|

|

|

|

|

|

Vol. 7 - Issue 6

July 18, 2018

|

|

|

|

|

|

| |

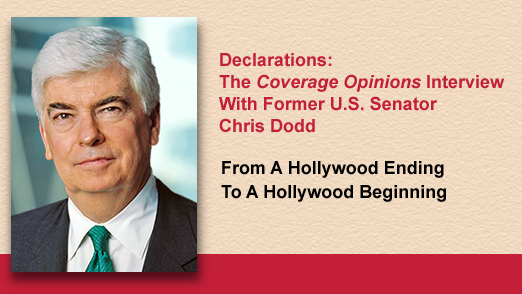

Chris Dodd welcomes me warmly into his office. We’re exchanging pleasantries. But my eyes are also darting between the array of unusual objects covering the walls. That’s a pen that President Obama used to sign the Affordable Care Act into law, the former Democratic Senator from Connecticut tells me, noticing my attention on it.

Dodd offers me a seat. It has wheels on it – I quickly realized. It’s the desk chair he used during his 30 years in the Senate. Dodd is sitting in his father’s Senate desk chair. What a coincidence, since it’s the first U.S. Senator Dodd about whom I have many questions. Before entering politics, Thomas Dodd had been an instrumental prosecutor in perhaps the most important trial in the nation’s history.

I’m visiting Chris Dodd at Arnold & Porter in Washington, where he recently joined. News of the retirement of Justice Anthony Kennedy broke just before my arrival. There is a computer screen over Dodd’s shoulder. CNN is on. The sound is muted but the images are all Kennedy. Dodd participated in the confirmation of numerous Supreme Court Justices. I’m two minutes in and on my second coincidence.

Dodd left the Senate in 2011. The 74-year-old is now back at a law firm for the first time since 1974. Fittingly, the man who hasn’t lost his Hollywood good looks just finished a seven-year tenure as Chairman and CEO of the Motion Picture Association of America. |

|

|

|

|

In his three decades in the Senate, Chris Dodd served as the principal author of such major legislation as Dodd-Frank, governing financial reform following the 2008 crisis, the Class Action Fairness Act of 2005, the Terrorism Risk and Insurance Act, the Private Securities Litigation Reform Act and the Family and Medical Leave Act.

But I haven’t taken the train to Washington to go over Chris Dodd’s Wikipedia page with him. I’m interested in things I can’t learn using Google (like the original name for the Dodd-Frank Bill; an obscure tidbit he shared). And I’m fascinated by the elder Senator Dodd’s significant role in causing a dozen Nazis to be executed for atrocities committed during World War II. Dodd is a gracious host, in no rush to shoo me out, even after an hour, and a gifted raconteur. His memory for names and dates from decades gone by–even down to the month–is remarkable.

My Old Kentucky Home

Chris Dodd graduated from the University of Louisville Law School in 1972. He was in a two-year program. “Way ahead of their time,” Dodd notes, referring to some chatter of late of cutting out the third year of legal scholastics. But how does the son of a Connecticut Senator end up in Kentucky, I wonder. “Primarily because I was the son of a Connecticut Senator.” Dodd was starting law school, he explains, at the same time that his father was up for re-election in a “very tough campaign.” The matriculating law student believed he’d be better-served avoiding that distraction. “That’s not to suggest to you, by the way, that I would have easily been admitted to Yale or the University of Connecticut,” Dodd says with a smile.

Dodd returned to Connecticut and went to work for a small law firm in New London. “My first trial was a guy who bought a boat with a hole in it,” Dodd says, laughing. But of his legal career, he says he “hardly got the seat warm.”

|

| |

|

| |

Return Of The Page

After two years of writing wills and representing local small businesses, a tightly held Congressional seat surprisingly opened up. Dodd was talked into running for it and won. So, at age, 30 the boat-hole litigator set sail for Washington.

Dodd was young, he acknowledges, to be in the House of Representatives. But the job was not unfamiliar. Pointing to his father’s extensive political experience, Dodd says he doesn’t “remember a time growing up that there wasn’t politics going on. So, I wasn’t sort of dropping into an arena without the knowledge.” And thanks to seeing his father’s wins and losses, Dodd says he didn’t arrive in Washington with a “glamorized version of politics.” He had, he tells me, “a deeper awareness [than] most 30 year olds running for public office about the vicissitudes of a political life.”

In 1981, just six years after his election to the House, Dodd began his first of five terms in the Senate. He jokes that he served with members who were there when he was a page in 1962. “I ended up sitting next to people who were snapping their fingers at me.”

The Influence Of The Nuremberg Trial

In 1945, Thomas Dodd, a 38-year-old Assistant U.S. Attorney, was tapped to serve on the United States prosecution team for the Nuremberg trial. Dodd spent fifteen months in Europe as a participant in the four-country joint effort to bring to justice 21 Germans for war crimes. He left his wife and five children back home in Connecticut, including fourteen-month old Christopher.

Dodd’s initial role was behind the scenes -- conducting pre-trial interviews of the defendants. He had hoped his job would end there as he was very keen to get back to Connecticut. But Dodd’s skills came to the attention of the lead prosecutor, Supreme Court Justice Robert Jackson. Dodd was called on to stay for the trial and Jackson elevated him to second in charge. In the end, all but three of the defendants were found guilty and twelve hanged.

[Justice Jackson wrote a dissenting opinion in Korematsu v. U.S., the Supreme Court’s 1944 opinion that upheld the constitutionality of Japanese internment camps during World War II. Korematsu was overruled the day before I’m sitting in Dodd’s office talking about Jackson. The coincidences are mounting.]

Understandably, Chris Dodd could have a bias in his praise of his father’s role in Nuremberg. But the German magazine, Der Spiegel, has none. It called Thomas Dodd “the star of the courtroom” with the gift of “being able to make the evidence sing.”

While in Europe, Dodd wrote hundreds of letters to his wife, Grace. They were thought to have been lost in a fire, until they were discovered, in 1990, in Chris Dodd’s sister’s basement. Dodd published many of them in “Letters from Nuremberg,” a 2007 book co-written with Lary Bloom.

The letters are remarkable on many levels. First and foremost, historical. The trial was plagued with challenges and its outcome was far from a foregone conclusion. Dodd’s letters offer a unique look at the prosecution efforts in real time, something the many post-verdict books can’t offer.

The letters are also deeply emotional, demonstrating a husband’s love for his wife. I tell Dodd there’s no way I can let my wife read the book. She’ll ask why I can’t write such affectionate letters. Dodd jokes that his first reaction upon reading the letters was “who’s this guy talking to my mother this way?” The letters are also prophetic. In one, Dodd mentions that, as he is not keeping a diary, the letters can serve as a record of what he sees and hears.

For Chris Dodd, his father’s letters are also very emotional. On September 1, 1945, Thomas Dodd wrote to his wife: “I suppose Christopher is growing rapidly. Did I understand correctly, from a brief sentence in one of your letters, that he is now walking?” When describing the importance of the trial: “Someday, the boys will point to it [Dodd had three sons at the time], I hope, and be proud and inspired by it. Perhaps they will be at the bar themselves and perhaps they will invoke this precedent and call upon the law we make here.” Dodd calls this a “powerful passage” in one the letters that he had “the hardest time reading.”

“Around our dining room table growing up,” Dodd tells me, “there was a lot of talk about Nuremberg.” And Dodd credits for his influence in Congress the commitment to the rule of law that his father’s work in Germany demonstrated. “We did something no one had ever done. We took this outrageous, corrupt and vicious government, responsible for the deaths of eleven million people, six million Jewish . . . and we’re going to give them a trial with a lawyer to present evidence. That was stunning . . . the magnitude of it.”

Thomas Dodd died while his son was in law school and never got to see that he followed in his path. “I’d like to think today, given the career over 36 years in the Congress, that he felt that I did continue his work in a way.”

Dodd gave high praise to his own wife, Jackie, for her instrumental role in bringing “Letters from Nuremberg” to fruition. As I was leaving, Dodd gave me an instruction: “Make sure you mention that.” A wise man.

Legislation Comes From A Story

I point to Dodd’s walls and the mementos of his legislative achievements that are household names. But what about one that Dodd cares deeply about that people may not know? The former member of the world’s most exclusive club does not need to think long. He tells me that his sister was blind from birth. It’s an issue personal to him. He worked to increase the number of people who can read Braille, telling me that only ten percent of the blind know Braille and it has the highest unemployment rate of any of the disabilities. He pushed publishers to timely release text books in Braille and lobbied to change the law that prevented the blind from working as Foreign Service Officers.

“When I passed the Help America Vote Act,” Dodd tells me, “I stuck a provision in there that made sure that a [blind person] would never have to vote with someone in the [voting booth]. It was insulting to my sister to have to have someone go in and know how she was voting.”

Dodd shared with me the story of a young girl who he met in church who was a quadriplegic. The girl’s mother expressed to him the challenges of working and having a child who needed constant care. “That’s Family and Medical Leave and that’s where it came from,” Dodd tells me. “A lot of legislation comes from a story.” The woman lived to be 23 and Dodd gave the eulogy at her funeral.

Dodd-Frank

The Dodd-Frank Wall Street Reform and Consumer Protection Act was passed in 2010, making dramatic changes to financial regulation following the 2008 crisis. The law owes its name to the significant efforts of Dodd, as Chair of the Senate Banking Committee and Representative Barney Frank, Chair of the House Financial Services Committee.

The Act, best known simply as Dodd-Frank, was of course on my agenda. But it is 2,000 pages and as dense as a New York subway train at rush hour. I gave up all hope of understanding it and simply prayed that Dodd didn’t ask me which provisions I found most interesting.

I joked with Dodd that every time he sees the name Dodd-Frank in print he must say to himself – “Hey that’s me.” Dodd opposed having his name on the law, he told me, voting against the motion made by a Pennsylvania Congressman to initially call it the Frank-Dodd Bill. “Barney said ‘you can’t do that, they’ll think it’s one person.’”

Dodd stresses to me that the law is designed to “minimize the next crisis. It doesn’t eliminate the next crisis. It just means you can manage it better so you don’t come on the brink of a total financial collapse.”

There have been recent efforts to roll back some of the law’s provisions. “Is it tough to pick up the paper and read that Dodd-Frank is being dismantled?” I ask Dodd about his namesake law. “It’s tough to read the stories because they really didn’t,” he says, chuckling. Dodd acknowledges that “any bill of that size and magnitude” is going to be subject to some changes. “The only perfect piece of legislation I ever saw was the Ten Commandments and we’re still debating those things 4,000 years later.”

“The recent legislation that was adopted is pretty minor,” Dodd characterizes the efforts. “There were a couple of things I didn’t like about it.” But with the profitability of banks today being historic in level, Dodd says he doesn’t “know what the complaint is. If the complaint is that they’re not making money, they’ll have a hard time convincing anyone who knows what they’re doing.”

Dodd then transitions into some technicalities of the Act and rattles off a long list of its major provisions that are still in place. He might as well be speaking to me in Chinese at this point. I need to get him off the subject quickly before he becomes the questioner.

Ironically, Dodd tells me that he spoke at the Central Bank of China and was presented with a copy of Dodd-Frank translated into Mandarin. He gets up, grabs a book from a shelf and opens it: “That’s Dodd-Frank in Mandarin.” And I thought I was the only one with that book.

The Hollywood Ending

I ask Dodd about gridlock in Washington. “There’s nothing quite like this moment,” he tells me. Asking about it in historical terms, Dodd describes the country as being “ripped apart” by the fight over the Affordable Care Act.

Dodd was instrumental in the passage of the healthcare law after becoming the Acting Chairman of the Health, Education, Labor and Pensions Committee in November 2008. Chairman, Senator Ted Kennedy, suffering from brain cancer, had been forced to pass the baton. Kennedy died in August 2009. Dodd and the Massachusetts Senator were very close friends for 30 years.

The healthcare bill passed in the Senate on Christmas Eve 2009. Dodd was heading home to Connecticut. But he made a stop at Arlington National Cemetery before the airport. He hadn’t yet visited Kennedy’s grave and chose this moment. Standing alone in the snow Dodd said to himself: “Do you want to do this for seven more years? And the answer was quicker than the question. I said ‘that’s enough.’ . . . I’ve never looked back.”

Hollywood And The Preordained Law Firm

How Dodd made the decision to quit the Senate is a Hollywood ending. And not long after, he began a seven-year tenure as Chairman and CEO of the Motion Picture Association of America – the trade association that represents the six major Hollywood film studios. The MPAA are also the folks who decide if a film should be rated G or NC-17 or somewhere in between. Dodd’s time at the helm included such challenges as competition from Netflix and Amazon, cyber-attacks and ever-present piracy.

But Dodd had no experience in the entertainment industry. So what was Disney CEO Bob Iger thinking when he recruited him? He must have been goofy. “The job is less about Hollywood than it is about representing the industry globally,” Dodd explains. “More than 70 percent of the revenues of the quote ‘Hollywood business’ come offshore.” People think “I was spending my time down there with George Clooney,” he says, laughing. In fact, he spent a “huge amount of time traveling” and built operations in Brussels and Asia.

Dodd gave me some good advice about the movie industry: the Golden Globes are more fun than attending the Academy Awards. I’ll keep that in mind.

Dodd joined Arnold & Porter Kaye Scholer at the start of this year, as Senior Counsel. He is working in such areas as legislative and foreign policy and financial services. The move feels preordained to him. One of the firm’s founders was Abe Fortas, who was a Yale Law School classmate of Dodd’s father’s. [Fortas would later join the U.S. Supreme Court.] And Dodd’s seat in the Senate had belonged to Abe Ribicoff before his retirement. Ribicoff then went to the Kaye Scholer firm in New York, which recently merged with Arnold & Porter.

Dodd touts the firm’s commitment to pro bono work -- saying that no other firm in the country does as much -- as well as the public service roles that many of its senior lawyers have held. “The pejorative today of this revolving door has discouraged this and I think to the detriment of the country.”

My time with Chris Dodd comes to an end and I’m packing up my things. He sums it all up very simply: “Life is good.” |

| |

[Elizabeth Vandenberg, a student at University of Iowa College of Law, assisted with this article.] |

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Vol. 7, Iss. 6

July 18, 2018

Game Of Drones: Court Finds Coverage When A Drone Sees Something Private

|

|

|

|

|

| |

So far it does not seem that drones have taken over the planet as promised, despite that they supposedly have a million and one uses. My Amazon packages are still delivered to my porch by a two-legged person – with a raucous welcome from the four-legged residents inside.

Nonetheless, predictions about the wide-spread use of drones has led to chatter about the availability of insurance coverage for injury and damage caused by a wayward drone. But it has mostly been limited to talk as there has been a dearth of decisions addressing these actual coverage issues. But those looking for guidance in this area now have one place to look -- the Rhode Island Superior Court’s recent decision in FBEye, Inc. v. Gumshoe Risk Retention Group.

The court in FBEye addressed the availability of coverage, under a commercial general liability policy, for an invasion of privacy caused by a drone that had a video camera attached to it. The coverage decision had its roots in a dispute between neighbors.

Tracy Nelson and Benjamin Marks had been next-door neighbors in East Greenwich, Rhode Island for fifteen years. And that’s about how many words they’d spoken to each other during that time. Marks was very private and a twelve-foot fence surrounded his yard. It was well in violation of the town’s current zoning code but had been grandfathered-in from an earlier time. Nelson often imagined that one day Marks would commit a heinous crime and Nelson would be on television telling the reporter than Marks was a quiet guy who kept to himself.

Nelson had spent 25 years as an FBI agent in Providence. He retired in 2012. But he missed the action. So in 2014 he started FBEye, Inc., a private investigation company. His assignments included such things as looking for dirt on client’s spouses, background checks for people doing on-line dating and assisting attorneys with accident investigations and criminal defense.

In 2017, Nelson purchased a drone and attached a video camera to it. He imagined that it could be useful in certain surveillance situations. Nelson’s first use of the drone was in his backyard to get familiar with its operation. In the course of doing so, the drone flew over Marks’s yard and videotaped what was behind his massive fence. Nelson was gob smacked by what he saw – a clothes line with numerous adult size super hero costumes hanging from it. There was one for Captain America, Spiderman, Green Lantern, Aqua Man, Bat Man and Flash. Nelson couldn’t imagine how Marks fit into the tights.

Unbeknownst to Nelson, Marks’s yard was under surveillance itself. Marks became aware that Nelson’s drone had videotaped Marks’s yard. Marks went ballistic over Nelson’s actions as the long-time secret identity of six super heroes had now been revealed. Marks filed suit, seeking damages for invasion of privacy and demanding that the videotape be destroyed.

Nelson sought coverage for the suit from Gumshoe Risk Retention Group, an organization providing insurance for detective agencies. Gumshoe had issued a Private Eye General Liability policy to FBEye, Inc. Gumshoe provided a defense to Nelson. However, it was under a reservation of rights. The insurer maintained that, while the policy provided “personal and advertising injury” coverage for invasion of privacy, the necessary requirement of oral or written publication of material had not been satisfied. As Gumshoe RRG saw it, the videotape of Marks’s backyard had not been publicized to anyone.

With Gumshoe’s heels dug in, and Marks’s threats mounting, Nelson settled the Marks action for $17,000 and then filed suit against Gumshoe seeking recovery of the settlement payment. Nelson and Gumshoe agreed to stipulated facts and filed cross motions for summary judgment.

The court in FBEye, Inc. v. Gumshoe Risk Retention Group, No. 17-2234 (R.I. Sup. Ct., Kent Cty., June 28, 2018) held that the Gumshoe policy afforded coverage for Nelson’s payment to settle the Marks dispute.

The court was not convinced by Gumshoe’s “no publication” argument. As the court saw it, the video images had been published to Nelson. Here’s the crazy way how. Because the drone was doing, what would have been the job of a Gumshoe employee, the court treated the drone as a de facto employee of Gumshoe. Therefore, there had been a publication of the video imagines from the drone to Nelson.

The court was not unmindful that its reasoning was unique. However, for support, it turned to Judge Cardozo, who famously discussed the need for the law to evolve with the times: “Precedents drawn from the days of travel by stagecoach do not fit the conditions of travel to-day.” MacPherson v. Buick Motor Co., 217 N.Y. 382 (1916).

|

That’s my time. I’m Randy Spencer. Contact Randy Spencer at

Randy.Spencer@coverageopinions.info |

|

| |

|

| |

|

|

|

|

Vol. 7, Iss. 6

July 18, 2018

Elvis Presley Enterprises, Inc. Makes A Wonderful Contribution To Coverage Opinions

|

|

|

|

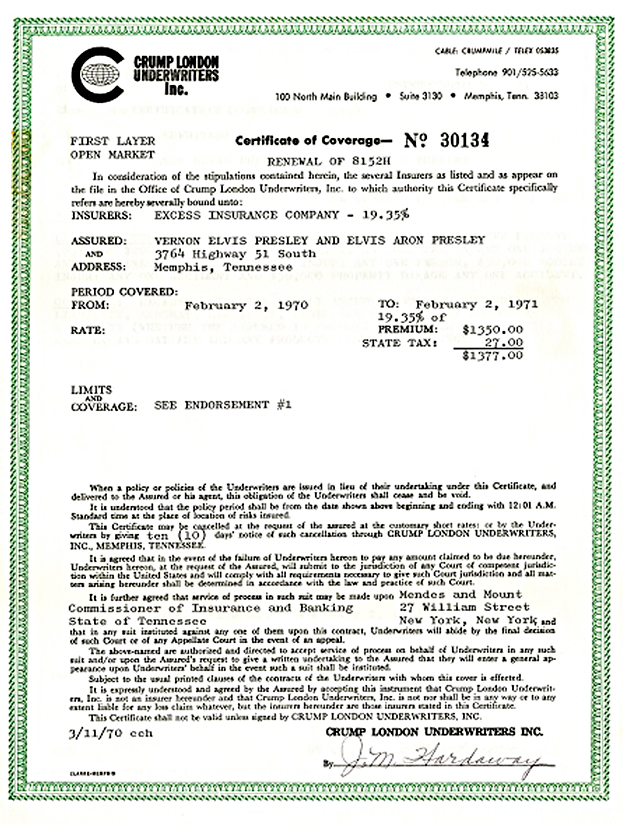

In the last issue of Coverage Opinions I mentioned the shock, during a recent visit to Graceland, of seeing Elvis’s parents’ homeowner’s policy on display. Issued by Camden Fire Insurance Company in 1947, the policy covered the Presley residence in Tupelo, Mississippi. Elvis was eleven years old at the time.

While I was very excited to see that policy, and share a picture of it in the last issue of CO, it also left me with an unsatisfied feeling. What about a picture of a policy covering the Graceland mansion itself? And not now, but back in the day when Elvis called it home and was hanging out in the Jungle Room. [Google that if you need to.] Now that would be the holy grail for Elvis Insurance fans. So I contacted Graceland and asked if they could provide me with such a gem. Of course the request seemed a longshot. Do they even have such a policy? And if they did would they really send a picture of it to me. Actually, and more importantly, would they even think my request was serious? I think they would. No one could not possibly make it up.

Well what a wonderful surprise it was when Graceland contacted me to say that it had found a 1970 policy, issued to Elvis at his Graceland address [3764 Highway 51 South, before it became 3764 Elvis Presley Boulevard.] And they’d be happy to let me use it for Coverage Opinions, no charge, if I signed a licensing agreement.

[As an added bonus, seeing an agreement containing these words was surreal: “This agreement is entered into 6/22/2018, by and between Randy J. Maniloff as agent for Coverage Opinions, digital publications, hereinafter referred to as “Agent” and Graceland/ Elvis Presley Enterprises, Inc., hereinafter referred to as “Graceland.” Me, an agent for Elvis Presley Enterprises, Inc. That got me all shook up!]

A king size thank you to Elvis Presley Enterprises, Inc. for kindly letting me share this picture with CO readers. I can’t tell exactly what it covers but it looks like it’s part of an excess policy of some type.

[You’ll see that the policy was issued to Elvis Aron Presley. On Elvis’s grave marker his name is displayed as Elvis Aaron Presley. Whether Elvis’s middle name was Aron or Aaron has been the subject of much discussion and involves some fascinating circumstances. If you Google it you’ll find some interesting articles on the subject.]

|

|

|

[Image courtesy of Graceland Archives.] |

| |

| |

|

|

|

| |

|

Vol. 7, Iss. 6

July 18, 2018

Hot Dog: The Wall Street Journal Published My Op-Ed

|

|

|

|

Some people are qualified to write op-eds for The Wall Street Journal on trade issues. Others tackle economic policy, politics or financial regulation. My op-ed, published in the June 27th Wall Street Journal, addressed the legal issues surrounding flying hotdogs caused by people in furry costumes. I know my limitations.

Here’s the backstory. Long-time readers of Coverage Opinions know that one of my all-time favorite cases is Coomer v. Kansas City Royals Baseball Club. The Kansas City Royals’s mascot, Sluggerr, an adorable furry lion, while standing on a dugout, tossed a hotdog – behind his back – into the stands. This was part of Sluggerrr’s between-innings hotdog launch. Unfortunately for Royals fan John Coomer, he chose the wrong moment to look at the scoreboard. The hotdog hit him in the eye. Coomer suffered a detached retina and needed eye surgeries. Litigation ensued.

In general terms, the issue at the heart of the case was this: Spectators at baseball games, seeking damages for injuries sustained by a foul ball, have a very difficult time recovering from the stadium operator. Courts, nearly across the board, have held that a baseball stadium operator is not liable for a foul ball injury as long as it screens the most dangerous part of the stadium and provides screened seats to as many spectators as may reasonably be expected to request them. Sluggerrr’s case raised the question whether this so-called “baseball rule” applies to an injury caused by a mascot.

Putting aside the details of a few years of litigation, the case made it all the way to the Missouri Supreme Court. In 2014 the high court of the Show Me State concluded that flying baseballs are not the same as flying hotdogs: “[I]f Coomer was injured by a risk that is an inherent part of watching the Royals play baseball, the team had no duty to protect him and cannot be liable for his injuries. But, if Coomer’s injury resulted from a risk that is not an inherent part of watching baseball in person—or if the negligence of the Royals altered or increased one of these inherent risks and caused Coomer’s injury—the jury is entitled to hold the Royals liable for such negligence[.]”

With that test set out, the court’s task was to answer whether being injured by a Sluggerrr-tossed hot dog was an “inherent risk” – which means involving the constitution or essential character -- of watching a Royals game in person. The court concluded that it is not. So Coomer could get his day in court. In a 2015 trial, the jury concluded that Sluggerrr was not at fault and neither was Mr. Coomer for looking at the scoreboard at the wrong time.

When it was reported not long ago that my beloved Phillie Phanatic’s between-innings hotdog launch injured a fan, when a frankfurter hit her in the face, I immediately put pen to paper and shipped off an op-ed submission to The Wall Street Journal. With the Sluggerrr case on the books, the Phanatic situation raised important legal issues – just as much as trade, economic policy, politics and financial regulation and all those other issues that appear on the paper’s opinion page. The world needed to know about this.

Hot dog – The Wall Street Journal published my effort. I hope you’ll check it out here:

http://www.coverageopinions.info/FlyingHotDogs.pdf

|

|

| |

Sluggerrr and the Phanatic doing legal research |

| |

Speaking of the Phillie Phanatic, he is clearly the smartest mascot in sports. |

| |

|

| |

| |

| |

|

|

|

|

Vol. 7, Iss. 6

July 18, 2018

Insurance Caption Contest

Win A Copy Of Insurance Key Issues

|

|

|

|

|

| |

| |

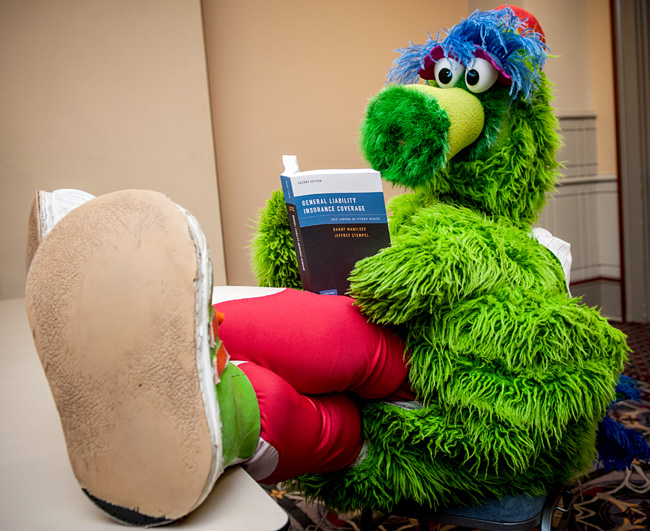

I love a good caption contest. Send me an insurance or insurance coverage related caption, thought bubble or speech bubble for this picture:

|

|

|

Deadline to enter: July 27. No limit on the number of entries.

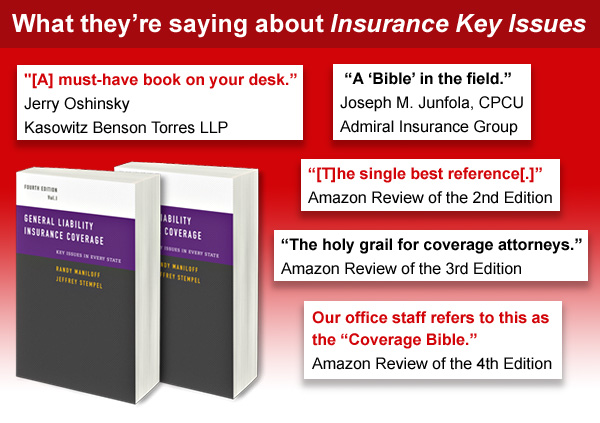

The best two will each receive a copy of the 4th Edition of Insurance Key Issues. |

| |

Check out the Sample Pages to see what Key Issues is all about: |

| |

|

| |

[Coverage Opinions Pen Update: I have received a new order of Coverage Opinions pens and they have been sent to many of the entrants of the Insurance Haiku Contest. If you have not yet received a pen, it is getting close. Thanks for your patience. I doubt I’ll do this get a pen if you enter the contest thing again. It seemed like a good idea at the time -- when I expected ten entries.] |

| |

| |

|

|

|

|

Vol. 7, Iss. 6

July 18, 2018

Insurance Key Issues: A Work Of Art

If The Old Masters Had Handled Liability Claims

|

|

|

|

|

|

|

|

|

| |

|

| |

|

| |

| |

|

|

|

|

Vol. 7, Iss. 6

July 18, 2018

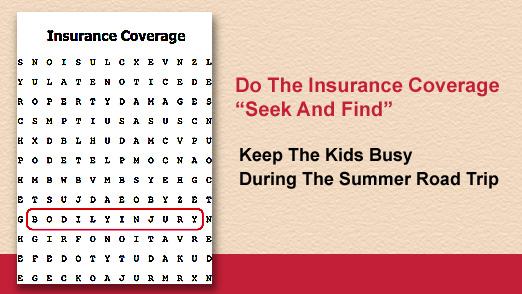

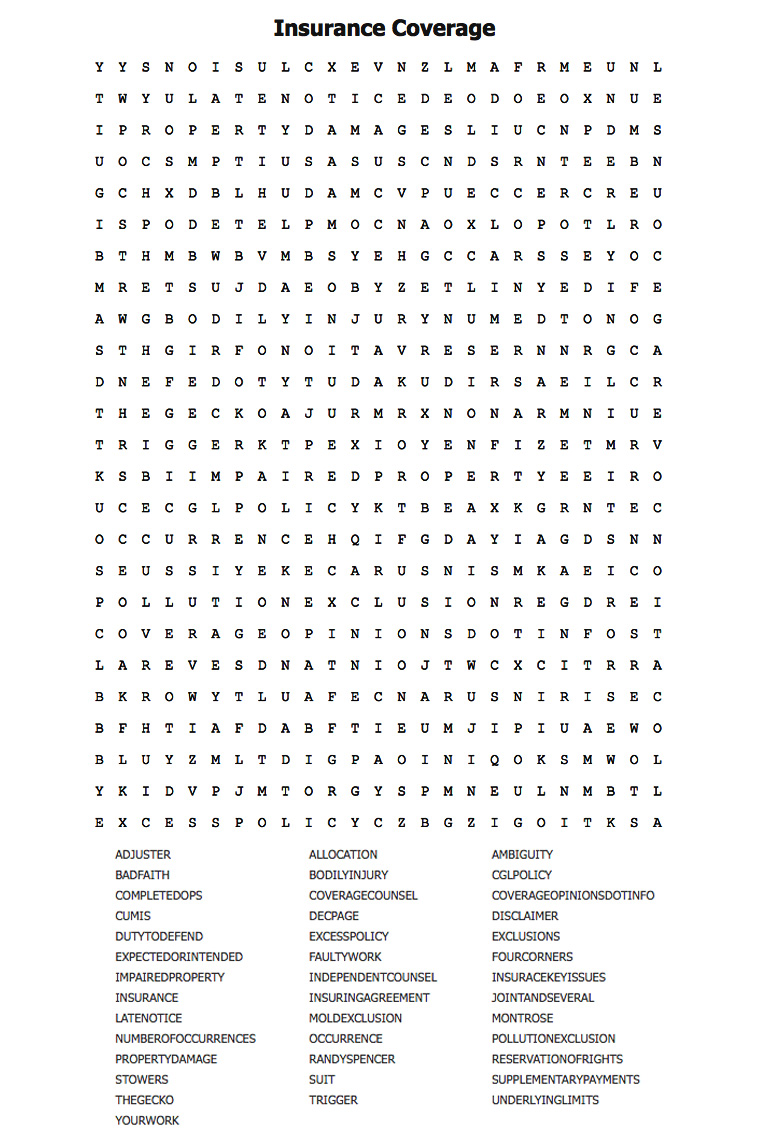

Do The Insurance Coverage “Seek And Find”

Keep The Kids Busy During The Summer Road Trip

|

|

|

|

I have no idea how it took me six years to think of this – an Insurance Coverage “Seek and Find.” And it’s just in time for your summer road trip. It’ll keep the kids occupied for hours in the back of the car. They’ll be so entertained by the Insurance Coverage “Seek and Find” that they won’t ask are we there yet?

|

|

|

|

| |

| |

|

|

|

| |

|

Vol. 7, Iss. 6

July 18, 2018

World Cup Special: Getting Hit By A Soccer Ball At A Professional Match

|

|

|

|

On these pages over the years I have addressed whether fans hit by baseballs, golf balls and hot dogs, while attending professional sporting events, can recover for their injuries. The legal issues are fascinating and of critical importance and the results are mixed. [They’ll probably asked Judge Kavanaugh his views on the subject at his Senate Confirmation hearing for the Supreme Court.]

The World Cup just ended. Congratulations to France. Much as I tried, I just couldn’t get excited about the World Cup without the United States participating.

In any event, in honor of the World Cup, I tackle here whether a spectator, injured by a soccer ball at a professional match, can recover for his or her injuries. Yes, such a case really exists, which is surprising since more people would watch the test pattern on the NFL Network than attend a soccer match.

Allred v. Capital Area Soccer League, No. COA07-647 (N.C. Ct. App. Dec. 16, 2008) addressed whether Teresa Allred could recover for injuries sustained while attending a professional women’s soccer match at State Capital Soccer Park in Cary, North Carolina. Allred was in the stands, behind one of the goals, when a ball sailed over the goal and struck her in the head. The incident took place during pre-game warm-ups, when many balls are hit toward the goal in a relatively short period of time. Allred sustained substantial head injuries.

Allred filed suit against Capital Area Soccer League, Inc. alleging that it was “negligent in: (1) failing to warn patrons of the risk of being struck by a soccer ball leaving the field of play; (2) failing to provide a safe environment for patrons; and (3) failing to install protective netting behind the goals to protect spectators.”

The trial court granted the defendant’s motion to dismiss. That the case was dismissed, at the pleadings stage, had much to do with the decision of the North Carolina Court of Appeals.

Not surprisingly, with a dearth of case law addressing soccer ball spectator injuries, the court turned for guidance to the abundant case law involving spectators injured by baseballs. At the outset, the court noted that North Carolina cases have uniformly been decided against the spectator, either because the stadium operator was not negligent or the spectator assumed the risk of being hit by a baseball.

The opinion has a lot to say about the duty of a stadium operator to keep spectators safe, as well as a plaintiff’s assumption of the risk of being injured. With those lessons in mind, the court turned to the matter at hand and reversed the trial court’s decision granting the defendant’s motion to dismiss. However, the decision is a far cry from finding the defendant liable. The court was clearly focused on the appropriateness of a dismissal at such an early stage.

Addressing the defendant’s negligence, the court noted that it owed to plaintiff a duty of reasonable care and that defendant had breached this duty based on the allegations that it failed to warn of the risk of being struck by a soccer ball, provide a safe environment for spectators and install protective netting behind the goals.

However, there was more to it: “The defendants’ duty to warn is qualified to the extent that the danger is known or so obvious that the plaintiff should have been aware of it. The question thus becomes whether plaintiffs’ complaint contains allegations which affirmatively establish actual or constructive knowledge, e.g., that the danger was either known to the plaintiff or so open and obvious that it should have been known to the plaintiff. We hold that it does not. Regarding actual knowledge, plaintiffs’ complaint specifically alleged that plaintiff ‘had no knowledge or underlying information that there was a significant risk of being struck by a soccer ball when attending such events at this facility.’ We hold that this allegation is sufficient to withstand defendants’ Rule 12(b)(6) motion on the basis of plaintiff's actual knowledge.”

But looking into its crystal ball, to a later point in the case, the court foreshadowed that the outcome may be different: “[W]hile plaintiffs’ allegation of no knowledge of the danger based on not having been to an event at this particular stadium is sufficient to withstand a motion to dismiss at this stage of the proceedings, it may not be sufficient to withstand a motion for summary judgment or a motion to dismiss at trial. Whether the plaintiff had knowledge of the danger is not limited to her experience at this particular stadium, but would encompass her knowledge of soccer in general, and of the sport derived from attendance at other venues.”

The specific issue of protective netting was disposed of easily: “Plaintiffs contend that defendants were negligent in failing to provide protective netting behind the soccer goals. It is clear from the baseball cases that the owner of a sports facility is not required to provide screening for all seats, only a portion of the seats. While the fact of some screening would bar recovery, plaintiffs’ complaint does not affirmatively disclose whether there was any protective screening at State Capital Soccer Park.”

Again, the court’s decision was clearly tied to the appropriateness of the trial court’s dismissal at the 12(b)(6) stage, which, the court noted, should be rare in a negligence claim. Indeed, the court observed that “[a] review of the cases dealing with spectator injuries at sporting events reveals that the overwhelming number of these cases are resolved at the summary judgment or trial stage of the proceedings.”

Based on the court’s pronouncements, I get the sense that, despite the plaintiff wining this battle, she was going to have an uphill climb to recover. So what happened? There are no additional opinions in the case on Lexis. I reached out to the lawyer for Teresa Allred and he informed me that the case was the subject of a confidential settlement after the appeals court decision.

|

|

|

|

|

|

|

Vol. 7, Iss. 6

July 18, 2018

Congratulations Dan Abrams – CO Interviewee’s New Book Makes NYT List And His Show Hits #1

|

|

|

|

The last issue of Coverage Opinions featured my interview with Dan Abrams, ABC News’s chief legal analyst. I spoke with Dan about his many projects, including his just-released book -- Lincoln’s Last Trial – The Murder Case That Propelled Him to the Presidency. The book offers a fascinating study of Lincoln’s 24-year career as a lawyer. Its centerpiece is a detailed account of Lincoln’s defense, just fourteen months before his 1860 election as President, of a man accused of stabbing another to death. The text has its genesis in a hand-written transcript of the trial -- discovered in 1989, wrapped in a ribbon, in a mouse-chewed shoe box in a garage. This rare find enabled Dan and his co-author to uniquely showcase Lincoln’s courtroom presence.

Congratulations to Dan on Lincoln’s Last Trial spending a few weeks on The New York Times Bestseller list!

Dan Abrams also hosts “Live PD” on Friday and Saturday nights on A&E. The show places its viewers into the passenger seats of police cars in several urban and rural cities, offering a real-time look at the work of law enforcement. Viewers witness live police stops. Needless to say, there is no predictability of what each one may bring.

On more than one occasion lately, “Live PD” has been the #1 rated show on cable television. Congratulations Dan!

|

|

|

|

|

|

|

Vol. 7, Iss. 6

July 18, 2018

SCOTUS Nominee, Judge Brett Kavanaugh, Has Addressed Number Of Claims

Using Five Distinct Rationales To Find For Policyholder

|

|

|

|

Coverage litigation is an infrequent subject before the D.C. Circuit. So it was not surprising that, even with his twelve years on this court, I could locate only one opinion authored by SCOTUS nominee, Judge Brett Kavanaugh, on the subject. Of course, since coverage cases do not get to the U.S. high court, looking into how Judge Kavanaugh has addressed such issues could be considered an impractical use of one’s time. Like learning how to ice fish in Arizona. But I was curious.

In the event that “number of claims,” for purposes of limits, is a litmus test issue for any Senators who will be voting on Judge Kavanaugh’s nomination, they will no doubt be scrutinizing his 2008 opinion in Essex Ins. Co. v. Doe, 511 F.3d 198 (D.C. Cir. 2008). And there’s a lot to examine there. Despite it being a brief opinion, Judge Kavanaugh used five distinct rationales to find in favor of the policyholder. I guess when you write just one opinion in a coverage case in twelve years you need to make the most of it.

Doe involved the extent of coverage for Associates for Renewal in Education, Inc. (A.R.E.), a children’s residential facility in Washington, D.C. John Doe, age 7, a resident, was sexually assaulted on four occasions, by four different older boys. Doe and A.R.E. ultimately settled a lawsuit. A.R.E. assigned to Doe its rights under a liability policy issued by Essex Insurance Company.

At issue before the D.C. Circuit was the number of claims. The policy contained a sublimit endorsement providing coverage for sexual abuse claims alleging negligent supervision. The coverage provided an “each claim limit” of $100,000 and an “aggregate limit” of $300,000 per year. The policy stated: “The sublimit of liability shown in this endorsement is the most [Essex] will pay for all damages including investigation and defense because of injury arising out of any one claim for sexual abuse and/or misconduct.” The policy defined the term “occurrence” to mean “an accident” and it was not disputed that there were four occurrences - one for each time Doe was assaulted. However, the policy did not define the term “claim” for purposes of the $100,000 “each claim” limit. Thus, the issue was whether there was one claim or four claims, when a sexual abuse victim makes a single demand for compensation for four occurrences.

Essex argued that Doe had only one “claim,” for the four occurrences, because he submitted only one demand for compensation. Doe argued that he had four “claims” because he was sexually assaulted on four different occasions.

Judge Kavanaugh found in favor of Doe, i.e., four claims (so up to the $300,000 aggregate was owed, less defense costs, as he also held that the endorsement was eroding). In addition to looking at some limited case law that favored Doe, Kavanaugh noted that the policy “tethers the term ‘claim’ to the term ‘occurrence’ and appears to establish a one-to-one relationship between (i) an occurrence causing injury to a third party and (ii) that third party’s ensuing claim against A.R.E.”

Kavanaugh needed little effort to reject Essex’s argument that the term “claim” means “the actual demand for money by the third-party claimant against A.R.E., regardless of how many occurrences the claimant alleges in the demand. But even apart from the contract’s linkage of claims and occurrences,” Kavanaugh stated, “Essex’s interpretation is illogical. First of all, it seems highly unlikely that a rational insurer or rational insured party would allow insurance liability coverage -- in a situation where a single third party suffers injuries caused by multiple occurrences -- to vary dramatically based solely on whether the injured third party happens to make (i) one summary demand against the insured A.R.E. or (ii) multiple demands against the insured A.R.E. Moreover, contrary to the logical implication of Essex’s argument, in a case with one sexual assault occurrence and one victim, A.R.E. obviously could not seek coverage from Essex for multiple claims simply because the victim sent multiple demand letters to A.R.E. For those reasons, we are not persuaded by Essex’s argument that the number of claims depends on the number of demand letters sent by the victim rather than on the number of occurrences.”

Kavanaugh added more reasons to find for Doe. Essex is “well aware how to limit [its] coverage for sexual abuse claims made against an insured. It could have used a $100,000 “each-injured-party limit” for coverage of sexual abuse claims.” Lastly, while Kavanaugh found the policy to be unambiguous, even if were ambiguous, D.C. law requires that it be construed against the insurer.

In one brief decision, Judge Kavanaugh used five rationales to find in favor of the policyholder – case law; policy language; reasonable expectations (without using that term); insurer being more sophisticated than the insured; and contra proferentem. Based on this, it seems he would give a thorough examination to any coverage case that came before the Supreme Court, which, of course, has less chance of happening than going ice fishing in Arizona.

|

|

|

|

|

|

|

Vol. 7, Iss. 6

July 18, 2018

Coverage For Invasion Of Privacy – But With No “Publication”

|

|

|

|

Commercial General Liability policies generally offer coverage for invasion of privacy committed by an insured. The standard ISO CGL policy includes, as a defined “personal and advertising injury” offense, the following: “[o]ral or written publication, in any manner, of material that violates a person’s right of privacy.”

However, while the policy affords coverage for violation of a person’s right of privacy, there are certain express qualifications – the privacy invasion must be on account of oral or written publication of material.

But, in Harleysville Preferred Ins. Co. v. Rams Head Savage Mill, LLC, No. 2409 (Md. Ct. Spec. App. June 28, 2018), the court concluded that coverage was owed for invasion of privacy without the happening of a publication of material. In fact, coverage was owed for invasion of privacy under a policy provision that didn’t even have the word privacy in it. [In actual fact, coverage was ultimately precluded based on a criminal act exclusion, but that does not negate the court’s decision regarding the availability of coverage for invasion of privacy.]

Rams Head is an interesting decision. A patron of the Rams Head Tavern was using a single-occupancy women’s restroom when a portable camera fell onto the floor from underneath the sink, close to the toilet. The culprit was determined to be Kyle Muehlhauser, the tavern’s general manager, who pleaded guilty to conducting video surveillance with prurient intent.

Class actions were filed by woman who alleged a variety of causes action, including intrusion of seclusion, and maintained that, as a result of the conduct of Mr. Muehlhauser and Rams Head, they suffered severe humiliation, violation, anxiety, loss of dignity, emotional distress, and the like.

Rams Head, during the two-plus years of surreptitious recording, was insured under three CGL policies issued by Harleysville. Putting aside some issues not relevant here, before the Maryland appeals court was whether coverage was owed under the policies’ “personal and advertising injury” coverage part.

In particular, the court focused on this aspect of the definition: “wrongful eviction from, wrongful entry into, or invasion of the right of private occupancy of a room, dwelling or premises that a person occupies, committed by or on behalf of its owner, landlord or lessor.” [The court did not address whether there was a “personal and advertising injury” on the basis of an “[o]ral or written publication, in any manner, of material that violates a person’s right of privacy.” This is seemingly on the basis that there was no publication of any recordings made.]

For various reasons, the court held that this aspect of the definition of “personal and advertising injury” was satisfied. First, the court had little trouble concluding that the woman were subjected to an invasion of the right of private occupancy of a room. Occupy, the court concluded, includes the temporary possession of a restroom. The phrase “right of private occupancy” includes the right of an individual who is occupying a single-occupancy restroom in a restaurant or tavern for its intended purpose to do so in private. And the court didn’t exactly go out on a limb in concluding that the video surveillance of such activities constitutes an “invasion” of that right.

The real battleground coverage issue was whether the invasion of the right of private occupancy was of a room, dwelling or premises that a person occupies. As Harleysville saw it, “invasion of the right of private occupancy of a room” does not appear alone in the policy. Thus, the phrase must be interpreted in its context and, here, it appears with two other phrases: “wrongful eviction from” and “wrongful entry into.” Each of these phrases, so Harleysville argued, requires the claimant to allege that they had a possessory interest in the property at issue.

But the court was not convinced, as Harleysville argued, that “right of private occupancy” in this coverage provision, requires “proof of a possessory interest in real property that is the subject of interference by its owner, typically in cases involving the dispossession of a tenant.”

The court based its conclusion on several reasons, including the grammatical structure of the policy language: “We also find it notable that ‘invasion of the right of private occupancy’ is not preceded by the word ‘other,’ which is a standard grammatical cue that a term is meant to encompass what came before it.”

There are other issues in the case and coverage was ultimately precluded based on a criminal act exclusion. But Rams Head is an interesting privacy decision – albeit involving a not-occurring-everyday set of facts.

|

|

|

|

|

|

|

Vol. 7, Iss. 6

July 18, 2018

Number of Claims: 3 Or 636?

|

|

|

|

In the world of insurance coverage, the word “claim” is one of the most frequently spoken. It is used by an injured party to describe its pursuit of relief against an insured-tortfeasor. The insured-tortfeasor then turns around and uses the term claim to describe its pursuit of coverage, from its insurer, for the claim being made against it by the injured party.

But, as the court in ProBuilders Specialty Ins. Co. v. Yarbrough Plastering, Inc., No. 16-16952 (9th Cir. June 25, 2018) demonstrated, the term “claim,” despite its lack of controversy when used in conversation, is not immune from disputes when it appears in an insurance policy. This result led to a significant exposure for an insurer. And one that it no doubt believed was not owed, based on its understanding of what’s a “claim.”

Lenox Homes hired Yarbrough Plastering to perform stucco and drywall work on several large residential developments in Bakersfield, California. Numerous homeowners sued Lenox for construction defects. It was the manner of these suits that gave way to a coverage dispute.

Specifically, 636 homeowners filed three separate lawsuits against Lenox in state court. Lenox filed three cross-complaints for indemnity against its subcontractors, including Yarbrough. Yarborough sought coverage from its insurer, ProBuilders. ProBuilders settled the claims against Yarbrough for $1.4 million—about $2,000 per home. ProBuilders filed a declaratory judgment action, seeking reimbursement of the entire settlement amount from Yarbrough. “ProBuilders alleges that, under the ‘per-claim’ deductible policies, Yarbrough owes a separate deductible for each of the 636 homes at issue in the three homeowners’ suits. Because the $2,000 per-home settlement falls below the deductible—either $4,000 or $10,000, depending on the applicable policy—ProBuilders says Yarbrough is obligated to reimburse it for the entire $1.4 million settlement.”

Good news for ProBuilders – the court concluded that its interpretation of the “per claim” deductible was reasonable. Bad news for ProBuilders – that wasn’t the only reasonable interpretation: “We agree with Yarbrough and the district court that only three deductibles are due—one corresponding to each of ProBuilders’ cross-complaints for indemnity. The policies specify that a separate deductible is due for each claim and contemplate that multiple claims can be joined in a suit.”

The downfall for ProBuilders was that the policies did not specify whether the operative “claim,” for purposes of the “per claim” deductible, was the homeowner’s claims against the general contractor (of which there were 636, grouped into three complaints) or the general contractor’s claim against the subcontractor, of which there were three, i.e., the cross-claims. Since the court held that both constructions were “reasonable and are supported by the policy language,” the interpretation favoring the insured controlled. Translation, the insured was responsible for only three deductibles – one for each cross-claim.

The court also rejected the insurer’s multi-deductible argument that Yarbrough would have been obligated to pay 636 deductibles if the homeowners had sued Yarbrough directly. But that was not relevant, as the court saw it: “Under California law, [t]he proper question is whether the provision or word is ambiguous in the context of this policy and the circumstances of this case.” (emphasis in original).

|

|

|

|

|

|

|

Vol. 7, Iss. 6

July 18, 2018

The “Waiver Rule:” This Is How Serious It Can Be

|

|

|

|

The most contentious provision for insurers, during the drafting of the ALI’s Restatement of the Law of Liability Insurance, was the possible adoption of the so-called “waiver rule.” In general, the rule provides that if an insurer refuses to defend its insured under a reservation of rights or does not seek a declaratory judgment that it does not owe coverage, and it is determined that it breached the duty to defend, the insurer waives the right to subsequently assert that there is no duty to indemnify. In other words, while a duty to defend may be owed, based on the allegations in the complaint, the insurer that did not follow one of these courses loses the right to argue that there is no duty to indemnify – a determination made based on the actual facts established.

The waiver rule appeared in the original draft of the Restatement. However, it had a much lower profile in the version that was ultimately approved – being discussed in comments as a possible remedy for an insurer’s bad faith.

Illinois applies the waiver rule. And a recent decision from its Appellate Court demonstrates just how significant this penalty can be – and why insurers fought its adoption as aggressively as they did during the drafting of the Restatement.

Country Mutual Ins. Co. v. Badger Mutual Insurance Co., No. 1-17-1774 (Ill. Ct. App. June 29, 2018) involved coverage for a conventional construction defect claim. Roe Construction performed construction and remodeling work at the residence of Steven Gelsomino. Property was damaged as a result of Roe’s alleged negligent failure to perform the work. Gelsomino’s homeowner’s insurer, Badger Mutual, paid Gelsomino for certain of the damage. Badger brought a subrogation action against Roe Construction, alleging that, as a result of Roe’s negligence, the building sustained property damage, including water damage. Of note, the complaint did not specify when the property damage occurred, but that its existence was learned in March 2010.

Roe tendered the complaint to Country Mutual, its commercial general liability insurer. Country refused to defend and a default judgment was entered against Roe in the amount of $222,000. Eight days later, Country filed a declaratory judgment action against Roe, Badger and Gelsomino, alleging that no coverage was owed on account of various reasons – no occurrence, its policy expired in 2006 and various exclusions.

For purposes here it is not necessary to delve into the construction defect coverage analysis undertaken by the court. The trial court held that Country breached its duty to defend Roe. As a result, the trial court held that, under Illinois law – the waiver rule -- Country was estopped from denying coverage in an action to collect the default judgment.

The Illinois appeals court affirmed. In doing so it provided an important announcement about the scope of the waiver rule.

But first, to get there, you must start with the duty to defend. The court held that Country had such an obligation: “[W]e find that the allegations of the underlying pleaded facts raising a potential of ‘property damage’ that occurred within the policy period. The policy covered ‘property damage,’ which was defined to mean ‘Physical injury to tangible property including all resulting loss of use of that property.’ The underlying complaint alleged that Roe’s negligent construction work caused Gelsomino’s building to sustain ‘property damages, including water damage.’ We acknowledge that such allegations do not specify what particular property was damaged. Nonetheless, given the minimal pleading threshold to trigger a duty to defend, the allegations raised at least the potential that there were damages covered under the policy.”

On the issue of whether property damage occurred during the policy period, the court was likewise guided by the “low” threshold for determining a duty to defend: “Although lacking specificity, the underlying allegations asserted property damage occurring sometime between August 2005 and the time the plaintiffs ‘learned’ of the damage in March 2010. Although this is a wide time frame, it undoubtedly overlaps with the policy period, and thus alleges at least the potential that some of the damages were covered. Thus, the complaint triggered Country’s duty to defend.”

Having determined that Country breached the duty to defend Roe – and not having filed a timely declaratory judgment action -- the appeals court turned to the estoppel issue.

Country argued that, by applying estoppel, the court “creates coverage” for damages taking place beyond the policy period. [Remember, the policy expired in 2006.] In other words, as Country say it, estoppel is limited to the insurer’s waiver of “policy defenses” and “should not prevent Country from asserting that the damages occurred beyond the expiration of the policy.”

Observing that Country’s situation was “of its own making,” and it could have litigated the issues it now seeks to, the court was not pursued by a distinction between a “policy defense” and the argument that no coverage is owed based on the failure of a policy to provide coverage in the first place. “We acknowledge that estoppel has been described as precluding an insurer from raising ‘policy defenses.’ [citation omitted.] However, Country cites no binding authority that expressly limits the application of estoppel in this context to ‘policy defenses.’ To the contrary, our supreme court in Clemmons [v. Travelers Insurance Co., 430 N.E.2d 1104 (Ill. 1981)] stated: ‘When a complaint against the insured alleges facts within or potentially within the scope of the policy coverage, the insurer taking the position that the complaint is not covered by the policy must defend the suit under a reservation of right or seek a declaratory judgment that there is no coverage. [Citation.] If the insurer does not, it is later estopped from denying coverage in a suit to collect the judgment.’” (Emphasis added by Country court).

Yes, Country Mutual v. Badger Mutual demonstrates why insurers fought the adoption of the waiver rule as aggressively as they did during the drafting of the ALI’s insurance Restatement.

|

|

|

|

|

|

|

Vol. 7, Iss. 6

July 18, 2018

When Sexual Misconduct Could Be A “Professional Service”

|

|

|

|

As a general rule, an individual seeking coverage, for liability on account of sexual misconduct, has an uphill battle -- and often-times a steep one at that. When the issue arises under a liability policy, often homeowner’s, challenges to coverage can be the lack of an occurrence (accident), exclusions for expected or intended injury or criminal acts and coverage prohibitions for reasons of public policy.

Claims for sexual misconduct can also arise under Professional Liability policies, such as those issued to medical professionals. Here too there can be high hurdles to coverage – although usually involving some different ones than under a liability policy. One issue that often arises, under a Professional Liability policy, is whether the alleged sexual misconduct was caused while the insured was performing a “professional service.” The question whether a loss was caused by an insured performing a “professional service,” whatever that may be, is a common one in many professional liability claims.

On one hand, that seems to be a question with an easy answer, as an Ohio Appeals Court recently noted in Beattie v. McCoy, No. C-170197 (Ohio Ct. App. June 29, 2018): “Under the natural and commonly accepted meaning of the policy terms, a physician, like McCoy, does not provide a ‘professional service’ by engaging in sexual conduct with a patient. Sexual conduct is not specifically identified as a professional service in the policy. It is so dissimilar from the professional services enumerated in the policy, that no construction of the policy language would support coverage for sexual conduct as a ‘professional service.’”

On the other hand, the issue could be less clear-cut than it seems, as it was the fact that the perpetrator was a physician that afforded him or her access to the patient-victim, not to mention with physical proximity perhaps being inherent part of the relationship. Therefore, arguments are sometimes made – on this basis and others tied to the nature of the physician-patient relationship -- that coverage is available to a physician, under a Professional Liability policy, for alleged sexual misconduct.

One such argument was made in Beattie. And despite the court’s strong pronouncement – “no construction of the policy language would support coverage for sexual conduct as a ‘professional service’” – it nonetheless described one manner in which coverage for sexual misconduct could be afforded.

Terrance McCoy had been Dolly Beattie’s internist since 1996. In October 2010, she informed him that she was suffering from depression. McCoy referred Beattie to a clinical therapist. In 2011, Beattie visited McCoy complaining of pain in her hands and body aches. McCoy examined Beattie’s back and shoulders. This led to a consensual romantic encounter. From there, Beattie and McCoy, both married, began, what the court described as a “tumultuous” sexual relationship.

The relationship soured. Beattie filed a complaint with the state medical board, which undertook an independent investigation. McCoy was forced to surrender his medical license in 2012 with no opportunity for reinstatement.

Beattie also filed suit against McCoy. She alleged that McCoy’s sexual behavior constituted medical malpractice. The trial court ruled in her favor and awarded over $850,000. Among other things, at issue before the Ohio appeals court – I’m eliminating some aspects not relevant -- was the availability of coverage under McCoy’s professional-liability policy. The question being whether McCoy injured Beattie “while performing a professional service?” The insurer defended McCoy under a “strict reservation of rights,” but declined any duty to indemnify him.

Of note, a significant issue in the underlying medical malpractice action was Beattie’s ability to offer the testimony of an expert – Stuart Bassman, Ed.D., a clinical psychologist. Bassman’s testimony became important in the coverage case. According to Bassman, “Beattie had sustained aggravation of her post-traumatic stress disorder (‘PTSD’), because of the affair with McCoy. Beattie already suffered from PTSD and other issues, including depression and anxiety, because of prior sexual violence inflicted on her in her youth. In Dr. Bassman’s opinion, McCoy should have known that Beattie was vulnerable because of her history, and with that knowledge, he exploited and ‘revictimized’ Beattie by having a sexual relationship with her.” Bassman also maintained that “Beattie exhibited transference phenomenon: when a patient unconsciously projects on an authority figure, like a treating psychologist in a psychotherapeutic relationship, feelings and behaviors associated with significant persons in the patient’s life.”

Turning to the availability of coverage, as noted above, the court seemed predisposed against it: “[N]o construction of the policy language would support coverage for sexual conduct as a ‘professional service.’” However, despite this, the court seemed open to the possibility that coverage, for sexual misconduct, could be owed on the basis that it qualifies as a “professional service.”

Specifically, the policy at issue provided coverage when an “insured becomes legally obligated to pay because of professional services * * * which should have been provided.” Beattie, arguing for coverage under McCoy’s policy, maintained that “refraining from sexual conduct with Beattie or rebuking her sexual advances was a part of the professional services that McCoy should have rendered. Beattie offered Dr. Bassman’s transference opinion to establish that McCoy, as a treating physician, was required as part of his professional services to avoid sexual misconduct with a patient exhibiting positive transference.”

In support of this argument, Beattie relied on a 1990 Minnesota Supreme Court opinion – St. Paul v. Love – where the court held that “sexual misconduct that is inextricably related to a therapeutic relationship between a psychologist and his patient, being treated for marital problems and childhood sexual abuse, could fall within the coverage of a therapist’s professional-liability insurance policy. The sexual conduct in Love, while ‘aberrant and unacceptable,’ was ‘so related to the treatment contemplated’ that it came within the scope of the insurance coverage for professional services provided or withheld.”

But the Beattie court was not persuaded: “Even under Love, Beattie cannot demonstrate as a matter of law that McCoy’s sexual conduct was inextricably related to the professional services that he provided or withheld.” The court noted that McCoy’s therapeutic relationship with Beattie was a limited one: “Since 1996, McCoy had been treating Beattie for a variety of minor medical ailments. When, in October 2010, Beattie informed McCoy that her depression was worsening and asked him for help, McCoy did not enter into an involved ‘therapeutic alliance’ with her. Rather he referred Beattie to Dr. Janet Stedman, a clinical therapist, for treatment of depression and anxiety. Her first appointment with Dr. Stedman was on October 21, 2010, almost exactly one year before McCoy’s sexual conduct began. While McCoy continued to prescribe medicine for these conditions, there is nothing in the record to indicate that McCoy engaged in the type of intimate psychological therapy contemplated in Love or in the Ohio cases cited above. McCoy’s deposition testimony revealed that he was not aware of traumas in Beattie’s childhood or young adult life. And Beattie, rather than being in thrall ‘to the authority of her trusted physician,’ threatened throughout the turbulent affair to report McCoy to the state medical board and to reveal their sexual relationship to his wife, and ultimately did so. Thus McCoy’s sexual conduct was not inextricably related to the medical or mental professional treatment that Beattie received. Beattie has not established that McCoy’s sexual conduct was a consequence of his treatment of her depression and anxiety, and thus his failure to avoid that conduct was a professional service which he should have provided.”

While Beattie/McCoy were handed the same result as many seeking coverage for injuries caused by sexual misconduct, the decision certainly leaves open the possibility of coverage, for a physician, if the sexual conduct was inextricably related to the medical or mental professional treatment that the patient received.

|

|

|

|

|

|

|

Vol. 7, Iss. 6

July 18, 2018

What Is A “Function?” – A Company Picnic Or Three Employees Having A Beer At Work?

|

|

|

|

Sentry Select Insurance Company v. Ruiz, No. 16-376 (W.D. Tex. June 20, 2018) involves an obscure issue. You can probably count on one hand the number of coverage professionals who have ever encountered it. But it’s interesting. So it’s here.

At issue is coverage for an automobile accident. But this was no red light-green line at the corner of Elm and Main. The story goes like this. Rudolph Mazda, in El Paso, Texas, was keen on selling cars. The sales people arrived at 9 a.m. and the dealership provided lunch on its premises to keep them in place to sell. Sales people were expected to stay as late as needed – sometimes until 10 p.m.

One day in December 2013, Marcelo Flores, a manager of Rudolph Mazda, sent Christian Ruiz, a salesman, to the store to purchase beer. This was done during working hours. The beer was placed in the Rudolph Mazda refrigerator and consumed that night, after work, and on the dealership’s premises, by Ruiz, Flores and another manager, Lynn Crawford.

After consuming beer, Ruiz struck salesperson Irma Villegas with his vehicle while she was walking in the Rudolph Mazda parking lot. Villegas suffered various injuries and filed suit against Ruiz, Flores, Crawford and Rudolph Mazda, asserting a variety of causes of action.

At issue was the availability of coverage for Rudolph Mazda under a Sentry Insurance garage liability policy, which provided protection for bodily injury caused by an accident and resulting from garage operations involving the ownership, maintenance or use of any auto. The policy also contained a broadened coverage endorsement, where the insurer agreed to “pay all sums the insured legally must pay as damages because of ‘bodily injury’ . . . arising out of the giving or serving of alcoholic beverages at functions incidental to your garage business provided you are not engaged in the business of manufacturing, distributing, selling or serving of alcoholic beverages.” (emphasis added).

Sentry and Rudolph Mazda disputed whether the beer consumption, on the night in question, fell within the scope of the undefined term “function” as used in the liquor coverage endorsement. Rudolph Mazda argued that any social gathering can be a “function.” Sentry did not see the term so broadly, arguing that the provision “only applies to company functions such as company Christmas parties, company picnics, etc.” A gathering of a few employees, who stay after work to socialize, is not a function, so said Sentry.

But the court was not persuaded that a “function” cannot be an after-work gathering of a few employees for beer consumption. The court’s rationale was simple -- there was nothing in the policy that evidenced an intent to exclude a particular type of social gathering from the meaning of the term “function.”

It is a curious decision. The court noted that, to determine the meaning of an undefined term, it is appropriate, as a starting point, to examine the dictionary definition. And it did so, which revealed that several dictionaries defined “function” as an official or formal gathering. There is little that is official or formal about a few co-workers having a brewsky after work. Even if “an intent to exclude coverage must be expressed in clear and unambiguous language,” isn’t that what the insurer did by using a term that has a clearly defined meaning?

[In case you are wondering, the court concluded that the Employer’s Liability exclusion did not apply as Villegas was no longer in the course of her employment when the injury occurred. Rather, she had ended her work and was in the process of leaving.]

|

|

|

|

|

|

| |

|

| |

|

|

WSJ: Insuring The World Cup

A July 5th article in The Wall Street Journal looked at numerous insurance aspects surrounding the World Cup. The court noted that Allianz lost a financial “bonanza” when it declined the opportunity to insure sales promotions or prizes that would be paid if defending champion Germany won the tournament. The German insurer passed as it believed that there was a high likelihood that its home team would repeat as winner. But Germany did a quick auf wiedersehen, getting knocked out in the group play. However, Allianz did score when it insured against a victory by Poland. Bold move. The article looks at a host of World Cup risks that are insured, such as cancellation, terrorism, cyber attacks, player injuries and transportation of tournament-themed merchandise.

Florida Federal Judge Gets In A Grove With Puns

This clever judicial prose from Judge Steven Merryday, of the District Court for the Middle District of Florida, in Travelers Indem. Co. v. Richard McKenzie & Sons, Inc., 17-2106 (M.D. Fla. June 28, 2018): “Citrus-grove owner Richard Hermanns attempts to squeeze $2.965 million from Travelers Indemnity Company based on Hermanns’s consent judgment against Richard McKenzie, the former manager of Hermanns’s grove and a former insured under a Travelers Commercial General Liability (CGL) policy with a ‘farm care-taker liability’ endorsement. . . . Hermanns’s effort to concentrate on the endorsement yields no fruit: The insurance policy excludes coverage, the consent judgment is unreasonable, and the insurer owed no duty to defend.”

Court Upholds Australia Forum Selection Clause (Policy Issued In California)

“Plaintiffs do not contend that the forum selection clause is the product of fraud or overreaching, but instead argue that it should not be enforced because it would contravene California’s strong public policies expressed in California Insurance Code sections 678.1 and 11580, and because Australia is not an adequate or convenient forum. Liberty responds that enforcement of the clause does not contravene any public policy with respect to venue and that plaintiffs are free to litigate their claim in Australia. . . . The public policy expressed in this section [Section 11580] is that plaintiffs have an avenue for relief, but not specifically one in California. As Liberty notes, Australian law has a similar provision that provides plaintiffs with the same ability to bring such an action. See Rep. at 11 (citing Civil Liability (Third Party Claims Against Insurers) Act 2018 (NSW) (Aust.). . . . While I am sympathetic to plaintiffs’ desire to litigate in California, I am bound by the precedent requiring enforcement of the forum selection clause in this action.” Lewis v. Liberty Mut. Ins. Co., 18-01138 (N.D. Cal. May 29, 2018).

Wow! Insurer Makes A Very Bold Argument

Look, I get it. It is a lawyer’s job to be a zealous advocate for his or her client. But sometimes lawyers make arguments that seem to take that too far. For a lawyer representing an insurer in a coverage case, that may apply to this argument: “At the hearing, American Family suggested that that if the term ‘loading’ can reasonably be understood to refer to both interpretations, American Family should get the benefit of both and exclude coverage for injuries that occur while someone is placing items in the boat and those which occur while placing the boat onto something else. But the law does not allow this ‘heads I win, tails you lose’ analysis. . . . American Family’s argument is not supported by Minnesota law, the term is ambiguous, and that ambiguity must be construed against the insurer.” Am. Family Mut. Ins. Co. v. Pilarski, No. 17-04463 (D. Minn. June 28, 2018).

|

| |

|

|

|

| |

|

|

|

|

|

|

|

|

|