|

|

|

|

|

|

Vol. 7 - Issue 7

September 26, 2018

|

|

|

|

|

|

| |

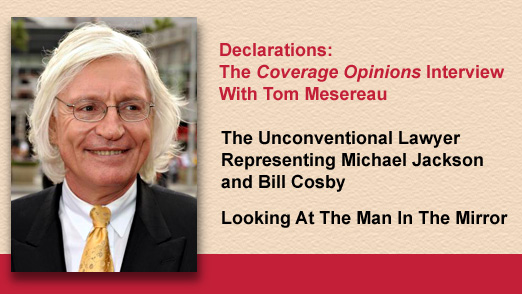

Tom Mesereau could have been the most famous lawyer on the planet. It would have been easy. It was 2005. Michael Jackson was getting ready to go on trial for various charges of sexual molestation. The proceeding was going to be the most-followed criminal trial on Earth since Tyrannosauruses roamed. Mesereau, Jackson’s lawyer, would be spending the next five months sitting inches away from the King of Pop. If the trial had been televised, Mesereau would have been seen in every living room from Toledo to Taipei. He would have spent the rest of his life unable to walk down the street in Tanzania without being recognized.

But the Jackson trial was not televised. Mesereau objected to cameras in the courtroom, despite that people in the Amazon, who’d never met an outsider, would now know his name. I pointed all of this out to Mesereau. But, he explained, “having witnesses see what other witnesses are saying, and then potential witnesses watching what commentators on T.V. were saying about the testimony,” would not have been beneficial to Jackson. Some lawyers make it about themselves, Mesereau told me. “That’s not what I do.”

Michael Jackson beat it – something that many said was impossible. Jackson would have turned 60 years old on August 29th. Just days before, I spent an hour on the phone with the lawyer who achieved that feat for the man who moonwalked. The silky-voiced Mesereau, once named as one of Barbara Walters’s “Ten Most Fascinating People,” was kind enough to speak to me from his Los Angeles office about his astonishing 40-year career, getting acquittal after acquittal in courtrooms across the country.

Mesereau, with his trademark long white hair [there were times it was brownish, he joked] has represented other high-profile individuals, such as Mike Tyson (rape charges dropped), Robert Blake (broke legal ground by securing bail in a potential death penalty case, following a three-week televised preliminary hearing), Joe Babajian, real estate agent to the stars (acquitted on fraud charges) and, most recently, Bill Cosby against sexual assault charges in Pennsylvania. Cosby was found guilty. Mesereau’s practice involves both white collar and violent crimes, often murder and sexual assault. He has spent two decades traveling to the Deep South to handle death penalty cases pro bono. And, on Saturdays, many meet at a Los Angeles church to provide services at the Mesereau Free Legal Clinic.

Tom Mesereau is an easy guy to figure out. The 68-year old son of an Army lieutenant colonial (close aide to General Douglas MacArthur) and grandson of the owner of the famed Mamma Leone’s restaurant in Times Square, has a simple secret sauce -- a lack of fear for the unconventional. Mesereau dished it out for me. We also discussed his recent defeat in the Cosby case, which he called “the most unfair trial I have ever been part of.” And he shared what goes through his mind when a Michael Jackson song comes on the radio.

A Lawyer Looking For His Way

Tom Mesereau’s road to the criminal defense bar was a circuitous one. Following a B.A. from Harvard and Master’s from the London School of Economics, the 1979 graduate of the University of California, Hastings College of Law bounced around -- a year at Hunton & Williams in D.C. followed by another as a prosecutor in California. From there he served as assistant to the president of a Getty Oil subsidiary. It wasn’t until Mesereau got to a small civil firm, where he was bringing in criminal cases, that the peg finally fit.

Mesereau’s resume presents a picture of a lawyer trying to find his way, I suggested. “I think that’s true,” he replied. “Most lawyers,” Mesereau explained, “lack the courage or the gumption to switch subjects. They try something and then they don’t like it and they try the same thing in another form.” But Mesereau did not fall into this trap. “What I was always willing to do was make a radical change if I thought it was a good idea. Everything interested me initially because I am interested in life, I am interested in people, I am interested in society so any subject was interesting for a while. But then the question would always come up ‘are you going to have passion for this the rest of your career?’”

I joked with Mesereau that he seems like the last lawyer in the world who would enjoy big firm life. “That’s correct,” he replied -- in a nanosecond. Mesereau had high praise for the “outstanding lawyers” at Hunton & Williams. But the firm wasn’t for him, concluding that “any organization requires that you master a set of survival skills and I realized that I had no interest in mastering such a set of skills.”

Despite Mesereau’s time at Hunton & Williams being limited to a year, it gave him a taste of criminal law, where he was involved in responding to the largest subpoena ever issued by the Federal Energy Regulatory Commission.

From this morsel, Mesereau next took a very large bite – joining the Orange County, California District Attorney’s office. But he quickly realized that he didn’t have the stomach for it. Mesereau’s first case was to prosecute a young woman for petty theft from a department store. He learned that the defendant had a history of physical, sexual, emotional and drug abuse. “My first instinct,” Mesereau told me,” was to want to hug this poor soul and get her the proper help but I was being asked to convict her.” He got the conviction. Afterward the other D.A.s wanted to celebrate. But Mesereau said he was “disgusted.” “I realized my compassion for people, my empathy for people who are poor or disenfranchised or had a tough go in life, was going to prevent me from being a particularly effective prosecutor.”

The Unconventional And Unpredictable Trial Lawyer

Mesereau has his pick of cases. But there are only so many hours in the day. How does he decide which ones to take?, I wondered. Some of it has to do with his current caseload and trial schedule, he explained. But he added that “the challenge can be very important.” Mesereau made clear that he is “not a criminal lawyer who cherry-picks cases. I am well aware of some lawyers who have been fortunate enough to win big cases and then they’re very careful with what they take, lest they lose one. I am not that kind of lawyer. I take pride in trying one difficult case after another. . . .I didn’t win the Michael Jackson case and then decide I’m not going to take tough cases. That’s not how I behave.”

Mesereau’s website describes himself as an “unconventional, unpredictable trial lawyer.” What does that mean? He explained it to me this way: “I said to myself at one point there’s got to be a reason why certain lawyers become the best and others don’t. Because you have to assume that most lawyers are intelligent, most lawyers are highly educated, most lawyers take a trial practice course or two. So why are some better than others? It can’t because they do the same thing that everybody else does. So early in my career I tried to figure out what the great lawyers did that others didn’t and they typically were not conventional lawyers.”

Mesereau also thinks civil litigators would be well-served to try something unconventional. He called pre-trial civil litigation “the worst preparation for a trial lawyer imaginable” noting that its practitioners are “nasty and unprofessional and hostile towards each other,” sending “one nasty gram after another. . . .To take all that nasty demeanor and nasty behavior and then drop it all before you walk into the courtroom is not easy, in my opinion.” Instead, he suggests, “if you are humane, decent, compassionate, if you are a real person, using real words, real phrases in a courtroom, you’re better off. And all of that seems to be anathema to civil litigators during their pre-trial work.”

|

| |

Michael Jackson: Keeping Handcuffs Off The Gloved One

In 2004, Michael Jackson was charged with molesting a 13-year old boy whom he had befriended. The alleged incidents, including providing alcohol to the boy, took place at Jackson’s 2,700 acre Neverland Ranch in Santa Barbara County, California. Mesereau represented Jackson. He considered it a death penalty case, as he did not believe that Jackson would survive prison. After a near-five month trial – 140 witnesses -- a jury found Jackson not guilty on all fourteen charges.

Mesereau was strongly warned by close friends not to take the case. He shared with me that he knows of some very prominent lawyers in California who had been approached to represent Jackson and declined. “I was repeatedly told nobody can win the case,” Mesereau said. “He’s been condemned all over the world. It’s being tried in a very conservative location [Santa Maria – the northern part of Santa Barbara County] and they’re going to let in evidence of other prior similar acts. You can’t win it. And I was told, if you lose it, the rest of your life will be defined by that loss. Everywhere you go in the world people will say ‘he sent Michael Jackson to prison.’” But Mesereau signed on: “I decided I am a criminal defense attorney. This is what I do. This is who I am. And I went for it.” |

|

|

|

| |

Mesereau, hearing every reason why he should request a change from such a conservative venue, took the issue into his own hands. He made the three-hour trip north from Los Angeles to Santa Maria. His purpose, he told me, was “to hang out in some bars and restaurants and just see what I could see and feel what I could feel.” The idea worked. Mesereau explained that “invariably people would come up to me and say ‘aren’t you Michael Jackson’s lawyer’ and I would say ‘yes’ and we would start chatting.” Mesereau learned that the residents of Santa Maria liked Jackson and were hoping the allegations were wrong. So, despite that “all these geniuses who appear on television were knocking my choice,” Mesereau said, sarcastically, he did not seek to move the trial out of Santa Maria. As Mesereau is telling me about his reconnaissance trip to Santa Maria I can’t help but think of something he’d said earlier – about great lawyers typically not being conventional lawyers.

Mesereau’s road trip revealed something else very important. While residents in the northern part of Santa Barbara County were indeed quite conservative, they were also quite libertarian. “Their view of government was,” Mesereau explained, “‘we’re good people so government don’t go too far into our lives.’” Mesereau was on to something. The prosecution filed a pre-trial motion to stop him from referring to them as “the government.” The motion was denied and Mesereau would often refer to the prosecutors as “lawyers of the government.”

Unconventionality also played a part in Mesereau’s opening statement in the Jackson trial. He did the unthinkable -- what he calls “heresy.” He did not tell the jury that the prosecution has the burden of proof and that it is one that is beyond a reasonable doubt. Mesereau believes that jurors want to know the truth. To Mesereau, a juror who hears this from a defense attorney thinks “his client is guilty, he just thinks he can stop them from providing it.”

“Walking into the Jackson trial,” Mesereau said, “I fervently believed we had the truth on our side, we had the evidence on our side and we were in the right. And I saw no reason not to flaunt that. . . . I wanted to be the bearer of truth, not them. I did not want to look like someone who was playing with technicalities. Let them look like it.”

The tone in Mesereau’s voice, when discussing Michael Jackson, leaves little doubt that he has very warm feelings for the pop icon, whom he says he got to know “probably in a way that few people do, given the severity of the circumstances.” Despite what you see of Jackson on stage, Mesereau told me “if he was sitting at a table with you and me he would be very shy and awkward.” Hearing a Jackson song on the radio causes Mesereau to think of “what a brilliant artist he was and what a nice, sensitive, kind person he was.”

The Cosby Case

Mesereau has a laid back, easy-going manner. To know how he is feeling is more listening for nuance in his voice than looking at his sleeve. But then I asked him about the Cosby case.

This spring, just outside Philadelphia, Bill Cosby was found guilty of aggravated indecent assault for drugging and sexually assaulting a woman. Mesereau represented Cosby in what was a re-trial of a 2017 case that ended in a hung jury. Mesereau was not involved in the first case.

When asked about the retrial, Mesereau bitterly rattled-off a long list of rulings that he believed were wrong, causing him to call the proceeding “the most unfair trial I have ever been part of.” These ranged from the breach of a prior agreement not to prosecute, the court’s mishandling of a statute of limitations defense, a statement by a juror and in-court outbursts by Cosby accusers that should have led to mistrials, the court allowing five other Cosby accusers to testify, but only one in the first trial, and there are more. [For an in-depth look at Mesereau’s outrage at the Cosby trial, check out You Tube for his interview with private investigator Scott Ross.]

Cosby was scheduled to be sentenced this week. Mesereau no longer represents the 81-year old comedian as he begins the appellate process.

Mesereau Free Legal Clinic

Mesereau began doing pro bono work in the 1980s, donating his time to various legal clinics and public service organizations. Following the Jackson trial, he decided to use his public persona to start the Mesereau Free Legal Clinic, which meets two Saturdays a month at a church in south Los Angeles. It is still going strong. Law students, college students and activists come together to help people with both civil and criminal problems.

“The more I did this kind of work,” Mesereau explained, “the more fulfilled and happier a lawyer I seemed to be.” He invites other lawyers to do the same, especially those who are unfulfilled and unsatisfied in their work: “One way to deal with that is go get involved in pro bono work and don’t be as concerned about greed and money and status and use your great education and skills to make a difference in society. You will be surprised what it does for you, let alone the people you are helping. I always say there are no losers in this process, everybody gains.”

Alabama Getaway

Once a year, for the past two decades, Mesereau’s commitment to pro bono work goes from south Los Angeles to the U.S. South. He works with long-time close friend and Alabama lawyer, Charlie Salvagio, to represent a defendant charged with murder, often times with the death penalty on the table. The scheduling takes some challenges, Mesereau explained, but “we just work it out.”

Last year, in Bessemer, Alabama, the duo secured the high-profile acquittal of Charleston Wells, a 17-year old African American accused of shooting to death Mike Gilotti, a white Iraq War veteran. The year before, the team represented Odell Marzette Allen in Birmingham, accused of murder by shooting the victim three times in the back. Allen was acquitted – based on self-defense.

In 2003, Mesereau and Salvagio handled the re-trial of Wesley Quick, who had previously been found guilty of murder and spent six years on Alabama’s death row. Quick’s retrial was the result of him being denied a free copy of the transcript from his first trial. This time Quick was acquitted, prompting a “Birmingham News” editorial that called the state’s approach to capital cases “slipshod.”

***

Tom Mesereau is well-known for his gray hair. But he doesn’t see it when he looks at the man in the mirror: "Many lawyers want to reach a point where they think they know everything there is to know about what they do and they stop learning. And their attitude is ‘I should be teaching you, not the reverse.’ That to me is a mistake because you never fully master trial practice. You are always a student in my opinion.”

|

| |

[Elizabeth Vandenberg, a 2L at the University of Iowa College of Law, assisted with this article.] |

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Vol. 7 - Issue 7

September 26, 2018

Halloween Candy And Insurance Coverage

|

|

|

|

|

| |

Halloween is here. Well, not really. But you’d never know it from my supermarket. They seem to think that people start buying Halloween candy on Labor Day. Having said that – I am delighted that the green Frankenstein-looking Peeps have been available since the beginning of this month.

Halloween, and, in particular, candy, was at the heart of a recent fascinating underlying and companion coverage case.

On October 31, 2015, Sanford Grigsby, like millions of others, passed out candy to the ghosts and goblins who knocked on his door in suburban Cleveland. But there was something about a stop at Grigsby’s house that differed from most. Grigsby was a dentist. So, in addition to Gobstoppers, his trick or treaters each received a small zip-lock bag containing a toothbrush and travel-size tube of toothpaste. The toothbrush was imprinted with Sanford Grigsby, D.D.S. and his office phone number. Inside the bag was a folded piece of 8 ½ x 11 paper, with Dr. Grigsby’s offer letterhead, and the text: “Happy Halloween! Enjoy your candy and then come see Dr. Sandy!” Grigsby knew it made him look like Scrooge – but he believed in never missing a chance to promote good dental health. Plus, thanks to the overzealous marketing tactics of toothpaste manufacturers, he had 500 travel-size tubes of toothpaste in his office that he was desperate to unload.

Skip McMaster, age 10, and dressed as Harry Potter, knocked on Dr. Grigsby’s door and was handed Gobstoppers and one of Grigsby’s toothbrush/toothpaste bags.

Two days later, Skip’s father, Melvin, ate Skip’s Gobstoppers (with Skip’s permission). Melvin bit down on the candy and cracked two crowns in his mouth. The cost to remake them was $6,000 plus plain and suffering and hours of time out of Melvin’s life to deal with the numerous dentist’s office visits.

Melvin decided to file suit against Dr. Grigsby. It was easy to identify Grigsby as the Gobstopper-ghoul. Skip did not like Gobstoppers and had made a note to himself to avoid Grigsby’s house the following year. And Melvin was willing to testify that Skip had received no other Gobstoppers in his candy bag. Product ID was satisfied.

Melvin had a difficult time finding a lawyer to take the case. Several turned him down on the basis that, as a matter of law, he could not maintain an action against Dr. Grigsby. As these lawyers saw it, Grigsby simply had no liability for the incident. Prepared to give up, Melvin went to see one last lawyer. This time the attorney saw a cause of action – strict liability. As for the law’s requirement that Dr. Grigsby be a manufacturer, retailer or distributor of the product, they would argue that he was a distributor. By including the toothbrush with his name and office phone number, plus the note stating “Enjoy your candy and then come see Dr. Sandy!,” Grigsby was in fact selling Gobstoppers, through a deferred payment scheme -- fees for dental services arising out of Gobstopper-caused cavities.

Melvin McMaster filed suit against Sanford Grigsby, D.D.S. in state court in Cuyahoga County, Ohio. He sought payment of $6,000 for the replacement of the two crowns and damages for pain and suffering.

Grigsby did not have a homeowner’s policy, with liability insurance, as he was renting his house and also did not have a renter’s policy. So Grigsby tendered the McMaster suit to his dental malpractice insurer – Molar Property & Casualty Ins. Co. Molar declined to defend Grigsby on the basis that the policy’s insuring agreement was not satisfied. Specifically, as Molar saw it, the complaint did not allege that McMaster’s injury was caused by Grigsby “arising out of the performance of dental services.”

With nowhere to turn, Grigsby retained a lawyer and filed the Ohio equivalent of a 12(b)(6) motion to dismiss for failure to state a claim. The court, in Melvin McMaster vs. Sanford Grigsby, D.D.S., No. 17-2145 (Cuyahoga Cty. Jan. 3, 2017) acknowledged that McMaster’s cause of action was novel. However, based on the high burden required for granting a 12(b)(6) motion, the court could not say that McMaster had no claim. The court explained: “If all Dr. Grigsby had done was given away toothpaste and a toothbrush, even with his name and office phone number, this court would not hesitate to conclude that Dr. Grigsby was simply a concerned dentist and not a distributor of Gobstoppers for purposes of the state’s strict liability law. But Grigsby went further. This court cannot say, at this preliminary stage, that Dr. Grigsby, having included the note inviting people to see him, after getting a cavity from the Gobstoppers, was not selling the candy, through the deferred payment scheme alleged by plaintiff.” Id. at 3.

Grigsby, now faced with the prospect of the litigation going forward, and a six-figure estimate for defense costs, settled the action for $22,500.

Grigsby, now spitting mad, filed suit against Molar P&C, seeing recovery of his $9,000 in defense costs, the $22,500 settlement and damages for bad faith. Molar filed a motion for summary judgment, arguing that McMaster’s injury was not caused by Grigsby “arising out of the performance of dental services.” Grigsby cross-moved.

Brace yourself. The court, in Grigsby v. Molar Property & Casualty Ins. Co., No. 18-1387 (Cuyahoga Cty. Sept. 5, 2018) held that McMaster’s injury was caused by Grigsby “arising out of the performance of dental services.” The court explained: “By giving out a toothbrush and toothpaste to the trick or treaters, Dr. Grigsby was acknowledging that eating candy can be hazardous to a child’s teeth. He was promoting good dental hygiene to address the risk. Based on the broad meaning given to the term ‘arising out of’ as used in insurance policies, and this court’s mandate to interpret a coverage grant broadly, this court holds that Mr. McMaster’s injury was arising out of the performance of Dr. Grigsby’s dental services.”

Scary decision.

The molar of the story: It’s safer to give out Peeps.. |

That’s my time. I’m Randy Spencer. Contact Randy Spencer at

Randy.Spencer@coverageopinions.info |

|

| |

|

| |

|

|

|

|

Vol. 7 - Issue 7

September 26, 2018

Video Webinar With Restatement Drafter Tom Baker [And Maniloff]

Significant Discount For Coverage Opinions Readers

|

|

|

|

|

|

| |

It is no secret that insurers have been critical of the recently approved ALI Restatement of the Law, Liability Insurance. Some of these criticisms are more serious than others.

I believe that there are four aspects of the new Insurance Restatement that are potential landmines that are lurking out there for insurers. These are issues that, if they take hold, could have a real impact on how claims need to be handled. They would provide opportunities for policyholders to advance their interests in coverage litigation. Interestingly, while many aspects of the Insurance Restatement have been criticized by insurers, these four potential landmines went largely undiscussed in the many articles written about the subject over the past few years.

I am pleased to have the opportunity to discuss the ALI’s Insurance Restatement with Tom Baker, Penn Law Professor and one of the principal drafters of the Restatement, as part of a (video) webinar being offered by the American Law Institute itself.

I hope you will join Professor Baker and me on October 24th to get our take on which aspects of the much-debated Restatement are most likely to influence courts, in which jurisdictions it is most likely to be relevant and how it can be used by policyholders and insurers. And I’ll discuss these potential landmines that may be lurking out there.

Don’t miss this great opportunity to learn about the Insurance Restatement from the man at the center of the debate for the past 8 years.

I have arranged a 40% discount on the cost of the webinar for Coverage Opinions readers.

Use Promo Code VC1024CO.

This webinar provides 1.5 CLE credits (including 30 minutes for ethics; check your state at the link below).

For more information about this webinar and to register, please visit the ALI's site: https://www.ali-cle.org/course/VCAH1024P

Randy

|

| |

|

| |

|

|

|

| |

|

| |

Vol. 7 - Issue 7

September 26, 2018

Insurance Key Issues: This Is What Makes The Book Unique |

|

|

|

| |

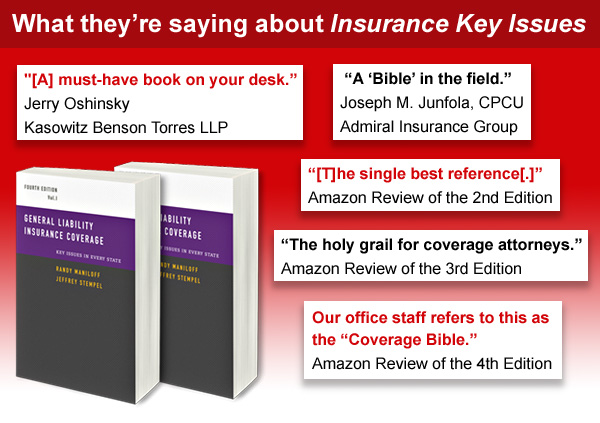

Fifty-state surveys of liability coverage issues are not unique. But there are two things that make them unique in General Liability Insurance Coverage: Key Issues In Every State.

• All of the 50-state surveys – which are extremely current -- are conveniently available in one location.

• At nearly 1,000 pages covering 20 issues, the extent of detail and case law is far more extensive than many 50-state surveys. There is often enough information to provide one-stop shopping to answer your question. If not, you’ll know exactly where to begin your additional research.

Check out these sample pages to see what I mean:

http://insurancekeyissues.com/SamplePages.pdf

The Insurance Key Issues Promise: If you like Coverage Opinions, rest assured that the same effort has gone into Key Issues for the past ten years.

Visit the Insurance Key Issues website: |

| |

|

| |

|

| |

| |

|

|

|

|

Vol. 7 - Issue 7

September 26, 2018

Encore: Declarations:

September 30, 2015

|

|

|

|

|

|

| |

Arizona Governor Doug Ducey recently appointed former Arizona Senator Jon Kyl to fill Senator John McCain’s seat until a special election is held in 2020 (although Kyl has not committed to serving past the end of this session). I had the privilege of interviewing Senator Kyl for the September 30, 2015 issue of Coverage Opinions. We discussed his long career, from insurance defense layer to Senate Minority Whip to attorney at Covington & Burling.

I told the man, once named by Time Magazine as one of the 100 most influential people on the planet, a political joke. He laughed really hard – and then started to suggest ways to change it. I was like – uh, this isn’t how it works. But Kyl must have thought he was back on the Senate floor and was offering an amendment.

Check out my interview with former, and now once-again, Arizona Senator Jon Kyl:

http://www.coverageopinions.info/Vol4Issue9/Declarations.html

|

| |

|

| |

|

|

|

|

Vol. 7 - Issue 7

September 26, 2018

Encore: Tom Brady Speaks To Randy Spencer About Deflate-Gate

|

|

|

|

|

| |

|

| |

For the past two weeks or so talk in the sports world has been dominated by one story – Deflate-gate. For the six people in America who do not know what this is, the New England Patriots were accused of using footballs, during the 2015 AFC Championship Game, that contained less air pressure than mandated by the National Football League rules. A softer football may be easier to grip and throw. The Patriots and its quarterback, Tom Brady, denied any wrongdoing.

Deflate-gate dialogue began on May 6th following the release of the “Investigative Report Concerning Footballs Used During The AFC Championship Game On January 18, 2015.” That’s the 243 page report, prepared by the NFL’s lawyer, Ted Wells, of his investigation to get to the bottom on the Deflate-gate story.

This report, now referred to as the Wells Report, reached, among others, the following conclusions: (1) It is more probable than not that Patriots locker room personnel – Jim McNally and John Jastremski -- participated in a deliberate effort to release air from Patriots game balls after the balls were tested by game officials; and (2) It is more probable than not that Tom Brady was at least generally aware of the inappropriate activities of the locker room personnel involving the release of air from Patriots game balls.

Then, just when the Wells Report was retreating from the front page, on May 11th the NFL announced the imposition of harsh penalties on the Patriots and Brady for their conduct. Brady was suspended for the first four games of next season without pay. The Patriots must forfeit their first round draft pick next year and a fourth round pick in 2017. The Pats were also fined $1 million. Of course, they’ll save a couple of million on Brady’s salary, so the team actually comes out ahead on the deal. How did the NFL not see that? In any event, with all this, Deflate-gate was back on the front page.

But despite the incredible noise that Deflate-gate has generated, Tom Brady has been virtually mum on the conclusions of the Wells Report and the sanctions imposed by the NFL. Until now. Brady has chosen to break his silence -- with an exclusive sit down interview with Randy Spencer.

Brady and I are seated at a back table in a small French bistro in Boston’s Beacon Hill neighborhood. It’s too late for lunch and too early for dinner so the place is empty. A young woman approaches – probably a college student. She shows no sign of recognizing the city’s most famous resident. Brady asks her what brands of water she has. She rattles off a few names. Unsatisfied with his choices Brady settles on an iced coffee. I was planning on ordering a Diet Coke. But that now seems out of the question so I also order an iced coffee – even though I really dislike it.

Randy Spencer: Tom, thank you for choosing Coverage Opinions and the Randy Spencer’s Open Mic column to discuss the Deflate-gate situation. I’m sure that media outlets have been relentless in pursuing you for an interview.

Tom Brady: No problem Andy.

RS: That’s Randy

TB: Right. Yeah, you can’t imagine. ESPN’s drool could end the California drought. And that Matt Louder guy hasn’t stopped calling.

RS: That’s Lauer.

TB: Whatever. I’ve never heard of him. They tell me his show starts at 7 in the morning. Is anyone up that early? [It is clear from Brady’s tone that his question is a serious one.]

RS: Tom, let’s get right to it. You’ve been criticized for not turning over your cell phone to the NFL’s investigators. And the NFL stated that that played a part in its decision to impose a four game suspension. If you had nothing to do with the deflation of footballs, why didn’t you just turn over your phone?

TB: Look man, I’m Tom Brady. One of the greatest QBs ever to lace ‘em up. I’m cooler than the Fonz on his best day. I’m cooler than that Dos Equis guy. I’m so cool I can get away with endorsing Uggs. Plus I got movie star good looks. I’m the Super Bowl MVP. And I’m married to Gisele Bündchen, a super model. And not just any super model – a Brazilian one. She’s even got two dots over one of the letters in her name.

RS: You’re all those things Tom.

TB: Yeah, well, that’s exactly why I couldn’t turn over my cell phone. I couldn’t let people see how many emojis I use when sending text messages. [Brady holds out his phone to show it to me.] You see those two little sunny side up eggs in frying pans? I sent Gisele a text this morning with those pictures, and just from that, she knew that I wanted two eggs for breakfast. And if I’d wanted three eggs I would have just sent her three of those little frying pans. Man, it’s amazing. And if I wanted toast and coffee....

RS: Wow! I never figured Tom Brady as an emoji guy.

TB: I know. Nobody would. You hear emojis and you think Tim Tebow. Not Tom Brady. That’s why I needed to keep my cell out of Wells’s hands.

RS: But that decision cost you four games without pay.

TB: Totally worth it.

RS: Yeah, I can see that. Speaking of the four game suspension, what do you plan on doing to keep busy during those weeks?

TB: [Brady lets out a sigh of exasperation] Don’t ask. Gisele’s got me painting the powder room and cleaning out the garage. She says it’s time for me to throw out my Tom Brady poster collection. If I’m lucky I’ll pull a hammie the first week and get Gisele off my back.

RS: Let’s talk about the Wells Report. It’s the size of a book. Did you read all 243 pages?

TB: I didn’t know they made 243 page books.

RS: The Wells Report concluded that it is more probable than not that you were at least generally aware of the inappropriate activities of McNally and Jastremski involving the release of air from Patriots game balls. Is that true?

TB: Yeah, that’s what the report says.

RS: No, I mean, is it true that you were generally aware of what McNally and Jastremski were doing?

TB: No way. “Generally aware.” “More probable than not.” Who talks like that? Not normal people. If they had the goods on me they’d say so in English. We’re talking about deflating footballs with tons of people around. How hard can that be to prove? This isn’t exactly who killed JFK?

RS: But what do you say about the scientific experiments that concluded that the psi measurements of the Patriots game balls at halftime cannot be entirely explained by the Ideal Gas Law?

TB: Go ask Marvin Greenbaum.

RS: Who’s Marvin Greenbaum?

TB: He’s the guy whose paper I copied off of in high school chemistry.

[The waitress approaches with the drinks. Someone has now tipped her off to who’s sitting at the table. Aren’t you Randy Spencer?, she asks. I acknowledge that I am. She’s asks if we can take a selfie. Of course I oblige.]

RS: Tom, how do you explain the mountain of circumstantial evidence laid out in the Wells Report that McNally and Jastremski were involved in deflating game balls and you were generally aware of it.

TB: Look, the Patriots put together a website that responds to all the conclusions in the Wells Report. Check it out. It’s all in there. It says [Brady makes double quotation mark symbols with his fingers]: “There is no evidence that Tom Brady preferred footballs that were lower than 12.5 psi and no evidence anyone even thought that he did.” I knew nothing. That’s how normal people speak. That’s not weasel lawyer language.

RS: But some of the stuff on that Patriots website is hard to believe. It says that the term “deflator” used between McNally and Jastremski was a reference to McNally wanting to lose weight. Do you really believe that?

TB: If that’s what the Pats’s lawyers say then I believe it. If Bob [Kraft – Patriots owner] tells the lawyers to write a report saying that the earth is flat, then the earth is flat. We have really good lawyers.

RS: The Wells Report says that McNally took the game balls into the bathroom for a minute and forty seconds and that’s when he supposedly deflated them. The said it can be done in that amount of time.

TB: I know. But McNally says he was in there peeing. And that can be done in a minute forty. And if that’s what he says I believe him. Jimmy’s just not gettin’ a fair shake.

RS: You’ve appealed your suspension and it will be heard by Commissioner Roger Goodell. Are you OK with that?

TB: Yeah, that’s cool. Rog and I get along fine and I think he’ll be fair. Besides, I was his wingman one night when we went out during Super Bowl week. Trust me. He owes me.

[Brady’s cell phone rings. He answers it. “Right.” “Ok.” “Yes.” “I’ll get them.” He hangs up and looks at me. “Gisele. She wants me to bring home a quart of milk and a Mercedes.”]

RS: Why do you think that the public is so fascinated by Deflate-gate?

TB: Because it’s about Tom Brady, man. Tony Romo could throw footballs as flat as Frisbees and it would get less coverage on the sports page than a cricket match.

RS: You must know that people are less likely to believe the Patriots’s story because of Spygate.

TB: Look, that was all Belichick’s thing. I have no idea what he was doing. What a dumb idea. I didn’t need to be Dick Tracy to beat the Jets.

RS: What’s it like being coached by Bill Belichick?

TB: Don’t get me started. The NFL is crawling all over me about some slightly deflated footballs and Belichick is the one they should be investigating and writing reports about. Do you know why he cuts the sleeves off his hoodies? To sell them on Ebay. Hey Rog, you think that’s in the best interest of the game?

RS: It was reported that you went to the Kentucky Derby a few weeks back and then jetted to Vegas for the Pacquiao—Mayweather fight later that night. How was the fight?

TB: What a bust! You wanna talk about real deflation?

RS: Tom, do you think that Deflate-gate will hurt your legacy?

TB: The only thing about Deflate-gate that might hurt my legacy is that I did an interview about it with a stand-up comic who writes a column for an insurance law newsletter. [Brady smiles to let me know he’s kidding. At least I think he’s kidding.]

RS: Tom, thanks for speaking with me. I appreciate it.

TB: No problem, Andy.

[Brady pulls out his cell phone and sends a quick text. He holds it out for me to see. It’s a picture of two hour glasses.]

I just asked Gisele to make me two soft boiled eggs.

|

That’s my time. I’m Randy Spencer. Contact Randy Spencer at

Randy.Spencer@coverageopinions.info |

|

| |

|

| |

|

|

|

|

Vol. 7 - Issue 7

September 26, 2018

The Wall Street Journal Looks At Various New Insurance Products

|

|

|

|

Curiously, The Wall Street Journal has recently had three separate articles looking at new products being offered by the insurance industry to address emerging risks. The insurance industry has long been adept at designing products to spread the risk of burgeoning exposures. For convenience, I set out below some quotes from the stories that address key aspects of the policies.

“More Schools Are Buying ‘Active Shooter’ Insurance Policies” (Tawnell Hobbs; August 2, 2018)

“Insurance underwriter McGowan Program Administrators, an Ohio-based leader in shooter insurance, has written over 300 active-shooter/workplace violence policies for school districts, charter schools, private schools and universities across the country since 2016, when it started offering the coverage. A company official said the company issued over 60 policies in July, and that it has paid out some policies. Shooter insurance is considered gap coverage, handling expenses not typically covered under general liability, such as funeral costs and death benefits. Annual premiums can range from about $1,800 for $1 million in coverage for small school systems to about $175,000 for $20 million in coverage for larger ones. Death benefits often are offered up to $250,000 per victim.”

“To set premiums, insurers consider factors including local crime data, student enrollment and district staff levels. They also consider what safety measures the schools have in place, says Paul Marshall, managing director for McGowan’s Active Shooter/Workplace Violence Insurance Program. He also considers whether schools are monitoring social media to spot potential threats and if schools offer active-shooter awareness training to students and staff.”

“Demand For Tuition Insurance Is Surging” (Douglas Belkin; August 20, 2018)

“Liberty Mutual Insurance started offering tuition-reimbursement policies this year, in part because of consumer demand. When a student drops out mid-semester parents are often ‘very surprised to learn that you may not get anything back,’ said Michele Chevalier, a senior director at Liberty Mutual.”

“Tuition insurance protects families in case their son or daughter has to drop out of school past the point at which a school offers tuition reimbursement, usually around halfway through the semester. Driving the increased demand are higher college costs and, to a lesser extent, rising mental-health disorders among college students that have raised concerns among parents that their children may struggle away from home.” [The plans generally do not cover dropping out for academic or disciplinary reasons.]

“Big Cities Insure Against Cyber Attacks” (Scott Calvert and Jon Kamp; September 7, 2018)

[There is nothing new about cyber insurance; but here is a look at a new trend in the customer base.]

“A majority of the 25 most-populous U.S. cities now have cyber insurance or are looking into buying it, according to a Wall Street Journal survey. A ransomware attack on Atlanta earlier this year—one of the biggest reported breaches of a city’s network—served as a warning to officials everywhere of the constant barrage from hackers. Cities and even library systems are being hacked more often than people realize, but many heard about Atlanta.”

“‘Compromise is inevitable,’ said Christopher Mitchell, chief information security official, at a Houston City Council hearing last month. His presentation helped persuade local lawmakers they needed a $30 million cybersecurity insurance plan with a $471,400 premium, an example of a burgeoning trend across the country. Policies vary, but insurance can cover hackers’ extortion demands, legal liabilities, computer-forensics expertise and costs for problems like having government services knocked off line.”

“‘I wanted A to Z to have it covered,’ said Mark Barta, risk management director in Fort Worth, Texas, which got a $5 million cyberpolicy with a $99,570 premium last year. ‘I didn’t want to be in a situation on a Monday morning hearing this happened, and saying, What do I do next?’”

|

|

|

|

|

|

| |

|

Vol. 7 - Issue 7

September 26, 2018

Mind The Gap: Excess Insurer Obligated To Drop Down Despite No Primary Exhaustion

|

|

|

|

I don’t often address cases in Coverage Opinions concerning the relationship between a primary and excess insurer. Frequently driven by their unique facts and policy language, they can be, at best, a Gala to Red Delicious comparison. At worst -- apples to washing machines. As a result, they do not offer takeaways that can be applied to other situations.

But Hunter v. AIG Property Casualty Co., No. 17-81020 (S.D. Fla. July 20, 2018) is a primary-excess case that I believe is suitable for discussion here as it offers a lesson to be learned. It involves coverage arising out of the following circumstances. In July 2012, Kara Walker was injured when she was struck by a firework caused by Kenneth Hunter’s alleged negligence. [The case does not address how this happened.]

Hunter was an insured under two policies. He had a homeowner’s policy with Tower Hill Insurance that was subject to a $100,000 liability limit. He was also insured under a group personal excess liability policy, issued by an AIG predecessor, to his employer. The policy’s limits were excess of $300,000 up to $5,000,000. You can see where this is going.

In January 2013, Tower Hill paid its $100,000 limit and negotiated a limited release for Hunter. In June 2016, Ms. Walker sued Mr. Hunter for negligence. AIG retained counsel, John Lurvey, to represent Hunter and instructed Mr. Lurvey to settle the action.

Hunter advised Lurvey that he did not agree to settling the claim. He made clear that he wanted to go to trial and requested that both he and his personal attorney be included in any settlement discussions. In May 2017, Hunter was informed that AIG settled the action for $750,000. Hunter and his personal counsel were not involved in the settlement. Hunter never consented to or signed any settlement agreement.

Next AIG demanded that Hunter reimburse it $200,000, representing the gap in coverage between Tower Hill’s $100,000 limit and the required $300,000 in required underlying limits under the AIG Policy. Hunter refused and filed the action seeking a determination that he is not legally obligated to reimburse AIG.

The court held that Hunter was not obligated to reimburse AIG. In doing so it set out a lot of policy language from the AIG policy. I’ll discuss what was critical in the context of the court’s decision.

First, the court noted that, pursuant to numerous aspects of the policy, AIG was liable only for amounts in excess of the required underlying limits of $300,000. The court also cited to several policy provisions making clear that Hunter “was required to maintain a minimum of $300,000 in underlying homeowners personal liability insurance or else run the risk of no excess coverage.” Reading all of this together, the court stated that “the intention is clear. Hunter was required to maintain $300,000 in underlying primary insurance limits or else forfeit his right to excess coverage under the [AIG] Policy.”

Clearly Hunter had not done so. Yet the court still held that Hunter was not obligated to reimburse AIG.

The court’s decision was tied to the language of the AIG Policy that addressed defense. Under the policy, AIG had a “duty” to defend and a “right” to defend: “The [AIG] Policy includes two distinctly different provisions regarding AIG’s duty to defend versus AIG’s right to defend. The first provision gave AIG the ‘right and duty to defend’ only once the underlying $300,000 limits were exhausted, whereas the second provision gave AIG ‘the right and...opportunity’ to participate in the defense of any claim ‘in all other instances’ which may create liability for AIG.”

With this distinction firmly in mind, the court held that “AIG had the right, but not the duty, to participate in Hunter’s defense in the state court lawsuit given that the underlying $300,000 limit was not yet exhausted. When the state court lawsuit began, $100,000 of the applicable $300,000 limit had already been paid out by Hunter’s only primary insurer to Ms. Walker. A fact AIG well knew. And while AIG may have had the right to then participate in and settle the state court lawsuit as AIG deemed expedient to protect its own interests under the [AIG] Policy, AIG does not now have the right to seek reimbursement from Hunter for a settlement that Hunter vociferously refused to take part in. (several citations and parentheticals omitted). Such an outcome would run contrary to the plain, ordinary, and proper reading of the [AIG] Policy. AIG, which acted to orchestrate the settlement with Ms. Walker without Hunter’s consent, plainly did not have the authority to bind Hunter. In the absence of such authority, Hunter never became obligated to pay the $200,000 gap in coverage. Thus, AIG is not entitled to the reimbursement it seeks.”

While primary-excess cases are frequently driven by their unique facts and policy language, this one involves policy language that is seemingly not unusual: numerous aspects of the excess policy state that the insurer is only liable for amounts in excess of the required underlying limits; several policy provisions state that the insured is required to maintain a certain minimum underlying limit; and the excess insurer’s “right and duty to defend” kicks-in only after the underlying limits are exhausted, as opposed to “the right and...opportunity” to participate in the defense in all other instances which may create liability for the insurer.

Thus, the decision offers a takeaway, for excess insurers, confronted with the opportunity to settle a case – and thereby limit its own exposure – but in the face of a known gap in underlying limits.

|

|

|

|

|

|

|

Vol. 7 - Issue 7

September 26, 2018

Another “Montrose Endorsement” Loss For An Insurer

|

|

|

|

I’ve been saying this for a while. In general, insurers have had mixed results in construction defect cases when it comes to enforcing the Montrose (known loss) endorsement. Some courts have interpreted them narrowly and applied a strict “sameness” test (my term) between the “property damage” that existed pre-policy inception date and that which took place during the policy period, for which coverage was being sought. Further, it is the “property damage” itself that must be known by the insured prior to the policy period and not the cause of the “property damage.” You could put it this way – if it looks like a mallard duck, and quacks like a mallard duck, it’s only a mallard duck and not a perching duck.

Based on some recent decisions (discussed in Coverage Opinions), and now Anderson v. Nationwide Mutual Ins. Co., No. 12-1057 (E.D. Calif. Sept. 7, 2018), it seems that courts are trending toward applying a strict “sameness” test. [Of course, construction defect cases are not what ISO had in mind when it put pen to paper on the Montrose endorsement.]

Anderson is a somewhat lengthy and complex case. I’ll limit the discussion here to just enough needed to make the point about application of the strict sameness test.

At issue in Anderson was the availability of coverage for an insured for construction defects that it caused. [The facts are not set out in a simple manner.] The key date at issue is April 10, 2007. This is when a Century Surety policy went into effect. The key policy provisions were described by the court as follows:

“The policies provided coverage for property damage which occurred during the policy period. The policies also defined an ‘occurrence’ to mean an accident, and stated that all property damage arising out of such an accident or series of related accidents was ‘deemed’ to have taken place at the time of the first such property damage, even if the nature and extent of the damage changed; and even if the damage was continuous, progressive, cumulative, changing or evolving. Additionally, the policies provided that there was no coverage for property damage which was known to the insured prior to the inception of the policy. Stated otherwise, the policies provided coverage only for new and different damage caused by new and different occurrences which occurred for the first time during the Century policy periods (in other words, after April 10, 2007).”

This is not exactly “Montrose Endorsement” language (at least what’s shown), but it is close and akin to it.

The court held, a least for duty to defend purposes (which included the consideration of extrinsic evidence), that the insurer could not deny coverage on the basis that “all of the damage was (a) caused by events that occurred prior to April 10, 2007, or (b) was of the same nature or extent as the damage that had occurred prior to April 10, 2007.”

The issue is highly fact intensive. Thus, I’ll cite liberally here from the opinion to best demonstrate the court’s application of a strict sameness test:

“Mr. Lohse [insured’s expert] also testified that this new and different damage was caused by new and different occurrences for the first time after April 10, 2007: ‘The causes we saw in 2008 were different from the prior drainage causes.’ The causes prior to 2008 were ‘partially because the park was still being developed . . . so that means you have a lot of construction debris’ and partially from ‘drainage design problems that were corrected before 2008’ or ‘poor design.’ In contrast, the new and different damage which occurred for the first time during Century’s policy period was caused by ‘the failure to maintain the drainage system so the water would freely flow into the retention pond’ and ‘because the drainage wasn’t maintained, kept free of debris.’ ***

Thus, the foregoing exhibits and testimony constitute evidence that the occurrences which pre-dated the Century policies were caused by improper design of the drainage system, while the occurrences after the inception of the Century Surety Company policies were caused by the negligence of the insured in failing to properly maintain off-site drainage, and not the same design issues which had been corrected prior thereto. These occurrences are plainly not ‘exposure to substantially the same general harmful conditions.’ They are patently different harmful conditions.

In other words, substantial evidence demonstrated new and different occurrences that happened for the first time within the Century policy period. Substantial evidence also demonstrated new and different harm as a result thereof.”

Lastly, and significantly, the court went on to hold that the insurer could be liable for a stipulated judgment – in excess of the policy limits.

|

|

|

|

|

|

|

Vol. 7 - Issue 7

September 26, 2018

Marijuana Deal Goes To Pot: Leads To Interesting “Wrongful Eviction” Coverage Case

|

|

|

|

The increase of legalized marijuana over the past few years has led to several decisions addressing coverage arising out of its use. [See below: If Your Coverage Was Coppertone: Coverage Opinions In August: What You May Have Missed – “Policyholders Will Shout Doobious Decision: Marijuana Coverage And An Issue I’ve Never Seen Before”]

A marijuana-related real estate deal gone bad landed a coverage case in a California federal court’s lap. Black Mountain Center v. Fidelity & Deposit Co., No. 17-1776 (S.D. Calif. July 26, 2018) involved coverage arising under the following circumstances.

Black Mountain Center owned the Haidinger Center in San Diego and leased commercial space to Victoria DuPont and Jeff Droege to operate a medical marijuana dispensary – and no other purpose. The parties agreed that the tenants could operate the marijuana dispensary upon receipt of a Conditional Use Permit (CUP). In November 2014, the tenants obtained a tentative CUP. However, it contained onerous requirements that neither party anticipated. For example, the need for Haidinger to have armed guards on the property. In addition, Haidinger was unable to obtain insurance for the complex because of the existence of a medical marijuana dispensary.

Haidinger believed that the CUP conditions materially altered the deal and concluded that it could not go forward with the project nor consent to the CUP conditions.

The San Diego Planning Commission eventually approved the CUP. However, Haidinger refused to sign it and notified the tenants that it was terminating the lease.

Not surprisingly, the tenants did not take this sitting down. Following certain demands, the tenants filed suit against Black Mountain Center, alleging that Plaintiffs denied Tenants’ quiet enjoyment of the property and breached the lease when Haidinger failed to sign the CUP. Tenants sought damages in the amount of $3,200,000.

Fidelity, Black Mountain’s insurer, denied liability coverage. Litigation ensued. The principal issue was whether coverage was owed under the “personal and advertising injury” section of the policy. Specifically, “Personal Injury means injury other than bodily injury arising out of one or more of the following acts: c. wrongful entry into premises that a person or organization occupies or wrongful eviction of a person or organization from premises that the person or organization occupies.”

The court held that, at least for duty to defend purposes, there was a wrongful eviction that satisfied the definition of “personal and advertising injury.”

The principle, at the heart of the decision, was that, under California law, a wrongful eviction extends to both actual and constructive evictions. The court also rejected the argument that “wrongful eviction” should be narrowly construed and limited to situations in which the landlord expels the tenant though the legal process.

With these principles in place, the court seemed to have little problem concluding that the “wrongful eviction” requirement had been satisfied.

“Plaintiffs assert that the record establishes that Tenants set forth sufficient facts and allegations to give rise to a constructive eviction which occurs when the landlord engages in acts that render the premises unfit for occupancy for the purpose for which it was leased, or deprive the tenant of the beneficial enjoyment of the premises.”

The court agreed: “Haidinger represented that he would execute the preliminary CUP, a prerequisite for obtaining the final CUP; Haidinger refused to sign the CUP; Tenants were unable to operate the premises as a medical marijuana dispensary; and Tenants incurred substantial expenses in reliance upon the aforementioned representations. . . . The above facts strongly suggest a constructive eviction claim potentially covered by the policy [duty to defend].”

Lesson for insurers: Take care when your insureds are leasing a joint to be used for a marijuana dispensary.

|

|

|

|

|

|

|

Vol. 7 - Issue 7

September 26, 2018

The Rarely Discussed Provision In The CGL Insuring Agreement

|

|

|

|

In Foremost Signature Ins. Co. v. Silverboys, No. 17-20581 (S.D. Fla. Sept. 11, 2018), the federal court addressed coverage for defective construction of a home. With one exception, Silverboys resembles most construction defect coverage cases. The court addressed whether the CGL Insuring Agreement was satisfied, namely, was there “property damage” caused by an “occurrence,” with the court making a distinction between an insured’s own defective work and damage to other property caused by an insured’s own defective work. There was also the question whether there was “property damage” on a loss of use basis. Northing to see here folks. Move along.

But there is. In addition to the widely popular “property damage” and “occurrence” issues, the court also addressed a part of the Insuring Agreement that nobody ever pays attention to – the “coverage territory” requirement. Namely, any occurrence must take place in the “coverage territory.” It is the green and black Jujyfruits of the CGL Insuring Agreement.

Here’s why it mattered. The home at issue was in the Bahamas. The insurer argued that the policy’s “coverage territory” requirement was not satisfied. It provided in relevant part – just as in the standard ISO commercial general liability policy – that the coverage territory includes “[t]he United States of America . . . or [a]ll parts of the world if . . . the . . . damage arises out of . . . [g]oods or products made or sold by you in the [United States]; or . . . [t]he activities of a person whose home is in the [United States], but is away for a short time on your business.”

The insurer argued that the “coverage territory” requirement was not satisfied because any alleged property damage was caused by an occurrence that took place in the Bahamas, which is outside of the coverage territory. The counter-argument was that “the alleged negligent conduct that caused the damage occurred in the coverage territory since Designer [the insured] failed to supervise Whittingham [the architect], made billing mistakes, and drafted the designs in Miami.”

The court did not struggle to conclude that the “coverage territory” requirement was not satisfied. It borrowed from Florida’s number of occurrences case law, as discussed in the Northern District of Florida’s 2015 decision in Auto-Owners Ins. v. Globe International: “There, the underlying complaint alleged that the insured was negligent in failing to perform background checks on employees who sexually abused children at a home in Haiti. The bulk of the alleged negligent hiring/supervision occurred at the insured’s offices in Pensacola, Florida. The damage — in that case bodily injury—occurred in Haiti. The policy’s coverage territory was identical to the one in this action. The court, relying on the ‘cause theory’ set forth by the Florida Supreme Court in Koikos v. Travelers Insurance Co., held that when the insured is being sued for negligence, an occurrence ‘is defined by the immediate injury-producing act and not by the underlying tortious omission.’ As a result, the court held that the occurrence that caused the injury was not the insured’s negligence in Florida, but rather, the sexual abuse in Haiti. . . . The location of the alleged property damage in this action is in the Bahamas, outside of the coverage territory.”

Thanks to a case involving the Bahamas, the “coverage territory” requirement had a day in the sun.

|

|

|

|

|

|

|

Vol. 7 - Issue 7

September 26, 2018

Interesting Look At The CGL Policy’s Definition of “Privacy”

|

|

|

|

Over the past several years there have been oodles of decisions addressing the meaning of right to privacy as used in the commercial general liability policy’s definition of “personal and advertising injury.” Many have arisen in the context of coverage for violations of the Telephone Consumer Protection Act, also known as junk faxes. The decisions have generally gone in two directions. In some cases, no coverage was owed because “privacy” means the right to secrecy -- to keep private facts private. And junk faxes don’t reveal private facts. Other courts found coverage to exist on the basis that privacy relates to a person’s right of seclusion -- to be left alone. And junk faxes interfere with that.

An Illinois federal court recently addressed the availability of coverage for an alleged violation of the right to privacy. The case did not involve junk faxes. But, since the relevant law provided coverage for junk faxes, an attempt was made by the insured to make the issue akin.

Before the court in NuWave, LLC v. Cincinnati Specialty Underwriters, No. 16-4504 (N.D. Ill. Sept. 5, 2018) was coverage for NuWave, for a suit filed against it by the West Virginia Attorney General, alleging that the company engaged in a variety of illegal telemarketing practices concerning the sale of its products. Most notably, it was alleged that NuWave used tactics to keep customers on the phone longer, to subject them to sales presentations.

NuWave sought coverage from Cincinnati, under CGL policies, on the basis that the West Virginia AG’s suit alleged “personal and advertising injury,” specifically, for injury arising out of “oral or written publication, in any manner, of material that violates a person’s right to privacy.” Cincinnati disclaimed coverage. NuWave filed a coverage action. The parties filed motions for summary judgment.

The court posed the issue this way: “Whether the consumer’s right to privacy could possibly include the right to be free from prolonged phone calls.”

NuWave argued that it did, pointing to the Illinois Supreme Court’s 2006 decision in Valley Forge Insurance Company v. Swiderski Electronics. Here, the Illinois high court held that coverage was owed, for sending junk faxes, on the basis that the right to privacy included the right to seclusion. NuWave attempted to extend Swiderski: “According to NuWave, this holding can be extrapolated to also find that, in a situation where the insured prolonged a phone call that the consumer voluntarily and intentionally made to the insured, the insured violated the consumer’s right to privacy. NuWave characterizes the Valley Forge holding as extending the right to privacy in this context to include the ‘right to be free from nuisance.’” However, the court was not convinced that, despite a couple of uses of the term “nuisance” in the Swiderski opinion, it was equating privacy and nuisance.

Instead, the court addressed the issue under the two generally accepted possible meanings of privacy – intrusion upon seclusion or disclosure of private facts -- and held that neither were caused by NuWave’s telemarketers. Simply put, as the court saw it, “[k]eeping a consumer on the phone longer than he wants to be, after he voluntarily and intentionally called, does not match the type of situation that qualifies as an intrusion on seclusion.”

Query: Would the outcome have been the same if the issue were your mother-in-law keeping you on the phone longer than you wanted?

On one hand, NuWave involves unique circumstances. So the decision could be seen as interesting, but with little chance of impacting future cases. Or perhaps not. Junk fax coverage litigation has led to two possible meanings of privacy. Broadly speaking, NuWave teaches that, going beyond the junk fax context, is not a basis to go beyond these established definitions.

|

|

|

|

|

|

|

Vol. 7 - Issue 7

September 26, 2018

Continuous Trigger For Construction Defects: This Is How Broad It Can Be

|

|

|

|

There is something funny about California when it comes to coverage for construction defects. Not funny ha-ha, but funny strange. Despite the prevalence of construction defect litigation in the Golden State, California courts have generally not approached the coverage issues in the traditional manner. More specifically, most states that address coverage, for construction defects, start with the fundamental question – does an insured’s faulty workmanship qualify as an “occurrence?” The answer to that question then sets the stage for addressing the possible application of various exclusions and determining which particular property damage may be covered.

But California courts have generally approached the topic in a more principled, and less policy language-centric, manner. In other words, the courts address coverage for construction defects with no mention of the “occurrence issue.” This is sometimes done with a citation to the 1990 California Court of Appeal’s seminal decision in Maryland Casualty Co. v. Reeder, which explained that “liability policies . . . are not designed to provide contractors and developers with coverage against claims their work is inferior or defective. The risk of replacing and repairing defective materials or poor workmanship has generally been considered a commercial risk which is not passed on to the liability insurer. Rather liability coverage comes into play when the insured’s defective materials or work cause injury to property other than the insured’s own work or products.” But, quite recently, see Global Modular, Inc. v. Kadena Pacific, Inc., 15 Cal. App. 5th 127 (2017) (calling it a decision that rejected an invitation “to ignore policy language in favor of a general principle against insuring against ‘business risks’”).

Not long ago a California federal court took up construction defect coverage in First Mercury Ins. Co. v. Kinsale Insurance Co., No. 18-71 (N.D. Cal. Aug. 21. 2017). At issue was coverage for contractors, for construction defects associated with the renovation of a large residence in San Francisco. The alleged defects included “a black, viscous substance oozing from various window and door assemblies,” as well as oxidation (rusting) and discoloration of stucco and the paint that had been applied to the stucco.

The court addressed some of the issues you would expect to see in a case of this type, such as the “your work” exclusion and determining covered vs. uncovered damages. It did so with a nod to Reeder, no mention of the “occurrence issue” and a quick pivot to the possible application of exclusions.

I’ll skip the discussion of these California issues. Those who swim in this pond can check them out. The issue addressed here, which may offer lessons wider than simply California, is how the court resolved trigger of coverage.

One of the insurers, First Mercury, sought a determination that any potentially coverage damage, i.e., outside the business risk exclusions, such as, the discoloration to surface paint applied to stucco, is not covered because it did not occur during the First Mercury policy periods. As First Mercury say it, its policy period ended in November 2014 and the paint damage was both alleged and proven to have occurred in late 2016 or early 2017. An insured and another insurer opposed First Mercury’s motion for summary judgment.

In making its argument, First Mercury acknowledged that California’s Montrose decision applied, to wit: “where the damage at issue is alleged to be a continuous and progressive injury, the date of discovery of the damage or injury is not controlling. It is only the effect -- the occurrence of bodily injury or property damage during the policy period, resulting from a sudden accidental event or the ‘continuous or repeated exposure to conditions’ -- that triggers potential liability coverage.”

However, First Mercury’s argument was, essentially, that paint discoloration is not in the nature of a continuous injury: “First Mercury asserts, without citation, that ‘[p]aint discoloration, unlike, for example, structural damage to a home, is not a latent defect. Consequently, the date on which the paint discoloration was first observed is at least presumptively the date of occurrence absent the presentation of evidence to the contrary.’”

First Mercury’s argument had the sense of “we know what the continuous trigger is designed to addressed, and this isn’t it.” And maybe it’s not. But summary judgment was not the right place for it.

But the court was not convinced: “First Mercury’s argument rests on the assumption that the Sluskys [homeowners] observed the paint discoloration at the same time when it first occurred. But there remains the possibility that the paint discoloration occurred earlier. As with ‘improper piling of dirt against [a] building’ that results in dry rot damage or a crack in a swimming pool that eventually leads to leakage, it is possible that here the occurrence of the paint damage began far earlier than when the Sluskys first observed it.” Thus, First Mercury’s motion for summary judgment was denied.

The continuous trigger was born out of a legal fiction. At least one court has said as much. “The continuous trigger theory is a legal fiction permitting the law to posit that many repeated small events occurring over a period of decades are actually only one ongoing occurrence. In cases where property damage is continuous and gradual and results from many events happening over a long period of time, it makes sense to adopt this legal fiction for the purposes of determining what policies have been triggered.” Pub. Serv. Co. of Colo. v. Wallis & Cos., 986 P.2d 924, 939 (Colo. 1999).

So perhaps it is no surprise that paint discoloration could trigger multiple policies, despite that it can be identified with the naked eye, unlike many other types of construction defect-related property damage, the happening of which cannot be.

|

|

|

|

|

|

|

Vol. 7 - Issue 7

September 26, 2018

If Your Coverage Was Coppertone: Coverage Opinions In August:

What You May Have Missed

|

|

|

|

- Very Interesting Development: Ohio Legislature Says No To The ALI Restatement of the Law, Liability Insurance

- Most Insane Duty To Defend Decision I’ve Ever Seen

Insurer Would Have Benefitted From The New ALI Insurance Restatement

- Determining Covered Vs. Uncovered Claims: Court Slams The Door On One Insurer’s Effort

- First Court Decision Post-ALI Restatement Adoption

- Policyholders Will Shout Doobious Decision: Marijuana Coverage And An Issue I’ve Never Seen Before

- The Great Insurance Policy Mystery

|

Coverage Opinions was on hiatus in August. Lots of people were on vacation and I needed a break from the task of putting together a full-blown issue, including the time-consuming interview. But I didn’t want CO to go completely silent. So I did some mini issues – a case here and a case there, here a case, there a case…. In case you were more focused on sun and sand, than coverage, in August, here’s what you missed in the Coverage Opinions mini issues.

Very Interesting Development: Ohio Legislature Says No To The ALI Restatement of the Law, Liability Insurance

On July 30th, Ohio Governor John Kasich signed into law SB 239. According to the Governor’s press release, it modifies the law concerning regional councils of governments to clarify that a municipal corporation eligible to designate a tourism development district may designate more than one district. Obviously, that’s important to someone.

SB 239 also names certain highways after people. For example, a portion of Interstate Route 270 in Franklin County is now designated the “Officers Anthony Morelli and Eric Joering Memorial Highway.”

But SB 239 doesn’t stop there. It then adds this provision: Sec. 3901.82. “The Restatement of the Law, Liability Insurance’ that was approved at the 2018 annual meeting of the American law institute does not constitute the public policy of this state and is not an appropriate subject of notice.”

I couldn’t locate much in the way of legislative history for this. A footnote in the Bill Analysis states: “Restatements of Law are nonbinding treatises on legal subjects that seek to inform judges and lawyers about general principals [sic] of common law. The American Law Institute is an organization of judges, legal academics, and practitioners that publishes the Restatements. The General Assembly may set the public policy of the state while the judicial power is vested in the courts of Ohio. Ohio Const., art. IV, sec. 1.”

On its face, the Ohio legislature’s statement, that the just-approved ALI’s Restatement of the Law, Liability Insurance does not constitute the public policy of Ohio, and is not an appropriate subject of notice, is not a big dent in the Restatement. Look, I love Ohio. I even had my picture taken a few years ago with the Red’s Mascot, Mr. Redlegs. Really. I can send you the picture. But Ohio is just one state.

But this Ohio action is still very significant. The insurance industry’s displeasure, with the Liability Insurance Restatement, has been well-documented. This legislative achievement demonstrates just how strong that objection to the Restatement is. Will other states follow suit? Are there any other efforts like this underway?

More broadly, what does this mean in Ohio for the ALI’s many other Restatements that it has adopted over the past many decades?

Does the Ohio legislature’s statement, that the General Assembly may set the public policy of the state and judicial power is vested in the courts of Ohio (cite to the Ohio Constitution) mean that the ALI’s other Restatements do not constitute the public policy of Ohio and are not an appropriate subject of notice? After all, the legislature’s statement addressed Restatements in general, vis-a-via the role of the General Assembly and courts, and did not speak to any specific concerns about the Insurance Restatement. Based on a Lexis search, Ohio courts, not surprisingly, have addressed Restatement provisions of all stripes in thousands of cases.

Most Insane Duty To Defend Decision I’ve Ever Seen

Insurer Would Have Benefitted From The New ALI Insurance Restatement

Sometimes there is little doubt that an insurer has a duty to defend. Other times there is a lot of doubt. Nonetheless, the court concludes that a defense is owed on account of the operation of legal principles. For example, the court decides that a defense is owed because the duty to defend is broad. So long as there is some possibility of coverage, the court explains -- even if it’s the same possibility as me beating LeBron at one-on-one – a defense is owed. Or a defense is owed because the court, in reaching its decision, was constrained by the allegations in the complaint, i.e., the four corners rule. No matter how clear it may be that extrinsic facts negate a duty to defend, the court simply could not consider them. It was forced to wear blinders. Its hands were tied.

Late last month a Texas appeals court concluded that an insurer was obligated to defend its insured for the later reason. But here the court’s rote application of the four corners rule led to an absurd result. It may be the most insane duty to defend decision I’ve ever seen. As insane as using the self-serve check-out at the supermarket when you have fruit.

Ironically, while insurers have spared no criticism of the ALI’s recently adopted Restatement of Liability Insurance, here, application of the Restatement would have benefited the insurer.

In Avalos v. Loya Insurance Co., No. 04-17-00070 (Tex. Ct. App. July 25, 2018) the court addressed whether an insurer had a duty to defend a motor vehicle accident.

Rodolfo Flores was moving his wife’s vehicle, outside their home, when he collided with the vehicle owned by the Hurtados. Flores’s wife, Karla Guevara, was insured under a policy issued by Loya Insurance Co. But the policy contained a named driver exclusion for Flores. Oh, that’s a problem. Solution -- the Hurtados, Guevara and Flores reported to the police and insurance company that it was Guevara – and not Flores – who was driving the vehicle at the time of the accident.

The Hurtados filed suit against Guevara, the supposed driver, for their injuries. Loya Insurance Company retained counsel to defend Guevara. Loya eventually figured out that Guevara was not the driver, but, rather, Flores was. Loya disclaimed coverage based on the named driver exclusion. Defense counsel retained by Loya withdrew and judgement was rendered against Guevara for $450,000.

The Hurtados, as assignees of Guevara, filed suit against Loya for a host of things – negligence, breach of contract and Texas statutory violations. The Hurtados alleged that Loya breached its duty when its counsel, retained for Guevara, withdrew. Loya filed a counter claim for fraud and a declaration of no coverage for a defense and indemnity.

In a Motion for Summary Judgment, Loya attached the deposition testimony of Guevara where she admitted that Flores was driving the vehicle at the time of the accident. For reasons not detailed in the opinion, the trial court granted Loya’s Motion for Summary Judgment.

The Texas Court of Appeals reversed.

The court’s description of the competing arguments were just what you would expect:

The Hurtados argued that a defense was owed based on the allegations in the complaint. Period. End of story. The court explained: “The Hurtados assert that under the eight-corners rule, an insurance company’s duty to defend its insured in a lawsuit is determined by looking to the allegations contained in the petition and the terms of the insurance company’s policy. According to the Hurtados, because they alleged Guevara was negligently operating her vehicle in the underlying car accident and she is covered by the insurance policy, Loya Insurance Company had a duty to defend Guevara in the negligence suit the Hurtados filed against her.”