|

|

|

|

|

|

Vol. 7 - Issue 3

April 11, 2018

|

|

|

|

|

|

|

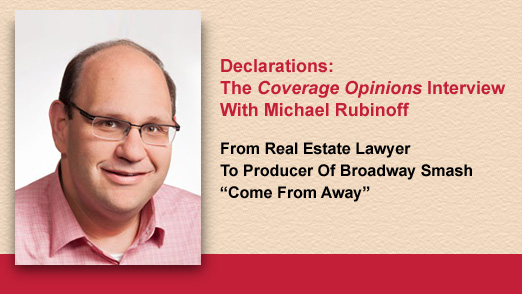

“You want to do WHAT?” That’s how Michael Rubinoff described to me people’s reactions to his idea. And no wonder they were so incredulous. The what was the making of a musical tied to the terrorist attacks of September 11, 2001. Many thought Rubinoff was unhinged. But nobody does now. His outlandish idea became “Come From Away,” the smash hit Broadway musical that just celebrated its one year anniversary at the Gerald Schoenfeld Theatre.

That it is a musical with a 9/11 connection is just part of what makes “Come From Away” peculiar. There’s this too -- Rubinoff dreamed up the idea while practicing law in Toronto.

I’m on the phone with Michael Rubinoff to understand how a musical, with an improbable premise and curious name, nominated for seven Tony Awards, winner of several Best Musical awards and one of the toughest tickets in town, was conceived of by a guy who made his living representing parties in commercial real estate transactions.

“Come From Away” tells a true, and under-reported, story that came about after U.S. airspace was closed immediately following the September 11th terrorist attacks. Many planes needed an alternative place to land. For 38 of them, it was a town in Newfoundland, Canada, called Gander (pop. 9,000). With no advance notice, the tiny Gander practically doubled in size when over 7,000 visitors landed, literally, on its doorstep. For several days the citizens of Gander opened their homes and hearts to these strangers. The town came to a standstill as its citizens took care of the needs of those they called the “come from aways.”

What took place in Gander is a story most definitely worth telling. But it sounds like the stuff of a documentary on the Discovery Channel. Not singing and dancing. This is 9/11! How could “Come From Away” even get made – and by a real estate lawyer -- and then reach the Great White Way? The show’s producer, Michael Rubinoff, with an easy-going manner and manic schedule, was kind enough to find 30 minutes to tell me. It is a story as fascinating as what took place in that small Canadian town sixteen years earlier.

“You want to do WHAT?”

My first question for Michael Rubinoff is the supremely obvious one. He explained that the idea for “Come From Away” grew out of his Canadian pride. The story of the many planes landing in Gander was reported in Canada. “It was a Canadian connection to what was such a tragic day,” Rubinoff told me. “It took years for more and more stories [about Gander] to came out,” he explained. And as they did “it made me so proud to be a Canadian.” The story stayed with him. “Every time I would read something about it, it would bring all this emotion and all this pride. It was a real recognition of what I believe are Canadian values. And I was proud to count myself as a Canadian alongside these incredible people in Newfoundland.”

But what about putting it to music? Here I should tell you that, in addition to practicing law full time, Rubinoff was producing musicals in Toronto. His philosophy in that role was that a musical requires “a compelling story and a compelling reason to musicalize that story.”

What happened in Gander was the compelling story. Putting it to music, he explained, is owed to the culture of Newfoundlanders. “The way they tell their stories is through music. . . . This is such a part of who they are,” he said. “There was no doubt in my mind that if the right people could come along that this could be a compelling musical.” But, he is quick to add, laughing, “I never believed that it was going to be what it has become. I certainly am in awe of that every day.”

So Rubinoff had his compelling story and compelling reason to musicalize it. But, in this case, it took more than simply checking these two boxes. This wasn’t exactly Hello Dolly, The Sequel he was pitching to proposed writers. Many turned him down. “How can you possibly do a musical about 9/11?” people asked, dubiously. “It sounded very distasteful,” Rubinoff acknowledges. “But I don’t think people really understood the story of what happened. They couldn’t get past 9/11 to even go further to do some of the research into what happened out there. That was mostly the reaction. You want to do WHAT?”

Rubinoff finally found his writers in the Canadian husband and wife team of David Hein and Irene Sankoff, whose work he came to know after seeing one of their productions and being “floored” by it. He reached out to Hein and Sankoff and the writing duo had enough interest in the story to pursue it further. They visited Gander for a month, on the tenth anniversary of September 11th, and returned with the stories need to create “Come From Away.” In hindsight, Rubinoff is thankful that so many turned him down. “David and Irene,” he said with emotion, “were the right people to tell this story. They had the right hearts and ability and empathy in terms of how to tell this story.”

But how this curious idea, that so many other writers wanted no part of, ultimately made it to the biggest of all stages has to do with Michael Rubinoff’s career as a lawyer. Or, to be more accurate, his decision to retire from it.

Practicing Law

Rubinoff earned his law degree from the University of Western Ontario in 2001 and entered private practice with a Toronto firm. He did some entertainment law work, but, explained, “it is hard to sustain a sole entertainment law practice in Canada.” The bulk of his work was commercial real estate and its financing.

But Rubinoff had a second job--theatrical producer. He described his shows as “mid-size,” often being the Canadian productions of ones that had been off-Broadway in New York. He raised the money, oversaw marketing and advertising and “sometimes I had to bring the laundry home and do it myself,” he said, chuckling.

Rubinoff called his dual life “a very interesting existence.” But not an easy one, he explains: “The demands of the practice of law are extremely significant and so are the demands for a producer. They were very long days. Getting into the office by 5 A.M., working away, going for lunch down to a rehearsal hall or a theater, working away again, and then getting down to the theater for curtain.”

Rubinoff tells me that he valued being the best lawyer he could be for his firm and clients. But, he also conceded, “I didn’t think it was a surprise to anybody where my true passion was, which was in the theater.”

|

| |

Law: Stage Left – Theater: Stage Right

On December 31, 2010, Michael Rubinoff practiced his last day as a lawyer. Three days later he started at Sheridan College, in Oakville, Ontario, as associate dean of visual and performing arts. “On my way from the car to the door I thought ‘what the heck did you just do? How could you leave a lucrative law practice’ … and go into academia?’” Rubinoff said he asked himself. “But I have to tell you it was the best decision I’ve made professionally And ‘Come From Away’ certainly would not exist if that did not happen.”

Rubinoff was not unfamiliar with Sheridan College. He described it as having “Canada’s leading music theater performance program” and, as a producer, had been going there to “scout talent.” He had also been the chair of the music theater program’s professional advisory committee, advising faculty on the currency of curriculum and trends in the industry.

|

|

|

|

Leaving the law for a full-time theater career had never been an end-game for Rubinoff. He told me that he loved law school and had “no regrets” about being a lawyer. But the positon at Sheridan, which he did not seek out, happened to be offered at a time when he had been figuring out what he wanted to do next: “Was the practice of law going to be the be-all-and-end-all or was I going to switch into something, whether it was going in-house or switching to something that was more engaged in entertainment?”

One of Rubinoff’s objectives at Sheridan was to transfer the program from one offering a diploma after three years to providing a degree after four years. This required a fourth year “capstone project,” where the students could apply the skills they’d learned to something substantial. That was the incubator for the creation of musicals, Rubinoff explained, which became The Canadian Music Theatre Project. The first musical that the Project workshopped was “Come From Away.” After that the show played at the La Jolla Playhouse, the Seattle Repertory Theatre, Ford’s Theatre in Washington, D.C. and the Royal Alexandra Theatre in Toronto, before opening on Broadway in March 2017.

So many were not interested in the story of “Come of Away” because they could only see tragedy. Rubinoff saw something different–the best of humanity on display following a demonstration of the worst in humanity. “Come From Away” is a wonderful feel-good story. Rubinoff’s story is also feel-good. He left the practice of law to pursue a passion. This he did for himself and the students of Sheridan College. But in the end so many more benefitted. |

|

Once A Lawyer…

While Michael Rubinoff may have practiced his last day as a lawyer at the end of 2010, that was only in an official capacity. His skills, he tells me, still prove useful to him these days in developing musicals: “The most important role you can play in supporting the writing, especially at the start, is by cross examining [the writers], in a really positive way. ‘What are you trying to say in this song? What are you trying to say in this verse? What are you trying to achieve?’” Rubinoff said that “writers are sometimes better at articulating things first before writing what they actually want to say.” This cross–examination, he explains, allows him to assist writers to get their songs to where they want them to be.

Rubinoff keeps his cross-examination skills sharp as a producer. But what about the ultimate melding of the two. Is there a musical about the law in Rubinoff’s crystal ball? I wonder. He laughs. “Something about lawyers and the law is very much on my mind. I have not found the way in just yet. But who knows?” he asks. Maybe there’s a story in “a lawyer leaving the practice of law and running away with the circus at a musical theater program,” Rubinoff says, chuckling. “I’m not sure yet because the story is still very much unfolding.” |

|

|

|

| [Elizabeth Vandenberg, a student at University of Iowa College of Law, assisted with this article.] |

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Vol. 7, Iss. 3

April 11, 2018

Take Me Out To The Ball Game…

So I Can Sue

|

|

|

|

|

| |

Baseball is here! Or, in other words, just five more months till football season. It’s been a struggle for baseball of late. It has ceased being the national pastime, having been surpassed by professional football, college football, the NCAA Men’s Basketball Tournament and even the NFL draft has more anticipation. A documentary on Nick Saban’s fabulous hair could charge more for a 30 second spot than a Tigers game.

But, thankfully, baseball still provides wonderful litigation (perhaps that’s the real national pastime). As a long-time student of litigation involving sports, especially when fans are involved, I was delighted to see the recent coverage decision in The Schenectady Manatees Baseball Club, Inc. v. Iceberg Insurance Co., No. 17-4296 (N.Y. Supr. Ct., Schenectady Cty., Mar. 30, 2018).

The coverage action arose out of the following circumstances. The Manatees are a semi-professional baseball team in Schenectady, New York. They are immensely popular and play their home games at The Ocean stadium. In 2015 The Ocean underwent a renovation and 500 seat expansion to bring the total to 3,500. To finance the renovations and expansion, the Manatees undertook an aggressive season ticket marketing campaign. This included boasting about many exciting culinary offerings that the newly refurbished stadium would feature. A season ticket brochure listed some of these – sushi, fish tacos, Portobello mushroom sandwiches and hot dogs with gluten free rolls.

Long time Manatees fan Herbert Greenblatt purchased two season tickets for 2016. During the opening game he tried the stadium’s new sushi and was pleased. Likewise with the fish tacos during the second game. Game three is where the trouble began. Greenblatt set out to sample the stadium’s much touted Portobello mushroom sandwich. However, he was informed at the concession stand that The Ocean did not offer them. He explained to the employee at the counter that the Manatees’ season ticket brochure stated that Portobello mushroom sandwiches would be served. But all the stadium employee could do was shrug his shoulders and offer to let Greenblatt speak to his supervisor.

Not satisfied, Greenblatt took the matter up with The Ocean’s management. They could only offer an apology, explaining that, at the time the brochure was printed, Portobello mushroom sandwiches had been intended to be sold. But they were left off the final list of new menu items.

Still not satisfied, Greenblatt filed suit, alleging in Herbert Greenblatt v. The Schenectady Manatees Baseball Club, Inc., No. 16-7612 (N.Y. Supr. Ct., Schenectady Cty.) that the Manatees induced him to purchase season tickets by offering to sell Portobello mushroom sandwiches at The Ocean and he relied on this promise when making his decision. Greenblatt included clams for fraud, fraudulent inducement, breach of contract, unjust enrichment, negligence and violation of various New York consumer protection laws. He alleged mental anguish and “loss of enjoyment of the Manatees game experience.” Greenblatt sought an injunction to compel the Manatees to sell Portobello mushroom sandwiches at The Ocean.

The Manatees provided notice of the Greenblatt suit to Iceberg Insurance Co., its commercial general liability insurer.

Iceberg gave The Manatees a chilly response -- disclaiming coverage for a defense. The insurer acknowledged that Greenblatt’s allegations of mental anguish qualified as “bodily injury” under New York’s seminal case -- Lavanant v. Gen. Acc. Ins. Co. of Am., 595 N.E.2d 819 (N.Y. 1992). However, the insurer maintained that Greenblatt was not seeking damages for “bodily injury.” As the insurer saw it, despite the host of claims and damages discussed in the body of the complaint, when push came to shove, and you examined the complaint’s Wherefore clause, all that Greenblatt was seeking was an injunction to compel the Manatees to sell Portobello mushroom sandwiches at The Ocean. Indeed, as the insurer noted in its response to the letter challenging the disclaimer, that’s what Greenblatt told the local paper in a story written about his suit. Greenblatt was quoted as saying, “I’m not trying to put the Manatees out of business. I don’t want their money. I just want to eat a Portobello mushroom sandwich while watching the team play. How hard can that be?”

The Manatees hired counsel to defend the Greenblatt action. After several months of motion practice the parties reached a settlement. While The Manatees did not agree to provide Portobello mushroom sandwiches at its games, the team would add white mushrooms to its salad and name it The Green-blatt. In addition, Greenblatt would get to dress up as the team’s mascot -- The Mighty Manatee – for one game. However, this part of the settlement was kept confidential, so that any young fans, who heard about the settlement, would not be disappointed to learn that The Mighty Manatee is really a person in a costume.

The Manatees incurred $40,000 in defense costs and filed suit against Iceberg, alleging a breach of the duty to defend. On cross motions for summary judgment the court held that the insurer breached its defense obligation.

The court was not convinced that Greenblatt was not seeking damages for “bodily injury.” The court acknowledged that Greenblatt’s Wherefore clause was limited to an injunction to compel the Manatees to sell Portobello mushroom sandwiches at The Ocean. However, the court concluded that, by alleging, in the body of the complaint, mental anguish and “loss of enjoyment of the Manatees game experience” – which was “property damage” based on loss of use -- Greenblatt was seeking “damages” because of “bodily injury” and “property damage.”

What’s more, the court took Iceberg to task for relying on Greenblatt’s statement to the press – “I’m not trying to put the Manatees out of business. I don’t want their money” – as part of its decision that he was not seeking “damages.” This, the court noted, was an impermissible use of extrinsic evidence to deny a duty to defend.

|

That’s my time. I’m Randy Spencer. Contact Randy Spencer at

Randy.Spencer@coverageopinions.info |

|

|

| |

|

|

|

|

Vol. 7, Iss. 3

April 11, 2018

Encore: Randy Spencer’s Open Mic

Bad Bad Leroy Brown And Insurance Coverage

|

|

|

|

|

| |

|

| |

Last week a California appeals court held that no coverage was owed to Leroy Brown for water damage caused by a broken pipe in his home. Apparently the insurer and court were not afraid to say no to the baddest man in the whole damn town. See Brown v. Mid-Century Ins. Co., 215 Cal. App. 4th 841 (2013).

This got me to thinking. If Leroy Brown were involved in a coverage case, then maybe other people, famous for having a part in a song, have also been involved in a coverage dispute that went so far as a reported opinion. It turns out that the answer is yes. And a lot. Look at how busy some of your favorite folks from songs have been.

Millers’ Indemnity Underwriters v. Maggie May Patten, 238 S.W. 240 (Tex. Ct. App. 1922)

Bille Jean Dowling v. Harleysville Ins. Co., 602 A.2d 871 (Pa. Super. Ct. 1992)

Rhiannon Moller v. State Farm, 566 N.W.2d 382 (Neb. 1997)

Roxanne Hicks v. Auto Club Group Ins. Co., 815 N.W.2d 473 (Mich. 2012)

Western World Ins. Co. v. Sharona Corp., 353 N.W.2d 221 (Minn. Ct. App. 1984)

Lola Ferguson v. State Farm, 2011 WL 4946349 (D. Alaska Oct. 18, 2011)

Fernando v. Chubb Group of Ins. Cos., 2012 WL 4754148 (La. Ct. App. Jan. 18, 2012)

Jimmy Corn v. Protective Life Ins. Co., 1998 WL 51783 (D. Conn. Feb. 4, 1998)

Mandy Allen v. Zurich Am. Ins. Co., 2012 WL 3061598 (W.D. Okla. July 26, 2012)

Allison v. State Farm, 266 Fed. Appx. 627 (9th Cir. Feb. 12, 2008)

Owners Ins. Co. v. Daniel, 2012 WL 6163139 (M.D.Ga. Dec. 11, 2012)

Diane Jack v. St. Paul Ins. Co., 1994 WL 14580 (Ark. Ct. App. Jan. 12, 1994) (ok, some artistic license there)

Vintage Plastics, LLC v. Mass. Bay Ins. Co., 2012 WL 1142722 (N.D. Okla. Apr. 4, 2012) (plaintiff represented by Casey & Jones) (yes, that one’s a stretch)

I disclaim all liability for any songs that get stuck in your head.

|

That’s my time. I’m Randy Spencer. Contact Randy Spencer at

Randy.Spencer@coverageopinions.info |

|

|

| |

|

|

|

| |

|

Vol. 7, Iss. 3

April 11, 2018

Thank You For Making Insurance Key Issues The #1 New Release Law Book On Amazon

|

|

|

|

|

|

| |

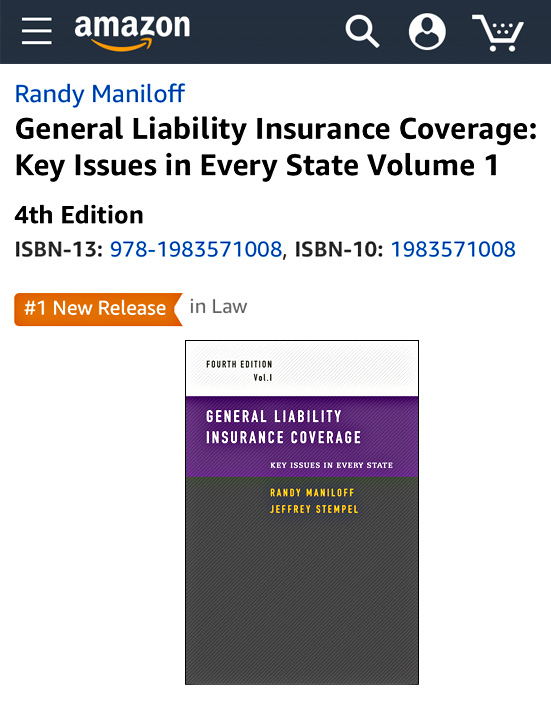

I am thrilled to report that the 4th Edition of General Liability Insurance Coverage - Key Issues In Every State debuted as the #1 "New Release" of all Laws Book on Amazon!

I didn’t buy any copies. And there are only so many I can get my mother to buy. So the only explanation for this successful launch is that Coverage Opinions subscribers made it happen. For this, Jeff and I are extremely grateful.

There is no satisfaction in writing a book (it's a slog and the economics make absolutely no sense). The only satisfaction comes from knowing that your peers are using it. Please accept my heartfelt thanks for providing this.

Insurance Key Issues is a unique 50-state survey book. The 4th Edition adds over 900 new cases - mostly from 2014 to 2017.

At close to 1,000 pages, Insurance Key Issues sets forth the rules that have been adopted by all 50 states, and the District of Columbia, for 20 important and commonly occurring general liability insurance coverage issues. And about half the issues are just as relevant for professional liability claims scenarios.

If you want an esoteric discussion of coverage, do not buy Insurance Key Issues. Buy a treatise. But if you just want to have the answers immediately at your fingertips, on the liability coverage issues that arise every day, then you'll be pleased with what Insurance Key Issues has to offer. The book provides significant details not always seen in 50 state surveys. Jeff and I would not have spent 10 years on a project unless we knew it was unique.

If you like Coverage Opinions, rest assured that the same effort has gone into Insurance Key Issues.

For more information visit the Insurance Key Issues website -- http://insurancekeyissues.com

|

| |

| |

| |

|

|

|

|

Vol. 7 - Issue 3

April 11, 2018

Contest:

Win A Copy Of The 4th Edition Of General Liability Insurance Coverage – Key Issues In Every State

|

|

|

|

| |

|

The last contest that I did, to win a copy of the 4th Edition of General Liability Insurance Coverage – Key Issues In Every State, was an overwhelming success – despite the effort it took to keep track of the ridiculous number of entries. Clearly the contest’s popularity had much to do with the ease of entering – just pick the winners of a few college basketball games. [See nearby article for winners.] Other CO contests have had loads of entries, but not nearly as many as this time, no doubt because of the effort those took to enter, such as the insurance coverage license plate contest or insurance coverage haiku contest.

Here’s the next contest (it’s more effort than picking a few basketball games, but still less than thinking of an insurance coverage haiku): Tell me an insurance coverage joke or riddle. For example, my favorite (and stop me if you’ve heard this): What do you call it when parties reach a settlement of a trigger and allocation dispute? Answer: A Montruce.

A couple of ground rules: Keep it clean (although, if you can somehow tell a dirty insurance coverage joke, Wow!) and nothing offensive. It must also be completely original. So if you Google “insurance jokes” I’ll do the same thing and out you. Deadline to enter: April 25

The two best jokes will each win a copy of the 4th Edition of Key Issues.

I am the judge and no complaining if you think your joke was funnier than one of the winners.

My gut tells me that there are not going to be a ton of entries this time, so if you enter you should have a decent chance of winning.

Gotta go – I just flew in from a coverage mediation in Cleveland and boy are my arms tired.

[No purchase necessary. Employees of Coverage Opinions are not eligible. Void where prohibited. And I hereby incorporate by reference all of the rules from the McDonald’s Monopoly Game. They must have tons of lawyers working on that and include all of the right fine print.]

|

| |

|

| |

|

|

| |

|

|

|

|

Vol. 7, Iss. 3

April 11, 2018

Why The 4th Edition Of Insurance Key Issues Is Only #3 On The Non-Fiction Bestsellers List

|

|

|

|

Answer: I couldn’t reach the top shelf. |

|

|

| |

|

| |

|

|

|

|

Vol. 7, Iss. 3

April 11, 2018

Announcing The Winners Of The Insurance Key Issues NCAA Final Four Contest

|

|

|

|

|

| |

In advance of the Final Four of the NCAA Men’s College Basketball Championship I invited Coverage Opinions readers to tell me the two teams that would play in the final game, the winner and the total points scored (without going over). The two entries with the most correct answers would receive a complimentary copy of the 4th Edition of Insurance Key Issues.

The response was incredible. The number of entries was so overwhelming that I had to pay someone to help manage them. It was like that episode of Star Trek where the Tribbles kept multiplying non-stop and became out of control.

Except for dealing with the administrative challenge, I was the real winner of the contest (cue the soppy music). I got to read some funny entries, some who provided analysis of their picks and some nice notes about Coverage Opinions and Key Issues. Thank you to all who entered and those who sent kind words. I tried to respond to them all, but it was overwhelming. Please do not hold it against me if I did not respond. Believe me, I appreciated it.

Now, to the winners of the Insurance Key Issues NCAA Final Four Contest:

Only one person got it all right – choosing the winner of all three games and getting the points in the final game (141) dead on. Congratulations to Ken Gorenberg of Barnes & Thornburg, LLP in Chicago. It is no surprise that Ken nailed it, as he provided a detailed analysis of his picks, based on certain city and school allegiances. As for the total points for the final game, Ken said: “In its [Villanova’s] two earlier title victories, the total scores averaged 140.5. This whole exercise is over the top, so it rounds up to 141.”

The Coverage Opinions Prize Patrol will be showing up at Ken’s door to present him with a copy of the 4th Edition of Insurance Key Issues. Congratulations!!

There were also five entries that tied for second with 140 points. The CO Prize Patrol will also be delivering copies of the 4th Edition of Insurance Key Issues to:

Donald J. Sonlin

Senior Vice President, Claim Officer

Chubb North America Claims

Basking Ridge, New Jersey

Barbara Laskaris

Assistant Vice President

Large Loss Specialist - Construction Defect Claims

Arch Insurance Group

San Francisco

Angela Paye, M.A.

Pauli-Shaw Insurance Agency

Arcata, California

Will Lehman, CPCU, ARM

Risk Manager

Cook Group Incorporated

Bloomington, Indiana

Richard Hartzen

Congratulations to the winners and thank you to all who entered. And congratulations to Villanova! Their victory parade could be seen from my office window last week.

Visit the Insurance Key Issues website: http://insurancekeyissues.com

|

| |

|

|

|

|

Vol. 7, Iss. 3

April 11, 2018

Big Moment For The Little Newsletter:

Coverage Opinions Quoted In The Wall Street Journal

|

|

|

|

The recent tragic accident, involving a pedestrian in Arizona who was struck and killed by an Uber self-driving automobile, caused The Wall Street Journal to take a look at how autonomous vehicles may impact the insurance system. I looked at this issue in a 2015 Coverage Opinions story. It was quite a thrill to see that the WSJ quoted from it for its story. Check it out here:

http://www.coverageopinions.info/DriverlessCars.pdf

See further down in this issue of CO for an updated version of the 2015 article.

|

|

|

|

|

Vol. 7, Iss. 3

April 11, 2018

Trust Me: You Gotta See The Name Of This Insured In A Coverage Case

Federal Court Clears Mary Poppins Of Wrongdoing

Win A Copy Of The 4th Edition Of Insurance Key Issues

|

|

|

|

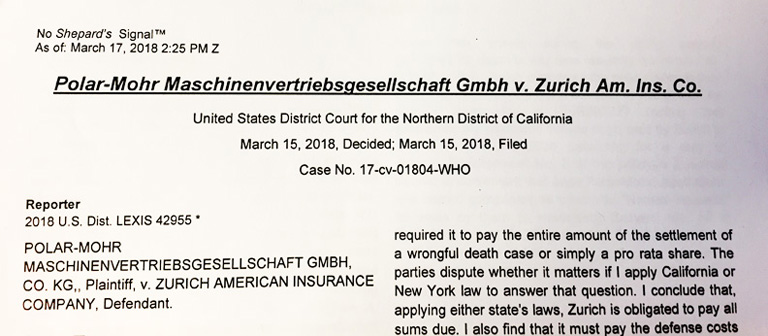

In mid-March the Northern District of California decided Polar-Mohr Maschinenvertriebsgesellschaft GMBH Co. KG v. Zurich, No. 17-1804 (N.D. Calif. March 15, 2018). Yes, that’s really the name of the insured. Hers’s a picture of the decision. |

|

|

| |

That’s gotta be the longest name of an insured in the history of insurance.

My advice to lawyers representing Polar-Mohr Maschinenvertriebsgesellschaft GMBH Co. KG -- do not refer to the company in a brief as: hereinafter “Maschinenvertriebsgesellschaft.”

I’ll send a complimentary copy of the 4th edition of Insurance Key Issues to the first person who can send me a coverage case – no, make that any case in the history of America -- involving a party with a longer name.

Clearly this is the Supercalifragilisticexpialidocious of insurance coverage. And as you’ll see in the nearby article – “Viking Bump For Policyholders: California Court Interprets New York Allocation Law As ‘All Sums’” -- some policyholders will likely be saying Maschinenvertriebsgesellschaft loud enough to always sound precocious.

This got me to thinking – Has the word supercalifragilisticexpialidocious ever been cited in a judicial decision? Yes, it has. Six times based on a Lexis search. One of the cases involves the rapper Ja Rule, who I was not familiar with until recently after hearing his wonderful performance of “Helpless” on the 2016 Hamilton Mix Tape.

But the supercalifragilisticexpialidocious decision that took my breath away is Life Music, Inc. v. Wonderland Music Co., 241 F. Supp. 653 (S.D.N.Y. 1965). It turns out that the producers of Mary Poppins were sued for copyright infringement. The charge? Their alleged use of Supercalifragilisticexpialidocious infringed the copyright of the song Supercalafajalistickespeealadojus. The court, wisely, stated: “All variants of this tongue twister will hereinafter be referred to collectively as ‘the word.’” I am not making this up.

Despite how similar “the words” appear, the court told the plaintiff to go fly a kite, holding that it was not entitled to an injunction against Mary and Bert.

First, the judge concluded that, after listening to “phonograph records of both works,” in his opinion, “as an average observer, there is no discernible similarity between the music of both songs.” The judge stated: “An affidavit by a musical expert, submitted by defendants, supports this conclusion. The expert analyzed and compared the melody lines of both songs and concluded that there is not a single instance of any two parallel notes appearing in succession, or of a single measure, phrase or theme showing the slightest melodic similarity.”

As for the remarkable similarity in the words themselves, this was not a basis for an injunction: “[D]efendants have submitted several affidavits of presumably disinterested persons who swear that variants of ‘the word’ were known to and used by them many years prior to 1949, when plaintiffs claim to have written their song. On the basis of the record before me, and for the purpose of this preliminary motion only, I find that ‘the word’ was known to and used by members of the public for many years prior to 1951, the date when plaintiffs allegedly published their song. The significance of this is not that defendants are immunized from infringement liability if they, in fact, copied from plaintiffs; a copier can hardly escape liability merely by asserting his right to appropriate the underlying ideas or public domain aspects of the copyrighted work. Rather, the fact that ‘the word’ was known to the public, coupled with affidavits by the defendant composers that they knew of ‘the word’ before plaintiffs composed their song, effectively negates, for purposes of this motion, the inference of copying which plaintiffs would have me draw merely from the highly questionable allegations of access plus the fact that ‘the word’ appears in both songs.”

As the writers of Supercalafajalistickespeealadojus no doubt saw it, Mary Poppins wasn’t so practically perfect in every way.

|

| |

|

|

|

|

Vol. 7, Iss. 3

April 11, 2018

What A Really Clever Idea For A Coverage Article

Guest Author: Michael Young, HeplerBroom, St. Louis

|

|

|

|

As a reader and writer of many insurance coverage articles, I am always impressed when someone comes up with a clever idea for one. It is not easy to do. That’s why I so liked this article from Michael Young, a very talented coverage lawyer at HeplerBroom, LLC in St. Louis. Michael took a famous coverage decision and examined it, not from the legal perspective, as we are all usually so wont to do, but its historical one. Kudos to Michael for this impressive piece and my thanks to him for letting me share it with Coverage Opinions readers. |

|

|

|

| |

The Little Known Story Behind Maryland Casualty v. Peppers

Michael Young

HeplerBroom, LLC

|

| |

| |

Perhaps no appellate court decision is more famous in insurance coverage circles than the Illinois Supreme Court’s opinion in Maryland Casualty Co. v. Peppers, 64 Ill. 2d 187, 355 N.E.2d 24 (1976). Most insurance practitioners know the case as one of the first to recognize the right of a liability insured to independent counsel (i.e. “Peppers counsel”) should a coverage defense raised by the carrier pose a conflict for a lawyer to represent both the interests of insured and insurer.

On a very simple level, the basic fact pattern in Peppers presents the classic conflict situation: the insured was alleged to have both negligently and intentionally caused bodily injury to the claimant. As the Illinois Supreme Court explained, “In the personal injury action if [the insured] Peppers is held responsible, it would be to his interest to be found negligent, which, under the policy of insurance, would place the financial loss on [the insurer] St. Paul.” The court continued: “On the other hand it would be to St. Paul’s interest to have a determination that Peppers intentionally injured [the claimant], which, by the terms of the policy, would relieve St. Paul of the obligation to pay the judgment.” Because of this conflict, the Supreme Court held that the insured was entitled to independent defense counsel.

A closer read of the facts in Peppers, however, reveals an even more interesting story. The insured owned three separate buildings on the same street: his home, another building and a Pizza Hut. “Because the Pizza Hut had been burglarized on numerous occasions,” the court explained, “Peppers had been staying in that building at night.” On the evening in question, “Peppers was awakened by a noise at the door which he determined was caused by someone trying to break in.” The court continued: “When he went to the door he saw a person fleeing. He shouted for him to stop and then fired his shotgun, wounding the fleeing person, James Mims.”

The idea of someone sleeping overnight in his Pizza Hut to prevent future burglaries seems very strange until one considers the time and place of these events: January 1971 in East St. Louis, Illinois. People familiar with East St. Louis today know it as a small city that struggles with high unemployment, poverty and crime. Sixty years ago, however, East St. Louis was a very different place.

Just across the Mississippi River from St. Louis, Missouri, East St. Louis grew into a major industrial and rail center in the first half of the twentieth century. Though always a bit rowdier than its counterpart across the river, East St. Louis became fairly prosperous during this time period. As described in the documentary “Made in USA: The East St. Louis Story,” “this was a city with neighborhoods, pretty parks, crowded schools, factory jobs and unions.” By 1960, Look Magazine had honored East St. Louis as an “All-America City.” [At the 2:15 mark in the “Made in USA” documentary, you can watch a parade the city held to celebrate this honor. It is incredible footage.] As the documentary explained, however, “what happened over the next ten, fifteen years would stun, anger and frustrate these citizens, as their hometown experienced a decline as incredible as its rise just a lifetime before.”

Specifically, industry began to leave the city. The large factories that had fueled the local economy were abandoned. Between 1960 and 1970, East St. Louis lost nearly 70 percent of its businesses. Unemployment increased at an alarming rate. Residents soon moved away. Between 1970 and 2000, the city lost 55 percent of its population. Crime rose. As the Federal Reserve Bank of St. Louis later described it, “East St. Louis and devastation became synonymous.”

It is against this historical backdrop that Mr. Peppers found himself in January 1971 protecting his Pizza Hut overnight with a shotgun. With people fleeing the area in droves and crime on the rise, it is perhaps easier to understand the circumstances that gave rise to the claim in Peppers. While Mr. Peppers’ insurance company rightfully may not have wanted to pay for bodily injury intentionally caused by its insured, the policyholder had an equal desire to prepare a defense that explained why he acted the way that he did in this time and place of devastating decline. For this reason, the Illinois Supreme Court agreed that Mr. Peppers was entitled to independent defense counsel, and in the process, created a doctrine that many insurance lawyers and professionals in and outside of Illinois still follow (and struggle with) forty years later.

Indeed, what the historical background of Maryland Casualty v. Peppers reveals is that many of the fundamental principles of insurance law that we take for granted every day, like the right to independent counsel, were not created in a vacuum. They are the result of real claims involving real people, and for good reason, as those principles continue and will continue to apply to real claims involving real people. We often read insurance law cases to quickly, pull the holding and apply it to a given claim. Sometimes we may draw better understanding of that holding if we take the time to consider more carefully the claim that gave rise to it.

Michael L. Young is a litigation attorney in the St. Louis office of HeplerBroom LLC with a primary emphasis in the practice of insurance coverage and bad faith. He represents insurance companies in Illinois and Missouri in complex insurance coverage matters at all stages of the claims process. Mr. Young also has advised insurers in drafting policy language and developing claims best practices. He has assisted insurer clients in recent legislative changes in insurance law in Missouri. He frequently presents and writes about these topics, including daily postings on LinkedIn. Mr. Young currently serves as the Vice-Chair of the Insurance Law Committee for the Illinois Association of Defense Trial Counsel (IDC). He has been named one of the Best Lawyers in America and a Missouri & Kansas Super Lawyer in Insurance Law. Mr. Young graduated from Washington University in St. Louis in 1999, summa cum laude, and from Saint Louis University School of Law in 2002, where he was the Valedictorian of his class.

|

| |

| |

| |

|

|

|

|

Vol. 7, Iss. 3

April 11, 2018

The Uber Accident: Insurance And Litigation Will Be Forever Changed

|

|

|

|

It was widely-reported, including with graphic video, that a pedestrian in Arizona was recently struck and killed by an Uber self-driving automobile in the testing stage. A secondary story to emerge from this tragedy has been questions about the overall safety of self-driving cars. Some companies have temporarily suspended the testing of their autonomous vehicles. Arizona put the brakes on allowing Uber to test such vehicles on public roads.

For the past several years predictions have abound that wide-spread use of self-driving automobiles is on the horizon. These vehicles promise numerous safety features. While automobile manufacturers long-ago conquered cruise control, and blind spot monitoring is an impressive innovation, I’m dubious that drivers will ever be playing Yahtzee on the way to work. In two centuries nobody has been able to eliminate train derailments. And they ride on a track, and usually with no other trains nearby.

Nonetheless, the talk of safe, self-driving automobiles, is now so serious that some insurance companies have warned investors, in securities filings, that there could be a decrease in demand for auto insurance. Personally, the idea of driverless cars just makes me want to buy more insurance.

But even if wide-spread adoption of driverless cars somehow becomes a reality, they will surely not be fool-proof. Given their technological complexity, that seems impossible. And unlike an inconsequential glitch with your office computer, here it will be control, alt and someone’s life is deleted. In addition to the technology not being without flaws, it will be many years before it is only driverless cars that are on the road. So there will still be plenty of opportunity for human factors to play a large part in automobile safety.

Admittedly I know nothing about the technology that supposedly makes driverless cars feasible and safe. But I do know something about lawyers. Just as day follows night, lawsuits follow car accidents. Wide-spread adoption of self-driving automobiles will dramatically alter the landscape for lawsuits following car crashes, and the insurance policies that fund the verdicts and settlements.

Right now, when there is an auto accident, it is rare to see the automobile manufacturer named as a defendant. Auto accidents are generally matters between the involved drivers. But when a self-driving automobile is involved, drivers will no longer be fighting over which one had the red light, but whose car is to blame.

However, if the car involved in the accident was designed not to have accidents, it is easy to see the automobile manufacturer, and the companies that made the component parts for the self-driving aspect, being named as a responsible party in lawsuits for countless automobile accidents. Accidents that are now simple, and quickly resolved, will become complex, drawn-out, technological fights between drivers and manufacturers over who’s to blame. Car crashes will go from one of the laws simpler problems to resolve to complex product liability litigation.

No matter how safe self-driving automobiles are, the manufacturers of automobiles, and their component parts, will still find themselves involved in enough cases to be at risk for serious financial consequences. They can expect to get to know their way around every courthouse in America.

And unlike at-fault drivers, who often-times have auto insurance policies with paltry limits, that is not likely to be the case for manufacturers of automobiles and their component parts. This is the plaintiff’s lawyers dream – a deep pocket for every automobile accident.

Manufacturers of cars and parts may shrug this off as something that they’ll pass on to their insurance companies. But insurers know something about how to put a price on risk, including their responsibility for the defense aspect of litigation. Given the claims frequency and severity, the manufacturers may find it cost prohibitive to go the insurance route. And if the solution is to build this risk factor into the price of the car, that would presumably make it more challenging for manufacturers to sell them.

Technological advances, no matter the convenience, quality of life or life-saving features that they provide, often-times come with unintended consequences. But when those consequences include lawyers, they can be particularly troublesome and expensive. Automobile manufacturers, who are racing to get to market with driverless cars, should be careful what they wish for.

|

|

| |

| |

| |

|

|

|

|

Vol. 7, Iss. 3

April 11, 2018

NJ MUST READ – No Surrender If Insurer Violates Merchants V. Eggleston

|

|

|

|

Those who handle coverage cases in New Jersey have long-known that, if an insurer retains counsel, and defends its insured under a reservation of rights, the insured must consent to such an arrangement. This rule dates back to the New Jersey Supreme Court’s landmark 1962 decision in Merchants Insurance Co. v. Eggleston.

New Jersey courts have imposed a simple sanction on insurers that fail to obtain their insured’s consent to being defended under a reservation of rights – loss of the insurer’s ability to assert an otherwise applicable defense to coverage.

Despite its significance, the consent issue in Eggleston has not generated many decisions in the past 50-plus years. This dearth has left open to discussion whether an insurer that defends its insured, under a reservation of rights, but without obtaining its insured’s consent, has automatically lost its coverage defenses -- or must the insured have been prejudiced by the lack of consent.

The New Jersey Appellate Division’s 2009 unpublished decision in Nazario v. Lobster House concluded that loss of coverage defenses was automatic, with prejudice suffered by the insured not being a consideration. The court was clear: “We find nothing in Eggleston or its progeny which suggests that the insured must prove actual prejudice to create coverage, or that the carrier may prove lack of prejudice to avoid coverage by estoppel, when a fully informed written consent is lacking. The control of the litigation without proper consent equates to creating the coverage without qualification under Eggleston.”

Notwithstanding Lobster House (and the Appellate Division’s 1967 decision in Sneed v. Concord Insurance Co.), the New Jersey Appellate Division just held, in a published opinion, that an insurer that defends its insured, under a reservation of rights, but without obtaining consent, is not automatically in boiling water.

Admittedly, while Northfield Insurance Company v. Ht. Hawley Insurance Company, No. A-1771-16T4 (N.J. Super. Ct. App. Div. Mar. 28, 2018) involves a unique scenario that played into the decision, the opinion still concludes that an insurer’s failure to follow Eggleston does not automatically lead to an insurer’s loss of coverage defenses.

The Empress Hotel, located near the ocean in Asbury Park, sustained roof damage during Superstorm Sandy. This caused water damage to the hotel’s interior. Prior to the storm, CDA Roofing Consultants had performed roof installation work on the hotel. Empress and its insurer, Mt. Hawley Insurance Co., filed suit against CDA and its subcontractor, alleging that CDA’s negligence enabled the damage to the roof to take place.

CDA’s liability insurer was Northfield. The insurer advised CDA that, for a host of reasons, it was disclaiming coverage for the Empress suit. However, Northfield stated that it was “willing” to provide CDA with a “courtesy defense,” subject to a reservation of rights. Northfield later commenced a suit against CDA, seeking a declaration that it had no duty to defend or indemnify CDA in the Empress suit.

Putting aside some procedural issues, Mt. Hawley and Empress argued, in the Northfield coverage action, that Northfield should be estopped from denying coverage for the claim against CDA, in Empress action, because Northfield violated Merchants v. Eggleston by failing to properly seek CDA’s consent to its control of the defense. The trial court agreed with Mt. Hawley and granted its motion for summary judgment.

The issue made its way to the New Jersey Appellate Division, which reversed the grant of summary judgment in favor of Mt. Hawley.

First the court addressed whether Northfield had complied with Eggleston by stating that it was “willing to provide” a courtesy defense. The court concluded that, at least for summary judgment purposes, it was possible that “CDA’s failure to decline that ostensible favor justifies a finding that CDA acquiesced in Northfield’s control of the defense of the underlying action. . . . [T]he statement that a ‘courtesy defense’ would be provided might plausibly be interpreted as an offer of a defense, and not as the insurer’s insistence on controlling the defense. And, if interpreted as an offer, CDA’s following silence could be interpreted as acquiescence in Northfield’s control of the defense; such a circumstance would not offend Eggleston or its progeny.”

This aspect of the opinion, involving a “willingness” to provide a “courtesy defense,” is unique. But it offers this take-away, as the court put it: rejection of “the argument that Eggleston permits avoidance of estoppel only if the insurer uses certain magic words in communicating with its insured.”

The more important aspect of the opinion is the court’s conclusion that, even if Northfield did not satisfy the Eggleston consent requirement, loss of its coverage defenses was not automatic. The court stated: “We reject Mt. Hawley’s argument and the motion judge’s determination that estoppel must always follow an insurer’s failure to fairly seek consent. Indeed, Eggleston hardly supports such a view because waiver instead of estoppel was found implicated there. Eggleston in no way suggests that estoppel immediately attaches when an insurer, while reserving its rights or declining coverage, assumes control of the defense without first obtaining the insured’s consent. On the other hand, we recognize that Sneed [v. Concord Ins. Co., N.J. App. Div. (1967)] would appear to have drawn such a conclusion; in fact, in Sneed, the panel held that ‘Eggleston adumbrates’ the conclusion that estoppel will automatically follow and ‘[p]rejudice to the insured will be assumed.’ We do not agree with that blanket statement.”

The court based its decision -- and recognizing that it was applying a summary judgment standard -- on two factors.

First, as a matter of law, estoppel precludes a party “from asserting rights which might perhaps have otherwise existed . . . as against another person, who has in good faith relied upon such conduct, and has been led thereby to change his position for the worse.”

Then, as matter of fact, looking at the reliance test, the court explained: “First, it has not been shown that CDA relied on what Northfield wrote and changed its position to its detriment. The factual record suggests that CDA was defunct when Northfield declined coverage and assumed CDA’s defense. Consequently, one might ask what CDA would have otherwise done if it had rejected Northfield’s ‘courtesy defense.’ It certainly did not appear to be prepared to defend itself; no doubt CDA would have defaulted if Northfield had not provided a defense, just as CDA defaulted in this declaratory judgment action. So, it is fair to conclude — at least for summary judgment purposes — that CDA did not adjust its conduct one way or another when advised by Northfield that it would provide a ‘courtesy defense.’ In short, the evidence is inconclusive if not lacking at this time as to whether CDA detrimentally relied.”

The court also concluded that there was no evidence to suggest that Northfield acted with an intention or expectation that its actions would be acted upon by the other party: “The ‘other party’ — CDA — wasn’t ‘acting’ at all; it was moribund if not completely defunct at the time. Whatever Northfield did or would do in defense of the underlying action was not likely to cause injury to CDA regardless of the outcome.”

Admittedly, that CDA was defunct made it easier for the court to conclude that CDA did not rely on Northfield’s actions and change its position to its detriment. Policyholders in future cases will no doubt raise that to distinguish their own Eggleston violation scenarios. Nonetheless, the decision is a significant one.

Complying with Eggleston is, of course, the best way for an insurer to proceed when retaining counsel and defending an insured under a reservation of rights. However, for insurers that fail to do so, an Asbury Park hotel teaches that it does not necessarily have to be no surrender.

|

|

| |

| |

| |

|

|

|

|

Vol. 7, Iss. 3

April 11, 2018

The Great Bad Faith Myth

|

|

|

|

Some policyholder counsel have a simple test for whether an insurer committed “bad faith”: anything done by the insurer short of exactly what he or she demanded. The policyholder lawyers in this camp would be well-served to read a state’s actual definition of bad faith. Any state will do. If so, they would see that, in real life, proving that an insurer acted in bad faith, especially when it comes to a claims decision, is a pretty tall order. Bad faith generally requires some pretty egregious conduct on the insurer’s part. But even if this ilk of policyholder lawyers saw this they probably still wouldn’t change their tactic.

It is not unlike a plaintiff’s attorney, with a simple negligence case, who opens up a thesaurus to the word “evil” when drafting a complaint. He or she just can’t help themselves from describing a wayward banana peel as having been the result of conduct that was malicious, wicked and depraved.

In any event, what these huff and puff policyholder counsel don’t understand, or can’t accept, or know, but pretend isn’t so, is that when it comes to an insurer’s claim denial, bad faith is very hard to prove. Even when a court determines that the insurer was flat out wrong, it is still very unlikely that the insurer will be found to have acted in bad faith. The various state standards, for proving bad faith, are just too high. As a result, simply being wrong in a claim denial is rarely bad faith by an insurer. [An insurer that fails to settle a claim, where there was a demand within limits, is a different kind of bad faith, and not what’s being addressed here.]

This reality was on display in Dominick’s Finer Foods v. Indiana Insurance Company, No. 11CH1535 (Ill. Ct. App. Mar. 1, 2018). In simple terms, the court held that the insurer’s claim denial was wrong. Nonetheless, the court had no trouble dismissing the insured’s bad faith claim.

At issue in Dominick’s, not just fine, but Finer Foods, was coverage for Dominick’s, for a claim brought by the estate of an individual, who was shot and killed in the parking lot outside Dominick’s in Chicago. Domininck’s sought coverage from a liability insurer, Netherlands Insurance Company. The insurer disclaimed coverage for a defense. Dominick’s, and others, reached a settlement in excess of $1 million and filed an action seeking a declaration of coverage and damages for the insurer’s alleged bad faith conduct. The trial court ruled for Netherlands. Dominick’s appealed.

Skipping some complexity, what matters for purposes here is this. Dominick’s was a tenant of the Kennedy Plaza Shopping Center. Dominick’s was an additional insured on a liability policy issued by Netherlands Insurance to Kennedy Plaza that provided as follows:

|

|

Such person or organization [Dominick’s] is an additional insured only with respect to liability arising out of:

a. Your [Kennedy Plaza] ongoing operations performed for that person or organization; or

b. Premises or facilities owned or used by you [Kennedy Plaza]. *** |

|

The allegations against Dominick’s boiled down to this: Dominick’s knew that there was criminal and gang activity going on near its store and failed to warn patrons and failed to provide adequate security.

Dominick’s argued that it was owed additional insured coverage because its liability was arising out of Kennedy Plaza’s operations performed for Dominick’s or the premises or facilities owned by Kennedy Plaza.

The court held that Dominick’s was entitled to coverage on the basis that “the premises-liability theory fell within the coverage language for ‘liability arising out of [the] premises.’ The sole basis for imposing a legal duty on Dominick’s under this premises-liability theory was its relationship to the ‘premises’—its status as the occupier of the property, on whom both the common law and the Premises Liability Act impose a duty of care. The ‘premises’ is thus directly and indispensably tied to the alleged legal duty on the part of Dominick’s in this case, and duty is a required element of its ultimate ‘liability’ to the plaintiffs in the Gallo litigation.”

The court rejected the insurer’s argument to the contrary, which the court described as a “floodgates argument.” As the insurer saw it, the court’s interpretation would lead to “nearly unlimited” coverage. For example, “‘Dominick’s might fire an employee in the parking lot,’ ‘might discriminate against a customer based on race or age’ there, or ‘might wrongfully use someone’s logo’ on the premises—and all of those acts, under this interpretation, would be covered under the policy.”

However, the court was not persuaded: “[T]hese examples provide the perfect frame of reference for why the interpretation we adopt is reasonable. In those examples given above, even if those events happened to occur on the ‘premises,’ the ‘liability’ of Dominick’s for those acts would have nothing whatsoever to do with the premises. A claim for wrongful termination would not base ‘liability’ on the premises at 3300 West Belmont Avenue but, rather, on the store’s status as an employer and its violation of some state or federal employment law. It would make no difference, from a ‘liability’ standpoint, whether a Dominick’s official fired the employee inside the store, in the parking lot, at a coffee shop down the street, by e-mail, or at a visit to the employee’s home.” (emphasis added).

The court also rejected the insurer’s argument that “the phrase ‘arising out of the premises’ in an insurance policy means that the loss occurred due to some defect in the premises,’ and because no such defect was alleged regarding the premises here, the complaint did not implicate coverage.”

So the insurer lost and it was obligated to provide coverage to Dominick’s for a defense and indemnity.

The opinion contains a lot more analysis of the “premises” issue, but I omitted it, as it is not relevant to the real point to be made here: despite being wrong on the coverage question, the court held that the insurer did not act in bad faith, which, under Illinois law, requires that the insurer’s conduct was “vexatious and unreasonable,” being based on a totality of the circumstances determination.

The court explained: “[Illinois Insurance Code] [S]ection 155 fees and penalties are not awarded simply because the insurer refuses to settle or was unsuccessful in litigation. Where there is a bona fide dispute concerning coverage, the assessment of costs and statutory sanctions is inappropriate, even if the court later rejects the insurer’s position. Though we have disagreed with Netherlands’s interpretation of the policy language at issue, we do not believe that its position was so unreasonable as to warrant damages under section 155. There is a difference between disagreeing with a party’s position and finding that position so untenable as to be unreasonable and evidence of bad faith. We have held that Netherlands’s position was too narrow to be the only reasonable construction of the policy, in light of the broad language ‘arising out of’ and the broad term ‘liability,’ but it does not follow that Netherlands’s position was, itself, unreasonable. The fact that an able and experienced trial judge agreed with Netherlands is further evidence that Netherlands's arguments and conduct do not warrant sanctions.” (emphasis added).

Knee-jerk bad faith policyholder counsel would be well-served to take note: an insurer’s position can be too narrow to be the only reasonable construction of a policy, but, not itself, unreasonable, to serve as evidence of bad faith. |

| |

|

|

|

|

Vol. 7, Iss. 3

April 11, 2018

The Continuous Trigger Has A Limit

|

|

|

|

We all know how the continuous trigger came to be and how it operates to potentially expand the number of policies that may be obligated to provide coverage. While the continuous trigger had its genesis in the context of asbestos and hazardous waste claims, for so-called “latent injuries,” the concept also forever altered the general mindset of insurance coverage analysis. Attempts to treat all kinds of claims -- even for non-latent injury – as “continuous” is now de rigueur. Policyholders these days take an “All the world’s a stage for the continuous trigger” approach to coverage whenever possible.

But despite policyholders’ best efforts, the continuous trigger has its limits, as demonstrated by Exel Direct v. Nautilus Ins. Co., No. 16-446 (S.D. Ohio Mar. 30, 2018). The facts here are very simple. In July 2006 a Sears dryer was installed in a customer’s home by a subcontractor of Exel Direct. The installation was incorrect and lead to lint accumulation. In 2014 the dryer caught fire and burned down the customer’s home as well as neighboring properties. State Farm insured the lost homes and brought a subrogation action against Exel Direct. Exel Direct sought coverage from Nautilus, which issued policies to it from 2004 to 2008.

The Nautilus commercial general liability policies provided coverage for “property damage” during the policy period. The fire took place in 2014. The last Nautilus policy was off the risk in 2008.

You can see where this is going….

Enter stage left -- the continuous trigger. Exel Direct argued that “the ‘property damage’ at issue is not the fire itself, but instead the improper installation of the dryer: ‘It is alleged that the contractor improperly installed the dryer and its venting, causing a gap that compromised the integrity, function and use of the dryer. From the installation forward, allegedly accumulating lint degraded the dryers function, and a fire ultimately resulted on April 30, 2014.”

While the court acknowledged that Ohio law recognized the concept of a continuous trigger, it concluded that it was not applicable to the claim at issue. In continuous trigger cases, the injury occurs during more than one policy period. But that was not the case here. The court explained: “[T]he damage to the dryer itself [the error in installing the dryer that led to an accumulation of lint] may have occurred continuously, including during the policy period, but the injuries that the homeowners alleged in the underlying case occurred in one fell swoop, well outside the policy period. Because the injuries alleged in the underlying cases did not occur during the policy period, they do not qualify as covered property damage under the policy, and Nautilus does not owe Exel a duty to defend or indemnify as a matter of law.”

Despite its conclusion, the court did not discount the possibility of the claim having implicated the continuous trigger: “[H]ad the underlying complaints asserted damage to the dryer, Nautilus may have been obligated to defend and indemnify as to the impairment of the dryer.”

“All the world’s a stage for the continuous trigger.”

|

|

| |

|

|

|

|

Vol. 7, Iss. 3

April 11, 2018

Viking Bump For Policyholders:

California Court Interprets New York Allocation Law As “All Sums”

|

|

|

|

In Polar-Mohr Maschinenvertriebsgesellschaft GMBH Co. KG v. Zurich, No. 17-1804 (N.D. Calif. March 15, 2018) – discussed above in “Trust Me: You Gotta See The Name Of This Insured In a Coverage Case” -- the California federal court was called upon to address whether “all sums” or “pro-rata” applied to Zurich’s obligation for an asbestos death caused by mesothelioma. At issue was a claim involving alleged asbestos exposures from 1964 to 1999, diagnosis/death in 2013-14 and a single Zurich primary policy in effect from 1984-85.

Zurich argued that pro-rata applied because, based on the express language of its policy, Zurich is “only responsible for liabilities arising out of bodily injuries that occurred during the policy period.” Polar-Mohr, the insured, countered that “the definition of ‘bodily injury’ acknowledges the policy’s continuing coverage for bodily injury claims,” which makes it “inconsistent with pro rata allocation.”

The applicable law was either NY or California. The court concluded that the law was the same in both states and adopted “all sums.” But here’s the rub. In doing so, the court addressed the New York Court of Appeals’s decision in In the Matter of Viking Pump, Inc., 27 N.Y.3d 244 (2016) and held that the Zurich policy’s definition of “bodily injury” as “bodily injury, sickness or disease sustained by any person which occurs during the policy period, including death at any time resulting therefrom” (emphasis added) was “precisely the type of language that the court in Viking Pump found inconsistent with the pro rata method of allocation.”

In reaching this decision, the court rejected Zurich’s argument that the phrase “including death at any time resulting therefrom” does not mandate “all sums” allocation. Such language, Zurich maintained, “does not signify that Zurich will provide coverage for bodily injuries that occur outside of the policy period but rather acknowledges that the policy will cover consequential damages, even those taking place after the policy period.”

The clear question that arises from the Polar-Mohr decision is this: Is the inclusion of the phrase “including death at any time resulting therefrom,” in the Zurich policy’s definition of “bodily injury,” really “precisely the type of language that the New York high court in Viking Pump found inconsistent with the pro rata method of allocation?”

There is only one way to find out – look at Viking Pump. The answer is clearly no. Viking Pump adopted “all sums” – and distinguished itself from New York’s pro-rata allocation rule as set out in Consol. Edison Co. of N.Y. v. Allstate Ins. Co., 98 N.Y.2d 208 (2002) -- on the basis that Viking Pump involved policies containing non-cumulation clauses or non-cumulation and prior insurance provisions. The Viking Pump court was clear on this, stating that “it would be inconsistent with the language of the non-cumulation clauses to use pro rata allocation here. Such policy provisions plainly contemplate that multiple successive insurance policies can indemnify the insured for the same loss or occurrence by acknowledging that a covered loss or occurrence may also [be] covered in whole or in part under any other excess [p]olicy issued to the [insured] prior to the inception date of the instant policy.”

It is hard to see how the phrase “including death at any time resulting therefrom,” in the Zurich policy’s definition of “bodily injury,” was “precisely the type of language that the court in Viking Pump found inconsistent with the pro rata method of allocation,” when the word “death” doesn’t even appear in the Viking Pump decision.

On one hand, the phrase “including death at any time resulting therefrom,” is a common one in the definition of “bodily injury.” It appears in the definition of “bodily injury” in ISO’s standard commercial general liability policy. On the other hand, an unpublished California federal court decision, interpreting New York law, is hardly a strong decision, yet alone binding precedent on any court. But despite that, unless the Ninth Circuit says otherwise – I do not know the possible appeal situation -- expect to see Polar-Mohr cited by policyholders in support of their argument that Viking Pump’s all sums approach to allocation goes beyond simply policies with non-cumulation clauses.

|

|

| |

|

|

|

|

| |

|

|

Never Have Truer Words Been Spoken In A Coverage Case

I recently had occasion to read Owens-Illinois, Inc. v. United Ins. Co., the New Jersey Supreme Court’s 1994 landmark decision on trigger and allocation in the long tail context. The last time I read it, start to finish, was probably twenty years ago. At that time, I am sure that I did not stop and consider one sentence from the opinion as I no doubt did many others. But this time around it was a much different story when I read Justice O’Hern’s description of the terms of a CGL policy’s insuring agreement (which the Justice quoted from Judge Landau in the New Jersey Appellate Division’s 1990 decision in Gottlieb v. Newark Ins. Co.): “Despite the relative familiarity of these concepts, the one hundred or so pertinent words in the coverage clause have spawned ‘a bewildering plethora of authority’ interpreting their meaning.” Twenty years later I paused and marveled at the incredible truth contained in this sentence.

Insurer Can Be Liable For Malpractice Of Its Staff Counsel

The last issue of Coverage Opinions addressed Kapral v. GEICO, No. 17-11511 (11th Cir. Jan. 23, 2018), where the federal appeals court held that an insured, under a GEICO automobile policy, could not maintain a malpractice action against the defense counsel retained by GEICO to defend him. The court cited two Florida decisions (the relevant state) holding that an insurer cannot be liable for the negligence of counsel that it retains for its insureds. Of note, the fact that the case at hand involved “staff counsel” did not dictate a different result. Now comes DiMuccio v. GEICO, No. 16-1307 (E.D. Calif. Mar. 19, 2018), where the court addressed the same question as Kapral and reached the opposite decision, in a case involving a defense provided for a motor vehicle accident: “GEICO argues it bears no responsibility for Plaintiffs’ contentions in this regard because they amount to attorney malpractice claims and cites authority to the effect that insurance carriers are not liable for the malpractice of trial counsel. See Merritt v. Reserve Ins. Co., 34 Cal. App. 3d 858, 880-82, 110 Cal. Rptr. 511 (1973). Merritt, however, was not decided in the face of facts like those confronted here, where Kevin Rodriguez was a salaried employee of GEICO and even described himself in correspondence to Pacific’s lawyer as ‘GEICO Staff Counsel.’ Under those facts, this Court can certainly not determine as a matter of law that Rodriguez was an independent counsel akin to the law firm hired by the carrier in Merritt.”

|

|

| |

|

|

|

| |

|

|

|

|

|

|

|

|

|