|

|

|

|

|

Vol. 4, Iss.4

April 8, 2015

|

|

|

|

| |

|

| |

Sales of the 3rd Edition of General Liability Insurance Coverage – Key Issues in Every State have been through the roof! Thank you to everyone who has purchased and a special thank you to insurers who are buying the book in bulk -- even by the dozen. [There is an attractive discount for volume purchases. Drop me a note at Maniloff@CoverageOpinions.info.]

Please check out Key Issues and see for yourself why so many find it useful to have, at their fingertips, a nearly 800-page book with just one single objective -- Proving the rule of law, clearly and in detail, in every state (and D.C.), on the liability coverage issues that matter most.

Much more information, and how to order, here:

http://www.InsuranceKeyIssues.com

***

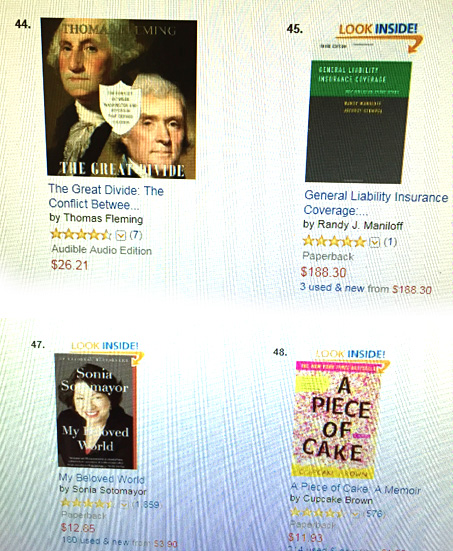

Justice Sotomayor And Key Issues

This story is just too good not to share.

Last year U.S. Supreme Court Justice Sonia Sotomayor turned me down for an interview, about her memoir My Beloved World, for Coverage Opinions. I recounted this story in CO at the time.

A few weeks back Key Issues was at #45 on Amazon’s list of the 100 Top Selling Law Books. Justice Sotomayor’s book was #47. I’d be lying if I said that I didn’t have a smile on my face seeing those two books on the same screen --

with Key Issues on top.

|

|

|

|

|

Of course this happened at some moment in time when Key Issues was on a selling tear. My Beloved World was, for good reason, #1 on The New York Times Best Seller list for Non-Fiction. Key Issues is only on The New York Times Best Seller list when my parents are describing it to someone. Put your money on My Beloved World to sell a few more copies than Key Issues. I’m optimistic. Not delusional. But sometimes life has funny moments.

|

|

|

|

|

|

|

| |

|

|

|

|

Vol. 4, Iss. 4

April 8, 2015

|

|

|

|

| |

|

| |

Here is how I see my life insurance working someday. I’m dead. My wife is loaded. And another guy is sleeping with her. There is just no other way to put it -- life insurance is a really bad deal for the dead guy.

So with terms like these, no wonder sometimes the beneficiary of a life insurance policy gets antsy waiting for the check and decides to hurry things along. Life insurance policies have been around for a very long time. And beneficiaries have been killing insureds to collect the proceeds for a very long time too. It didn’t take Lex Luther to figure this out.

But despite some seeing it as a great idea, the law wags its finger at this sort of thing. Many states have a so-called Slayer’s Statute, whereby a beneficiary, under a life insurance policy, cannot collect the proceeds if he or she murdered the insured. This won’t bring the dead guy back, but least he won’t spend eternity as angry.

Since a beneficiary is prevented from collecting under a life insurance policy, if he murdered the insured, the law books are filled with cases where that’s the matter at hand. My favorite is Prather v. Michigan Mutual Life Ins. Co., 19 F. Cas. 1244, an enjoyable one from Indiana in 1878. As I said, this is an old idea.

John Prather sought to collect $3,000, under a life insurance policy issued by Michigan Mutual on the life of his wife, Mary Prather. But Michigan Mutual was not keen on paying as it believed that Mary died from arsenic poisoning at the hands of John. The court examined several reasons why John may have killed Mary, including this one: John owed his first wife $3,000 in alimony. That sure sounds like motive. But I see it as actually supporting John’s position. If John owed his first wife $3,000 in alimony, and planned to kill his second wife to get the money to pay, surely he would have taken out a policy for more than $3,000. Committing murder just to break even makes no sense. Anyone who would take such a risk would surely want to walk away with some dough in his pocket. [Sadly, the court never answered the question whether John committed murder as the opinion was limited to jury charge issues. Maybe I’ll sign up for ancestry.com to try to figure out how it turned out.]

The internet is filled with stories of people that allegedly committed murder to collect life insurance. There was even a website devoted entirely to all things related to the subject – including a discussion of how to plan it. It was there a couple of weeks ago but has since been taken down. Too bad. You would have enjoyed it.

So with the story of beneficiaries killing insureds being as stale as an airport bagel, I was surprised that author Nelson DeMille took up the subject – as he did in a story called Death Benefits. But DeMille is a fiction writer of extraordinary talents. His books take up residency on The New York Times Best Seller list -- including at the #1 spot. DeMille’s stories and style – thrillers of many types, mixed with laugh out loud humor, often sarcasm – are as unique as DNA. So a threadbare story like this one, in DeMille’s hands, goes from I know where this is going to holy cow (or insert a different word) I never saw that coming.

Death Benefits is a short story -- really short, like, it takes 30 minutes to read cover to cover short ($1.99 Amazon download) – about Jack Henry, a bestselling author whose future looks bleak. Jack’s past few books did not do well and he owes the tax man a hefty sum. But despite this, his extravagant spending hadn’t changed to reflect his new reality. Jack comes to the realization that, after a career of wealth and fame, he is now broke. As he is sitting in his study, in his Upper East Side townhouse, pondering his situation, and what his new life will be like, he sees the bill for a life insurance policy -- $5 million – on his agent. The policy had been taken out years before when Jack had an important insurable interest in his agent’s life. Jack was the beneficiary. The premium bill was his lottery ticket, as he called it. And Jack Henry, who’d studied the subject of murder for some novels, sets out to cash it in.

Death Benefits left me thinking about DeMille’s new take on an old insurance story long after I finished it. It also left me wondering how DeMille got the idea for it? What made him write a tale with an insurance angle? None of his many books had one. I reached out to DeMille and asked him if I could run these things by him. He graciously agreed. His answers left me picking up my chin from the ground.

DeMille dropped the bombshell right out of the box: “I used to be an insurance adjuster for Liberty Mutual Insurance Company.” You always hope for a gem when interviewing someone. This was the Hope Diamond. DeMille went on to tell me that it was the early 1970s and he handled first-party homeowners and third-party claims, such as auto. In addition, his work included some insurance investigating for fraud, which he found fascinating. DeMille also cited to an early 1970s television show with Ricardo Montalban involving insurance fraud. With such things planted in his mind, he told me that he “always wanted to write a novel with insurance fraud – murder – as the background.”

It made sense. “They always say ‘write about what you know’ and I knew it then,” DeMille said. But there was one problem. He couldn’t sell a publisher on the idea. And it is still this way today – something that DeMille finds disappointing. Insurance fraud is rampant, Demille explains. And the public understands it. But the publishing business and movies and television don’t really deal with it that much, DeMille says. “They think there’s something not sexy about it, but it is, because usually the underlying story is interesting.”

So DeMille’s answer to the question, how did he come up with the idea for Death Benefits, comes down to this: “Not being able to write the novel that I wanted to, I decided to write the short story -- and that was Death Benefits.”

I knew there was a risk that DeMille’s answer could have easily been something as banal as It came to me one day when I was standing in line at the post office. But just as with his novels, DeMille told me a story that I never could have imagined.

DeMille offered another source of inspiration for Death Benefits: “I think a lot of authors’ fantasy is to kill their agent.”

Nelson DeMille has published eighteen novels. His favorite, and mine too (of any book -- ever), is The Gold Coast (about a lawyer). Take my word for it. DeMille’s nineteenth book – Radiant Angel – is set to be released on May 26.

Here’s some advice. If you ever get the chance to speak to your all-time favorite author on the phone – take it. It is a special experience.

|

|

|

| |

|

|

|

|

Vol. 4, Iss. 4

April 8, 2015

Man Sues Dog:

Court Finds That Insurer Has Duty To Defend German Shorthaired Pointer

|

|

|

|

|

|

Frequent readers of Coverage Opinions know that I have a soft spot for coverage cases involving dogs. Sadly, they often involve dog bites. There’s just not much litigation over dogs licking faces. In general, the story is similar. Dog bits man. Man sues dog’s owner. Dog’s owner sues his insurance company.

The recent decision in Morrison v. Sioux Falls Mutual, No. 2014-2469 (So. Central Dist. Ct., N.D. Mar. 23, 2015) takes a different route. A really different route. Dog hurts man. Man sues dog. Yes, you read that right -- Man sues dog. Dog’s owners sue their insurance company. Court holds that insurer had a duty to defend -- the dog.

Believe me. I know. It sounds like one of those cases that people like to point to as evidence that the legal system is broken. The ones that tort-reformers discuss and then immediately need a paper bag to breath into. But as crazy as it sounds, the court’s decision actually followed well-established coverage law.

Morrison involves coverage for an unfortunate canine incident. Tom Robertson purchased some furniture from Rick and Sharon Morrison that he found on Craig’s List. Robertson’s car wasn’t big enough to enable him to transport all of the furniture in one trip. And since he lived about 75 miles away from the Morrisons’ home in Bismark, North Dakota, Robertson completed the purchase by making trips on three consecutive Saturdays.

The Morrisons had a dog – a German Shorthaired Pointer named Felix. Robertson was a life-long dog lover but did not own one on account of his wife’s allergy to pet dander. On all three trips to the Morrison’s house, once the furniture was loaded into Robertson’s car, Robertson spent time talking to the Morrisons and playing with Felix. By the third visit, Robertson and the Morrisons had become friendly and Robertson couldn’t get enough of Felix. At one point Felix walked into the room with his leash in his mouth -- indicating that he wanted to go for a walk. Rick Morrison suggested that Robertson take Felix on his walk. Robertson agreed without hesitation. Morrison showed Robertson the route that Felix like to take and off they went.

Robertson and Felix got about a block from the house when Felix spotted a squirrel. He bolted. Hard. Robertson had no warning and the force of the 60 pound dog pulled him down. Robertson suffered bumps and bruises and a badly sprained wrist.

Robertson sued the Morrisons in small claims court. Perhaps because his injuries were not too serious, he acted pro se. Robertson alleged that the Morrisons failed to warn him that Felix, being a German Shorthaired Pointer, was a hunter. Thus, having owned Felix for two years, the Morrisons surely knew that if Robertson didn’t hold the leash tightly, with minimal slack, he would be pulled down if Felix saw a squirrel or rabbit and went after it. Robertson named as defendants Rick and Sharon Morrison. Then, in a very odd move, Robertson named “Felix Morrison” as a defendant.

The Morrisons sent the complaint to Sioux Falls Mutual, their homeowner’s insurer. The insurer denied coverage, including a defense, on the basis that Robertson’s injuries were not caused by an “occurrence,” defined as an accident. The insurer relied on the statement in the complaint that, having owned Felix for two years, the Morrisons knew that if Robertson didn’t hold the leash tightly, he would be injured if Felix’s hunting instincts took over. The disclaimer letter made no mention of potential coverage for Felix.

The Morrisons and Robertson settled the matter for $1,500. The Morrisons then filed suit against Sioux Falls Mutual. A small amount, but the Morrisons’ counsel included a count for bad faith.

The court held that coverage was not owed to the Morrisons for a defense nor its $1,500 settlement. The analysis was brief. The court essentially adopted Sioux Falls’s argument that, because the Morrisons owned Felix for two years, they must have known that if Robertson didn’t hold the leash tightly, he would be injured if Felix saw a squirrel.

But that was not the end of the case. The court observed that Sioux Falls’s disclaimer letter made no mention of any potential coverage owed to defendant “Felix Morrison.” The court acknowledged that it was an absurdity that a dog could be named as a defendant in a law suit – and then have rights to a defense under its owner’s insurance policy. But the court focused on the black letter insurance rule that an insurer is obligated to defend complaints even if they are “groundless, false or fraudulent.” As the court saw it: “It that rule is to have any meaning, then an insurer is obligated to defend a dog that is named in a lawsuit.”

Of course, the obligation to defend Felix only existed if Felix were an “insured” under his owner’s homeowner’s policy. And the court had little troubling concluding that he was. The policy’s definition of insured was: “The named insured and, if residents of your household: your relatives; and any person under the age of 21 who is in the care of the Named Insured.” The court cited to the Supreme Court of Texas’s decision in Strickland v. Medlen, 397 S.W.3d 184 (Tex. 2013), where the Texas high court observed that: “America is home to 308 million humans and 377 million pets. In fact, American pets now outnumber American children by more than four to one. In a nation where roughly 62% of households own a pet—with about 78 million dogs and 86 million cats (and 160 million fish)—it is unsurprising that many animal owners view their pets not as mere personal property but as full-fledged family members, and treat them as such.” Id. at 187 (citations and internal quotes omitted). “A study found that 70% of pet owners thought of their pets as family members.” Id. (citation omitted).

Thus, having concluded that Felix was a resident “relative” of the named insured, he qualified as an “insured” under the Sioux Falls policy. And since there was no allegation in the Robertson complaint that Felix, unlike his owners, breached any duty to warn, the court held that a defense was owed to Felix. The court also observed that “insured” included a person under the age of 21 who is in the care of the Named Insured, but the policy did not require a resident “relative” to be a person. Thus, at a minimum, the policy was ambiguous and was required to be interpreted in favor of coverage.

Lastly, the court took issue with the fact that Sioux Falls’s disclaimer letter made no mention of potential coverage for Felix. The court cited to a North Dakota insurance reg. that required Sioux Falls to respond to claims of all insureds it in a timely manner. Having failed to do so for Felix, the court refused to dismiss the bad faith count filed against Sioux Falls.

As ridiculous as the opinion is, it is hard to say that it is not supported by the policy language and case law. A ruff decision for Sioux Falls Mutual.

That’s my time. I’m Randy Spencer. Randy.Spencer@coverageopinions.info |

|

| |

|

|

|

|

Vol. 4, Iss. 4

April 8, 2015

When April Fools’ Day Goes To Court

The Wall Street Journal And Harrods Go To War Over A Joke

|

|

|

[I know. April Fools’ Day was a week ago. And it’s not exactly the kind of holiday that can be celebrated a few days late – like a birthday. Nonetheless, I didn’t want to completely ignore it. Here is the April Fools’ Day article that appeared in the April 1, 2014 issue of Coverage Opinions.]

Most April Fools’ Day jokes end with a good natured laugh between the fooler and the foolee. But, this being the land where baseball and litigation are competing for title of National Pastime, you have to expect that some April Fools’ jokes do not end right there on the first of the month. When it comes to April Fools’ Day litigation, one type of case stands out as being particularly abundant – parodies appearing in newspapers. Some are student papers and some general circulation. In general, the target of the April Fools’ joke doesn’t find it funny and it’s off to the races for the lawyers. One newspaper case in particular led to an international dispute, with litigation filed on both sides of the Atlantic, involving complex constitutional and jurisdictional issues, and opinions issued by a federal district court and the Second Circuit.

But before getting to that, take a quick look at my favorite April Fools’ Day case involving a student newspaper. In Lange v. Diercks, 808 N.W.2d 754 (Iowa Ct. App. 2011), the court addressed whether articles in an April Fools’ Day edition of a high school student newspaper encouraged students to “potentially commit unlawful acts, violate school regulations, or cause material and substantial disruption to the orderly operation of the school.” It sounds like the parody edition of the newspaper was encouraging students to blow up the school -- and providing them with the materials. Well, not exactly. Consider this capital offense that the students committed. There was a quote from one student who said he would “like to go to a Chippendale’s tryout” after graduation. As the school principal saw it - the publication of the word “Chippendales” encouraged students to come into school and take off their clothes. And there were other jokes in the parody edition of the newspaper that were just as innocuous, yet just as ridiculously viewed by the school district as creating a risk of anarchy. Thankfully the students won and the newspaper’s faculty advisor had the reprimands removed from his file.

But not all April 1st newspaper parodies are this small scale. Consider what happened when the world’s most famous newspaper and the world’s most famous department store got into a tussle over an April Fools’ Day joke. This story comes from Dow Jones & Co., Inc. v. Harrods, Ltd., 237 F. Supp. 2d 394 (S.D.N.Y. 2002).

Harrods, the well-known department store in London, issued a press release on March 31, 2002 headlined “Al Fayed Reveals Plan to ‘Float’ Harrods.” “The release stated that Al Fayed, Harrods’ Chairman and effective owner, would issue on the following day an important announcement ‘about his future plans for the world-famous store,’ including a first-come-first-served share option offer. Journalists seeking further comment were directed to contact ‘Loof Lirpa’ at Harrods. In fact, ‘Loof Lirpa’ is ‘April Fool’ spelled backward. On April 1, 2002, the planned announcement posted on the designated website described Al Fayed’s decision to ‘float’ Harrods by building a ship version of the store to be moored in London on the embankment of the Thames River. The announcement included a limited offer of ‘shares in this exciting new venture.’ Persons who registered on the website by noon that day, ‘the first of April!’, were promised ‘a share certificate.’”

The Wall Street Journal got taken by the joke. It read the March 31 press release as purporting to announce that Harrods planned to ‘float shares,’ i.e., a public offering of stock. Rather than wait to see Harrods’ actual disclosure on the next day, it published an article, in the print editions of the Journal, and on the Journal’s website, reporting that Harrods would disclose plans that day to publicly list the company’s shares.

The story doesn’t end there. It’s just getting warmed up, in fact. “Upon learning that Harrods’ announcement had been an April Fools’ joke, the Journal published a correction so advising its readers in an item that appeared in its April 2, 2002 print editions in the United States as well as on WSJ.com. Three days later, Dow Jones countered with a story it asserts was intended as the Journal’s own brand of wry, light-hearted humor. . . . The Journal’s ‘Deals & Deal Makers: Bids & Offers’ column on April 5, 2002 published an item entitled ‘The Enron of Britain?’ The first sentence of the April 5 Article, which appeared in the Journal’s United States print edition and on WSJ.com, states that: ‘If Harrods, the British luxury retailer, ever goes public, investors would be wise to question its every disclosure.’ It then detailed the April Fool’s joke, which the story reported had been mistaken by ‘some news organizations’ as an announcement of a plan to sell Harrods shares publicly. Dubbing the prank ‘[n]ot exactly Monty Python-level stuff,’ the column questioned whether Harrods could ‘get in trouble for messing with the facts?’ by issuing the bogus press announcement.”

Enter the lawyers. Or, as the court put it so eloquently: “Promptly the face of comedy began to furrow and its smile to curl into what often becomes tragedy’s first sour frowns and snarls: incipient litigation.” Harrods did not see any humor in the Journal’s article, especially the part about linking Harrods, “a law abiding and historic British institution,” as it referred to itself, with Enron. Dow Jones and Harrods next engaged in back and forth letter writing in which they argued over the Journal’s article and whether it was defamatory. Dow Jones maintained that the mention of Enron merely reflected “tongue-in-cheek hyperbole.” Harrods called Dow Jones’s contention that the article was meant to be humorous as “simply an incredible, if not bizarre, assertion.” Harrods demanded a published apology. Dow Jones continued to maintain that the article contained only “non-actionable opinion” and it repeated a willingness to publish a letter to the editor if Harrods submitted one.

On May 24, 2002, Dow Jones commenced a declaratory judgment action against Harrods and Al Fayed in the Southern District of New York. Harrods instituted litigation in the High Court of Justice in London on May 29, 2002. To make a very long story short, the New York federal court addressed whether it had jurisdiction. In an opinion that is 59 Westlaw pages long (that’s monster-size in case you don’t use Westlaw), and as complex as it is long, the court held that it did not have jurisdiction. The Second Circuit, in a mere two Westlaw page opinion, affirmed.

So how did the story turn out? According to a February 17, 2004 article on UK newspaper The Guardian’s website, the case went to trial in England and the jury found for Dow Jones. Harrods was ordered to pay Dow Jones’s legal fees. According to the article, Mr. Fayed said in a statement: “I was not concerned with winning damages in this case; I simply wanted the Wall Street Journal to accept its comparison was unwarranted and to apologise to me and to Harrods. It seems that the Wall Street Journal does not have the simple good manners and grace to do this.”

It came out during the trial that there were only ten subscribers to the U.S. version of the Wall Street Journal in Britain and there had been only twelve hits on the article on the Journal website by September 2002. I’m guessing that Harrods does not carry the paper.

|

|

| |

|

|

|

|

Vol. 4, Iss. 4

April 8, 2015

Jets And Sharks And Insurance Coverage: Judicial Writing At Its Finest

|

|

|

Forget whether you can tell a book by its cover (a lot of times you really can I think), I have long maintained that you can very often tell a coverage case by its opening paragraph. A recent one from the New Jersey Appellate Division has as good as a lede as you’ll ever see. And it only got better from there. Canon v. Palisades Insurance Company (N.J. Super. Ct. App. Div. Mar. 25, 2015) started out with this gem:

“This case involves a street fight between two groups of combatants, some of whom were employed as telemarketers with two local companies. Not surprisingly, the challenge to fight, the acceptance of that challenge, and negotiations over the combat site were all done telephonically.”

Yes, as hard to believe as it sounds, that is precisely what the case is about. But the court didn’t stop there. It took the opportunity to make the events leading up to the street brawl resemble lawyers on opposite sides trying to schedule a mediation:

“While waiting for Green, Soto received a call from someone identified only as Dom, who challenged Hyslop’s group to a fight. Hyslop’s group accepted the challenge but could not agree where to stage the combat. Dom’s group proposed fighting near Borough Hall, but Hyslop’s group rejected that location as too crowded and proposed three different locations, the Lakeview Apartments, Fielek Park, and the Skytop Gardens Complex. All three sites were rejected by Dom’s group.”

The two groups then continued phone discussions and a location agreeable to both sides was chosen. However, the fight didn’t take place as scheduled. One group arrived in a car with the occupants carrying baseball bats. The other group, expecting a traditional fist fight, was unarmed, and hurriedly left. However, the parties were willing to continue settlement efforts: “The two cars drove to the Skytop Gardens Complex while their occupants made phone calls trying to reschedule the fight.”

To make a long story short, someone was eventually shot in the head. He filed suit against some of the individuals on the other side. A default judgment was entered in the amount of $65,000. Seeking to satisfy the judgment, the victim then filed an action against the auto insurer for one of the assailant’s parents. The substantive coverage issues in the case are not significant enough to warrant discussion here – “expected or intended” and “use of an auto.”

Sadly, the opinion does not mention what caused these two groups to want to kill each other. Maybe each one tele-marketed the other.

[The opinion in Canon v. Palisades Insurance Company is per curiam, so I can’t give kudos to any particular author -- only the authors collectively: Judges Simonelli, Guadagno and Leone.]

|

|

| |

|

|

|

|

|

|

Vol. 4, Iss. 4

April 8, 2015

Minneapolis’s Star Tribune Op-ed:

The Target Data Breach: Settlement Data Suffers From A Breach Of Common Sense

|

|

|

The mid-March settlement by Target, of the numerous data breach class actions filed against the retailer, following disclosure of millions of its customers’ debit and credit card numbers, will cost the company about $25 million.

I had the privilege of publishing an Op-ed concerning the settlement in Minneapolis’s Star Tribune. Target is headquartered in Minneapolis so it was neat to share my views with so many directly involved in the litigation. The problem with the Target settlement is not that it achieved no benefit. It did. But these benefits will come at a great disproportion to the costs.

Please check out the Op-ed here

|

|

| |

|

|

|

|

|

|

Vol. 4, Iss. 4

April 8, 2015

Well That Was Easy: Construction Defect: One Insurer’s Simple Solution To It All

|

|

|

If you are reading this then you are familiar with the surfeit of litigation, over the past decade-plus, concerning the availability of insurance coverage for construction defects. In very general terms you could say that there have been two types of cases – ones where coverage turns on whether faulty workmanship qualifies as an “occurrence” and another where the scope of the insurers’ willingness to provide coverage is expressed in one of many endorsements specifically drafted for that purpose. In this second category there are endorsements addressing when property damage must take place, limitations on the insured’s permissible operations, the relationship between the insured and its subcontractors, limitations on additional insured rights, and so on.

In Hanover Ins. Co. v. Plaquemines Parish Government, No. 12-1680 (E.D. La. Mar. 19, 2015), the court addressed coverage for defects associated with the construction of a community center in Boothville, Louisiana. But the case does not fall into either of these categories. Instead, it involves a policy that sets forth an insurer’s position on covering construction defects in a much simpler manner.

The case started out involving a performance bond and morphed into one resembling traditional construction defects. The court observed that the initial filings “spawned an avalanche of litigation” – 30 parties and 90 pleadings. It reminds me of a huge construction defect case I was involved in, in New York, a few years ago. When it came time for a mediation, there were so many party representatives, defense lawyers, defense adjusters, coverage lawyers, coverage adjusters, and experts that it was necessary to rent Madison Square Garden to accommodate everyone. The arena’s club boxes were used as breakout rooms. And it was perfectly understandable that the case was so huge case. At issue was a defective doorbell on a condo unit. [I made all that up. But if you thought for a second that it was true, it’s because you do CD work and know that it could have been.]

The specific dispute before the court involved the availability of coverage, under a general liability policy, for a stucco installer. There were two claims brought by the owner (Parish) against the stucco installer: negligently installing the stucco and breaching its contract to install the stucco.

The insurer argued that no coverage was owed, for either of the Parish’s claims, on account of the policy’s breach of contract exclusion: “This insurance does not apply and no duty to defend is provided by us for ‘bodily injury’, ‘property damage’, ‘personal injury’ and ‘advertising injury’ for claims, ‘suits’, accusations, charges or any loss, costs or expense, whether express or oral, for breach of contract, breach of an implied in law or implied in fact contract. This exclusion also applies to any additional insured under this policy.”

The owner did not dispute that the exclusion clearly and unambiguously precluded coverage for the breach of contract claim. At issue before the court was whether the breach of contract exclusion precluded coverage for the owner’s negligence claim. How could it, according to the owner? The claim is for “negligence” and the exclusion applies to “breach of contract.” Case closed.

However, it could, and did. As the court saw it, based on a review of other Louisiana cases, the owner was alleging that the stucco installer was negligent by: “failing to follow generally accepted construction practices and by negligently constructing the Building, by failing to properly oversee and undertake the construction of its work, by causing and/or contributing to delays, and by failing to adhere to standards for a reasonably prudent contractor in the Plaquemines Parish area.” However, despite this “negligence” claim, “all of the duties alleged by the Parish are personal to the Parish in its capacity as owner of the building and would not have existed but for the contract at issue.” The court observed that the Parish had not alleged that the stucco installer “breached any general duty owed to the public at large.” Thus, the court concluded that the breach of contract exclusion applied to the negligence claim.

That there were both negligence and breach of contract claims alleged against the stucco installer is nothing unusual. In fact, unusual would have been if those two claims had not been alleged. And that the negligence claim did not allege that the insured breached any general duty owed to the public at large is also not unusual. Unusual would have been if it did. Thus, negligence claims generally alleged in construction defect actions aren’t much different than in Plaquemines Parish -- they would not have existed but for the contract at issue.

A simple solution to a complex issue. This construction defect case was certainly easier to resolve than trying to figure out if faulty workmanship qualifies as an “occurrence.” |

|

| |

|

|

|

|

|

|

Vol. 4, Iss. 4

April 8, 2015

Court Allows Insurer To Settle And Then Seek Recovery Of Uncovered Damages

|

|

|

It is one of the toughest issues of them all for insurers. The insurer is defending its insured under a reservation of rights. There are strong coverage defenses. The underlying case is getting close to trial. There is a demand to settle within limits. It is a settlement that should be accepted based on liability and damages considerations. But the insurer does not believe that coverage is owed. So it is not pleased at the prospect of settling. But if it accepts the demand, it could lose its coverage defenses. If it does not accept the demand, because of the coverage defenses, it may be liable for the verdict – excess or otherwise. And, of course, a declaratory judgment is unlikely to solve the problem as trial is probably approaching and a DJ could never be resolved in time.

An issue along these lines played out not long ago in American Western Home Insurance Co. v. Donnelly Distribution, Inc., No. 14-797 (E.D. Pa. February 6, 2015). The case is not the exact scenario that I described -- but it certainly provides guidance to an insurer confronting it.

Donnelly Distribution was named as a defendant in a slip and fall action. The plaintiff alleged that her foot became entangled in the loop of a plastic tie used to wrap papers allegedly distributed or used by Donnelly. Donnelly was defended by its insurer, American Western Home Ins. Co., under a reservation of rights. For whatever reason, American Western did not believe that it owed coverage, for defense or indemnity, and filed a declaratory judgment action.

The District Court in the declaratory judgment action ruled that Donnelly was entitled to defense and indemnity. Shortly before trial the action was settled for $150,000. American Western was to pay $125,000 toward the settlement. American Western appealed the decision in the declaratory judgment action and the Third Circuit reversed -- ruling that American Western was not obligated to defend or indemnify Donnelly. American Western then filed an action seeking reimbursement of the $125,000 that it paid to settle the personal injury suit.

The court in the reimbursement action held that American Western was entitled to the recovery of the amount paid. The court did not announce any general rule governing an insurer’s right to reimbursement of a settlement following a judicial determination that no coverage was owed for it. And the court acknowledged that the procedural posture of the underlying case “is an important piece of the right-to-reimbursement analysis.” However, how the court reached its decision, permitting reimbursement, provides some lessons, and possible assistance, for an insurer that is confronted with a settlement demand for a claim that it does not believe is covered.

First, the court’s decision makes clear that the insurer will be in the best posture to seek reimbursement, of an uncovered claim, if it filed a declaratory judgment action seeking a determination of the lack of coverage. The filing of such declaratory judgment action is also likely to be more effective if it was filed as far in advance of the trial as possible. But, admittedly, even when that is done, there may still not be a ruling on coverage in time to guide the insurer’s response to the settlement demand. This is where American Western v. Donnelly comes in.

American Western argued that it was entitled to reimbursement of the settlement on an unjust enrichment theory. The insurer acknowledged that its policy contained no right of reimbursement and that it was not proceeding on a contract theory. The court’s reasons for allowing reimbursement of the settlement were several and tied to certain Pennsylvania case law. But the take-aways are as follows.

While Pennsylvania courts have endorsed the general doctrine, prohibiting recovery for voluntary payments made due to a mistake of law, this was a different kind of “mistake in law” situation: “American Western did not make the payment under a mistake of law. American Western has consistently disputed its obligation to pay under the insurance policy through a reservation of rights letter and a letter disclaiming coverage. Additionally, American Western clearly communicated to Donnelly its dispute over its obligation[.]”

Second, the court observed that “[w]hile the settlement payment certainly benefitted American Western, the Court concludes that it greatly benefitted Donnelly as well. This case was settled well within policy limits. Thus, the Court thinks it unlikely that Donnelly faced a situation in which it would be hit with an excess verdict. However, the settlement guaranteed a fixed settlement amount and capped costs, whereas a trial could have led to a verdict greater than the settlement in a case in which it was ultimately decided that American Western owed no duty to indemnify Donnelly.”

Lastly, the court noted a practical aspect of its decision to allow reimbursement. The Third Circuit was aware that a settlement had been reached in the personal injury action when it issued its decision that no coverage was owed. Based on this, the court observed: “It therefore seems unlikely that American Western would have no duty to indemnify but would be barred from receiving reimbursement once its duties and obligations were litigated in this forum. If such a distinction existed, it would provide an incentive for the insurer to not settle, hoping that it owed no duty to indemnify, or stall on litigating and paying a settlement, hoping that its duties would be clarified before it made any payments. This Court does not wish to encourage either of those responses.”

Based on these rationales, an insurer that is undertaking its insured’s defense, under a reservation of rights, and has filed a coverage action, but that is not resolved before a demand to settle is made, has an argument that any settlement it makes is one for which it is entitled to reimbursement, following any judicial determination that no coverage was owed for such settlement. [Of course, the insured’s financial ability to actually reimburse the settlement payment is a key practical issue.]

Having filed the declaratory judgment action, it cannot be said that the insurer’s settlement payment was voluntarily made due to a mistake of law. To the contrary, in fact. Filing the coverage action evidences the insurer’s clear belief that no coverage is owed. Second, the settlement benefits the insured. Since coverage may not be owed, the settlement prevents a verdict greater than the settlement amount, for which the insured may have no coverage, as was the case in Donnelly.

Donnelly makes an important point. By filing a declaratory judgment action, even if it is not resolved in time before a settlement demand is made, an insurer has more options when an underlying action gets down to the wire and it faces two choices – both difficult: settle and possibly lose coverage defenses or not settle and face liability for the verdict – excess of the settlement amount or policy limits. American West filed a coverage action and thereafter had an option after being confronted with the settlement demand.

|

|

| |

|

|

|

|

|

|

Vol. 4, Iss. 4

April 8, 2015

Don Ho-ly Cow:

Designated Premises Endorsement: Insurers Need To Consider A Change [Top 10 Case Of The Year Candidate]

|

|

|

I have never been one of those people who believes that, anytime an insurer is told by a court that it must provide coverage, that it didn’t believe was owed, the insurer needs to amend its policy language. That is simply not feasible or sensible. There are myriad reasons why an insurer may lose a case. And one lose on an issue, or even a few, may not be a reflection of the policy’s ability, in the grand scheme, to do its intended job.

But sometimes a decision comes along, especially from a state high court, involving an important policy provision, that is interpreted so far afield from its intent, and with reasoning that other courts may find easy to adopt, that insurers need to take a hard look at whether a change is in order. The Hawaii Supreme Court’s decision in C. Brewer and Co., Ltd. v. Marine Indemnity Ins. Co., No. SCWC-28958 (Hawaii Mar. 27, 2015), addressing the interpretation of a Designated Premises Endorsement, in the return-to-the-drawing-board category. There is more to the decision than I’ll discuss here. But the following will make the point.

In March 2006, a large portion of the Kaloko Dam in Hawaii collapsed, releasing over three million gallons of water. It caused the loss of seven lives and extensive property damage. At the time of the dam breach, James Pflueger owned the dam. Pflueger filed suit seeking damages and indemnification from C. Brewer and Company, Ltd. According to the Pflueger complaint, C. Brewer sold him the dam, allegedly aware of the dam’s questionable structural stability. C. Brewer then filed a complaint, against seventeen insurance companies, seeking various rulings on coverage.

Particularly at issue here was coverage under a James River Insurance Company CGL policy, in effect at the time of the dam breach. Putting aside certain lower court rulings, the issue before the Supreme Court was the applicability of a Designated Premises Endorsement. Specifically, James River argued that the policy’s DPE limited coverage to liability “arising out of the ownership, maintenance, and use of the [designated] premises.” And, most importantly, the dam site was not listed as a designated premises.

It seems pretty clear, right? And I have no doubt that James River thought so too. But C. Brewer didn’t. And neither did the court. In fact, the court also saw the issue as a pretty clear one. The court agreed with C. Brewer that the “policy provides coverage for injury and damage arising out of its ‘use’ of its corporate headquarters to make negligent corporate decisions [the HQ was a designated premise] even though the resulting damage happened at the unlisted Dam site.” I know. It’s breathtaking.

The court’s decision was tied to its conclusion that “arising out of” is “ordinarily understood to mean ‘originating from,’ ‘having its origin in,’ ‘growing out of,’ or ‘flowing from.’ In the insurance context, this phrase is often interpreted to require a causal connection between the injuries alleged and the objects made subject to the phrase.”

The court also supported its decision in this way: “James River seeks to rewrite the term ‘arising out of’ to limit liability to injury and damage occurring on designated premises. Such a construction of the DPE would effectively convert the James River policy from a CGL policy to a premises liability policy that limits coverage to certain premises. James River’s argument contradicts the policy, which specifically states that it is a ‘commercial general liability’ policy.” (emphasis in original).

The court had more reasons for its decision. The policy’s inclusion of “personal and advertising injury” in the DPE means that “decisions made at C. Brewer’s corporate headquarters would likely be the cause of any advertising injury; however, the resulting injury would not occur on designated premises.” Lastly, “the James River policy’s broad coverage territory similarly encompasses the United States, Canada, Puerto Rico, and, under certain circumstances, other parts of the world.”

Even if there are aspects of the policy or facts at issue here that are unique – no two cases are ever exactly alike; and here the facts and policy language weren’t so unique – C. Brewer is a significant decision for insurers that seek to limit their CGL coverage to liability ON designated premises. That is certainly what James River thought it was selling to C. Brewer. The idea that its policy provided coverage, for injury and damage arising out of its insured’s “use” of its corporate headquarters (a designated premise) to make negligent corporate decisions that resulted in damage happening at a non-designated premise, was surely not the intent of the DPW. Not even close. Given that it is not difficult to see other courts finding this argument attractive, Aloha insurers if you use DPEs. |

|

| |

|

|

|

|

|

|

Vol. 4, Iss. 4

April 8, 2015

Just Because It Looks Like A Duck: When Bodily Injury Is Not “Bodily Injury”

|

|

|

Given how broad duty to defend standards generally are, an insurer faced with a complaint, that has a lot to say about an insured’s responsibility for causing bodily injury, may be gun shy about arguing that it does not owe a defense, under a policy that provides coverage for damages for, well, bodily injury. That is no doubt what confronted Gemini Insurance Company, concerning a complaint filed by the State of West Virginia, against Gemini’s insured, Anda Inc. But Gemini and its counsel understood the real issue. The duty to defend may be broad, but it is not robotic.

Travelers Ins. Co. v. Anda, Inc., 12-62392 (S.D. Fla. Mar. 9, 2015) involves coverage for Anda, a distributor of controlled substance prescription drugs, for claims brought against it by the State of West Virginia. The opinion sets out the facts succinctly: “West Virginia alleges that Anda ‘violated West Virginia statutes and regulations that govern controlled substances and consumer protection’ by ‘distributing controlled substances without sufficient monitoring and controls.’ For example, West Virginia alleges that Anda and other prescription drug manufacturers sold pharmacies such large quantities of abused prescription drugs that the number of prescription drugs in some communities is far greater than the population could actually warrant. This practice of unfettered distribution to ‘pill mills’ cost West Virginia an estimated ‘$430 million annually in ... 2010 with costs projected to be as much as $695 million annually by 2017.’ These figures are derived from additional costs to West Virginia’s hospitals, schools, courts, social service agencies, jails, and prisons due to the epidemic.” Six hundred and ninety-five million dollars annually by 2017. That is a staggering amount of money. The stakes here were very high.

But despite the complaint’s many allusions to bodily injury, Gemini maintained that it did not owed a defense to Anda under a policy that provided coverage for damages for bodily injury. As Gemini no doubt saw it, there is more to the duty to defend analysis than simply having allegations that read like bodily injury and then automatically concluding that a defense must be owed.

The competing arguments were straightforward. They went like this. Gemini argued that it did not owe Anda any duty to defend because West Virginia was not asserting claims for bodily injury, but, rather, for its own economic losses. Anda argued it was covered under the Gemini policy because the State was seeking damages “for bodily injury.” As Anda saw it, the State’s “claims stem from addictions, diseases, and sickness related to West Virginia citizens’ abuse of prescription drugs.”

The court sided with Gemini: “West Virginia asserts claims only for its own economic loss and not ‘for bodily injury.’ It does not purport to assert claims on behalf of individual citizens for the physical harm sustained personally by those citizens, for instance. Instead, West Virginia seeks relief from the massive costs suffered by the State due to Anda’s distribution of drugs allegedly in excess of legitimate medical need. Any reference to the drug abuse and physical harm to West Virginia citizens merely provides context explaining the economic loss to the State.”

Despite facing a complaint alleging all sorts of things about bodily injury, Gemini did not reflexively conclude that a defense was owed. Instead, the insurer understood the real issue and so did the court: “Any reference to the drug abuse and physical harm to West Virginia citizens merely provides context explaining the economic loss to the State.” |

|

| |

|

|

|

|

Vol. 4, Iss. 4

April 8, 2015

Insurer Providing A Defense Need Not Fund Insured’s Counterclaim

|

|

|

We’ve all had this situation. An insurer is defending an insured. The insured believes that it has a counterclaim against the plaintiff. Defense counsel files the counterclaim or the insured hires separate counsel, to work with the insurer-appointed counsel, to file the counterclaim. However, the insurer does not wish to pay the legal fees associated with the counterclaim. After all, the counterclaim is not a suit filed against the insured. And a claim filed against the insured is what the duty to defend is all about. It often gets worked out. Sometimes the insured agrees to pay for the prosecution of the counterclaim. Sometimes the insurer pays it because it ultimately benefits the defense of the insured. But it does not always get worked out. In Mount Vernon Fire Insurance Co. v. Visionaid, Inc., No. 13-12154 (D. Mass. Mar. 10, 2015) it didn’t. So off to court everyone marched.

In very brief terms, VisionAid, a manufacturer of eye wash, terminated its Vice President of Operations. The employee filed suit against VisionAid alleging wrongful termination. Mt. Vernon undertook VisionAide’s defense under an employment practices policy. VisionAid sought to file a counterclaim against the employee for misappropriation of funds. Mt. Vernon withdrew its reservation of rights and informed VisionAid that it would not fund the counterclaim for two reasons: “[I]t was beyond its obligations under the Policy and appointed counsel was fully capable of exercising independent judgment while defending VisionAid.” VisionAid’s answer was filed by appointed counsel, who worked with VisionAid’s personal counsel, who filed the counterclaim.

The court, following a lengthy analysis, held that Mt. Vernon was not obligated to fund VisionAid’s counterclaim. Of note, the policy at issue defined “claim” as a proceeding initiated against VisionAid. While the “initiated against” language played a part in the court’s decision, it does not appear that it dictated the result.

What makes the VisionAid opinion useful is that the court addressed, one by one, so many of the very arguments that are often raised by insureds when seeking to have a counterclaim funded as part of a defense being provided to it by an insurer.

The Broad Duty To Defend Obligates The Insurer To Fund The Counterclaim

While insurers have a duty to defend a complaint in its entirety, including non-covered claims, Massachusetts’s so-called “in for one, in for all” rule only imposes a broad duty to defend and “is simply not implicated when an insured seeks affirmative relief.”

The Counterclaim Is An Aid To The Defense Of The Insured

Insureds often argued that insurers should fund a counterclaim because it could defeat or otherwise offset liability, i.e., the counterclaim is “inextricably intertwined with the defense.” This is also part of the argument that the best defense is an offense.

The court rejected this argument as a basis for requiring that Mt. Vernon fund VisionAid’s counterclaim: “VisionAid’s misappropriation counterclaim against Sullivan is not necessary to defeat his age discrimination claim. That is because appointed counsel for VisionAid need only present evidence of a ‘legitimate, nondiscriminatory reason for terminating’ Sullivan.” Further, in rejecting the inextricably intertwined argument, the court stated: “[T]he misappropriation counterclaim does not automatically offset VisionAid’s potential liability. Were VisionAid to prevail on its counterclaim and recoup misappropriated funds from Sullivan, Mount Vernon would not be entitled to such funds to offset its liability if Sullivan simultaneously prevails on his age discrimination claim.”

The Counterclaim Creates A Conflict For The Insurer’s Retained Counsel

The court rejected VisionAid’s argument that appointed counsel has an incentive to “devaluing or impairing the counterclaim to the point that would remove it as an obstacle to settling with [the employee].” The court stated: “Mount Vernon and appointed counsel do not have an interest in devaluing the counterclaim. The strength of VisionAid’s counterclaim both weakens the wrongful termination case against VisionAid and increases appointed counsel’s bargaining power in settlement negotiations. Devaluing the counterclaim would undermine Mount Vernon’s own interest in limiting Sullivan’s recovery for wrongful termination.”

Requiring Separate Counsel To Pursue The Counterclaim Would Make The Defense Unwieldy

Insureds often argue that insurers should fund a counterclaim, as part of the defense already being provided, because too many cooks in the courtroom can make a defense unwieldy. The court dismissed this: “[U]nlike the prospect of limiting the defense of an insured to particular claims, there is nothing inherently impractical or unwieldy about VisionAid relying on its own separate counsel to assert the counterclaim. In its answer to the state court complaint, appointed counsel drafted the answer and VisionAid’s own counsel drafted the counterclaim. That indicates an ability of separate attorneys to collaborate and yet accomplish their distinct objectives. The Court declines to acknowledge VisionAid’s parade of horribles with respect to divided representation.” |

|

| |

|

|

|

|

| |

|

|

Bar’s Policy That Excludes Assault & Battery Is Not Illusory

It is not surprising that a bar owner, who did not pay a lot of attention to the ins and outs of his insurance, would be surprised to learn that his commercial general liability policy contained an Assault & Battery exclusion, as many do. That’s what happened to a tavern owner in Tennessee, who was sued for wrongful death, when a patron was beaten to death in the parking lot of his establishment. The tavern owner argued that, between the Liquor Liability exclusion [version in a standard CGL policy] and A&B exclusion, the coverage was illusory because it would not pay benefits under any reasonably expected set of circumstances. As he saw it, “common sense dictates that customers visit a tavern to drink alcohol and it is reasonably foreseeable, and expected, that intended injuries arising out of a fight on the premises would take place.” The court disagreed. Atlantic Casualty Inc. Co. v. Norton, No. 12-650 (E.D. Tenn. Mar. 23, 2015).

|

|

| |

|

|

|

|

|

|

|

|

|

|

|