|

|

|

|

|

Vol. 4, Iss. 10

October 28, 2015

|

|

|

|

| |

|

| |

|

|

The Abel trial took place in 1957. A year earlier Donovan argued a “number of occurrences” case before the Supreme Court of Washington. Really. I’m not making this up. I couldn’t. (See Truck Insurance Exchange v. Rohde, 303 P.2d 659 (Wash. 1956)).

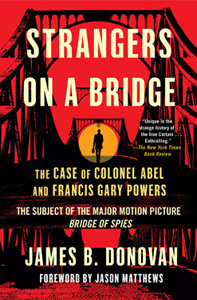

Since learning that an insurance (um, coverage) lawyer had done something so breathtakingly unique I have had a insatiable appetite to learn more about James B. Donovan. On one hand, the information is out there. The Abel trial and Powers swap are chronicled, in great detail, in Donovan’s own words in his fantastic 1964 book Strangers on a Bridge (recently re-released by Simon & Schuster). In addition, a biography of Donovan has been published as well as a collection of his speeches.

But my main interest is James Donovan--the insurance coverage lawyer. And, as you can imagine, the great majority of what’s been written about Donovan’s life does not go down that road. So for help I sent an inquiry to the email address listed on a website that chronicles Donovan’s life (jamesbdonovan.com). In return I received a wonderful note from Beth Amorosi, Donovan’s granddaughter, who runs the informative website, and was more than happy to assist me. Beth provided me with background material concerning the insurance aspect of her grandfather’s career that I could have never found easily. In addition, she generously arranged for me to interview all three of Donovan’s living children. These were three phone calls I won’t soon forget.

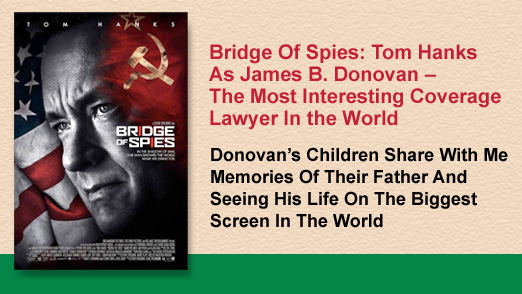

James B. Donovan: The Role Made For Tom Hanks

If all James Donovan had done in his career was to be a highly accomplished insurance lawyer, represent notorious spy Rudolf Abel and negotiate his release for an American spy pilot, he would unquestionably get the award for most interesting coverage lawyer in the world. Except those are just a couple of items on his remarkable resume. Here is how Donovan’s life is described by Beth, his granddaughter, on her website.

Born in New York City in 1916, James B. Donovan graduated from Fordham University and Harvard Law School. A commander in the Navy during World War II, he became General Counsel of the Office of Strategic Services and was Associate Prosecutor at the principal Nuremberg trial. [I learned that he was responsible for the powerful visual evidence.]

Mr. Donovan subsequently acted as chief counsel in major trials and appeals in over thirty states, and was an insurance lawyer and partner at Watters and Donovan. He was defense counsel to Colonel Rudolf Abel, subsequently negotiating for his exchange with American U2 pilot Francis Gary Powers. He was Democratic candidate for United States Senator from New York in 1962; served as General Counsel for the Cuban Families Committee, obtaining the release of more than 9,700 Cubans and Americans from Castro’s Cuba; was President of Pratt Institute; and was President of the Board of Education of the City of New York. He died in 1970, and was survived by his wife and four children.

As I see it, Tom Hanks was perfectly cast for the role of James B. Donovan. After all, Donovan’s life resembles that of Forrest Gump.

James B. Donovan: Insurance Lawyer

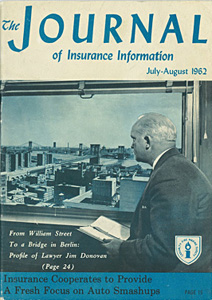

Beth Amorosi provided me with a copy of the July-August 1962 issue of the Journal of Insurance Information featuring her grandfather on the cover. It includes a profile of Donovan’s life as an insurance lawyer. Basically it’s the article I am trying to write here – except I was scooped by 53 years. I don’t know who wrote this wonderful piece except that his or her initials are E.G.D. I wish I did so that I could say thank you (if possible) for all of the borrowing of information that I am about to do. [Figuring out who E.G.D. is, is on my to-do list. It should be pretty easy.]

According to the JII article, in 1946 or so, following his involvement with Office of Strategic Services and the Nuremberg trial, the 30 year old Donovan became general counsel of the National Bureau of Casualty Underwriters. But the road to that office dates back to Donovan’s WWII days, where he developed a top-secret disability and life insurance program for civilian scientists who were taking great risks in research.

The JII article describes the project like this: “All Donovan had to do was to find U. S. insurers willing to underwrite a hazard they could know nothing about, on insureds whose names and precise jobs they could not be told, at rates which could not be based on experience. On top of this, the companies had to agree to pay claims they could not even investigate!” But Donovan pulled it off, using a syndicate of insurance, and the companies even made a small profit.

Having joined the National Bureau of Casualty Underwriters right when Congress had passed the McCarran-Ferguson Act, Donovan was directly involved in the state vs. federal fight over insurance regulation. He even litigated the issue in the Eighth Circuit where he was successful and cert. was denied by the Supreme Court.

In 1950 Donovan joined with Thomas Watters, Jr., a former deputy insurance commissioner of Iowa (played by Alan Alda in the film), to form the law firm Watters & Donovan in New York and Washington. The firm’s clients included numerous large insurance companies. During his career, Donovan served as Chair of the Insurance section of the ABA.

Following Donovan’s death in 1970, the Watters & Donovan firm went through various successions and, in 2002, became Donovan Parry McDermott & Radzik. The firm’s Dan McDermott, renowned maritime and maritime insurance lawyer, now with Marshall Dennehey in New York, recently published a moving tribute to Donovan in The National Law Journal (Oct. 19). I spoke to McDermott and he was happy to share some stories with me. While he never met Donovan, the former insurance lawyer is a daily presence in McDermott’s life. McDermott sent me a picture of his office featuring some courtroom sketches from the Abel trial.

While not a lot has been written about Donovan’s career as an insurance lawyer, I learned much from a review of his insurance cases. There are a lot to read. I can only mention a few here.

In the Rohde case mentioned above (Wash. 1956), Donovan successfully represented insurers, as amici curiae, in establishing that a single occurrence limit applied, under an automobile policy, where an insured vehicle struck three motorcycles in quick succession.

In Morton v. Maryland Casualty Co., 151 N.E.2d 881 (N.Y. 1958), Donovan, representing insurers as amici curiae, was on the winning side of the New York high court’s decision that an underlying plaintiff could not bring suit in New York, pursuant to Louisiana’s direct action statute.

In Aetna Casualty and Surety Co. v. General Casualty Co., 140 N.Y.S.2d 670 (N.Y.A.D. 1955), Donovan, again as amici curiae, was unsuccessful in arguing that no coverage was owed under an auto policy, to a permissive user, for injuries sustained by the named insured when he was a passenger in his own vehicle, being driven by the permissive user.

In Weissblum v. Glens Falls Insurance Company, 244 N.Y.S. 689 (N.Y.A.D. 1963), Donovan convinced the New York Appellate Division that an insurer was not liable for coverage, for 189 damaged windows, because the insured did not establish that he was “legally obligated to pay” for such damage. The insured only established that he was obligated because of a contractual assumption of liability, which was excluded under the policy.

There is no denying Donovan’s bone fides as a coverage lawyer. He was no dabbler. This makes it all that much more remarkable that, from 1957 to 1962, he was involved in the Abel case and spy swap.

Incidentally, the Abel case no doubt kept Donovan away from his private insurance practice for long periods of time. Yet, for all those years of working on it, he received the paltry sum of $10,000. And Donovan donated all of it to charity.

James B. Donovan: Conversations With His Children

I am so grateful to Beth Amorosi for arranging for me to speak with her mother, Jan Donovan Amorosi, age 71, in New York City, as well as James Donovan’s other two children, John Donovan, 69, in Norwalk, Connecticut and Mary Ellen Fuller, 65, in Alcolu, South Carolina. Beth arranged back to back to back phone calls for me with her mother, uncle and aunt. I’ve never had three phone calls in a row with my own relatives.

Donovan’s children could not have been kinder to me or more generous with their answers to my questions. They were not on the phone to talk about themselves, but, of course, I had to ask whether certain things in the film, about their characters, were real or fictionalized. For a Curious George-type like myself that’s just too tempting to pass up.

Donovan’s children attended the Bridge of Spies New York opening at Lincoln Center and had the chance to spend time with Steven Spielberg and Tom Hanks. Mary Ellen recounted that Spielberg commented how much he enjoyed the opportunity to meet a character’s family – something that doesn’t always come up – with Spielberg pointing out that his last film was Lincoln.

When one’s father’s life is portrayed by Tom Hanks, the first question that has to be asked is the most obvious – well, how did he do? Each one of Donovan’s children had a similar response. They didn’t say simple things like -- Hanks did well or Hanks really got it right. Instead they judged Hanks’s performance very high by the emotional responses that it brought out in them. For Mary Ellen, seeing Hanks as her father made her realize just how much she missed him. Jan was brought to tears by how harshly Hanks was treated during his time in Berlin putting together the spy swap. John praised Hanks for, in addition to bringing out the feeling of missing his father, pulling off his father’s “steadfastness” “leavened by occasional wit.”

Mary Ellen told me that, seeing her father finally being recognized, for the important things that he had done in his life, has been very emotional for her. And that gets to the heart of what’s so amazing about Bridge of Spies. It’s not just the story of James Donovan. It’s his story being told on the biggest of all screens in the world -- Steven Spielberg directing Tom Hanks. This isn’t some documentary being screened at an indy film festival.

As the oldest of the three children I asked Jan for her most vivid memory of the Abel case. She recounted the thrill of traveling to Washington to attend the oral argument in Abel’s appeal before the United States Supreme Court. She also recalled being in a cab with her father, a week before he traveled to Berlin, and sensing an excitement in him. She can remember seeing him rubbing his palms together – something he did when he was looking forward to something. The real purpose of her father’s upcoming trip to Europe had not been revealed to his family (a cover story was used); so only later did she suspect knowing the reason for his excitement in that cab.

John also had tremendous memories of his father and the Abel case. Incredibly, in June 1956, at age eleven, he was present in the Washington Supreme Court, in Olympia, when his father argued “number of occurrences” in Truck Insurance Exchange v. Rohde. His vivid memories of the case were remarkable. John also had the unique experiences of being with his father on visits to Abel in prison as well as to Cuba and meeting Castro. He recalled Abel being not much different from how he was superbly under-played by Mark Rylance in the film. On one prison visit to Abel, John sang him a ditty that the family had written: “Rudolf Ivanovich Abel” sung to the tune of Rudolf the Red Nosed Reindeer.

The screenplay for Bridge of Spies was written by Matt Charman, along with Joel and Ethan Coen. [My sense is that Charman did the heavy-lifting.] John had a breakfast meeting with Charman when he was writing the script. Charman was a good listener. John read me an email that he had just received from the writer -- thanking him for bringing his father alive.

That James Donovan died at age 53, of a heart attack, is staggering – both for its sadness and remarkableness that he did so much in such a short period. I asked John Donovan what else might his father have accomplished if his life had not been cut so short. He speculated that it may have been related to education, having been President of the New York City Board of Education and Pratt Institute. John dismissed the possibility of politics -- as he didn’t think his father was too upset about losing the race for a United States Senate seat.

When you watch Bridge of Spies it is so easy to compare Tom Hanks to Gregory Peck in To Kill a Mockingbird. Both played lawyers who zealously represented unpopular clients and were subject to public scorn for doing so. Mary Ellen told me that MGM obtained the rights to Donovan’s book, Strangers on a Bridge. But for whatever reason the film never came to pass. James Donovan was going to be played by Gregory Peck.

|

|

|

| |

|

|

|

|

Vol. 4, Iss. 10

October 28, 2015

|

|

|

|

| |

|

| |

|

| |

I am very excited to share that Coverage Opinions is partnering with National Underwriter and American Lawyer Media in the following webinar that I will be presenting on November 18th:

The Definitive Reservation of Rights Checklist: 50 Things That Every ROR Needs.

https://www.eiseverywhere.com/ehome/rorwebinar/325590

No matter how much experience a person has drafting Reservation of Rights letters, it is still easy to omit something. There is no set way to draft them and courts have been penalizing insurers for issuing Reservation of Rights letters that they do not believe are adequate. And this penalty can be severe -- the loss of coverage defenses.

50 things that every ROR needs sounds like a lot. But I can make the case that there are that many things that every ROR should have -- or consider.

This Is The Most Practical Webinar That Someone Will Ever Attend. Most webinars involve esoteric discussion of case law that is forgotten 5 minutes after the webinar is over. Here, lawyers and adjusters will leave with a 50-item ROR checklist that they can begin to implement, in their actual work, 5 minutes after the webinar is over.

I am also pleased that the webinar is approved for CLE and adjuster CE in various states. Too many programs are approved for CLE for lawyers but not adjuster CE. Getting CE approval was a must-have for me in the arrangement.

Early registrations have been fantastic. Some law firms and insurance companies are signing up groups by the dozen.

If you like Coverage Opinions, rest assured that I put the same passion and effort into this webinar.

I hope you’ll check out the program.

Details here:

https://www.eiseverywhere.com/ehome/rorwebinar/325590

Randy

|

|

|

| |

|

|

|

|

Vol. 4, Iss. 10

October 28, 2015

Halloween And Insurance Coverage

(Or Not) |

|

|

|

|

| |

On Saturday night nine trick or treaters will knock on my door. And three of them with be under the age of two and have no idea what’s going on. I know this because I’ve been in my house for fifteen years and have kept data on it. My street just isn’t popular on Halloween. I guess it makes sense. There are no sidewalks. Presumably that’s an issue of concern for responsible parents. Plus, if such an election were held, the people next door would be voted most likely to give out loose candy corns.

But despite all this, I will still have four bags of candy at the ready -- as I always do. And my wife will look at me, as she always does, and ask – why? It’s just fear. Plain and simple. I know what the numbers tell me. I know I’d be more than prepared with a single bag. But every year I worry that this will be the one when an avalanche of kids show up. I just can’t bear the thought of running out of candy and scurrying around the kitchen to find something as a substitute. Imagine handing an adorable little Elsa a can of Mandarin oranges and telling her that they are just as good as a Kit Kat – while Elsa’s mom is telling me not to worry about it and just let it go.

Now here’s where I planned to turn this scary tale into one with an insurance coverage angle. However, the idea I had didn’t work out. That happens sometimes. And tomorrow is my publishing deadline. And I have a wedding to go to later today. Who makes a wedding at two in the afternoon on a football Sunday? Who? Plus I don’t even know the happy couple. I wouldn’t know them if they sat down next to me on the train. It’s my wife’s friend’s son. And it’s an hour away. Some town in Jersey I’ve never heard of. My wife is going to think I have diabetes when I need to go to the bathroom every ten minutes – to check scores. Can’t we just send a Cuisianart? -- I pleaded with my wife. So the chances of me writing an insurance-related column, between now and tomorrow, are not good. Like a 14 point underdog not good. So this is it.

That’s my time. I’m Randy Spencer. Contact Randy Spencer at

Randy.Spencer@coverageopinions.info

|

|

| |

|

|

|

|

Vol. 4, Iss. 10

October 28, 2015

Coverage Opinions Turns 3!

Next Issue:

An Absolute Blockbuster Interview! |

|

|

|

| |

|

| |

I am excited to report that this issue marks the 3rd Anniversary of Coverage Opinions. If there has ever been a labor of love in my career, this is it. Like any such endeavor, on some days there has been more of the former than the later. But despite the challenges, I could not be happier with how things have gone for CO over the past three years.

I am so grateful to readers who send me cases and story ideas and the many famous (and no so famous – but fascinating nonetheless) lawyers who take the time to let me interview them for the Declarations column. CO is not exactly the Weekend Interview in The Wall Street Journal and I’m not Larry King. I treat every one of these opportunities as a privilege and take them very seriously. Next Issue: A blockbuster interview!! A huge get for CO! And thank you to Randy Spencer for hanging-in for every issue, despite his occasional belly-aching about having the most popular column in CO, but not getting paid.

Of course, there could be no three-year anniversary to mark if it were not for you -- the Coverage Opinions reader. I can’t thank CO readers enough for taking the time to do so, despite having such busy schedules and being inundated with other newsletters, and the like, competing for their time. I also appreciate all of the reader mail that I receive – mostly positive, but sometimes taking me to task for something I said or didn’t say -- and that’s fine too. Please accept my sincere appreciation for enabling me to send a Coverage Opinions thee-year anniversary announcement.

Randy

Comments, questions, criticism, hate mail, how’s my driving, ideas for making CO better -- I’m all ears. Write to me at Maniloff@CoverageOpinions.Info

|

|

|

| |

|

|

|

|

Vol. 4, Iss. 10

October 28, 2015

Why You Should Be Reading This Issue Of Coverage Opinions

|

|

|

I have great news for you. Since you are reading Coverage Opinions right now that means you are not watching a commercial for Draft Kings or Fan Duel. No need to thank me. Just a little favor for you, dear reader.

|

|

| |

|

|

|

|

Vol. 4, Iss. 10

October 28, 2015

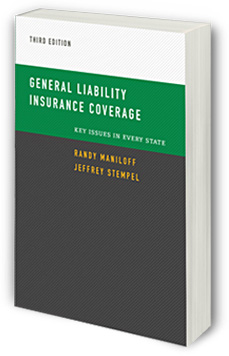

General Liability Insurance Coverage – Key Issues In Every State

Save 40% Off The Amazon Price

|

|

|

|

| |

|

| |

Use Discount Code WVQRK7LZ at the following “Create Space” site to get a 40% discount off the 3rd Edition of General Liability Insurance Coverage – Key Issues in Every State:

http://www.createspace.com/5242805.

Everything you want to know about the 3rd Edition of Insurance Key Issues is here:

http://www.InsuranceKeyIssues.com

See for yourself why so many find it useful to have, at their fingertips, a nearly 800-page book with just one single objective -- Providing the rule of law, clearly and in detail, in every state (and D.C.), on the liability coverage issues that matter most.

|

|

|

| |

|

|

|

|

Vol. 4, Iss. 10

October 28, 2015

Of Pizza And Definitions (Part 2)

|

|

|

| |

|

In the last issue of Coverage Opinions I noted a sign, on the register at New York Pizza Suprema, my favorite pizza place, that caught my eye. When it comes to insurance coverage, definitions are everything. So, as one attuned to such things, this sign, providing a very specific definition of the word “immediately,” made me chuckle.

|

|

|

|

| |

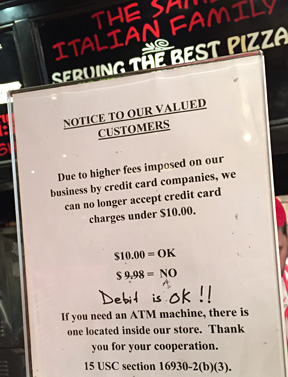

I was back at New York Pizza Suprema a couple of weeks ago. And there was another sign. Once again the folks at NYPS are busy defining things. This time the pizza guys want to leave no doubt just how much dough must be spent to use a credit card. Policyholder lawyers will definitely appreciate this sign, since they believe that nothing is ever written clearly enough..

[By the way, I checked out 15 USC 16930-2(b)(3). I couldn’t find it. I did find 15 USC 1693(2)(B)(3) which has something to do with consumer protections and compliance costs associated with electronic banking. The next time I’m in NYPS I’ll say: two plain and what’s 15 USC 16930-2(b)(3) mean?]

Incidentally, New York Pizza Suprema (8th Avenue and 31st Street – one minute from Penn Station if you make the light at 8th) was featured in a front page Wall Street Journal story in 2011, as the only pizza place to receive a perfect score from a pizza blogger who sampled a slice -- over a two and a half year period -- at all 362 “slice joints” in Manhattan. Look it up. It’s a great story.] |

|

|

|

| |

| |

|

|

|

|

Vol. 4, Iss. 10

October 28, 2015

From Boo To Sue: Are Haunted Houses Liable For Scaring Their Visitors?

|

|

|

[This article originally appeared in the October 30, 2013 issue of Coverage Opinions.]

It is the oldest admonishment in the book from parent to child – don’t talk to strangers. But one day a year we make an exception. And more than just letting our kids talk to strangers, we even let them accept food from them. Of course parents change the rules on Halloween. But while parents can be flexible on Halloween, can the legal system? A hallmark of the legal system is its predictability. Is it less predictable when Halloween is concerned?

One Louisiana appeals court said yes: “On any other evening, presenting a frightening or threatening visage might be a violation of a general duty not to scare others. But on Halloween at trick-or-treat time, that duty is modified. Our society encourages children to transform themselves into witches, demons, and ghosts, and play a game of threatening neighbors into giving them candy.” Bouton v. Allstate Ins. Co., 491 So. 2d 56 (La. Ct. App. 1986) (also noting that the Louisiana legislature has recognized Halloween as a special occasion by exempting it from the statute which prohibits the wearing of masks in public places).

But does this “Halloween rule” apply to haunted houses? All sorts of duties are imposed on property owners to maintain a safe premises. Do these same rules apply when the premises are advertised as having, as their only purpose, to scare visitors? Indeed, many visitors will leave a haunted house disappointed if they were not frightened while there. That being the case, can the visitor of a haunted house now turn around and sue for injuries sustained in the process of getting what he asked (and paid) for?

Just as with the trick-or-treaters in Bouton, haunted houses seem to universally get special treatment at the court house. Based on my research, there have been five reported judicial decisions nationally in which a visitor of a haunted house sought recovery for an injury sustained on account of being scared (a few other cases involve haunted house injuries but not on account of the fright factor). In all five cases the injured patron was not able to recover because of the unique nature of a haunted house. [Here’s the eeriest factor -- all five cases are from the Court of Appeal of Louisiana. What is up with that?] Take a look at the following:

In Mays v. Gretna Athletic Boosters, 668 So. 2d 1207 (La. Ct. App. 1996) the plaintiff, a 10 year old girl, was frightened when a character at a haunted house jumped out at her. She ran – running directly into a visqueen-covered cinder block wall. The court rejected her argument that covering a brick wall with black visqueen in a dark haunted house is an unreasonably dangerous condition which defendant had a duty to prevent plaintiff from running into. “The very nature of a Halloween haunted house is to frighten its patrons. In order to get the proper effect, haunted houses are dark and contain scary and/or shocking exhibits. Patrons in a Halloween haunted house are expected to be surprised, startled and scared by the exhibits but the operator does not have a duty to guard against patrons reacting in bizarre, frightened and unpredictable ways. Operators are duty bound to protect patrons only from unreasonably dangerous conditions, not from every conceivable danger.”

In Bonanno v. Continental Casualty Co., 285 So. 2d 591 (La. Ct. App. 1973) the plaintiff, an 84 year old woman, fell while in the “devil’s den” of a haunted house. A person disguised as the devil was mechanically projected into the room on an overhead track. The court held that the plaintiff obviously assumed the risk of being frightened, jostled and pushed about when she entered the attraction. “Whether Mrs. Bonanno fell as a result of being jostled by the crowd [her version] or in a frightened attempt to get away from the ‘devil’ [defendant’s version] is unimportant. She obviously had knowledge that she could anticipate being confronted by exhibits designed to startle and instill fear. She had to realize that the very nature of the attraction was to cause patrons to react in bizarre, frightened and unpredictable ways. It would be inconsistent in this case for this court to allow plaintiff to recover for damages which resulted from her being frightened, precisely the effect that the ‘Haunted House’ was calculated to produce.”

In Reech v. Optimist Club of Downtown Baton Rouge, 408 So. 2d 399 (La. Ct. App. 1982) the plaintiff was injured when bumped in a chain reaction of bumping started by someone that was frightened in a “scare station” of a haunted house. An actor, in a dark area, was wearing an ‘alien’ mask and had control of a strobe light that he would turn on at various intervals for the purpose of startling individuals when they came into the room. The court, reaching the same assumption of the risk conclusion as in Bonanno, held that the plaintiff could not recover. The court observed that the purpose of a haunted house is to affect people, there were no defects in the flooring and the effect of the scare station would be lost with bright lights.

In Galan v. Covenant House New Orleans, 695 So. 2d 1007 (La. Ct. App. 1997) the plaintiff, after exiting a haunted house and being thanked for coming, was injured when “Jason” (Friday the 13th), hiding behind a visqueen covered fence, started up a chainsaw for purposes of frightening the visitors one last time. The court held that, despite the timing of this fright, the plaintiff could not recover. “It appears to be plaintiff’s contention that this last exhibit, because it was unexpected, created an unreasonable risk of harm. However, the very purpose of a haunted house is to frighten its patrons. … [T]he fact that the plaintiff did not expect this last exhibit does not mandate that the exhibit is unreasonable. Accordingly, we find no breach of duty on the part of defendant by its actions in placing the last exhibit in the visqueen walled alleyway exiting the haunted house because defendant owed no duty to plaintiff to guard against her reactions at any point while in the attraction.” (emphasis in original).

In Durmond v. Billings, 873 So. 2d 872 (La. Ct. App. 2004) the court followed Galan to deny recovery to a plaintiff also injured in a “Jason” chainsaw incident. Plaintiff fell and broke her leg when approached by Jason, holding a chainsaw, in a haunted cornfield maze. “[W]e find that no duty was owed by the Billingses to Mrs. Durmon in this case to warn or protect her from her reaction to being frightened by ‘Jason,’ an experience she expected to have and for which she paid an additional admission fee.” (emphasis in original).

So the moral of this tale is clear. You go to a haunted house expecting to (and paying to) be surprised, startled and scared by the exhibits. You have the right to complain when the experience is not scary. But there is no complaining when you get what you asked for.

I am of course curious why the only judicial decisions to have ever addressed whether a visitor of a haunted house can recover for an injury sustained on account of being scared are from Louisiana. Even if I missed one or two (and I don’t think I have), Louisiana would still have many many multiples of the 2% of such cases that it would across all states evenly. If anyone has any ideas about this – serious or jokey – I’d love to hear them.

|

|

| |

|

|

|

|

Vol. 4, Iss. 10

October 28, 2015

Very Significant Duty To Defend Case:

If You Read Only One Article In This Issue Of CO….

|

|

|

If you read only one article in this issue of Coverage Opinions, make it the one about my webinar – “The Definitive Reservation of Rights Checklist: 50 Things That Every ROR Needs.” If you read two, make this one the other.

There have been a lot of cases over the past few years, between Travelers and Centex Homes, involving construction defect coverage. I do not pay attention to them. It seems like a complex story and one that would be futile to understand if you came in late – like trying to understand Breaking Bad by only watching the last episode.

But I took a look at the latest episode of the Travelers -- Centex Homes mini-series and it was a whopper. And I understood it.

In Travelers Indemnity Co. v. Centex Homes, No. 11-3638 (N.D. Calif. Oct. 7, 2015), the court addressed Travelers’s duty to defend Centex, in construction defect litigation, under a policy issued to a Centex contractor.

Travelers acknowledged that it had a duty to defend Centex in certain actions. The issue at hand was whether Travelers had nonetheless breached the duty to defend because it had been late in acknowledging it. Well how late had it been? Not very. But as the court saw it, late is late – no matter how little. And that’s just half the story.

In one situation, a complaint was filed against Centex on April 19, 2011. With a responsive pleading due 30 days after a complaint is filed, Travelers’ duty to defend was not triggered until May 19, 2011. However, Travelers did not accept Centex’s tender until June 1, 2011. This means that, as the court put it, “there were at least 13 days during which Travelers had a duty to defend Centex but did not provide a defense. As a result, Centex had to employ its own counsel.” In another situation, Travelers did not accept Centex’s defense until 67 days after a response pleading to a complaint was required.

As if that’s not enough, the court also held: “A failure to provide counsel or to guarantee the payment of legal fees immediately after an insurer’s duty to defend has been triggered constitutes a breach of the duty to defend, even if the insurer later reimburses the insured [which Travelers had done].” (emphasis added).

What about Travelers’s right to investigate whether it owed a defense, you ask. The court addressed that. “Of course, an insurer is free to conduct an investigation beyond the point at which its duty to defend has been triggered. Such an investigation may lead to facts establishing that there is no possibility of coverage, thereby ending the insurer’s duty to defend. An insurer may not, however, deprive an insured of the security implicit in the duty to defend -- specifically, ‘the right to [immediately] call on the insurer’s superior resources’ as opposed to having to marshal its own resources to mount a defense against a claim that possibly falls within the policy’s coverage.”

As a result of the court’s conclusion that Travelers breached the duty to defend, Travelers lost the right to control Centex’s defense.

Should insures make duty to defend decisions as quickly as possible? Sure. But a court that holds that an insurer breached the duty to defend, despite acknowledging a defense just 13 days after an answer was due, and reimbursing the insured for its defense costs during this gap, unquestionably fails to recognize the realities of certain administrative issues involved in claims handling – especially at a large insurer.

|

|

| |

|

|

|

|

Vol. 4, Iss. 10

October 28, 2015

Appeals Court: Primary Insurer Must Initiate Settlement Negotiations; Excess Insurer? -- No

|

|

|

It is unquestionably one of the most challenging issues to confront an insurer – the demand to settle a claim within the insured’s limits of liability. We all know the drill. An insurer has been defending its insured for a while. The case is coming down to the end and trial is on the horizon. The insurer is at the point where it knows as much about the liability and damages issues as it ever will. And with that information, the possibility of a verdict in excess of the limits of liability is known to be a real one. A demand to settle within the insured’s limit of liability, thereby relieving the insured of the risk of personal liability, is made by the plaintiff. All things considered, the applicable state standard, for whether the insurer should accept the limits demand, has been met. In other words, not accepting the demand will saddle the insurer with liability for an excess verdict. [Of course, when there are also coverage issues, the degree of difficulty here goes from multiplication to calculus. But that’s not the issue today.]

But there is another version of this story. Change one fact -- a demand to settle within the insured’s limit of liability is never made. In this situation, insurers generally see themselves as relieved of any risk of exposure for an excess verdict. After all, even though the insured has a legitimate risk of personal liability for a verdict above its policy limit, the insurer’s hands are tied. Right? Without a demand to settle within the insured’s limit of liability, what’s it to do? No matter how much it makes sense to settle the case, the opportunity to do so just isn’t there.

Granted, that’s not always true. In some states, such as Oklahoma, the “duty of good faith and fair dealing requires primary insurers to do more than ... simply not refuse unconditional settlement offers within [its policy] limits. [I]f an insured’s liability is clear and the injuries of a claimant are so severe that a judgment in excess of policy limits is likely, a primary insurer has an affirmative duty to initiate settlement negotiations.” SRM, Inc. v. Great American Insurance Co., No. 14-6160 (10th Cir. Aug. 25, 2015) (citations and internal quotes omitted).

In SRM, Inc. v. Great American, the Tenth Circuit examined, in detail, whether Oklahoma’s rule, applicable to primary policies, requires excess insurers to take that same affirmative step.

The court describes the facts like this: At a rail crossing in rural Oklahoma, “a Union Pacific Railroad train t-boned an SRM dump truck as the truck crossed the tracks in the path of the oncoming train. The collision killed the truck driver and derailed the train causing extensive damage to the train’s engines, its cars, and three of its workers.” The three injured train workers sued Union Pacific, SRM, and SRM’s primary auto insurer. SRM’s excess liability insurer, Great American, “received notice of the claims and monitored the case for potential exposure under its umbrella policy.”

SRM’s personal attorney demanded that the primary and excess insurers tender their respective limits to settle the case. He asserted that the injured train workers’ claims alone would exceed the $6 million in combined liability coverage. The primary insurer was willing to offer its $1 million liability limit to Union Pacific to settle that claim, “or to tender its limit to SRM and Great American for their use in negotiating a settlement with Union Pacific and/or the other claimants. But Great American rejected that approach and urged an aggressive defense.”

After the court rejected SRM’s cross-claim and best defense, personal counsel renewed his demand that Great American tender its $5 million policy limit to settle the case. “He warned that any delay in tendering the entire $6 million available for settlement might make it impossible to settle at a later date. Great American again declined, stating it required additional discovery to properly evaluate the claims and suggesting the claims would be resolved in mediation after discovery was complete.”

Before mediation, the primary insurer’s-retained defense team “revised its estimate of potential exposure to be between $4–4.5 million and $7 million. A Great American-retained attorney estimated economic damages at roughly $8 million, but estimated a jury would award between $2 and $4.65 million. At the mediation, the plaintiffs initially demanded $20 million but later in the day reduced their demand to $6.5 million. Great American countered with $450,000. . . . A week later, the case settled for $6.5 million. The primary insurer paid $1 million; Great American paid $5 million and SRM paid $500,000.

SRM sued Great American. It’s argument was simple: if Great American had investigated the claims, and initiated settlement negotiations by tendering its policy limits earlier in the litigation, the case would have settled within the $6 million policy limits. In other words, SRM would not have been required to pay $500,000 to settle the claims. SRM argued that Great American’s failure to take these actions violated the insurer’s implied duty of good faith and fair dealing.

But the court concluded that Great American had no such duty. It reached its decision based on strong reliance on the language of the Great American policy: “As the district court correctly concluded, the policy was unambiguous: Great American’s contractual duties to investigate, settle, or defend claims against SRM did not kick in until SRM’s primary insurer exhausted its policy limits by actually paying claims.” But, the court observed, this did not happen until the primary insurer paid its respective policy limits to settle the claims against SRM. “At that time, Great American fully discharged its contractual obligations by simultaneously contributing its policy limits toward settling the case.”

SRM sought to overcome this policy-language based argument by resorting to an “implied duty” – “[T]he duty of good faith and fair dealing is . . . independent of policy language, and therefore applies equally at all times to all insurers—whether primary or excess—regardless of when an insurer’s express contractual duties to the insured kick in.” But the court rejected the “implied duty” argument, concluding that the language of the Great American policy was paramount.

When all was said and done, the court held that, at most, an excess insurer’s duties are limited to considering and evaluating a reasonable, within-limits settlement offer.

The SRM court’s decision is entirely justifiable based on the policy language rationale. However, it is not difficult to imagine a court, in a state that imposes an affirmative duty on a primary insurer to initiate settlement negotiations, when an insured’s liability is clear, and a judgment in excess of policy limits is likely, to turn around and impose the same affirmative duty on an excess insurer. A court that imposes this duty on a primary insurer may not have a difficult time concluding that, despite what the policy language may say, the duty of good faith and fair dealing is independent of policy language and, therefore, applies equally to all insurers.

|

|

| |

|

|

|

|

Vol. 4, Iss. 10

October 28, 2015

Breach The Duty To Defend: Court Has Sobering Words For Insurers On The Rates To Be Paid To The Insured’s Counsel: “Reasonableness Inquiry Is Inappropriate”

|

|

|

The rates to be paid to the insured’s personal counsel is often-times an issue where there is not a lot of common ground between insurers and insureds. The issue arises in a few of different contexts: an insurer is obligated to defend an insured using independent counsel; an insurer is found to have breached the duty to defend and must now reimburse its insured’s defense costs; and an insured is a prevailing party in coverage litigation and is entitled to recover its attorneys fees.

You know the arguments. The insurer asserts that the rates to be paid to the insured’s counsel should approximate those paid by the insurer to its panel counsel. The insured replies that the panel counsel rates are low, and not the market rate, because they are set with an understanding that, by accepting the rates, the panel lawyers will be in line for repeat assignments.

Of all the scenarios where this issue arises, the insurer surely has the hardest road when it has been found to have breached the duty to defend and must now reimburse its insured’s defense costs. This was the very clear message recently sent by a Wisconsin federal court in Fleet and Farm of Green Bay, Inc. v. United Fire and Casualty Co., 13-1013 (E.D. Wis. Oct. 7, 2015).

The court found that United Fire, having breached its duty to defend, was responsible for paying the attorney’s fees that its insured had incurred in providing its own defense.

United Fire sought to obtain unredacted copies of the insured’s counsel’s bills. Its argument was that it needed unredacted copies to determine whether the fees sought were reasonably and necessarily incurred.

The court denied the insurer’s request – and it wasn’t quiet about it.

First, the court observed that, according to the Wisconsin Supreme Court, damages for breach of the duty to defend include “costs and attorneys fees incurred by the insured in defending the suit.” The Fleet and Farm court observed: “Notably, the [Supreme] court did not modify attorney’s fees with the adjective ‘reasonable,’ which suggests that a reasonableness inquiry is inappropriate.”

The court then added some further clarification of this point. While it offers insurers some protection, concerning the reasonableness of fees, it’s not much:

“Having refused to provide a duty to defend, the insurer also gave up its right to control the defense, as well as the ‘reasonableness’ of its attendant costs. The Plaintiff [insured] is therefore correct that United Fire is not entitled to take a fine-toothed comb over its legal bills, which, after all, it paid in the normal course of business. That said, it is not as though courts must rubber-stamp all such fee requests. Inherent in the nature of damages—any damages—is a limited reasonableness component that derives in part from the injured party’s duty to mitigate. For example, an insured cannot expend millions of dollars in fees in a hundred-thousand-dollar case and expect its bills to be paid without a peep from the insurer. The governing principle mandates that the damages awarded must ‘naturally flow from the breach.’

What this means is that an insurer in a situation like this has a very limited ability to challenge attorney’s fees that were actually incurred. This, no doubt, is not only a nod to the fact that the insurer forfeited its right to control the defense, but also a recognition that fees incurred at arm’s length in a free market are entitled to a certain level of deference that does not tolerate second-guessing. Here, at the time the fees were incurred—i.e., the underlying litigation and in this coverage action—the question of coverage was hardly so clear that the Plaintiff had any incentive to run up the bill or to proceed on the assumption that United Fire would later be on the hook for those fees. The fees were coming out of the Plaintiff's pocket, and like any similarly-situated party, it made judgments about value and quality. Allowing a secondary ‘reasonableness’ inquiry (often years later) would add expense and squander judicial resources.”

I’ll refrain from offering any commentary here. None is needed.

|

|

| |

|

|

|

|

Vol. 4, Iss. 10

October 28, 2015

Insurer Between A Rock And A Hard Case:

Limits Demand That Does Not Release All Insureds

|

|

|

It is the proverbial “damned if you do and damned if you don’t” situation for insurers. An insurer is presented with a policy limits demand to settle for one insured – and it should be accepted based on liability and damages considerations -- but the settlement offered will not secure a release for all insureds.

If the insurer accepts the settlement offer, and secures a release for one insured, then the insured that is not released can be expected to allege that the insurer acted in bad faith, by exhausting the policy without consideration of its interests. If the insurer does not accept the settlement offer, because what’s proposed does not secure a release for all insureds, then the insured who did not obtain the settlement that had been offered to it, can be expected to allege that the insurer acted in bad faith. This insured will invariably argue that the insurer is liable for any resulting excess verdict because the liability and damages justified the insurer accepting the settlement offer.

This conundrum for insurers -- one court calling the issue a Hobson’s choice -- was addressed by a Kansas District Court in Kemp v. Hudgins, No. 12-2739 (D. Kansas Sept. 22, 2015).

Kemp is a very long and detailed opinion. It would take forever to describe it here. Plus, doing so would distract from the point I’m trying to make – which is simply how one court addressed the issue. So I’ll take the easy way out – which is also the best way to describe the case. I’ll quote the court’s conclusion:

“Dairyland [Insurance Company] insists that it would have breached its duty of good faith to Kelley, had it accepted Kemp’s initial settlement demand to release only Hudgins in exchange for the policy limits. Kemp contends that Dairyland would not have breached any duty to Kelley by settling because the policy did not cover negligent entrustment claims, and suggests that Dairyland failed to reasonably investigate its potential liability on such a claim under Kansas law. . .

The Court agrees with Dairyland that its rejection of Kemp’s initial offer to settle without a release of both insureds was not in bad faith because Dairyland reasonably believed it owed a duty of good faith toward both insureds—Hudgins and Kelley—to obtain a release of both. [I]n this case the uncontroverted facts establish that Dairyland quickly offered to pay its policy limits to Kemp to settle the claim. The only point of contention between the parties was whether the policy limits settlement would be in exchange for a release of Hudgins, or of Hudgins and Kelley. Although Kemp did not ask to explicitly reserve his right to pursue a negligent entrustment claim against Kelley, the Court finds that this is a distinction without consequence. Whether or not Kemp explicitly reserved his right to pursue a claim against Kelley, under a negligent entrustment theory or otherwise, his refusal to release Kelley left her open to liability after Dairyland exhausted its policy limits in settling the claims against Hudgins. For the same reasons explained by Judge Marten in Brummett [v. American Standard Insurance Co., No. 04–1114–JTM, 2005 WL 1683610 (D. Kan. July 18, 2005)] the Court finds that Dairyland’s rejection or repudiation of the initial settlement offer was within the bounds of good faith because it did not include a release of both insureds.”

There are not a ton of cases addressing this issue, but it’s not a barren wasteland either. The cases to do so go both ways. And the arguments on both sides are easy to see. Here’s another to add to the mix.

|

|

| |

|

|

|

|

Vol. 4, Iss. 10

October 28, 2015

California Supreme Court To Address One Of My Favorite Issues - “Use Of An Auto”

Two Lewis Brisbois Lawyers Superbly Explain What’s At Stake

|

|

|

I’ve always liked “use of an auto” cases – be they in the context of coverage under an auto policy or the auto exclusion in a general liability or homeowners policy. It is usually a make or break issue for coverage and the cases have a way of involving peculiar facts. And there’s a reason for that.

After all, since automobiles are designed with a clear purpose in mind, getting to Point B, what’s “use of an auto” shouldn’t be all that hard to figure out. So, if “use of an auto” is being litigated, then, by definition, it’s probably because the claim involves something more than a person simply sitting behind the wheel, motoring down the road and minding their own business. These “use of an auto” cases are also legion. Again, not surprising, since automobiles are so prevalent, on a daily basis, in so many people’s lives.

These are a few of my favorite things when it comes to “use of an auto” cases:

|

|

|

|

| • |

|

Colon v. Liberty Mutual Ins. Co., New Jersey Superior Court, App. Div., Jan. 20, 2012 (automobile driver that bit police officer on the arm during a traffic stop did not qualify as use of an auto for purposes of a homeowners policy) (extra tidbit -- upon being stopped driver gave her name to the officer as Beyonce Knowles). |

| • |

|

Sunshine State Ins. Co. v. Jones, Florida Court of Appeal, Jan. 18, 2012 (grabbing the steering wheel to annoy your girlfriend, while she is driving, did not qualify as use of an auto for purposes of a homeowners policy). |

| • |

|

Hays v. Georgia Farm Bureau Mut. Ins. Co., Georgia Court of Appeals, Feb. 14, 2012 (using a pick-up truck and a pulley system, in attempting to lift a portable toilet onto the top of a deer stand, qualified as use of an auto for purposes of a homeowners policy). |

|

|

But not all discussion of “use of an auto” cases need focus on the oddball facts (as I enjoy doing). There are serious legal issues at work too. Two lawyers from Lewis Brisbois Bisgaard & Smith recently did a very fine job demonstrating, in a Law360 piece, that a serious discussion of the legal issues can be had as well.

According to Michael R. Velladao and Nicole R. Kardassakis, of LBB&S’s Los Angeles office, the Ninth Circuit, in Gradillas v. Lincoln General Insurance Company, 792 F.3d 1050 (9th Cir. 2015), recently certified the following question to the California Supreme Court: “When determining whether an injury arises out of the ‘use’ of a vehicle for purposes of determining coverage under an automobile insurance policy and an insurance company’s duty to defend, is the appropriate test whether the vehicle was a ‘predominating cause/substantial factor’ or whether there was a ‘minimal causal connection’ between the vehicle and the injury?”

Mr. Velladao and Ms. Kardassakis see the answer to this question as potentially leading to a significant increase in the extent to which “use of an auto” is satisfied for purposes of an auto policy.

Specifically at issue in Gradillas is whether “use of an auto,” under an auto policy, is satisfied where a bus driver rapes a woman while on a bus, where the driver had moved the bus to a secluded area prior to committing the crime.

As the LBB&S lawyers describe it, California has long applied a stringent “substantial factor” test for determining whether an alleged bodily injury “arose out of” the use of the vehicle. But the authors believe that this could all change on account of the issue certified to the California high court. They describe what could happen, if the less stringent standard is adopted, like this:

“The Ninth Circuit’s question sets the stage for potentially expanding the interpretation of what constitutes the use of a vehicle from what is — the substantial factor test — to what could be — the minimum causal connection test. If the California Supreme Court adopts the more fluid minimum causal connection test, a vehicle would no longer have to serve as the instrumentality in causing the alleged injury or damage. Rather, all that would be required is a simple connection between the alleged injury or damage and use of the vehicle. Hence, so long as the use of the vehicle facilitated the alleged injury or damage, coverage would be afforded under the insuring agreement of an auto policy. This change would not only upset nearly half a century of legal precedent, but would also dramatically expand the coverage afforded under automobile policies. Such an expansion would impose upon insurers the obligation to provide coverage for all injuries having a minimum causal connection to the use of a vehicle — coverage for which the insurers did not bargain.”

[Of course, “use of an auto” is (or should be) a zero sum game. In other words, if it is easier to satisfy “use of an auto” for purposes of an auto policy’s grant of coverage, then it should likewise be easier to satisfy the “use of an auto” exclusion in a general liability or homeowners policy. However, it seems pretty obvious that auto policies play a much bigger role in the context of automobile accidents than CGL and homeowners policies. So the authors are certainly focused on the more important side of the equation.]

|

|

|

|

|

Vol. 4, Iss. 10

October 28, 2015

Broad Interpretation Given To Liquor Liability Exclusion:

New ISO Exclusion Not Needed

|

|

|

The Liquor Liability Exclusion, contained in commercial general liability policies, has been under attack. In general, some courts have held that the exclusion does not apply to the failure to prevent the excluded conduct. In other words, say a bar patron is served alcohol, gets in his car and causes an accident that injures someone. This is conduct that is clearly excluded under the CGL policy’s Liquor Liability Exclusion. However, some courts have held that the exclusion does not apply to a claim that the insured’s negligent supervision or hiring or training of others caused the accident.

In an attempt to prevent such interpretation, the Liquor Liability Exclusion, contained in the 2013 version of ISO’s CG 00 01 form, was amended to state that it applies “even if the claims against any insured allege negligence or other wrongdoing in: The supervision, hiring, employment, training, or monitoring of others by that insured; or Providing or failing to provide transportation with respect to any person that may be under the influence of alcohol, if the ‘occurrence’ which caused the ‘bodily injury’ or ‘property damage’” is otherwise excluded.

[Of course, ISO having made this change, the door is now open to the policyholder argument that any Liquor Liability Exclusion, that does not contain this additional broadening language, provides coverage for “failure to prevent” claims. Otherwise, as the old policyholder saw goes, why was there a need to change the form?]

In Capitol Specialty Insurance Corporation v. PJD Entertainment of Worcester, No. 14-40086 (D. Mass. Sept. 1, 2015), a Massachusetts federal court did not need any new policy language to hold that a Liquor Liability Exclusion precluded coverage for a “failure to prevent” claim.

Kailee Higgins, age 20, was working as a dancer at Centerfolds. She was encouraged to consume excessive amounts of alcohol. While intoxicated and obviously impaired an employee of Centerfolds escorted her to her vehicle. Higgins was involved in an accident and suffered severe injuries, allegedly due to Centerfolds’s service of alcohol and failure to take reasonable precautions to prevent her from driving. Higgins and Centerfolds reached a settlement in the amount of $7.5 million. Higgins agreed to hold Centerfolds harmless for all but $50,000. Centerfolds assigned all rights it has against its insurer, Capitol Specialty, to Higgins.

A CGL policy issued by Capitol Specialty was subject to a $1 million limit. The Liquor Liability Policy, which Capitol Specialty acknowledged provided coverage, was subject to a $300,000 limit. At issue was the applicability of the Liquor Liability Exclusion contained in the CGL Policy.

The Liquor Liability Exclusion did not contain any specific language addressing an insured’s “failure to prevent.” Nonetheless, the court, calling the exclusion straightforward, held that it applied:

“Coverage does not apply to ‘bodily injury . . . for which any insured may be held liable by reason of: (1) [c]ausing or contributing to the intoxication of any person; (2) [t]he furnishing of alcoholic beverages to a person under the legal drinking age or under the influence of alcohol; or (3) [a]ny statute, ordinance, or regulation relating to the sale, gift, distribution, or use of alcoholic beverages.’ The phrase ‘by reason of’ is unambiguous; it ‘means ‘because of,’ and thus necessitates an analysis at least approximating a ‘but-for’ causation test.’ . . . Based on the allegations of the state court complaint, there is no question that Higgins’ injuries had their genesis in Centerfolds’ actions of serving and encouraging her to consume excessive amounts of alcohol. Without that conduct of Centerfolds’ management and staff, Higgins would not have become intoxicated, she would not have driven home impaired, and she would not have suffered bodily injuries for which Centerfolds is liable. Therefore, coverage is precluded because Centerfolds’ liability exists ‘by reason of causing or contributing to the intoxication of’ Higgins.”

The court was confronted with a “failure to prevent” argument but put a cork in it (at least under the facts before it; which is a significant point, as the court alluded to): “The Court rejects Defendants’ alternative interpretation. … Defendants claim that Higgins’ injuries were not caused by the service of alcohol, but by the negligent failure to prevent impaired driving. (citations omitted). Defendants assert that the words ‘by reason of’ must be construed narrowly, and require that the excluded conduct correspond with the precise theory of liability in the underlying action. Essentially, Defendants argue that because ‘negligent failure to prevent impaired driving’ is not specifically enumerated in the exclusion, coverage is not precluded. To be sure, this might be a different case if Higgins was intoxicated when she arrived at Centerfolds, did not drink while she was there, and Centerfolds allowed her to drive away while still obviously impaired. But those are not the facts of the underlying complaint, which alleges in unequivocal terms that Centerfolds is liable for its conduct in serving and encouraging Higgins to drink in excess.”

While the absence of “failure to prevent” language, in the Liquor Liability Exclusion, did not preclude its applicability in PJD Entertainment, the new version of ISO’s exclusion is undoubtedly going to have an impact in liquor liability claims, under CGL policies, going forward.

|

|

|

|

|

|

| |

|

|

Sexual Abuse Can Be Within The Scope Of Professional Liability Coverage

For lots of reasons, securing coverage, under a professional liability policy, for sexual abuse, is going to be an uphill battle. But as a Connecticut federal court recently explained, under some scenarios, coverage can attach: “Lastly, the parties dispute whether the underlying lawsuits properly implicate HPL [Hospital Professional Liability] coverage, or if allegations of sexual abuse are necessarily outside the scope of professional liability insurance. There is certainly not, as PEIC would have it, a bright-line exclusion, because the Connecticut Supreme Court has held that a dentist’s professional liability insurance covered claims that he sexually assaulted a patient after (or while) negligently administering excessive nitrous oxide. See St. Paul Fire & Marine Ins. Co. v. Shernow, 222 Conn. 823, 610 A.2d 1281 (1992). In that case, the Court held that ‘[w]hen [a] medically negligent procedure is so inextricably intertwined and inseparable from the intentional conduct that serves as the basis for the separate claim of a sexual assault, we join with those jurisdictions that conclude that professional liability policies must, in such instances, extend coverage.’ Id. at 830, 610 A.2d 1281. The underlying claims in this case allege that Dr. Reardon for several decades purported to conduct a child growth study under the auspices of the Hospital, and that the study was at least in large part a ruse to sexually exploit children. They do not allege that a person who happened to be a medical professional abused children on his days off, or even that he opportunistically abused his patients at the Hospital, but rather that he devised a long-term medical study to be carried out under the Hospital’s imprimatur and ostensibly under its professional supervision and that a principal purpose of that study was to find and abuse his victims. The medical study and the sexual abuse could hardly be any more ‘inextricably intertwined.’” Pacific Employers Ins. Co. v. Travelers Casualty and Surety Co., No. 3:11-924 (D. Conn. Sept. 25, 2015).

No Coverage Owed To Landlord For Tenant’s Marijuana Growing Operation

A New York Federal Court held in United Specialty Insurance Co. v. Barry Inn Realty, Inc., No. 14-4892 (S.D.N.Y. Sept. 8, 2015) that no coverage was owed to a landlord, under a property policy, for damage to his building, caused by a tenant’s marijuana growing operation. The tenant had modified a number of building components and created extreme humidity needed to grow marijuana, which caused significant damage throughout the building. The court held that no coverage was owed on account of a policy exclusion for loss or damage caused directly or indirectly by dishonest or criminal acts by anyone to whom the insured entrusts the property for any purpose. It was not disputed that the damage was caused by acts that were criminal and dishonest in nature.

At issue was whether the landlord had “entrusted” the property to the tenant. The court held that entrustment had taken place: “Here, entrustment is manifest in the course of dealings between Barry [landlord] and Castelliano [tenant]. Negotiation of the lease took place over a three-month period. Denti [landlord] questioned Castelliano about his experience in operating a bar and restaurant, was shown a bar and a restaurant that Castelliano was allegedly operating in Yonkers, and met with an individual who claimed to be working on obtaining a liquor license for the planned sports bar. After extensive negotiations, the parties entered into a five-year lease for the Premises. The lease is fourteen pages in length and contains various negotiated terms and conditions. Denti’s interaction with Castelliano, the three-month negotiation process, and the lease itself suggest a measured and deliberate decision by Barry to permit Castelliano to occupy the Premises.”

|

|

| |

|

|

|

|

|

|