didn’t. “I like challenges,” Panetta tells me. “When I am given the opportunity to face something new, and it offers a new challenge, I enjoy the opportunity to be able to get into that job and make it work. And, you know, I guess in that sense the Italian in me tells me you don’t give up. You keep fighting back.”

While Panetta could have easily been soured toward public service, and gone in a different direction, he didn’t. Today, his Institute for Public Policy, founded in 1997, has, as one of its missions, preventing young people from eschewing public service because of a belief that government is broken.

After being handed his walking papers by Nixon, Panetta went on to write a book about the experience. Then, after a year working as an Executive Assistant for New York City Mayor John Lindsay, Panetta took a break from politics and returned to Monterey. He spent five years practicing law with his brother, doing “a bit of everything.” And given his background with school desegregation he took on civil rights work.

But the public service bug bit again. Panetta ran for the House of Representatives. And in 1977 he began the first of eight terms representing the California district in which he was born and raised.

Carmelo Panetta And The Balanced Budget

In 1992 Panetta was re-elected to his ninth term in Congress. But he wouldn’t go on to serve it. Thanks to his extensive work on the House Budget Committee, including acting as its Chair for several years, Panetta was tapped by President Clinton to be his Director of the Office of Management and Budget.

In that role, Panetta orchestrated an unthinkable legislative achievement – a balanced budget. He had spent his career as a deficit hawk – guided by the principle that servicing the national debt takes away from the nation’s ability to attend to other priorities. Panetta explains it to me this way: “It goes to the heart of the ability of our democracy to get things accomplished. You cannot just simply create the kind of huge debt that we have created again now and expect that you are going to have the resources or capability to really accomplish the things that need to be done.”

Panetta had grown up hearing of the evils of debt. His father, Carmelo, was a successful restauranteur in Monterey. “My father taught me that it was very important obviously to work hard, but to also be careful with what you earn and he always operated on a cash basis,” Panetta says. “‘What the hell is that for when you can pay in cash,’” Panetta tells me was his father’s response upon seeing that his son had a gasoline credit card. “That was the ethic they built into me and it came together when I got elected and then got on the Budget Committee.”

Having been a student of his father’s lessons on debt, I suggest that Carmelo Panetta played a part in the nation achieving a balanced budget. “I think that’s right,” Panetta says, laughing.

Panetta adds a postscript to the story: “I always thought that once we balanced the budget and added surplus that we would never go back to deficit spending and to huge debts -- but that changed real fast.”

I pose this scenario to Panetta -- It’s 2020, a Democrat is in the White House, Panetta is home in Monterey – in the house his father built on a farm in the late 1940s -- and the phone rings. The voice on the other end is the President’s, telling him that the national debt is crippling the nation. We need you back to solve it, the President implores him. I ask Panetta is he’s getting on a plane to Washington? He laughs. “You know, at this stage of the game, 3,000 miles away from Washington, I’m enjoying life. I’ve certainly committed my life to public service and I’ve never regretted that. In my own way, in whatever way I can, I’ll continue to try to serve my country.”

An Eerie Road Trip

On September 11, 2001, Panetta was out of politics. But he found himself in Washington that day, testifying in the House Office Building about an oceans project in which he was involved. Following the terrorist attacks, he wanted to get back home to Monterey. But with all flights grounded, flying was not an option. Panetta rented a car and drove cross-country.

Panetta witnessed first-hand how Americans, coast-to-coast, absorbed the impact of September 11th. He would later go on to lead the CIA and be at the helm of locating Osama bin Laden and planning the mission in Pakistan that would kill him. Then he would be Secretary of Defense and oversee the hostilities that grew out of 9-11.

[Panetta was played by James Gandolfini in “Zero Dark Thirty,” a film that dramatizes the hunt for bin Laden. Of the Sopranos star’s portrayal of him, Panetta has said that he did a “great job.”]

That Panetta made such a cross-country drive is eerie, I tell him. It’s as if he was destined for his roles at CIA and the Defense Department and his 9-11 road trip was an orientation, designed to give him a first-hand view of the country, and people, whose safety he would go on to ensure.

Panetta is not unmindful of my observation. “I’ve often -- particularly when I was offered the job as CIA Director -- thought back to that trip that I took from Washington to California right after 9-11 and really got a sense how the country was responding to that attack. I could feel, wherever I stayed, that . . . there was a sense of real patriotism. It was time for the country to pull together and deal with this attack. You could just feel it at the grass roots as I drove across the country and that feeling never left me.”

The CIA And Pushing The Button

Panetta served as Director of the CIA from 2009 to 2011. Is a lawyer the best person for that job? Doesn’t the CIA act kinda lawlessly, I ask Panetta, telling him that I mean no disrespect. He doesn’t take offense -- and assures me that the laws are being followed at Langley. Panetta confronted the CIA’s legal mechanism often, he explains, as he called himself a “combatant commander” (a term coined by his predecessor, Michael Hayden).

Given the nature of the missions – taking out terrorists -- Panetta says that he found himself “making life and death decisions almost on a daily basis. And when you do that, there is not only the issue, obviously, of conscience, how you do it in accord with your beliefs about protecting life, but, at the same time, you’ve got to make sure that when you are pushing the button that the law is on your side.”

When it comes to putting targets on a list, Panetta explains that it is done with counsel “making sure that they should be on that kind of list, and doing that in conjunction with the Justice Department and their counsel, to get them to sign off, and then having the White House counsel also ultimately approve that. There is an entire legal process that is at the foundation of what you do.”

Lesson Of Compromise

Even lawyers who did not spend significant time practicing law most likely cannot divorce the experience from their alternative careers. And Panetta is no exception. Indeed, it taught him a skill that was at the very heart of his lifetime in politics – the art of compromise.

“The ability to govern and find compromise is very difficult these days as we have seen. . . . As an attorney, this is what you are going to be doing,” Panetta explains. “You are going to have to know what the other side is going to argue. How does the law support their position? How do the facts support their position? You are going to have to then determine the law and the facts with your own client but you are also going to have to look at where possibly these things can be resolved. Particularly these days with mediation and arbitration, it is almost constant and you are trying to determine how can you resolve these issues. I think having that legal background is extremely important when it comes to politics and to public service.”

Area 51: “Little Men From Outer Space”

I had one more question for Leon Panetta. And I was not throwing away my shot. I tell him that he would make me famous if he gave me a scoop. I can see the curious look on his face through the phone. I lay it on him. Would the former Director of the CIA admit that there are aliens at the Air Force’s Area 51 in the Nevada desert?

“I would love to give you that one,” Panetta says, laughing loudly. “I watch these movies and there’s always this sudden revelation that they’ve got somebody from outer space locked in a hole someplace in Area 51. You know, I have to tell you, as Director of the CIA, and also Secretary of Defense, I never found the location that I’ve seen in movies. There is a location there, but it clearly doesn’t include little men from outer space.”

Sure it doesn’t, says the man who is part of the conspiracy.

[Elizabeth Vandenberg, a student at the University of Iowa College of Law, assisted with this article.] |

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Vol. 8 - Issue 3

March 20, 2019

|

|

|

|

|

|

| |

|

|

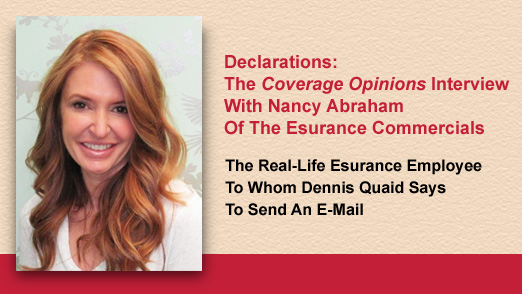

Esurance's Nancy Abraham with the very likeable Dennis Quaid. |

| |

You’ve no doubt seen the new Esurance television campaign – “Surprisingly Painless” -- where Dennis Quaid discusses the benefits of purchasing insurance from the company. In one commercial, Quaid ends by saying that, if you don’t believe him, you can believe this real-life Esurance employee who he introduces -- Nancy Abraham. Quaid invites viewers to send her an email at Nancy@esurance.com.

As an insurance enthusiast, with the inquisitive nature of Curious George, the chances of me not sending an email to Nancy Abraham were about the same as not eating a bowl of Jelly Bellies put in front of me.

Lo and behold, Nancy Abraham is a real Esurance employee -- Vice President, Integrated Marketing Communications. And she was kind enough to answers my questions about the company’s new campaign, its decision to use Dennis Quaid as its spokesperson and having the actor invite millions of people to send her an email.

I am a long-time student of insurance company commercials and the spokespeople/characters that they use to sell their products. [I once made a formal request to GEICO to interview the Gecko for Coverage Opinions. I swear. The company did not respond. The request probably never ever got past his handlers.] Having thought a lot about the subject, I give Esurance’s “Surprisingly Painless” campaign very high marks.

Take Farmers Insurance. The company goes to highly dramatic lengths to explain that insurance pays money when things go wrong. If a hippopotamus escapes from the zoo, and steps on your Toyota, it’s covered. Good to know. Thanks, nerdy Farmers Guy. But I think most people are already familiar with the you-pay-us money, we-pay-you-if-something-bad-happens concept.

Instead, Esurance tackles head–on the biggest problem facing the purchase of insurance – what people don’t know. Insurance can be confusing. The purchasing process can be intimidating. And it can be expensive. This is not a good consumer combination. Who wants to spend that much money for a product that you do not fully know what it is? Esurance endeavors to make the insurance purchasing process, well, surprisingly painless. But the company focuses on more than just the nuts and bolts of the transaction -- it seeks to educate its customers. And as a part-time insurance educator, I’m all for that. [To Dennis Quaid: You are welcome to guest lecture anytime in my Insurance Law class at Temple Law School. Monday’s at 10 A.M. Room 7A.]

The company is clearly doing something right. Of the nearly 7,500 customer reviews on Esurance’s website, 84% are five stars and 12% are four stars.

But don’t listen to me. Here’s what Nancy Abraham, that real-life Esurance employee, has to say about the company’s new “Surprisingly Painless” ad campaign.

Coverage Opinions: Insurers use a variety of approaches when selling auto and homeowners insurance to attempt to distinguish their policies from other companies. What made Esurance take the “surprisingly painless” approach?

Nancy Abraham: We did a lot of research on how people feel about the insurance experience, and found that there are still quite a few pain points when it comes to buying, owning and using insurance. People think insurance is complicated, confusing and expensive. So, Esurance identified an opportunity to improve the customer experience. We’re on a journey to make insurance simple, transparent and affordable. In other words, surprisingly painless. This campaign isn’t just about finding a catchy marketing slogan, it’s our promise to address these pain points and improve the experience, and the entire company is working hard to live into that promise.

CO: What are some things that Esurance does to attempt to achieve this painlessness?

NA: We’re addressing the entire insurance experience, from buying to owning to using. Here are just a few examples in each of those areas:

- Buy – We’re streamlining the quote process so there’s more simplicity around getting the coverage that’s right for you. We’re also rewriting all of our coverage descriptions in laymen’s terms so they’re simple and easy to understand, making the buying experience very clear cut and transparent.

- Own – Our mobile app makes it easy for people to do almost anything, including file a claim, pay your bill, request a tow and access your insurance ID card, and we’re constantly optimizing that experience. We’ve also introduced more flexibility around when and how you pay us, so it becomes a much more painless experience.

- Use –Our photo claims tool allows you to file a claim by simply submitting a photo from your phone, so there’s no need to wait for a claims adjuster to come out and assess the damage. This greatly increases the speed and convenience of filing a claim.

Another thing we’re doing is actually working with regulators to try to make more long-term changes in what we’re able to do for our customers. Insurance has been a certain way for 100 years, but we’re challenging regulators to look at things a little differently. The goal is to encourage a bit more flexibility in how we can engage with our customers, allowing us to further improve their experience.

CO: What are some things that Esurance does to attempt to educate its customers?

NA: We have a resource called Coverage Counselor which helps people understand what coverage is right for them. It’s a really simple way for people to feel more educated and confident that they’re properly protected. To make insurance more affordable we offer DriveSense, which is a mobile app that tracks your driving habits and rewards safe drivers with discounts on their premiums. The safer you drive the more you can save. But more importantly, it’s educating drivers on when they may be engaging in risky driving behavior, so they can improve. We’re not only there for you when something goes wrong, we also want to help people prevent things from going wrong in the first place, and becoming a safer driver helps protect yourself and everyone else on the road.

CO: What made Esurance choose Dennis Quaid as its spokesperson?

NA: We went through a very careful selection process and established criteria to pick the right spokesperson. We wanted an iconic actor who is both credible and authentic, and most importantly, recognized and liked by our target audience. We were also looking for someone who was famous for dramatic roles, but has a dry sense of humor and brings an earnestness that can be funny in ways that are surprising (which was key to the execution of this campaign); someone who is seasoned and confident and could effortlessly personify a challenger brand; someone people wouldn’t expect; and of course, someone who is highly likeable. Dennis Quaid checked all of these boxes. He was a natural choice, and the results have proven he was the right choice! Plus, he’s an Esurance customer!

CO: What was your reaction when someone walked into your office and said: “Hey Nancy, we’re going to do this television commercial, where Dennis Quaid will tell millions of people to send you an email, and we’ll have your email address at the bottom of the screen. You’ll love it.”

NA: I did love it! We really wanted to do something that would engage people and create an open dialogue with consumers so we could get real feedback on how we’re doing. We’re on a journey to make insurance surprisingly painless, and in order to truly be successful we need to be talking to people constantly. This was a unique way to engage people and build relationships, and it’s been well received. We’ve gotten thousands of emails and have been replying to all of them. The choice to have a real Esurance employee in the commercial was easy because we’re all about being transparent. So when Dennis says, “don’t believe me, ask a real Esurance employee,” you better believe you’re going to see a real Esurance employee!

CO: What are some of your favorite emails received?

NA: Well, I’ve received a few marriage proposals! But honestly, it’s been great to see the range of emails that have come in because it means people are excited to engage with us. I do love when people write in with questions about Esurance or how they can save, because it gives us an opportunity to educate them and help them feel more confident in their insurance decisions. It’s also been a great outlet for getting direct feedback on the progress we’re making to improve the customer experience. This opportunity to interact with more people further helps us make insurance simple, transparent and affordable for our customers.

CO: Now that you’ve appeared on screen with Dennis Quaid have your turned all “Hollywood?” Sunglasses in the office? Telling people that they’ll have to talk to your people?

NA: Not exactly. What’s been great about this whole experience is the fact that this ad has really resonated with people in a way we hadn’t expected. Yes, people always want to know if I’m a real person, but more importantly, people also really want to learn more about insurance, and this is a fun entry point for them to get that information.

CO: Would Esurance be interested in purchasing one million copies of my book, “General Liability Insurance Coverage – Key Issues In Every State,” to send to its customers to further their education of insurance? I’m sure I can get you a volume discount.

NA: Haha, thanks for the offer! We’re trying to keep things pretty simple and concise for our customers, but it sounds like an interesting read! |

|

|

| |

|

|

|

|

Vol. 8 - Issue 3

March 20, 2019

Encore: Randy Spencer’s Open Mic

So, Not So Cute Now: Woman Uses Emojis And Gets Sued

|

|

|

|

|

|

| |

As far as I can tell, there are three categories of people when it comes to the use of emojis: (1) those who use them way too much and should have their iPhones confiscated by the FCC (e.g., sending condolences to someone, on the death of their loved one, should not be done via text, using pictures of a crying face and casket; (2) those who never use emojis and, in fact, look down their noses at people who do; and (3) those who understand the purpose of emojis and use them appropriately (e.g., my 9-year old daughter will text me three pictures of an ice-cream cone as her way of saying – let's go to Baskin-Robbins).

But no matter what type of emoji user you are, the Rhode Island trial court's decision in Bertha Hopkins, as assignee of Linda Hopkins v. Roger Williams Ins. Co. teaches us that, if you are going to send a text with emojis, be sure that it doesn't end up in the wrong hands.

Bertha Hopkins hosted a Thanksgiving dinner at her home in 2014. To be in attendance was her daughter-in-law, Linda Hopkins, and several others. Bertha was to make the turkey. In the week leading up to the holiday, numerous group texts went back and forth between Bertha, Linda and other guests, over who would make which side-dishes.

On the day after Thanksgiving, Linda responded to the last group text with a text containing nothing but the following three emojis:  . Someone on the text distribution replied, asking what the text meant. Linda did not respond to the group. However, Samantha Roberts, Bertha's first cousin did. She replied to the group – "the turkey was dry last night." Linda had meant to remove Bertha from the group text before sending it. But she didn't. Bertha received both texts and was not amused. She responded to the group, disputing that her turkey was dry and, in fact, claiming that she was a fantastic cook and had never made a dry turkey in her life. But Bertha didn't stop there. She sued Linda and Samantha for defamation, alleging that both women damaged her reputation as a great cook. See Bertha Hopkins v. Linda Hopkins and Samantha Robbins , No. 15-0236, Superior Court of Rhode Island (2/24/15). . Someone on the text distribution replied, asking what the text meant. Linda did not respond to the group. However, Samantha Roberts, Bertha's first cousin did. She replied to the group – "the turkey was dry last night." Linda had meant to remove Bertha from the group text before sending it. But she didn't. Bertha received both texts and was not amused. She responded to the group, disputing that her turkey was dry and, in fact, claiming that she was a fantastic cook and had never made a dry turkey in her life. But Bertha didn't stop there. She sued Linda and Samantha for defamation, alleging that both women damaged her reputation as a great cook. See Bertha Hopkins v. Linda Hopkins and Samantha Robbins , No. 15-0236, Superior Court of Rhode Island (2/24/15).

Linda sought coverage for the suit from her homeowner's insurer -- Roger Williams Ins. Co. Samantha did not own a home and had no homeowner's insurance.

Linda's policy provided "personal injury" coverage for, among other things, "[o]ral or written publication, in any manner, of material that slanders or libels a person or organization."

Roger Williams Ins. Co. disclaimed coverage to Linda. The basis for its disclaimer was that, while Bertha clearly alleged that Linda libeled her, it had been done by way of emojis, which was not in the form of "oral or written publication of material."

With no defense forthcoming from Roger Williams, Bertha and Linda settled the suit for $20,000. Bertha dismissed Samantha from the action. Linda assigned her rights, under her Roger Williams homeowner's policy, to Bertha. Bertha executed a covenant not to execute the judgment against Linda.

Bertha sued Roger Williams to collect the $20,000 judgment. The court in Bertha Hopkins, as assignee of Linda Hopkins v. Roger Williams Ins. Co., No. 15-5696, Superior Court of Rhode Island (3/3/16) held that no coverage was owed. As the court saw it, the only possible defamation committed by Linda was in the form of the text message that she sent containing the three emoji symbols. While Samantha had sent a text, using words, stating that "the turkey was dry last night," Linda did not use written words to defame Bertha. On that basis, the court concluded that the three emoji symbols were not "written material."

The court chose emojis to state its conclusion:

|

That’s my time. I’m Randy Spencer. Contact Randy Spencer at

Randy.Spencer@coverageopinions.info |

|

| |

|

| |

|

|

|

|

Vol. 8 - Issue 3

March 20, 2019

Belated Happy Mardi Gras: Appeals Court Interprets The “Coconut Exclusion”

|

|

|

| |

This article originally appeared in the March 19, 2014 issue of Coverage Opinions. Sometimes I make stuff up in CO. This is a real case. Really.

Just when you thought you’ve seen it all, along comes Brooks v. Zulu Social Aid and Pleasure Club, 110 So. 3d 703 (La. Ct. App. 2013). At issue was the applicability of the “Coconut Exclusion” in a commercial general liability policy. [And I thought my “Insurance Key Issues” coverage book was pretty comprehensive. Apparently not so much.]

Faith Brooks sustained injuries (at least a broken nose) when a coconut thrown by a rider in the Zulu parade hit her in the face. She and her family filed suit against the Zulu Social Aid and Pleasure Club, alleging that her injuries were caused by: The deliberate and wanton act or gross negligence of the Zulu Krewe and organization, its officers, directors and members, in several non-exclusive ways, including: throwing a coconut from the float directly at Faith Brooks, striking her in the face; failing to enforce the mandatory rules and regulations adopted by the Zulu Krewe and organization, the Mardi Gras Association and the City of New Orleans barring any member or float rider from throwing a coconut or other inherently dangerous hard object from the float at the spectators; and throwing a coconut when Zulu, its members and float riders, knew or certainly should have known, that injury to one or more spectators was substantially certain, if not inevitable. Lloyd’s was named as a defendant in plaintiffs’ first amended petition.

Lloyd’s issued a policy (presumably commercial general liability) to Zulu. Lloyd’s undertook Zulu’s defense under a reservation of rights. The Lloyd’s policy contained, by way of a General Change Endorsement, the oooold “Coconut Exclusion,” which provided: “[i]t is hereby agreed and understood that there will be no coverage for any coconut thrown in any fashion from anywhere on the float. Coconuts may be handed from the first layer of the float only.”

Seems simple enough. This isn’t exactly some manuscript antitrust endorsement in a D&O policy we’re talking about here. Lloyd’s, not milking the case, filed an answer and motion for summary judgment on the same day. The trial court granted Lloyd’s motion.

Zulu went to the Court of Appeal of Louisiana and argued that summary judgment was inappropriate because the petition stated that the claims presented were “non-exclusive.” This, Zulu argued, created the possibility of liability pending further, adequate discovery. In other words, Zulu maintained that it was “impossible to say that the Lloyd’s policy excluded coverage pending adequate discovery.”

The appeals court concluded that Zulu’s argument had merit. The court was quick to point out that, in reaching its decision, it was not meaning to suggest or imply that Lloyd’s appointed counsel rendered anything less than adequate representation to Zulu. “Instead, it merely appears from the record that no discovery was conducted on Zulu’s behalf during the time that it was represented by Lloyd’s appointed counsel.” Under these circumstances, the court held that the trial court “abused its discretion in ruling on the motion for summary judgment before allowing Zulu a meaningful opportunity to conduct discovery. Because there is the possibility that additional discovery could reveal a material issue of fact, the granting of summary judgment at this stage of the case was premature.”

While the court held that summary judgment for Lloyd’s was premature, it seems inevitable that that’s where the case is going. I’ve looked at the Coconut Exclusion six ways from Sunday and I just can’t see any way a policyholder can crack this nut.

|

|

|

|

|

|

| |

|

Vol. 8 - Issue 3

March 20, 2019

26th Annual West Coast Casualty Construction Defect Seminar

Attendees To Receive Complimentary Copy Of 4th Edition Of Insurance Key Issues

|

|

|

|

|

| |

The 26th Annual West Coast Casualty Construction Defect Seminar is being held from May 9-10, 2019 at the Disneyland Hotel in Anaheim. Yes, 26th annual! There are some CD claims that have not been resolved in 26 years.

With 1,500 attendees, this is the must-attend construction defect seminar for all those involved with construction defect litigation and claims -- insurers, coverage lawyers, plaintiffs counsel, defense counsel and those on the science and technology side of CD. This is the Davos of construction defect seminars.

I am delighted to announce that attendees of this year’s West Coast Casualty Construction Defect Seminar will receive a complimentary copy of the 4th edition of General Liability Insurance Coverage – Key Issues In Every State!! How exciting is that!

I’ll be there and I know I’ll see some CO subscribers. It’s a small world, after all.

More information about the 26th Annual West Coast Casualty Construction Defect Seminar is here:

http://www.cvent.com

|

|

|

|

|

|

|

Vol. 8 - Issue 3

March 20, 2019

Contest: Obscure Claims Under A CGL Policy

Win a Copy Of Insurance Key Issues

Get A Coverage Opinions Pen: Just Ask (I Have 10 Left) |

|

|

|

|

| |

In the course of my teaching duties at Temple Law School this semester, I have gone through many important provisions of a commercial general liability policy with the students. Doing so has caused me to notice some terms that I have never even remotely thought about in all these years. And I’m sure that’s the case for many long-time insurance professionals.

For example, I’ve never even come close to having a claim that involved any of the following provisions in a CGL policy:

- The vending machine exception to the definition of “your product”

- An “insured contract” on the basis of a sidetrack agreement

- The exception to the aircraft exclusion for liability assumed under an “insured contract” for the ownership, maintenance or use of the aircraft.

- Coverage for a bail bond, as a supplementary payment, for a “traffic law violation”

- The “war exclusion” for purposes of a claim for “personal and advertising injury”

If anyone has ever been involved in a claim where one of these CGL policy provisions was in play, I’d love to hear about it. The first two people who can tell me the details of such a claim will each get a copy of the 4th edition of Insurance Key Issues. I know. I know. You could just make a story up. But would anyone really do that? We’re talking about a copy of an insurance book. I’m not giving away a Tesla here folks. I trust you. Well, mostly. I reserve the right to cross-examine any entrant if something doesn’t smell right.

Get A Coverage Opinions Pen – Just Ask

I started out with hundreds. I now have just ten Coverage Opinions pens sitting in a drawer. If anyone wants one just ask. The first ten people to reply will get the pen that will change their lives. It’s as life changing as a squip (Broadway trivia). |

|

| |

| |

|

|

|

|

|

Vol. 8 - Issue 3

March 20, 2019

Fill In Your Insurance Coverage Bracket:

64 Coverage Issues – Which Is The Most Interesting?

|

|

|

|

This insurance coverage bracket originally appeared in the March 14, 2016 issue of Coverage Opinions.

If you are reading this it means you are wondering if Saint Mary's has a prayer in the opening round of the NCAA Men's Basketball Tournament. Look, your bracket is going to be busted by Thursday night, when that number 8 seed you took to make it to Final Four go down in flames. It serves you right for listening to some expert on ESPN.com. When it comes to the NCAA Tournament bracket, I'd put my money on Mildred from HR over an ESPN expert any day of the week.

Rather than be frustrated that you’ve wasted ten bucks on the NCAA office pool once again, fill in the Insurance Coverage Bracket and choose the most interesting coverage issue. You can’t lose – since there is nothing to win. But if there were, you would still lose to Mildred from HR.

|

|

| |

| |

|

|

|

|

|

Vol. 8 - Issue 3

March 20, 2019

Geez, This Is Really Pathetic

|

|

|

|

|

| |

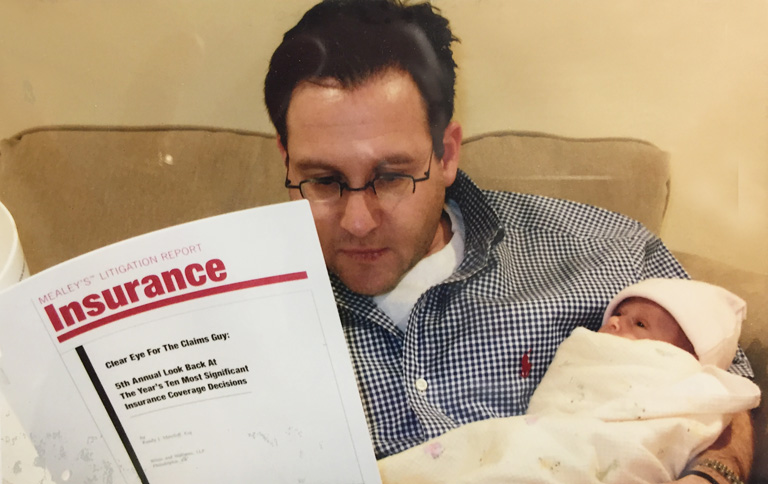

I was going through a rarely used drawer in my office recently and came upon this picture that I had forgotten about. It was taken on April 16, 2006. My daughter was ten days old at the time. And there I was -- reading her the 5th annual Top 10 Coverage Cases of the Year article.

Don’t worry – I read her real books too – like that that children’s classic: Oh, The Places In An Insurance Policy You’ll Go.

|

| |

|

|

|

|

| |

|

Vol. 8 - Issue 3

March 20, 2019

The Wall Street Journal Looks At The History Of Insurance

|

|

|

|

The Weekend Wall Street Journal is the proverbial box of chocolates. And imagine my surprise a couple of weeks back when I found this gem – an article on the history of insurance.

In “Insuring Against Disaster” (February 23-24), columnist Amanda Foreman looks at the history of insurance and goes way, way back – to the Babylonians and the 18th Century B.C. Code of Hammurabi, which, the author says, provided a “primitive form of insurance known as ‘bottomry.’ According to the Code, merchants who took high-interest loans tied to shipments of goods could have the loans forgiven if the ship was lost. The practice benefited both traders and their creditors, who charged a premium of up to 30% on such loans. The Athenians, realizing that bottomry was a far better hedge against disaster than relying on the Oracle of Delphi, subsequently developed the idea into a maritime insurance system. They had professional loan syndicates, official inspections of ships and cargoes, and legal sanctions against code violators.”

Interestingly, the article points out that in “Christian Europe, insurance was widely frowned upon as a form of gambling—betting against God. Even after Pope Gregory IX decreed in the 13th century that the premiums charged on bottomry loans were not usury, because of the risk involved, the industry rarely expanded.”

It’s an interesting article and one worth checking out. |

| |

|

| |

|

|

|

|

|

Vol. 8 - Issue 3

March 20, 2019

Alaska Supreme Court And A Lawyer’s Advice On Dealing With A Bad Faith “Set-Up”

Gary Zipkin: From America’s Coolest Coverage Lawyer To Its Hottest

|

|

|

|

|

| |

Back in early 2014 I interviewed Gary Zipkin of Anchorage’s Guess & Rudd, P.C. I was fascinated to learn about practicing coverage law in Alaska. If three cars hit a moose, is that one “occurrence” under the moose’s auto policy? So who better to ask than someone doing it for 45 years on the carrier-side (and Best Lawyers’s 2013 “Insurance Lawyer of the Year” for Alaska).

At the time, I dubbed Gary Zipkin the coolest coverage lawyer in America. Gary, who just turned 70, is now wrapping up his career in Alaska and easing into retirement – in Hawaii. He tells me his home on the Big Island offers him and his wife, Barbara, a beautiful view of both Mauna Kea and Mauna Loa. These volcanoes are dormant. If that changes, Gary will no doubt come out of retirement and handle volcano coverage cases.

Gary Zipkin is no longer the coolest coverage lawyer in America. He is now the hottest.

Gary leaves behind a legacy of coverage work. So much of Alaska’s coverage law is the product of cases in which Gary was involved. And here’s one more. Even on his way out the door, Gary Zipkin is making coverage law in Alaska.

Allstate Insurance Co. v. Kenick, No. S-16509 (Alaska Jan. 25, 2019) addresses a procedural issue – the preclusive effect of a federal court declaratory judgment, in favor of an insurer, against its insured in a subsequent state court proceeding. But, as Gary explains in his write-up below, the case offers so much more -- a lesson for insurers facing a bad faith “set up.”

A single-car accident, causing multiple injuries to the teenage female passenger, led to a third-party claim against the driver. Liability was never in doubt but the passenger’s injuries, though significant, did not appear permanent or disabling in the long-term. The attorney for the passenger subsequently sent a poorly worded demand letter to Allstate’s adjuster that demanded policy limits by a date certain or, alternatively, Allstate’s agreement to negotiate a settlement pre-suit. Allstate’s adjuster responded by saying, in effect, that Allstate would extend a settlement offer within 2 weeks of the purported deadline – which it did, offering full policy limits in settlement.

At that point, the passenger brought in new counsel, who immediately announced that Allstate’s offer was untimely, that Allstate had missed a firm deadline for tendering offering limits, and that Allstate was therefore in breach of its duty of good faith and fair dealing. The new attorney announced that the passenger would no longer be willing to accept policy limits since her injuries were worth so much more than limits.

Anticipating that its insured would soon enter into an agreement with the passenger whereby the insured would agree to a consent judgment and assign his rights against Allstate to the passenger, Allstate initiated a declaratory judgment action in federal court, asking the court to confirm that Allstate had not breached its contractual duties. A few months later, after the insured had entered into that arrangement, Allstate amended its DJA to seek the court’s determination that the consent judgment was invalid and unenforceable against Allstate.

The federal action proceeded to a jury trial where I was lead counsel for Allstate, and the jury’s unanimous verdict confirmed that Allstate, acting through its adjuster, had acted reasonably in response to the original demand letter by offering full policy limits in settlement of the third-party claim two weeks after the alleged deadline.

This verdict was then appealed to the Ninth Circuit (where I presented Allstate’s arguments) and the appeals court affirmed the judgment in all key respects -- reversing only the trial court’s decision, following the verdict, that the insured’s consent judgment (for more than 20 times the amount of policy limits) and assignment of rights, although unexcused and therefore a breach of the insured’s duty to cooperate, did not void the Allstate policy, meaning that Allstate remained obligated to pay the policy limits it had offered – but no more than policy limits.

Nevertheless, the passenger’s attorneys (including the attorney who had tried and lost the federal case and the appeal) were able to convince a state superior court judge that the federal action had not foreclosed a separate state court action against Allstate and its adjuster based on a claim and theory of negligent adjusting, and that the passenger (and her mother, who asserted her own negligent infliction of emotional distress) could also seek punitive damages against Allstate on the theory that the adjuster’s conduct was reckless. The state court claim then proceeded to trial in the locale where the passenger and her mother had resided and resulted in a huge award that included the full amount of the underlying consent judgment and millions more for punitive damages.

Allstate then appealed to the Alaska Supreme Court, arguing (primarily) that the federal verdict and judgment precluded the state court action because the federal jury’s decision that Allstate had acted reasonably precluded a second claim against Allstate or its adjuster (whose conduct Allstate had ratified) based on the very same conduct, whether presented as a negligence claim or as a contract claim. The court vacated and reversed the state court judgment, vindicating both Allstate and its adjuster, both of whom now seek awards of attorney’s fees and costs in the trial court (since Alaska law permits the prevailing party in all civil actions to recover a portion of its attorney’s fees from the losing party or parties – but that’s a story for another day!).

The key takeaways from this case are that insurers facing these kinds of “set-ups” are not defenseless and can take proactive steps, such as filing a declaratory judgment action in federal (or state) court and ratifying the conduct of its adjuster, thereby taking the initiative and changing the narrative. In this example, Allstate became the plaintiff in the DJA, with the burden of persuasion, yes, but also with the opportunity to put its case on first and to speak both first and last during final argument. Those advantages should not be overlooked.

Gary added some additional anecdotes:

Here’s something that readers may ask themselves – didn’t Allstate file a Petition For Review with the Alaska Supreme Court immediately following the ruling by the state court judge allowing the case to proceed in state court? The answer is that Allstate did file a Petition For Review, seeking an interlocutory order that would stop the state court action from proceeding. That petition was denied – for unknown reasons. Perhaps the Supreme Court was busy dealing with other cases, who knows?

I actually presented a 2-day lecture about this case to an Insurance Law class at Harvard Law School (approximately a year before the Supreme Court’s decision) and one of the students asked whether Allstate had considered filing a motion or petition in federal court under the exception to the Anti-Injunction Act, seeking an order from the federal court stopping the state court action.

What a GREAT question! I explained that the defense attorneys were so confident the state court judge was not going to allow the case to proceed to trial in state court that we elected not to do so. Having chosen that approach, Allstate could no longer go to federal court for such relief. The professor (Bruce Hay) has now invited me back to speak with his class once again now that the Supreme Court has decided it. I can’t wait. Those students are “wicked-smart!

|

| |

|

|

|

|

|

Vol. 8 - Issue 3

March 20, 2019

Insurer Wins $15 Million From Its TPA For Mishandling A Policy Limits Demand

|

|

|

| |

Clearly things did not go well between QBE and American Claims Management, Inc., its third-party claims service administrator, on one particular automobile liability claim. QBE alleged that it sustained significant damages on account of the alleged failure of ACM to follow the parties’ claims management agreement.

The California Court of Appeal decision in QBE Ins., Inc. v. American Claims Management, No. D073345 (Cal. Ct. App. Feb. 4, 2019) involves the aftermath of an arbitration award for QBE over the handling of the claim. The court described the claims handling scenario as follows:

“In February 2011, Cortes was involved in a traffic collision with the Cardonas. Cortes’s insurance policy had a $30,000 liability limit per accident. That month, the Cardonas mailed a policy limits demand to ACM, giving it 15 days to respond. When ACM sought to accept the offer after the deadline had elapsed, the Cardonas rejected it. In November 2012, the Cardonas sued Cortes. With QBE’s approval, ACM hired attorneys to defend Cortes. In June 2015, following a trial, the Cardonas obtained a judgment against Cortes in the amount of $20,974,903.

ACM did not timely communicate to QBE its receipt of the demand letter. The Panel wrote in its final award: ‘In what would become a disturbing pattern, ACM also neglected to inform QBE that [] Cardona had called ACM . . . to follow up on his demand letter, that the demand letter expired . . ., and that [an ACM employee who was subsequently fired] failed to contact Cardona until [after the demand letter’s deadline]. In other words, ACM apparently chose to withhold from QBE evidence of its own negligent performance under the Agreement that . . . had potentially exposed ACM to hundreds of thousands, if not millions of dollars for bad faith.’

In June 2016, ACM and QBE further stipulated that $15 million was a reasonable amount to settle the Cardona lawsuit against QBE, and it was a good faith settlement. They agreed that no party can challenge the amount of the settlement, and no party ‘will assert that the other party acted as a volunteer by entering into the settlement.’ QBE subsequently paid the Cardonas that amount.

QBE sued ACM to recover the $15 million settlement plus more than $1 million in legal fees that QBE incurred in the related action.”

The arbitration panel ruled that QBE proved that ACM was deficient in the performance of its responsibilities to QBE under the claims management agreement. The Panel ruled: “The starting point for the Panel’s analysis of contract damages is with ACM’s failure to timely review the letter demand, timely respond thereto and ultimately pay policy limits on behalf of Cortes. Had it done so, QBE would have only incurred an expenditure of $30,000[ ], [Cortes’s] full policy limits. . . . QBE ultimately paid $15 [million] to resolve the Cortes and Cardonas claims. All but $30,000[ ] of this payment was required because of ACM's breach.”

The court’s decision does not address the ins and out of ACM’s alleged failure to follow the parties’ claims management agreement with respect to the demand to settle. That’s what the arbitration was about.

Instead the court addressed ACM’s argument that the arbitration award should not be confirmed and, instead, vacated or corrected. But the court did not do so. As it explained, its hands were tied: “Considering the strong public policies favoring arbitration as a speedy and relatively inexpensive means of dispute resolution, the scope of judicial review of private, binding arbitration awards is extremely narrow. (citations omitted). We can neither review the merits of the controversy, the arbitrator’s reasoning, or the sufficiency of the evidence supporting the award, nor correct or vacate an award because of an arbitrator’s legal or factual error, even if it appears on the award’s face.”

The appeals court concluded that ACM’s claims, as to why the arbitration award should not stand, were assertions of legal error. This, the court explained, was outside the scope of its permissible review of an arbitration award: “[t]he arbitrator’s resolution of these issues is what the parties bargained for in the arbitration agreement.”

Given the extent to which some insurers use TPAs for handling claims, situations no doubt arise where the insurer disagrees with a TPA’s actions. But this one is a doozy of a coulda, shoulda situation.

|

|

|

|

|

|

|

Vol. 8 - Issue 3

March 20, 2019

Does SIR Apply To First Layer Only Or All Excess Layers?

|

|

|

| |

Deere & Company v. Allstate Insurance Company, No. A145170 (Cal. Ct. App. Feb. 25, 2019) involves an interesting excess-related coverage issue. Excess cases often do not get discussed in Coverage Opinions, as they can be policy-language driven. As a result, they may be too unique to offer a lesson or guidance for future cases. And offering such guidance is one of the key factors for choosing a case for inclusion in CO. But Deere & Company merits discussion here because it’s a unique issue and the court’s decision turned on policy language that is not unusual.

At issue in Deere was coverage for claims filed against Deere, for bodily injury, caused by exposure to Deere’s asbestos containing products – brakes, clutch assemblies and gaskets used in Deere’s machines. Needless to say, it’s complicated. It involved coverage under 100+ policies issued to Deere from 1958 to 1986. The trial was in three phases between 2006 and 2013. Someone could have completed law school – twice – in less time.

The recent California appellate court decision addressed how to treat the self-insured retention in Deere’s policies. Of note, Deere’s insurance program, for its products claims, did not include primary policies. Instead, Deere had a series of first layer umbrella policies that provided coverage in excess of a self-insured retention. It ranged from $50,000 to $1,500,000 over time. Deere also had several layers of excess policies that sat above the first layer umbrella policy.

The issue before the court was this: Coverage under the first layer umbrella policies was subject to Deere’s satisfaction of the self-insured retention. But what about the excess policies above that? Was coverage under those policies also subject to satisfaction of the self-insured retention?

The trial court answered yes. The appeals court reversed.

The court set out a variety of policy language and observed that the issue was tied to the extent that the “following form” provision incorporates the terms of the underlying policies. Critical to the court’s analysis was that the scope of coverage, under a following form policy, is generally subject to the same conditions and limitations as the underlying policy – but with the exception for the limits of liability.

The court had little trouble reaching its conclusion that the SIR was not applicable to the excess layers above the first layer umbrella: “The plain language of the first-layer umbrella policies and the higher-layer excess policies makes clear that Deere has no obligation to pay additional retained limits once the aggregate limits of the underlying policies have been satisfied. Section two of the higher-layers policies is entitled ‘Limit of Liability—Underlying Limits’ and provides that the only precondition to liability attaching to the higher-layers policies is that the ‘Underlying Umbrella Insurers have paid or have been held liable to pay the full amount of their respective ultimate net loss liability’ of $10 million (varies per policy) per occurrence, but $10 million (varies per policy) in the aggregate. It further states that the higher-layer insurer ‘shall then be liable to pay only the excess thereof … .’ This section says nothing about higher-layer excess coverage being conditioned on Deere paying any additional SIR or retained limit before liability attaches. Moreover, there is no language in this provision that justifies treating Deere as an underlying umbrella insurer or treating the retained limits in the underlying policies as ‘insurance’ for this purpose.”

|

|

|

|

|

|

|

Vol. 8 - Issue 3

March 20, 2019

Court Addresses Coverage For Wile E. Coyote v. Acme Anvil Company Claims

|

|

|

| |

Can you imagine if Wile E. Coyote brought products lability claims against all those Acme-named companies from which he bought devices to try to take down the Road Runner. The devices always backfired, leading to all manner of serious injuries. Acme’s general liability insurer would surely need some serious manuscript endorsements to address this challenging exposure.

I couldn’t help but think of an anvil, falling on top of the Coyote, when I saw the exclusion at issue in United Specialty Ins. Co. v. Everest Construction, No. 18-45 (D. Utah Feb. 28, 2019).

Kimberly Delobel, a building inspector, filed suit against Everest Construction, after she was seriously injured upon being struck by an eighty-five pound package of roofing shingles that had been thrown, by an Everest employee, off the roof of a building at a construction project.

Everest sought coverage from its general liability insurer, United Specialty. The insurer denied that it owed a defense, citing that oooold “Fall From Heights” exclusion:

“Bodily injury” sustained by any person at the location of the incident, whether working or not, arising out of, resulting from, caused by, contributed to by, or in any way related to, in whole or in part, from a fall from heights. For purposes of this exclusion, a ‘fall from heights’ shall be defined as a fall from any elevation where there is a height differential between surfaces. This also includes the fall of an object causing, contributing to, or in any way relating to, in whole or in part, a person sustaining “Bodily injury.”

Everest argued that the “Fall From Heights” exclusion did not apply because the bag of shingles did not “fall” off the roof, but, rather, it was thrown. As Everest saw it, the “Fall from Heights” exclusion was silent as to thrown objects.

The court agreed: “United Specialty argues that ‘fall’ includes an object thrown from above. But the court agrees with the Defendants that United Specialty’s interpretation is strained. The court concludes, after having reviewed the various dictionary definitions cited by the parties, that the usually accepted understanding of ‘fall’ means that an object drops to the ground without involvement by a human actor.”

Unique issue. Interesting decision.

I reached out to Everest Construction for comment. A company spokesperson had two words to say: “Meep Meep.”

|

|

|

|

|

|

|

Vol. 8 - Issue 3

March 20, 2019

Court Shows The Perils Of Withdrawing A Defense – Even If The Right Exists

|

|

|

| |

Withdrawing an insured’s defense can be perilous business for an insurer. In my experience it is a decision that insurers take seriously. And it is an action that they do not take frequently. Lots of courts say that an insurer has a duty to defend its insured until there are no potentially covered claims remaining. But there is not a lot of guidance beyond this easy to say statement of law – especially when it comes to what information the insurer can consider in determining that there are no potentially covered claims remaining.

The paradigm withdrawal situation (and the easiest one, if there’s such a thing) is when the only potentially covered count has been dismissed from the case, such as by the plaintiff or court. But that happens infrequently. The more challenging scenario is when an insurer believes that it can withdraw a defense based on information revealed during discovery. Can that information be considered by an insurer to withdraw its defense, in the face of a complaint (or a complaint and other information, in an “extrinsic evidence” state) that still triggers a defense?

Putting aside these legal issues, there is another factor that insurers consider when it comes to withdrawing a defense. Doing so, especially close to trial, can have bad optics. In any subsequent coverage litigation, it will be easy for the insured to paint the insurer as having abandoned its insured. Somerset Pacific LLC v. Tudor Insurance Company, No. 17-7099 (E.D. La. Feb. 5, 2019) demonstrates a timing factor that insurers should not overlook when considering the withdrawal of a defense.

Tudor Insurance Co. defended Somerset Pacific in a personal injury action. A two-year old child was severely burned by hot water in an apartment complex owned by Somerset. Somerset was insured under a $1,000,000 primary liability policy issued by Tudor and a $10,000,000 excess policy issued by National Union.

Four months before trial, Tudor settled the case, for its policy limit, but did not secure a release of Somerset’s excess exposure. At that point, Tudor’s plan was for its counsel to withdraw after the excess carrier, National Union, assumed the defense.

However, National Union did not accept the defense right away. A dispute arose over it. After National Union did accept Somerset’s defense, counsel retained by Tudor withdrew from the case. Somerset was now forced to switch to new defense counsel just months before trial.

[While this was going on, Somerset retained its own counsel, as it saw the risk of uninsured exposure.]

Tudor maintained that, “pursuant to Louisiana law it has a right to settle for its policy limits without securing a release of Plaintiff’s uninsured exposure provided the settlement does not prejudice Plaintiff. Tudor argues that Plaintiff cannot show that the settlement prejudiced it because Tudor continued to defend Plaintiff after its settlement until its excess carrier assumed its defense, and Plaintiff was not ultimately subject to any uninsured liability.”

Even if all that’s true – the legal principle and lack of uninsured exposure -- the court still held that Tudor could be liable for bad faith – a decision not made by the court as it concluded that it involved fact issues.

True – the insured was never without defense counsel. But the problem for Tudor had to do with the timing of its decision to withdraw. The court explained: “[T]he insurer must make every effort to avoid prejudicing the insured by the timing of its withdrawal from the litigation. . . . Arguably there may be a point in ongoing litigation at which the insurance company’s withdrawal from the defense of the insured would be so prejudicial to the insured’s interests that it would constitute a breach of the company’s duty to act as a fiduciary toward the insured and to discharge its policy obligations in good faith. Although Plaintiff was never left without a defense, a jury could find that the timing of Tudor’s withdrawal, and the dispute that accompanied it, prejudiced Plaintiff and required it to incur additional attorneys’ fees in protecting its interests.”

|

|

|

|

|

|

|

Vol. 8 - Issue3

March 20, 2019

“Claims Made” Insurers Take Notice: Policy Language Deficient For “Relation Back” Argument

|

|

|

| |

The Ninth Circuit’s decision in Attorneys Insurance Mutual Risk Retention Group, Inc. v. Liberty Surplus Insurance Corp., No. 17-55597 (Feb. 15, 2019) is very short – about a page. But it still has a lot to say. And it is a decision that insurers, that write “claims made” policies, should pay close attention to.

At issue was coverage for attorney J. Wayne Allen, under professional liability policies issued by Liberty Surplus Insurance Corp., for claims arising out of a probate case and related action. [Attorneys Insurance Mutual Risk Retention Group had been defending Allen and was seeking contribution for defense costs.]

Liberty had issued a 2009-2010 policy and a 2010-2011 policy. A probate case had been filed against Allen during the 2009-2010 policy period. A related civil action was filed against Allen during the 2010-2011 policy period.

Liberty maintained that it owed no coverage by asserting a commonly-used “relation back” argument. Specifically, Liberty argued that Allen failed to report the probate case to it during the 2009-2010 policy period. Thus, when Allen sough coverage for the related civil action, under the 2010-2011 policy, Liberty argued that none was owed, because it related back to the earlier probate case. Thus, the civil action was also considered to have not been reported during the 2009-2010 policy period.

Liberty’s argument was based on the following provision contained in the 2010-2011 policy:

“Claims alleging, based upon, arising out of or attributable to the same or related acts, errors or omissions shall be treated as a single Claim regardless of whether made against one or more than one Insured. All such Claims, whenever made, shall be considered first made during the Policy Period or any Extended Reporting Period in which the earliest Claim arising out of such acts, errors or omissions was first made, and all such Claims shall be subject to the same Limits of Liability.”

Critical to the court’s analysis was the 2010-2011 policy’s definition of “Policy Period:” “the period from the Inception Date of this Policy to the Policy Expiration Date as set forth in the Declarations or its earlier termination date, if any.” (emphasis added). The “Declarations” identified the policy period as July 31, 2010 until July 31, 2011.

Here’s where it got problematic for Liberty. Under the definition of Policy Period – which refers to this policy -- the later related civil action, filed against Allen during the 2010-2011 policy period, was considered first made during the 2010-2011 policy period. In other words, the language of the 2010-2011 policy did not support relation back to the 2009-2010 policy.

The 2010-2011 policy’s reference to “policy period” is clearly intended to be a reference to an earlier policy’s policy period. However, the language did not support it. The court stated: “As the district court correctly noted, ‘[a]dopting Liberty’s interpretation would require the court to give different meanings to the same term used in the same policy, which would run afoul of the rules of contract interpretation.’”

Claims made insurers – check your policies. It is an easy fix.

|

|

|

|

|

|

|

Vol. 8 - Issue 3

March 20, 2019

Unique Issue Regarding Duty To Defend A Class Action

|

|

|

| |

I’ve always found this to be an interesting duty to defend issue. A class action complaint is filed against the insured. The complaint describes some injury or damage sustained by the named plaintiff(s). These named plaintiff(s) allegations do not trigger a duty to defend. However, it’s a putative class action. If it is certified, there could be hundreds or thousands of plaintiffs. And some of their claims may trigger a duty to defend. But the class has not been certified. And it may never be certified. And if the duty to defend is tied to the allegations in the complaint -- Look, the allegations in the complaint do not trigger a duty to defend. You can see what’s going on here.

While the issue does not arise everyday, it has not gone without some judicial consideration. And courts have held that the potential claims, of a putative class, can trigger a duty to defend. Given the defense costs that can arise in a class action, this can be no small issue.

This was the situation before the court in Liberty Mutual Insurance Co. v. Dometic Corp., No. 17-882 (N.D. Ind. Mar. 6, 2019). Dometic Corp. was named as a defendant in three putative class actions alleging that it sold “gas absorption refrigerators, mainly for RVs, containing a defective cooling unit that can leak flammable gases and cause fires.” Liberty undertook Dometic’s defense, under a reservation of rights, and filed an action seeking a declaratory judgment that it had no duty to defend or indemnify Dometic for the underlying complaints.

At issue were Liberty Mutual’s one-year general liability policies issued to Dometic between 2001 and 2004.

The two competing arguments were just what you would expect to see:

“Liberty Mutual first argues that it has no duty to defend Dometic against the underlying complaints because no named plaintiffs allege a potentially covered property damage claim during a policy period. It’s undisputed that the property damage claims of the named plaintiffs in the underlying complaints all occurred years after the Liberty Mutual policies expired. Liberty Mutual therefore contends it has no duty to defend because ‘[i]f the pleadings reveal that a claim is clearly excluded under the policy, then no defense is required.’”

“Dometic argues that although the named plaintiff’s claims fall outside of the coverage periods, the court can and should consider the putative classes’ claims, which would fall within the unexhausted policy coverage periods.”

The court noted that, while there were no cases addressing Indiana law on the issue, courts outside of Indiana have done so. The court was able to cite to, and discussed, several decisions holding that the potential claims, of a putative class, can trigger an insurer’s duty to defend. And importantly, the court noted that Liberty could point to no cases that disagreed.

Without getting into some of the weeds, at the heart of the court’s decision was that, while the property damage claims of the named plaintiffs all occurred years after the Liberty Mutual policies expired, the complaints alleged that hundreds or thousands of fires had caused millions of dollars in property damage. The court rejected Liberty’s argument that the putative class claims were too remote or speculative to trigger a duty to defend.

Following its conclusion that no exclusions applied, the court held that Liberty had a duty to defend its insured.

|

|

|

|

|

|

|

| |

|

|

Ohio Supreme Court To Address Allocation

Ohio’s top court has agreed to answer the following question: “Whether an insured is permitted to seek full and complete indemnity, under a single policy providing coverage for ‘those sums’ the insured becomes legally obligated to pay because of’property damage that takes place during the policy period, when the property damage occurred over multiple policy periods.” Lubrizol Advanced Materials, Inc. v. Natl. Union Fire Ins. Co., No. 2018-1815 (Ohio Mar. 6, 2019).

South Carolina High Court Allows Insurer To Sue Defense Counsel For Malpractice

In what may be the longest decision I’ve ever seen addressing this issue, the Supreme Court of South Carolina held in Sentry Select Ins. Co. v. Maybank Law Firm, LLC, No. 27865 (S.C. Mar. 6, 2019) that an insurer may maintain a malpractice action against counsel hired to represent its insured. The court elaborated: “However, we will not place an attorney in a conflict between his client’s interests and the interests of the insurer. Thus, the insurer may recover only for the attorney’s breach of his duty to his client, when the insurer proves the breach is the proximate cause of damages to the insurer. If the interests of the client are the slightest bit inconsistent with the insurer’s interests, there can be no liability of the attorney to the insurer, for we will not permit the attorney’s duty to the client to be affected by the interests of the insurance company. Whether there is any inconsistency between the client’s and the insurer's interests in the circumstances of an individual case is a question of law to be answered by the trial court.”

PA Construction Defect: Indalex Controls Over Kvaerner (Product-Based Claim)

This is inside baseball except for those who follow Pennsylvania law concerning coverage for construction defects. For those who do, this will make sense. In Brayman Constr. Corp. v. Westfield Ins. Co., No. 18-00457 (W.D. Pa. Mar. 6, 2019), the court held that Kvaerner did not apply, and, instead, Indalex dictated an “occurrence:” “Here, in its original demand, Brayman alleged that Gavco breached the subcontract and its warranties by delivering defective and nonconforming concrete to the project, particularly with respect to the drilled shafts of Piers 1, 3, 5 and 6 of the bridge structure. Further, Brayman alleged that Gavco’s defective concrete negatively impacted the project and caused Brayman damages in the drilled shafts of the bridge structure. These allegations support that Gavco’s defective concrete caused damage to something other than the concrete itself, namely the drilled shafts. Thus, the original and amended demand alleged a product-based tort claim, different from the holding in Kvaerner and the other cases cited by Westfield, which involved claims for faulty workmanship and/or were decided before Indalex. . . . Brayman has sufficiently alleged that Brayman claimed against Gavco for coverage for an ‘occurrence sufficient to support a duty to defend and to indemnify under the holding in Indalex.”

Peach Clobber For Policyholder: Pollution Exclusion Applies To Welding Fumes

In a decision about as surprising as the Globetrotters beating the Washington Generals, the Eleventh Circuit, applying Georgia law, held that a pollution exclusion precluded coverage for bodily injury caused by occupational exposure to welding fumes containing iron. Based on existing Georgia law, the court’s decision in Evanston Ins. Co. v. Sandersville R.R. Co., No. 17-14487 (11th Cir. Feb. 8, 2019), that welding fumes, for purposes of the pollution exclusion, unambiguously qualify as an irritant or contaminant, should not leave anyone flabbergasted.

WSJ: California Market For Homeowner’s Policies Challenging

This lead from the front page of the February 11, 2019 Wall Street Journal: “Californians who want to insure their homes against the next wildfire are paying a price for two years of record-breaking blazes. Home-insurance companies in the Golden State are canceling some policies, refusing to sell new ones in certain areas and applying for rate increases as they look to reduce wildfire risk.” [Nicole Friedman; “After Fires, Insurance Holders Struggle”]

Need For Insurer To Reserve Rights For Each Insured

In Auto-Owners Ins. Co. v. Cribb, No. 17-106 (N.D. Ga. Feb. 5, 2019), the Northern District of Georgia made clear that an insurer’s rights must be reserved for each insured individually. And, of significance, doing something I’ve never seen before in an ROR case, the court pointed to policy language to support this point: “Here, the policy was issued to ‘Insured: Brian Thurman & Richard Davis DBA BR Mountain Homes, LLC’. Each insured is treated separately for purposes of coverage, by way of the ‘separation of insureds’ provision in the policy: [text of provision].”

|

| |

|

|

|

| |

| |

|

|

|

|

|

|

|

|

|