|

|

|

|

| |

| |

|

Vol. 3, Iss. 11

July 16, 2014

|

|

|

|

|

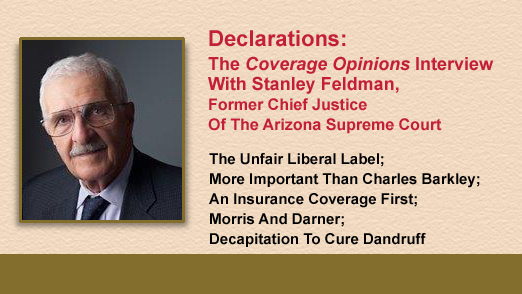

I read several profiles of Stanley Feldman and the former Chief Justice of the Arizona Supreme Court is often labeled as a liberal or some other similar-meaning term. Of course, nobody was calling then-Justice Feldman a liberal on May 29, 1984, the day that the Arizona high court issued his decision in Gilbreath v. St. Paul Fire & Marine Insurance Co. Here Feldman wrote that no coverage was owed to a day care center for liability arising out of the sexual assault of a child by a center employee. His rationale: “While it may appear curious that the proprietors of a day care center contracted for insurance which excluded the risks most likely to occur, the words used in endorsement number 2 indicate that is exactly what was done here.” Deciding a coverage case based on policy language is hardly the hocus pocus of a liberal jurist. What does this prove? Nothing that I didn’t already know – labels are for the lazy.

Chief Justice Feldman authored in the neighborhood of 400 opinions during his 21 years on the Arizona Supreme Court. To be sure, conservatives will be able to find lots that they believe make Feldman deserving of the liberal title. But to sum up a Supreme Court Justice’s two-decade career in one word is simply not fair. Those lawyers doing so would surely object to having their own careers described as mediocre simply because they lost some cases.

Over a 21 year period any Supreme Court Justice is going to hear cases involving every issue imaginable. By definition judges are the ultimate general practice lawyers. But Feldman, having spent many years as a personal injury lawyer before joining the high court, surely had lots of ideas about insurance coverage the first day he donned a robe.

I took a look at the opinions that Justice Feldman authored in coverage cases involving liability insurance policies. While there are certainly some that insurers can point to and say, See, I told you, Feldman’s a liberal, the overall score was just as I expected -- a mixed bag, with policyholders winning some and insurers winning some.

Chief Justice Feldman was kind enough to speak with me about his career – both his long-service on the Arizona Supreme Court and in private practice, including as a mediator. I also asked him about being labeled as a jurist. I don’t know much about Arizona (I’ve been to Tombstone -- which I highly recommend (for a day)), but it was an honor to speak to the man that the Phoenix New Times News said for 20 years “had as much impact on life in Arizona as anyone.” [And that’s saying a lot. Charles Barkley spent four seasons with the Phoenix Suns while Feldman served as Chief Justice.]

Joining The Supreme Court

Justice Feldman joined the Arizona Supreme Court in 1982. A seat had opened up and Feldman applied. The Commission on Appellate Court Appointments, part of the state’s merit selection system, sent three names to Governor Bruce Babbitt. Feldman got the nod.

I asked Justice Feldman if it was difficult to make the transition from many years practicing law to all of a sudden being one of the five most important people in the state making it. While he acknowledged that it took some getting used to, to go from advocating for one side to being a neutral in the middle, he didn’t express a lot of difficulty with the transition. He’d said that he’d done a lot of appellate work in private practice and as President of the State Bar of Arizona (an integrated bar, i.e., mandatory) he had a prior relationship with the high court.

Training For The Arizona Supreme Court

Chief Justice Feldman’s training for the judiciary began long before he attended the University of Arizona College of Law in the early 1950s. He spent his earliest years in the Bronx during the depression where his father ran a grocery store and his mother modeled fur coats. At age five the family moved to Tucson to address his mother’s respiratory problems. There his father opened a window coverings business.

Despite graduating first in his law school class, Feldman couldn’t get a job or even land an interview for that matter. There were few opportunities for Jewish lawyers at that time. So he opened an office by himself and focused principally on personal injury cases. Later he formed a firm that would become the one where he still practices today – Haralson, Miller, Pitt, Feldman & McAnally.

I asked Chief Justice Feldman if his upbringing, and nature of his private practice, is what led to him often being referred to as the judge who was “the champion for the little guy.” I purposely didn’t use the word “liberal” as I knew from my preparation for the interview that he really dislikes that term. But using the softer term, champion for the little guy, didn’t go over well either. He was quite clear that he doesn’t agree with that label either.

The former Chief told me that by growing up in a small business family it gave him a certain way of looking at the world. It was part of him. He made no apologies for being who he was. “I didn’t leave me behind when I came to the court,” he said.

Judicial Philosophy; An Insurance Coverage First; The Verdict

So if Chief Justice Feldman rejects the liberal label, and if he’s not the so-called champion for the little guy, what is he? He explained to me that the hallmark to his jurisprudence is four things: common sense, a sense of reality, history and precedent.

My review of Justice Feldman’s opinions in coverage cases left no doubt that the man who majored in history, and once considered a career as a history teacher, includes a historical element in his jurisprudence. He told me that he looked at history when confronted with issues in private practice and brought this technique for understanding issues to the court – which he said “was new to other members.” Indeed, you get a sense from reading Feldman’s opinions that throughout his many years in private practice there was a supreme court justice inside fighting to get out. Nobody just wakes up one day and begins to write so scholarly.

Nowhere was Chief Justice Feldman’s use of history in his decision making more apparent to me than in Ohio Casualty Ins. Co. v. Henderson (1997). The case involved the application of the “expected or intended” exclusion. In reaching his decision Feldman looked in detail at the drafting history of the exclusion going back to 1960. I’ve seen coverage cases that look at the drafting history of the pollution exclusion. I’ve seen coverage cases that look to the drafting history of the “business risk” exclusions for guidance. But I have never seen a decision – and there a ton of them in this category – that looked at the drafting history of the “expected or intended” exclusion to reach a decision. [And when I went looking for one last week, Ohio Casualty v. Henderson was the only that I could find.]

By the way, Justice Feldman held in Henderson that no coverage was owed on account of the “expected or intended” exclusion: “[C]ommon sense and reason tell us some type of bodily injury was so substantially certain to occur when the three armed men entered a presumably crowded theater during business hours that we must infer an intent to injure without regard to Henderson’s claimed lack of specific intent.” Insurers can’t complain about this outcome or the test that was adopted to reach it.

My verdict on Justice Feldman’s handling of liability coverage cases is this. If you just count decisions -- policyholders did better. But in every case, regardless of who won, I saw Justice Feldman’s use of common sense, a sense of reality, history and/or precedent in how the outcome was reached. Disagree with the outcome. Disagree with the reasoning. Call what he views as common sense nonsense. But criticism of his effort would be entirely unfair. Justice Feldman’s opinions are lengthy and unquestionably scholarly. Whatever you think of a decision, you’d be hard-pressed to say that Feldman didn’t give the issue a fair look.

Mediation And The Star-Struck Factor

Chief Justice Feldman retired from the Supreme Court at the end of 2002 and returned to private practice. His bio on his firm website lists insurance coverage near the top of the list of his practice areas. He also serves as a mediator, arbitrator, consultant and expert witness on various matters, including, first on the list – insurance law.

I wondered if Arizona practitioners found it intimidating to work with one of the state’s most famous lawyers. Were lawyers star-struck, so to speak, when mediating a case with their former Chief Justice? He didn’t think so. Instead he told me that, as a former Supreme Court Justice serving as a mediator, he feels that the parties come to the process with higher hopes and expectations that what he says will carry more weight.

Where he did see a star-struck effect was with law students. When teaching he felt that they were afraid to argue with him because of his position. “You wanna be lawyers, argue with me,” he implored students. “Tell me why I’m wrong.”

Justice Feldman’s Insurance Coverage Legacy: Morris And Darner

No discussion of Chief Justice Feldman’s record in liability coverage cases would possibly be complete without discussing his two most noteworthy:

In United Servs. Auto Ass’n v. Morris, 741 P.2d 246 (Ariz. 1987), Justice Feldman addressed whether an insured that is being defended under a reservation of rights violates the cooperation clause if it settles the case without its insurer’s consent. He answered the question like this: “An insurer that performs the duty to defend but reserves the right to deny the duty to pay should not be allowed to control the conditions of payment. The insurer’s insertion of a policy defense by way of reservation or nonwaiver agreement narrows the reach of the cooperation clause and permits the insured to take reasonable measures to protect himself against the danger of personal liability. Accordingly, we hold that the cooperation clause prohibition against settling without the insurer’s consent forbids an insured from settling only claims for which the insurer unconditionally assumes liability under the policy.” Id. at 252. However, the insured must still prove that coverage is owed and the settlement was reasonable.

One subsequent Arizona appeals court put Morris this way: “[T]he insurer must be made aware that it may waive its reservation of rights and provide an unqualified defense, or defend solely on coverage and reasonableness grounds against the judgment resulting from the Morris agreement.” Leflet v. Redwood Fire and Cas. Ins. Co., 247 P.3d 180, 185 (Ariz. Ct. App. 2011).

Justice Holohan dissented. More about that below.

Justice Feldman told me that, as he saw it, there was nothing revolutionary about his decision in Morris. “It was grounded in precedent and common sense.”

In Darner Motor Sales, Inc. v. Universal Underwriters Ins. Co., 682 P.2d 388 (Ariz. 1984), Justice Feldman authored an opinion that adopted the reasonable expectations doctrine for purposes of the interpretation of insurance policies. A detailed analysis of Darner is beyond the scope here. The decision has nearly 1,400 citing references on Westlaw. Justice Feldman told me that he saw Darner as a perfect example of his 4-part method for reaching decisions. The decision’s money paragraphs are as follows:

“[I]n proper circumstances, [the reasonable expectations doctrine] will relieve the insured from certain clauses of an agreement which he did not negotiate, probably did not read, and probably would not have understood had he read them.” Id. at 399. However, Feldman also explained that, “if not put in proper perspective, the reasonable expectations concept is quite troublesome, since most insureds develop a ‘reasonable expectation’ that every loss will be covered by their policy … the reasonable expectation concept must be limited by something more than the fervent hope usually engendered by loss.” Id. at 395.

Expanding on the reasonable expectations doctrine, then-Vice Chief Justice Feldman stated in Gordinier v. Aetna Cas. & Sur. Co., 742 P.2d 277 (Ariz. 1987) that “Arizona courts will not enforce even unambiguous boilerplate terms in standardized insurance contracts in a limited variety of situations: 1. Where the contract terms, although not ambiguous to the court, cannot be understood by the reasonably intelligent consumer who might check on his or her rights, the court will interpret them in light of the objective, reasonable expectations of the average insured; 2. Where the insured did not receive full and adequate notice of the term in question, and the provision is either unusual or unexpected, or one that emasculates apparent coverage; 3. Where some activity which can be reasonably attributed to the insurer would create an objective impression of coverage in the mind of a reasonable insured; 4. Where some activity reasonably attributable to the insurer has induced a particular insured reasonably to believe that he has coverage, although such coverage is expressly and unambiguously denied by the policy.” Id. at 283-84 (citations omitted) (italics in original).

In Philadelphia Indem. Ins. Co. v. Barerra, 21 P.3d 395 (Ariz. 2001), Justice Feldman, looking at the factors from Gordinier, held that a DUI exclusion, in a rental car agreement, that precluded coverage for a customer who got into an accident while driving a rental car intoxicated, was unenforceable, as it violated the lessee’s reasonable expectations. “Regardless of ambiguity, or even a complete lack thereof, this case is an example of one of the ‘limited variety of situations’ in which Arizona courts will not enforce boilerplate terms in standardized insurance contracts.” Id. at 404.

Justice Holohan, the Morris dissenter, dissented in Darner – and it’s one of the strongest I have ever seen. He stated: “Every insurance company in this state must review its current method of operation because today’s decision will significantly affect current policies and future policies written in this state. Of course, a company may elect to cease doing business in this state because of our ‘enlightened’ insurance law, but, hopefully, a more cautious approach may be deemed prudent until such time as appropriate legislation can be sought to establish the insurance policy as a document with some binding effect. In the interim it appears that every insurance agent will be required to do a complete review of the policy with the insured and establish some form of record to support the conclusion that the insured was advised and understood the nature, extent and limitations of the policy which was purchased. The sale of insurance in Arizona may take on much the same formality as the taking of a plea of guilty in a criminal case. Darner at 406-07. Holohan added: “Whatever evil the majority is attempting to eliminate, the remedy advanced is like decapitation to cure dandruff—a cure that is far worse than the disease.” Id. at 407.

I couldn’t hang up the phone without asking Chief Justice Feldman about Holohan’s dissent. He said he got along fine with Holohan and called him a “fine judge.” As for Holohan’s prediction in Darner about insurer’s leaving Arizona, Feldman put it this way: “I guess he was wrong.”

|

|

| |

|

| |

|

|

|

|

Vol. 3, Iss. 11

July 16, 2014

Biting Off Someone’s Nose:

It Snot An Occurrence

|

|

|

|

|

|

For years little kids have been subjected to adults grabbing their noses and then placing a thumb between two fingers and declaring: “I got your nose!” To the relief of the child the nose is then miraculously returned to its rightful place on their face. While tens of millions of nose removals have been quickly remedied, for Josh Pemberton it wasn’t just a case of Uncle Joe being crazy Uncle Joe.

A portion of Pemberton’s nose was bitten off in a bar fight in Washington. To be clear, Pemberton’s nose was not just bitten. A portion of it was bitten off. The only thing more painful that having a portion of your nose bitten off is watching commercials with the Trivago guy.

Not surprisingly Pemberton filed suit against the attacker – Kenneth Nieto (Ni-ate-o). Not surprisingly Nieto sought coverage under his homeowner’s policy. Not surprisingly the insurer disclaimed coverage on the basis that biting off someone’s nose is not an occurrence. Not surprisingly it had been pleaded in the complaint that it was. Not surprisingly coverage litigation arose over whether biting off someone’s nose can be an accident. And, not surprisingly, a case involving coverage for biting off someone’s nose ended up in Coverage Opinions.

The fight at issue in Metropolitan Prop. Cas. Ins. Co. v. Nieto, No. 13-5805 (W.D. Wash. July 2, 2014) started between two women over one of them pretending to “borrow” a cigarette out of the other’s purse. One of the women had the other pinned to the floor and was punching her with closed fists. Their boyfriend’s and husband’s got involved and began rolling around on the floor. Pemberton began head-butting Nieto in the lip. Nieto then bit down and severed a portion of Pemberton’s nose.

The last unsurprising part of this story is the Washington District Court’s decision that no coverage was owed, despite how the incident may have been pleaded: “Starting a fight, or joining a fight, and biting another’s nose are all deliberate acts, and no unforeseen event rendered them accidental. Pemberton’s complaint strategically couches the Nietos’ actions in ‘negligence’ terms, but that word choice cannot conceal the intentionality of their acts. The policy unambiguously excludes intentional actions from coverage.”

I set out to learn if Nieto is the first-ever case to address coverage for biting off someone’s nose. It seems like it may have been. It’s not. In fact, not only is it not the first, there are a few others. But what happened in West American Insurance Co. v. Maestas, No. 84-K-1584 (D. Colo. April 21, 1986) just blew me away. It makes Josh Pemberton’s injury look like a paper cut. The Maestas court put the facts like this: “The facts are worth noting. Maestas and Castro were occasional drinking buddies who were acquainted through work and softball team activities. On the night of December 5, 1982, they were drinking and socializing in a bar. The evening’s events did not remain subdued and tranquil, however. Epithets were exchanged and fisticuffs ensued. Maestas and Castro were asked to leave the bar premises. Round two took place in the parking lot. Though each claimed the other was the initial aggressor, Maestas lost; his nose and ears were bitten off.” [Castro was convicted of criminal assault and sentenced to four years in prison.]

The Maestas court held that no coverage was owed, despite the complaint’s allegation that it “sought damages from Castro due to negligence!” The court used few words to reach its decision but they were nothing to sneeze at: “West American Insurance Company is the issuer of a homeowner’s policy to Castro which protects the homeowner from lawsuits based on the negligent conduct of the policy holder. Thus, mirabile dictu, we now see why Maestas ascribes the loss of his nose and ears to Castro’s failure to exercise the care that a reasonably prudent person would under similar circumstances. Of course, it cannot be gainsaid that a reasonably prudent person would eschew similar circumstances. Thus, the law’s time-honored test of reasonable prudence is inapplicable to the facts presented. After the fashion of William of Occam preference should be given to a test of known quantities: three bites do not a negligence case make.”

A review of nose-biting coverage cases reveals the following lesson:

If you seek coverage for biting off a nose;

Your insurer will certainly oppose;

You will have it tough when it comes time to depose;

So here is what I propose;

Stick to the method of Uncle Joe’s.

That’s my time. I’m Randy Spencer.

Contact Randy Spencer at Randy.Spencer@coverageopinions.info

|

|

| |

|

|

|

|

Vol. 3, Iss. 11

July 16, 2014

July 4th: You May Not Have Known This

|

|

|

This is coming a little late for July 4th but here’s an interesting patriotic factoid that perhaps you may not have known: some states have statutes that exempt America flags (and their own state flags) from their sales tax requirement. According to an internet article that I found on the subject there are ten states that preclude sales tax on the retail sale of flags and four with statutes that apply the exemption in narrower situations.

I didn’t research the legislative history of these statutes but the rational for them seems kinda obvious – encourage patriotism. However, also in the “didn’t know this category” are some flag retailers. For example, my home state, Pennsylvania, has a statute that exempts American flags from sales tax. See 72 Pa. Stat. § 7204(32). Nonetheless it is not uncommon, especially in a small retailer, to purchase a flag in Pennsylvania and be charged sales tax. [Incidentally, the Pennsylvania statute that creates the sales tax exemption for flags also takes dental floss off the hook for sales tax. Id. at sub-§ (4).]

I know what you are thinking. This sounds like a star spangled class action suit against any retailer that has been charging 6% more for flags than allowed by law. While the average flag purchaser’s damages would be under a buck, when has that ever been an impediment to a consumer class action? Ridiculous consumer class actions are as American as hot dogs. So imagine a class action about flags. It would be the Yankee Doodle of lawsuits. [Actually, it might be sorta complicated since the retailer probably paid the tax to the state, so maybe the retailer has a right to a refund, which could fund the damages to the consumer. But attorney’s fees would still be owed. Well, whatever.]

So if you are buying a flag and live in Connecticut, Florida, Maryland, Massachusetts, New Jersey, New York, Pennsylvania, Rhode Island, West Virginia or Wisconsin check your receipt. |

|

| |

|

|

|

|

|

|

Vol. 3, Iss. 11

July 16, 2014

Stars Of TBS -- Sullivan & Son And Pete Holmes -- Read Coverage Opinions

|

|

|

|

If you are not watching Sullivan & Son (TBS--Tuesday at 10PM EDT) you are missing a very funny sit-com. It is Cheers – without a censor. But it’s not all beer, laughs and bawdry humor for show star Owen Benjamin. As you can (sorta) see here (in this, unfortunately, poor quality photo), when Owen is not doing all of those things he turns to his passion for liability insurance coverage. And he knows just where to go to get the latest news. Check out Sullivan & Son (Season 3 just started).

|

|

|

|

|

Another (former) star on TBS, Pete Holmes (voice of the E*Trade baby and fantastic stand-up comedian), and host of the sadly, just cancelled, The Pete Holmes Show, also satisfies his cravings for insurance coverage by reading Coverage Opinions.

|

|

|

|

|

| |

|

|

|

|

|

|

Vol. 3, Iss. 11

July 16, 2014

Feng Shui And Insurance Coverage

|

|

|

I read a lot of coverage cases. And if you read Coverage Opinions with any regularity you know that I have a soft spot for coverage cases with unusual facts. The recent case of Patel v. American Economy Ins. Co., No. 12-4719 (N.D. Cal. May 8, 2014) is in the unusual facts category.

Namrata Patel’s dental office sustained smoke damage from a fire in the basement of a commercial building. Patel sought coverage from her property insurer, American Economy Insurance, for direct physical damage, loss of business income for twelve months (she was forced to relocate her business when the building closed for repairs) and necessary extra expenses. So far nothing out of the ordinary. Hold on.

Patel also sought coverage for $50,275 for a Feng Shui consultant she hired before reopening the office after the fire. She used a Feng Shui consultant to “restore energy balance” and determine “placement of furniture and dealing with forces of Qi.” [I had to look up Qi. Despite there being a long Wikipedia entry on the subject I still don’t understand exactly what it is.]

The court held that coverage for the Feng Shui consultant was not owed “[b]ecause Patel has failed to provide evidence that the cost of Feng Shui consultant services are a ‘direct physical loss’ or a ‘necessary’ ‘extra expense’ under the terms of the policy.”

The court’s conclusion was that “[c]ourts have interpreted the words ‘direct physical loss’ and similar provisions in insurance contracts to mean damage to tangible, material objects.” The court rejected Patel’s argument that the words ‘direct physical loss’ include Feng Shui services because ‘in order for Patel to replace the damaged personal property she utilized Feng Shui which she first utilized when she first placed the property.’”

Further, “[t]hat Patel chose to use a feng shui consultant does not mean that the expense for those services were ‘necessary’ ‘[t]o avoid or minimize the suspension of business’ as defined under the ‘Extra Expense’ provision of the policy. She argues that the policy is ‘vague’ because it does not specifically exclude coverage for feng shui consultants. Accepting her argument would lead to the illogical result that American Economy must explicitly define all possible services that do not fall under its coverage.”

I have no doubt that Feng Shui is an important part of many people’s lives. But as far as Feng Shui costs being the subject of damages in an insurance claim, Patel v. American Economy Ins. Co. is the first-ever reported decision to address the issue. So Dr. Patel did not go home empty handed in the Feng Shui department.

As a curious George-type I wondered the extent to which Feng Shui has been at issue in all legal cases -- of every shape and size. Conclusion: Feng Shui has just about eluded the legal system -- period. It kinda makes sense that it would know how to do that.

Here are a couple of decisions where Feng Shui was a key component:

Clay v. Mercado, 224 S.W.3d 277 (Tex. Ct. App. 2005): A huge salt water aquarium was delivered to a customer by its manufacturer. The customer was practicing Feng Shui and wanted to place the aquarium in a certain location on a tile floor. The manufacturer told her that it would leak because the floor was uneven. The customer insisted that it be installed there anyway. The manufacturer complied even though he knew it would leak. You know where this is going. Twenty months later the entire side of the aquarium tank blew out, spilling 220 gallons of saltwater, fish and coral unto the floor. The fish died. The court went on to address claims under the Texas Deception Trade Practices Act.

Le v. C.I.R., No. 5957–09S (U.S. Tax Ct. 2010): The U.S. Tax Court held that a taxpayer was a professional gambler and, thus, his gambling losses were deductible as business expenses. The court rejected the IRS’s argument, that the taxpayer’s use of Feng Shui, to determine “lucky days” on which to gamble, was irrational and not businesslike. The court explained: “The standard, however, requires only that the profit objective be actual and honest. It would be difficult to find on the record before the Court that petitioner’s approach to making a profit was irrational. For example, if someone’s investment in a stock or a business were based on Feng Shui or some other cultural judgment, that would not per se be ‘irrational’. Petitioners used their best judgment and successfully tested their business approach. Ultimately, the fact that their approach was unsuccessful does not make it irrational.” |

|

| |

|

|

|

|

|

|

Vol. 3, Iss. 11

July 16, 2014

The Shot Dog Heard ‘Round The World:

Missouri High Court Finally Rules In Sluggerrr

(The Kansas City Royals Mascot) Case

|

|

|

|

|

|

| |

|

Sluggerrr studies the court's decision in Coomer v. Kansas City Royals |

|

|

|

The litigation saga of Kansas City Royals mascot Sluggerr, an adorable furry lion, captivated me. Sluggerrr tossed a hotdog into the stands, hit a fan in the eye and caused serious injuries.

I love litigation with odd facts and I have long-been a student of litigation involving the interaction of fans and sporting events. If you read Coverage Opinions with any regularity you’ve seen several examples of this. For these reasons, the Sluggerrr case is one of my all time favorites. I was thrilled to be quoted in the Associated Press story about the Missouri Supreme Court’s recent decision in Sluggerrr.

Sluggerrr’s problems all started at a September 2009 Kansas City Royals game when he threw, behind his back no less, a four ounce foil wrapped hotdog into the stands. This was done as part of Sluggerrr’s “Hotdog Launch,” a feature of every Royals home game since 2000. Between innings Sluggerrr stands on the roof of the visitor’s dugout and uses an air gun to shoot hotdogs to fans seated beyond hand-tossing range. When his assistants are reloading the air gun, Sluggerrr tosses hotdogs by hand to the fans seated nearby.

On this day one of the wiener’s that had been tossed by Sluggerrr hit fan John Coomer. Coomer testified that he saw Sluggerrr turn away from the crowd as if to prepare for a behind-the-back throw. But, unfortunately for Coomer, he chose that moment to turn and look at the scoreboard. He never saw Sluggerrr throw the hotdog. A “split second later ... something hit [him] in the face,” and he described the blow as “pretty forceful.” Coomer suffered a detached retina and needed eye surgeries. Of course litigation ensured.

For his negligence count Coomer alleged that the Royals “(through its employee, Sluggerrr) failed to exercise ordinary care in throwing hotdogs into the stands, that the team failed to adequately train Sluggerrr on how to throw hotdogs into the stand safely, and that the team failed to adequately supervise Sluggerrr’s hotdog toss.” [It’s amazing that the Royals allegedly couldn’t train Sluggerrr how to throw hotdogs into the stands safely, but could apparently train a massive carnivore not to eat the hot dogs.]

In general terms, here’s the issue at the heart of Sluggerrr’s case. Fans seeking damages for injuries sustained by a foul ball have a very difficult time recovering from the stadium operator. The majority of courts that have confronted the question have adopted the so-called “Baseball Rule,” which limits the duty owed by baseball stadium operators to spectators injured by foul balls. The Baseball Rule generally provides that a baseball stadium operator is not liable for a foul ball injury as long as it screens the most dangerous part of the stadium and provides screened seats to as many spectators as may reasonably be expected to request them. Sluggerrr’s case raised the question whether this “baseball rule,” or “no duty rule,” should also apply to an injury caused by a mascot.

Sluggerrr was successful at trial in Missouri state court. A jury found the furry lion to be zero percent at fault and Mr. Coomer to be one hundred percent at fault. However, the Missouri Court of Appeals reversed, holding that it was error for the trial court to charge the jury on primary implied assumption of the risk when it comes to a flying hotdog. The appeals court explained: “Everyone who participates in or attends a baseball game assumes the risk of being hit by a ball, because the risk of being hit by a baseball is a risk inherent to the game. However, the risk of being hit in the face by a hot dog is not a well-known incidental risk of attending a baseball game. Consequently, a plaintiff may not be said to have consented to, and voluntarily assumed, the risk merely by attending the game.”

The case went to the Supreme Court of Missouri which held oral argument on September 11, 2013. The Phillie Phanatic filed an amicus brief supporting Sluggerrr. I’d been waiting anxiously for the Missouri high court’s decision in Sluggerrr’s case.

[Incidentally, it was stated during the Supreme Court oral argument that no court has ever applied the “no duty” rule to the activities of a mascot. This is not so clear. In 2004, in Kohri v. The Phillies, a Pennsylvania trial court held that the “no duty” rule applied to an injury that was allegedly caused by the antics of the Phillie Phanatic. The case was affirmed by the Pa. Superior Court and the Pa. Supreme Court declined to hear an appeal.]

The Missouri Supreme Court’s decision in Sluggerrr finally came on June 24. The court issued a 36-page unanimous decision. A good chunk of the decision is devoted to how Missouri law treats the “century-old” affirmative defense of assumption of the risk. Putting aside many pages of analysis, the court held as follows:

“[I]f Coomer was injured by a risk that is an inherent part of watching the Royals play baseball, the team had no duty to protect him and cannot be liable for his injuries. But, if Coomer’s injury resulted from a risk that is not an inherent part of watching baseball in person—or if the negligence of the Royals altered or increased one of these inherent risks and caused Coomer’s injury—the jury is entitled to hold the Royals liable for such negligence and, to the extent the reasonableness of Coomer’s actions are in dispute, the jury must apportion fault between the parties using comparative fault principles.”

With that standard now set the Missouri Supreme Court turned to address whether being injured by Sluggerrr’s hot dog toss is an “inherent risk” of watching a Royal’s home game. To do so the court addressed whether such risk is “structural” and “involved in the constitution or essential character” of watching such game.

The court concluded that it is not: “The rationale for barring recovery for injuries from risks that are inherent in watching a particular sport under implied primary assumption of the risk is that the defendant team owner cannot remove such risks without materially altering either the sport that the spectators come to see or the spectator’s enjoyment of it. No such argument applies to Sluggerrr’s hotdog toss. Millions of fans have watched the Royals (and its forebears in professional baseball) play the National Pastime for the better part of a century before Sluggerrr began tossing hotdogs, and millions more people watch professional baseball every year in stadiums all across this country without the benefit of such antics.

Some fans may find Sluggerrr’s hotdog toss fun to watch between innings, and some fans may even have come to expect it, but this does not make the risk of injury from Sluggerrr’s hotdog toss an ‘inherent risk’ of watching a Royals game. As noted above, ‘inherent’ means ‘structural or involved in the constitution or essential character of something: belonging by nature or settled habit,’ Webster's Third New International Dictionary (1966), at 1163 (emphasis added (by court)). There is nothing about the risk of injury from Sluggerrr’s hotdog toss that is ‘structural’ or involves the ‘constitution or essential character’ of watching a Royals game at Kauffman Stadium.”

Please indulge me one more long quote to describe the court’s decision: “[T]he Court holds as a matter of law that the risk of injury from Sluggerrr’s hotdog toss is not one of the risks inherent in watching the Royals play baseball that Coomer assumed merely by attending a game at Kauffman Stadium. This risk can be increased, decreased or eliminated altogether with no impact on the game or the spectators’ enjoyment of it. As a result, Sluggerrr (and, therefore, the Royals) owe the fans a duty to use reasonable care in conducting the Hotdog Launch and can be held liable for damages caused by a breach of that duty. Sluggerrr’s tosses may—or may not—be negligent; that is a question of fact for the jury to decide. But the Royals owe the same duty of reasonable care when distributing hotdogs or other promotional materials that it owes to their 1.7 million fans in all other circumstances, excepting only those risks of injury that are an inherent part of watching a baseball game in person.”

I was very surprised by the Coomer decision. The court’s decision, that the antics of a mascot are not an inherent part of watching a sporting event, because they are not part of the “constitution or essential character” of what’s taking place on the field, misses the point. I agree with the Royals when they say that, while the hotdog toss, admittedly, has nothing to do with what’s going on inside the diamond, it is a part of the overall stadium “experience.”

Let’s face it. Baseball is as much a business as it is a sport. The Royals need to sell tickets or else there will be no “constitution or essential character” of anything going on in Kauffman stadium. Mascots are part of a team’s effort to sell tickets. My eight year old daughter wants to go to a Phillies game for only one reason – the see The Phillie Phanatic. The breaks between innings, and fan disinterest when a game has ceased to be competitive, are also an inherent part of the game. The use of mascot antics to address these very situations makes the mascot a direct extension of the game itself. Indeed, at minor league games, the many (sometimes crazy) things happening off the field might just be the “constitution or essential character” of the game.

Coomer, being a lengthy, tremendously detailed and unanimous opinion, from a supreme court, is now surely the go-to case for all other courts nationally, to consider for guidance, when confronted with a mascot injury case. This is the Marbury v. Madison of mascot injury cases. Will this decision cause teams to rethink some of their mascot promotions and antics or take additional measures to keep spectators safe? I doubt it. What happened to Mr. Coomer can be chalked up as a freak accident.

Thus, the biggest take-away from Sluggerrr is not so much a test for assumption of the risk vis-à-vis mascot injuries -- but that the test can have wider application. Assumption of the risk clearly applies to any injury caused by a foul ball or flying bat. But for a court looking to Coomer for guidance, for other game-related injuries, the question will be whether it arose out of the “constitution or essential character” of the game. Based on the narrow interpretation of this by the Coomer court, assumption of the risk will often strike out as a defense.

|

|

| |

|

|

|

|

|

|

Vol. 3, Iss. 11

July 16, 2014

A-L-Aye Yi Yi: The Next Chapter In “The Principles Project”

|

|

|

The American Law Institute’s “Principles of the Law of Liability Insurance” project rolls along. Actually, given the glacial speed of the process, it is more accurate to say that it is chugging along. But even the hare eventually covered a lot of ground and that’s what is happening here.

As I reported in the June 4th issue of Coverage Opinions, the principals of the Principles, Professors Tom Baker and Klye Logue, informed me that at its May meeting the ALI membership approved all of the remaining sections of Chapter 2 without amendment (in general, involving various issues concerning the duty to defend and reservations of rights). Chapter 3 (which includes allocation and contribution; exclusions; conditions; insuring clauses; and application of limits and deductibles) will be worked on for the next year, with the goal of submitting a complete draft of Chapter 3 to the ALI Council for its approval in Fall 2015, and then to the membership in May 2016.

Several of the sections of Chapters 1 and 2 have been met with insurer concerns, generally on the basis that they adopt minority positions. It would be well-beyond the scope of this brief article to address such concerns here. I did address one troubling aspect of Chapter 2 in detail in the April 23rd issue of Coverage Opinions – the hourly rate that independent counsel can charge. I was pleased to learn that my article led to a relatively small editorial change.

With Chapter 3 next up, I take a brief look here at one provision of the draft that strikes me as very problematic for insurers. The draft text of section 36 defines the term “accident,” unless stated otherwise in a liability policy, and when used in an insuring clause, as follows: “an action or event that causes a result that the insured does not subjectively expect or intend.” In fairness I have to admit that I have not seen any of the Comments or Reporters’ Notes concerning this definition.

As I also wrote about, separately, in the June 4th issue of Coverage Opinions, courts have been struggling with the meaning of the term “accident” for a very long time. A very, very long time. The term “accident” is usually not defined in a liability policy. These days a policy provides coverage for an “occurrence,” which, in turn, is defined as an “accident, including continuous…” (you know the rest).

I have come to the conclusion that the question whether injury or damage was caused by an “accident” gets the nod as the oldest continuously running insurance coverage issue. It is the Mousetrap of insurance coverage. The earliest American case that I could find, addressing whether an “accident,” for purposes of insurance coverage took place, is from 1835 (Howell v. Cincinnati Ins. Co., Ohio Supreme Court). And English cases go back further. But it’s not just that there are a lot of really old cases addressing the “accident” question -- it’s that some of them look remarkably similar to ones that were decided yesterday. In other words, not only have courts been grappling for 180 years with the coverage question whether injury or damage was caused by an “accident,” but they haven’t figured out the answer after all this time.

The ALI Principles depart from most liability policies and define “accident.” But to do so as “an action or event that causes a result that the insured does not subjectively expect or intend” is likely to result in coverage for undeserving situations.

Courts have long-been confronted with claims by insureds who did the most outrageously intentional acts, and then maintained that coverage was owed because they did not expect or intend the injury that resulted. So it was an accident. However, many of these courts have also long seen through these assertions of subjective intent as being implausible. Indeed, some judges even use language to suggest that they are snickering inside at the argument that someone could have engaged in such an outrageous act and then asserted: yeah, but I didn’t mean to cause that injury. Courts usually solve this problem by concluding that, despite the insured’s assertion otherwise, when an injury is substantially certain to occur (or some similar language), it was not caused by an accident.

But to specifically define “accident” using a subjective test is to open the door to the argument that coverage is owed to a guy who cold-cocked another in the face – but now claims that he only meant to break the other’s nose and, thus, did not subjectively expect or intend to cause the brain damage that occurred when the victim fell to the ground [This sounds like an extreme example but it’s not. Lots of cases resemble this situation.] By using an express subjective definition of “accident,” an injury, despite the substantial certainty that it was going to occur, may be determined to have been caused by an accident. While courts may find an insured’s assertion, that an injury was not subjectively expected or intended, to be ludicrous, they may nonetheless be compelled, if following the ALI Principle, to rule in the face of incredulousness. After all, with policy language being the test for determining coverage, courts may be constrained to conclude that it trumps common sense.

Surely even the strongest pro-policyholder advisors involved with the ALI Principles can’t believe that coverage is owed based on self-serving statements of intent that fly in the face of reality. |

|

| |

|

|

|

|

|

|

Vol. 3, Iss. 11

July 16, 2014

The Latest Pollution Exclusion Scorecard

|

|

|

|

|

|

Jeff Stempel and I are currently in the process of preparing a 3rd edition of “General Liability Insurance Coverage: Key Issues In Every State.” Lauren Kelly, soon to be second-year student at Villanova Law School, is spending the summer helping me with the project as a Research Assistant. [Eight weeks with me. Can you imagine. School can’t start fast enough for the poor girl.]

Lauren just finished her research on the Absolute/Total Pollution Exclusion chapter. Based on her findings, which includes a staggering 67 new cases since the 2nd edition (early 2011), here is the current national scorecard on the Pollution Exclusion:

Since 2011, 36 states had a state or federal court decision addressing the Pollution Exclusion. Of these recent decisions, seven came from state Supreme Courts.

In general, the overall national Pollution Exclusion picture looks like this: 24 states apply the Pollution Exclusion broadly, to all hazardous substances, and not simply so-called “traditional environmental pollution.” Twenty states apply the Pollution Exclusion narrowly, limiting its application to traditional environmental pollution. In three states the issue is not so clear cut. And three states have never addressed it.

There have always been Pollution Exclusion cases addressing whether somewhat odd substances are considered a “pollutant.” This has not changed. Since 2011, courts have addressed whether such things as aroma from curry, cooking oil, deli odors, ejaculate, swine waste odors and bat guano qualified as a “pollutant.”

The moral of the story is quite obvious. There continues to be no end to the extent that Pollution Exclusion decisions leach from federal and state courthouses all over the country. With many coverage issues, once the state high court speaks, litigation tails off. But there has never been the case with the Pollution Exclusion.

|

|

| |

|

|

|

|

Vol. 3, Iss. 11

July 16, 2014

The “You” Issue: Following South Dakota Supreme Court’s Decision ISO Needs To, Err, Rushmore To Fix Its CGL Policy

|

|

|

I’m not one of those people who thinks that every time an insurer loses a liability coverage case the sky is falling and ISO needs to stop what it’s doing and amend its bread and butter CGL form to prevent a repeat of the situation. Not at all.

General liability coverage cases involve the application of the facts of a potentially infinite number of accident scenarios to an insurance policy with static provisions, zealous advocates on both sides and a human decision maker. All of that translates into a situation where insurers and policyholders will each win some and lose some. Based on these many variables at play, not to mention that the policy provision at issue may not arise with great regularity, every insurer loss is not a harbinger of a nuclear winter.

But sometimes I see a decision, involving the language in ISO’s form CG 00 01, that I believe both creates unintended coverage and could have wide-ranging enough implications, such that it justifies the organization’s consideration whether a change is in order. The South Dakota Supreme Court’s recent decision in Dakota Fire Ins. Co. v. J & J McNeil, LLC, No. 26827 (S.D. June 25, 2014) is in this category.

Before getting to the specifics of the South Dakota case, here’s an explanation of the issue in general. ISO’s Commercial General Liability form CG 00 01 states, right at the outset, that the terms “you” and “your” refer to the Named Insured shown in the Declarations and any other person or organization qualifying as a Named Insured under the policy. The policy also provides a fairly lengthy section, mid-way through, describing who qualifies as an “insured.” And, of course, parties often-times qualify as an “additional insured,” in one way or another, under a named insured’s policy. That the policy has a Separation of Insureds clause further makes clear that there may be many insureds at issue.

The persons and entities who qualify as “insureds” and “additional insured” are just that -- “insureds” and “additional insureds.” In other words they are not “named insureds.”

Now turn to some of the exclusions in ISO’s CGL form. In the “business risk” category there is an exclusion for “‘property damage’ to ‘your work’ arising out of it or any part of it and included in the ‘products-completed operations hazard.’” There is an exclusion for “‘property damage’ to ‘your product’ arising out of it or any part of it.” And there is an exclusion that provides, in part, that no coverage is owed for “property damage” to “property that has not been physically injured, arising out of: [a] defect, deficiency, inadequacy or dangerous condition in ‘your product’ or ‘your work’; or [a] delay or failure by you or anyone acting on your behalf to perform a contract or agreement in accordance with its terms.”

What all of these exclusions have in common is that they apply to the work or product of a named insured. That’s because they are written, and defined, in terms of “you” and “your.” And as the policy makes clear in its preamble, the terms “you” and “your” refer to the Named Insured shown in the Declarations. In addition to the business risk exclusions, the ISO policy contains numerous other places where coverage, exclusions and conditions are described in terms of “you” and “your,” i.e., the named insured.

As a result of this distinction in the policy between “you” and “your,” being a named insured, and simply an insured, the stage is set for disputes whether certain insureds are subject to certain policy provisions. The argument is certainly there for the making that exclusions, written in terms of “you” and “your,” do not apply to a person or entity that is simply an “insured” – and not a named insured. If so, then an additional insured, who was perhaps added to a policy for no premium, or less than the cost of a hot dog and soda at a baseball game, gets more coverage (because not subject to the business risk exclusions) than a named insured, that paid many thousands of dollars in premium. Of course that makes no sense. But the often-applied rule of insurance policy interpretation is that, when the policy language is clear, look no further.

This is no far-fetched issue. Many courts have addressed the fact that “you” and “your” refer to the named insured when determining the availability of coverage. The cases involve a hodge-podge of circumstances. But the fact is that many exist, as pointed out by the First Circuit in Wright-Ryan Const., Inc. v. AIG Ins. Co. of Canada, 647 F.3d 411, 417-18 (1st Cir. Jul 27, 2011):

"Decisions interpreting the use of “you” and distinguishing between the “Named Insured” and “Additional Insured” are common, due to the ubiquitous use of those terms in insurance policies:

Insurance carriers often employ the terms “you” and “your” throughout the language of a policy. These terms are typically defined as referring to the named insured shown in the declarations of the policy, and any other person or organization qualifying as a named insured under the policy. Accordingly, “you” and “your” do[ ] not encompass individuals or entities added as an additional insured to the policy.

3 Russ & Segalla, supra, § 40:26 (footnote omitted). The mainstream of opinions interpreting this or similar definitions has held “you” to be unambiguous and to refer solely to the individual or organization identified as the “Named Insured” in the policy Declarations. See, e.g., Nat’l Union Fire Ins. Co. v. Liberty Mut. Ins. Co., 234 Fed.Appx. 190, 193 (5th Cir.2007) (taking “as a given” that, under definition of “you” identical to the definition here, “you” was limited to the named insured and did not encompass an additional insured); Alexander v. Nat'l Fire Ins., 454 F.3d 214, 226–27 (3d Cir.2006) (same); Seaco Ins. Co. v. Davis–Irish, 300 F.3d 84, 86 (1st Cir.2002) (holding that definition of “you” was unambiguous and referred only to named insured)."

To take one specific example, in Old Republic Insurance Co. v. Kemper Casualty Co., No. 04-1902 (3rd Cir. May 13, 2005) the federal appeals court rejected an insurer’s argument that the term “your work,” as used in an exclusion, could not be limited solely to a named insured, because that would provide greater coverage to an additional insured than a named insured. The court was not buying the insurer’s argument that the exclusion, because it was applicable to a named insured, operated indirectly to preclude coverage to an additional insured. The court’s decision was based on the fact that the terms “you” and “your” were clearly defined in the policy as referring to the named insured shown in the declarations.

With this background now turn to the South Dakota Supreme Court’s late-June decision in Dakota Fire Ins. Co. v. J & J McNeil, LLC. John McNeil (McNeil) was a member, owner and operator of J & J McNeil, LLC, an excavation and snow-removal company. To keep it simple I’ll set out the rest of the facts verbatim from the opinion:

“Along with his home, McNeil’s property included a large shed which was used primarily to store the LLC’s equipment. The LLC owned a number of vehicles, including a 93–foot Caterpillar scraper (scraper). McNeil also owned a number of vehicles personally, including a 2008 Shelby GT (Shelby), which was subject to the perfected security interest of Harris Bank. During the summer months, McNeil stored the Shelby in the garage attached to his home. During the winter months, McNeil stored the Shelby in the nearby shed, freeing up room in his garage. The Shelby was wholly maintained by McNeils personal funds and had no business purpose.”

“In the early hours of November 13, 2008, McNeil needed to service the scraper and mobilize it for a commercial development project. In order to service the scraper, it needed to be moved inside the shed. Although usually parked out of the way in the back of the shed, the Shelby was parked in a manner that interfered with the scraper’s entrance. McNeil moved the Shelby out of the shed and parked it adjacent to the shed’s exterior, allowing him to pull the scraper into the shed. After servicing the scraper, it was ready for mobilization. Prior to backing the scraper out of the shed and unbeknownst to McNeil, the Shelby, which had a manual transmission, rolled down the incline outside of the shed before coming to rest outside of the shed’s garage door. When McNeil backed the 605 horsepower, 93–foot–long Caterpillar Challenger out of the shed, he did not see the Shelby and drove over it. The impact from the seven-and-a-half-foot tires effectively destroyed the Shelby.”

So to summarize this unfortunate accident, John McNeil, while driving a large piece of equipment, on behalf of J & J McNeil, LLC, smushed an automobile that he owned personally. McNeil sought payment for his automobile from Dakota Fire, the LLC’s general liability insurer.

The general liability insurer maintained that no coverage was owed on account of the policy’s exclusion for “property you own, rent or occupy.” While McNeil was an insured under the LLC’s policy, and owned the automobile, the court held, without too much effort, that the exclusion did not apply. That’s because the court saw it this way: “The policy plainly states that the term ‘you’ only refers to the Named Insured. As given by the policy’s Declarations, the only Named Insured is J & J McNeil, LLC. [John] McNeil is not listed as a Named Insured in the policy’s Declarations. Therefore, the ‘property you own, rent, or occupy’ exclusion only refers to the LLC’s property. The facts clearly dictate that the LLC did not own or rent McNeil’s Shelby.”

It is easy to see how the result could have been different for Dakota Fire. If the policy’s exclusion had applied to “property an insured owns, rents or occupies,” then coverage would have been precluded because the damaged Shelby was owned by an insured [John] under the LLC’s policy.

There are certainly instances in a liability policy where “named insureds” should be treated differently than “insureds” (or additional insureds). But it seems difficult to fathom that the CGL policy should come with a built-in argument that, in some situations, additional insureds or omnibus insureds are entitled to more coverage than named insureds. Where is ISO on this? Ironically, those letters are sometimes used as an acronym for In Search Of. |

|

| |

|

|

|

|

Vol. 3, Iss. 11

July 16, 2014

Serving An Absolut Exclusion Straight Up

|

|

|

When you think of the word “absolute” modifying a policy exclusion, the pollution exclusion probably comes to mind. But despite the definitive sounding name of something called the Absolute Pollution Exclusion – we don’t cover pollution, no way, no how – the real story has been much different. Anyone reading this knows that courts across the country are deeply divided over whether the exclusion, despite its broad language and name, applies to any claim involving a hazardous substance or is limited to so-called traditional environmental pollution. See “The Latest Pollution Exclusion Scorecard” in this issue.

Based on the Absolute Pollution Exclusion experience, it may not be unreasonable to wonder if something called the “Absolute Auto Exclusion,” contained in a CGL policy, is really so absolute after all. That was the issue in a recent federal appeals court decision and, trust me, it’s worth reading on.

But first, why even the need for an “absolute” auto exclusion when the ISO commercial general liability form contains an “auto” exclusion? The “auto” exclusion contained in ISO’s standard CGL form applies, in general, to injury or damage arising out of the ownership or use of an auto. However, for the exclusion to apply, the auto must be owned or operated by or rented or loaned to any insured. On the other hand, the “absolute” auto exclusion applies to injury or damage arising out of the use of any auto. Period. In other words, the “absolute” auto exclusion removes the qualification that the auto must have some connection to an insured, i.e., that it must be owned or operated by or rented or loaned to any insured.

As a result of this, the Absolute Auto Exclusion can be quite broad in its application, as demonstrated very clearly by the Eleventh Circuit’s decision in James River Ins. Co. v. Fortress Systems, LLC, No. 13-10564 (11th Cir. June 24, 2014). Some of the following is taken from the Southern District of Florida’s opinion in the case.

Bodywell Nutrition, LLC, a sports nutrition and dietary supplement company, retained Fortress Systems to manufacture a powder-form drink called First Order. While FSI manufactured First Order without defect, the companies with whom FSI subcontracted the shipping of the product used vehicles without proper cooling systems. This caused the First Order powder to clump together and became insoluble. Bodywell filed a complaint against FSI.

FSI was insured under a $5 million CGL policy issued by James River. This was no small claim. Bodywell and FSI entered into a settlement in excess of $10 million including an assignment of policy rights against James River, which had disclaimed coverage.

At issue in the subsequent coverage dispute was the applicability of the Absolute Auto Exclusion – barring coverage for property damage arising out of the use of any auto. The exclusion stated: “‘Bodily injury’ or ‘property damage’ arising out of the ownership, maintenance, use or entrustment to others of any aircraft, ‘auto’ or watercraft. Use includes operation and ‘loading or unloading’ which includes the handling and placing of persons by an insured into, onto or from an ’auto.’ This exclusion applies even if the claims against any insured allege negligence or other wrongdoing in the supervision, hiring, employment, training or monitoring of others by that insured, if the ‘occurrence’ which caused the ‘bodily injury’ or ‘property damage’ involved the ownership, maintenance, use or entrustment to others of any aircraft, ‘auto’ or watercraft.”

That’s a mouthful. The Eleventh Circuit described the exclusion in simpler terms: By its plain language, the Absolute Auto Exclusion precludes coverage for damage arising from the use of any auto, without exception.

The Absolute Auto Exclusion had been added to the CGL policy by endorsement – replacing the standard “auto” exclusion in Fortress’s policy. James River asserted that the Absolute Auto Exclusion applied because the clumping occurred as a result of the shippers’ failure to use temperature controls in their vehicles. To be clear, Fortress had nothing whatsoever to do with the shipping of First Order, other than to hire other companies to do the shipping using their vehicles.

Applying Nebraska law, the Florida District Court concluded that the Absolute Auto Exclusion applied. The court rejected the argument that damage did not arise out of the use of the shippers’ vehicles, but, rather, the heat in the vehicles. “By Bodywell’s own admission, First Order was damaged by the shippers’ failure to use climate-controlled vehicles. . . . Bodywell claimed that the shippers failed to heed the warning labels requiring that First Order be stored in a cool dry place, and ‘either used transport vehicles that were not temperature-controlled or did not use any temperature-controlling capabilities that were available in those vehicles.’ . . . Bodywell’s statements show that it was the manner in which the vehicles were used, or the capabilities of the vehicles employed, that damaged First Order. There is a clear causal connection between the use of the shippers’ vehicles and the subsequent property damage. Therefore, the Court concludes that the damage arose out of the use of an auto, and that Defendants’ coverage claim is barred by the Absolute Auto Exclusion.” The Eleventh Circuit, in agreement with the reasoning of the District Court, affirmed.

Fortress demonstrates that the “absolute,” in the Absolute Auto Exclusion, isn’t kiddin’ around. The decision shows in stark terms the significant difference between an “auto” exclusion and an Absolute Auto Exclusion. Fortress itself had nothing whatsoever to do with the actual shipping of First Order. That would have clearly prevented the applicability of a standard “auto” exclusion. But not so with the unqualified Absolute Auto Exclusion. Conclusion: the insurer realized a multi-million dollar savings based on taking the “absolute” road with the Auto Exclusion. |

|

| |

|

|

|

|

Vol. 3, Iss. 11

July 16, 2014

Hoosier Maneuver: How To Crack The Indiana Pollution Exclusion Nut

|

|

|

The best way to describe how insurers have fared in Indiana, in their attempt to enforce the pollution exclusion, is this. Insurers are the Brazilian soccer team. Policyholders are the German team. Indiana has surely been a very difficult place for insurers on the pollution exclusion. Ironically, it could be the easiest state -- if insurers drafted the exclusion using the simple instructions that the Indiana Supreme Court has provided.

In general, in Indiana, for the pollution exclusion to apply, the hazardous material argued to be a “pollutant” must be specifically mentioned in the pollution exclusion. State Auto. Mut. Ins. Co. v. Flexdar, Inc., 964 N.E.2d 845 (Ind. 2012).

Last week an Indiana federal court held that a non-specific pollution exclusion precluded coverage for groundwater contamination by TCE. How did the insurer in Visteon Corp. v. National Union Fire Ins. Co., No. 11-200 (S.D. Ind. July 7, 2014) pull this off in the face of Indiana’s strong case law requiring that the “pollutant” at issue must be specifically mentioned in the pollution exclusion? Easy, the insurer succeeded in arguing that Michigan law applied to the dispute.

This 50-Nifty approach was also successful for the insurer in Chubb Customs Ins. Co. v. Standard Fusee Corp., 2 N.E.3d 752 (Ind. App. Ct. 2014), where it convinced an Indiana appeals court that a non-specific pollution exclusion precluded coverage for perchlorate contamination from manufacturing marine signal/safety flares, which fell within the pollution exclusion. The insurer did so by first convincing the Supreme Court of Indiana that Maryland law applied. |

|

| |

|

|

|

|

| |

|

Vol. 3, Iss. 10

June 25, 2014 |

|

|

| |

|

|

|

|

|

Ewing’s Undoing?: 5th Circuit Holds That Contractual Liability Exclusion Precludes Coverage For Garden Variety Construction Defect Claim

In January, the Supreme Court of Texas, in easily one of the most important coverage cases of 2014, held in Ewing Construction Co. v. Amerisure Insurance Co. that the “contractual liability” exclusion, contained in a CGL policy, did not preclude coverage for a construction defect claim involving not out of the ordinary facts. The Texas Supreme Court’s decision came following the case’s earlier time spent in the 5th Circuit. Not since the Alamo has there been a fight in Texas this big.

The day Ewing was decided it seemed like it was case closed on the issue. Not so fast. With Davey Crocket-like determination, Mid-Continent Casualty Company convinced the 5th Circuit in Crownover v. Mid-Continent, No. 11-10166 (5th Cir. June 27, 2014) that, despite Ewing, the contractual liability exclusion still precluded coverage for a garden variety construction defect claim.

I could say lots more about the case, but instead I’ll leave that to Lee Shidlofsky and Doug Skelley, who represented Ewing Construction. Their blog post about the case at Shidlofsky Law Firm provides extensive commentary. Notwithstanding the 5th Circuit’s decision in Crownover, I still see policyholders, and their frequent amicus supporters on construction defect issues, coming out as Santa Ana on this one.

Latest Entry In The Moronic Class Action Category

The Wall Street Journal Law Blog recently reported that a putative class action has been filed in New York federal court against Chobani, Inc., alleging that the company tricks consumers into believing that its Greek yogurt is actually Greek.

The Law Blog reported that the complaint states: “Defendants purposefully market their Products as ‘Greek’ yogurt when there is nothing ‘Greek’ about the Products.” Further, “[n]one of the Products sold in the U.S. are made in Greece or made by Greek nationals even though Defendants market themselves as ‘America’s Top Greek Yogurt.’”

According to the Law Blog, Chobani officials say the suit is without merit and that its central claim is the equivalent of complaining that Canadian bacon isn’t from Canada. In a statement the company said: “Our fans also understand that, like English muffins and French fries, Greek yogurt is a product description about how we authentically make our yogurt and not about where we make our yogurt in Upstate New York and Idaho.”

It is remarkable that Kraft has gotten away all these years with selling Philadelphia cream cheese that is not made in Philadelphia.

Pennsylvania Supreme Court To Revisit PMA v. Aetna After Nearly 60 Years

If you practice coverage law in Pennsylvania then you are familiar with the “PMA issue.” You have to be. And even if you are not regularly in Pennsylvania you may also have come across it. In very general terms, insurers have long-cited to the Pennsylvania Supreme Court’s 1967 decision in PMA v. Aetna to maintain that the Employer’s Liability exclusion (even when it says employee of “the” insured and not “any” insured; and there is a separation of insureds clause) precludes coverage for all insureds, even if the injured plaintiff is not an employee of the insured seeking coverage.

PMA v. Aetna has been a controversial decision. Nonetheless, because it is a Pennsylvania Supreme Court decision, courts have been required to follow it, notwithstanding rumblings that they would have ruled differently if writing on a clean slate. Despite all of the debate surrounding PMA, this near-60 year old decision has never been revisited by the Pennsylvania Supreme Court. Until now.

On June 20, the Pennsylvania Supreme Court agreed to hear an appeal in Mutual Benefit Ins. Co. v. Politopoulos, where the Superior Court, constrained to follow PMA, dealt with its displeasure with the decision by distinguishing it. The Pennsylvania Supreme Court granted the insurer’s Petition for Allowance of Appeal and agreed to answer the following question: “Whether the Superior Court properly ruled that Pennsylvania Manufacturers’ Association Insurance Co. v. Aetna Casualty & Surety Insurance Co., 426 Pa. 453, 233 A.2d 548 (1967) (“PMA”) did not control in the instant case because of the divergence in wording between the ‘severability clause’ in PMA and the language in the Umbrella Policy here, finding that the plain unambiguous language in the case at hand provides coverage for the liability in question.”

Montana Supreme Court To Address Late Notice—Prejudice Issue

In Atlantic Casualty Ins. Co. v. Greytak, No. 13–35133 (9th Cir. June 25, 2014), the 9th Circuit Court of Appeals sent this text to the Montana Supreme Court: “We have found no Montana court decisions that resolve the question of whether an insurer must demonstrate prejudice due to lack of timely notice to avoid defense and indemnification of its insured pursuant to a claim by a third party. A declaration by your Court on this question would guide us in resolving the parties’ dispute. Your acceptance of the request for certification of this question will also be of great assistance in correctly applying Montana law.”

|

|

| |

|

|

|

|

|

|

|

|

|

|

|