|

|

|

|

|

Vol. 3, Iss. 2

January 29, 2014

|

|

|

|

|

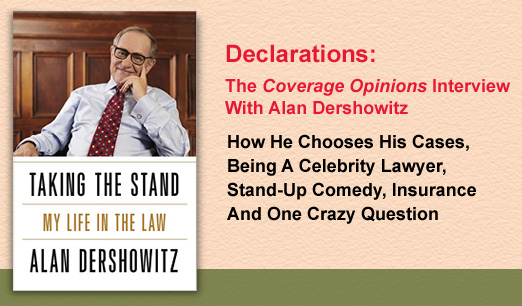

I was very excited when Alan Dershowitz agreed to let me interview him for Coverage Opinions. After all, his schedule is frenetic, I’m not exactly Larry King and insurance is no doubt low on the list of legal topics on his mind. While he just published a book, it is his 31st and six of them were national bestsellers, including Chutzpah, which went to #1 on The New York Times bestseller list. So I am certain that he was not looking at my little insurance newsletter as some sort of promotional bonanza for his latest book. It is clear that Dershowitz was simply doing a nice thing when he sent me a couple of e-mails on a Saturday essentially saying – Here’s my number. Call me Monday at 11. And he could not have been more gracious on the phone. It was really a thrill to speak with one of the most preeminent lawyers of our time. My parents told everyone they know.

Dershowitz’s many books cover such topics as civil liberties, specific cases, various aspects of the legal system, Israel and the Middle East and even fiction. But his latest is different. While all of those topics are discussed, Taking the Stand – My Life in the Law is also very personal.

Alan Dershowitz’s story is well-known. He is the youngest ever professor at Harvard Law School (just retiring after 50 years there) and has been a part of or led the defense team for many famous, or infamous, clients, such as Bill Clinton, Julian Assange, O.J. Simpson, Claus von Bulow, Mia Farrow, Jeffrey MacDonald, Patty Hearst, Mike Tyson, porn star Harry Reems (of Deep Throat fame) and the list goes on. His representation of von Bulow was the subject of a book and movie – Reversal of Fortune. [Jeremy Irons played von Bulow and won the Academy Award for Best Actor.] Dershowitz has also advised many in legal, political and other matters, such as President Obama, Benjamin Netanyahu, Ted Kennedy, Brando, Sinatra, Michael Jackson, Elie Wiesel and countless other celebrities and high ranking public officials.

Something I’d always wondered about Dershowitz was answered head-on in his book. Despite his incredibly impressive client list, yes, there is a downside to hiring him as your lawyer. Some people hate him and his involvement may raise the profile of your case in the media. This is all explained to prospective clients in “the warning” as he calls it. Another risk he cautions about is that “[p]rosecutors sometimes work harder when I am their opponent, because they think that beating me in court will be a kind of trophy.”

I asked Dershowitz if his celebrity causes judges to give him a more difficult time during oral argument. For the most part – no. He feels that most judges enjoy having him before them because he comes prepared, with a carefully worked out argument, and that’s what they want – and it’s something that they don’t always get from lawyers. But he also told me that there are some judges, who perhaps lack self-confidence, and are worried that people will think that they are not up to job, that can be tough on him.

Besides his well-known cases, Dershowitz has also served, pro bono, as appellate counsel to numerous convicted individuals in their attempts to win post-trial exoneration or some other type of relief. Of course, for this work he has made his share of enemies. While the right to counsel is a bedrock principle of our legal system, some people just don’t get that and simply see him as a gun hired to free the guilty. This generates hate mail, some really visceral, that Dershowitz hangs on his office door to show students what to expect if they become public figures.

Not surprising, Dershowitz’s pro bono efforts do not get the same attention as his work for celebrity clients. Indeed, he knows that his eventual obituary will emphasize his cases representing the famous. This is very troublesome to Dershowitz. Since he has had a life-long practice of setting the record straight with regard to things written about him, he has penned a letter to the editor to be sent after his death. Among other things, his posthumous response to his obituary states: “Your understandable emphasis on my high-profile cases distorts my record by downplaying the numerous pro bono cases I handled on behalf of obscure and indigent clients. I made it a policy throughout my life to devote at least half of my professional time to nonpaying cases and causes.”

Dershowitz’s work on behalf of obscure and indigent clients results in requests for his services from individuals who believe that they have been wrongly convicted and are looking for justice from the appellate courts. I am sure that many of these requests sound sympathetic and describe grave injustices that the writers believe have befallen them. I asked Dershowitz how he chooses which pro bono appellate cases to take.

While he explained that it is a combination of factors, and hard to quantify, there is one mandated requirement: “I have to get pissed off.” He told me that he has to get angry – the trial court acted unfairly toward the defendant, the jury was prejudiced or the prosecution overreached. Taking an appeal, he explained to me, is a huge time commitment. “So to take on that kind of commitment I really have to be motivated and the motivation comes from a sense of outrage. So it’s as much emotional as it is intellectual.” And still there are other factors that militate in favor of his selection of a case. He explained to me that he prefers very hard and challenging cases, ones that everyone says you can’t win and he prefers less popular defendants to popular ones. He told me that, given the vast amount of time involved to do everything needed to handle an appeal (and to do so his no stone unturned way), he is only able to take on about a half dozen of these cases per year.

As I said, Taking the Stand is very personal. Dershowitz describes his upbringing in Brooklyn’s Boro Park, a Modern Orthodox community of second generation Jews. His family was not able to afford luxuries and it provided little in the way of books, music, art or secular culture. He attended a yeshiva high school and was a terrible student. He hated his teachers and the feeling was mutual. His love for conflict, doubt and debate was simply not appreciated by the teachers.

But everything changed when he got to Brooklyn College and Yale Law School, where he excelled. At Yale he was first in his class and elected editor in chief of the Yale Law Journal. From Yale Dershowitz served as a law clerk for Judge David Bazelon of the D.C. Circuit Court of Appeals and then Justice Arthur Goldberg of the United States Supreme Court. An important aspect of his time with Justice Goldberg was the planting of seeds to abolish capital punishment. The efforts ultimately succeeded, even if it was short-lived.

Autobiographers usually feel the need to begin their effort with a description of their formative years. After all, is there a more logical place to begin an autobiography? This sometimes makes for reading that is deadly dull and adds little to the story. But Dershowitz’s pages on his formative years are nothing of the sort. They are as interesting as everything else in Taking the Stand. As you progress through the book it becomes clear that Dershowitz’s formative years played a large part in shaping his long career that was to come.

What makes Taking the Stand such a compelling and enjoyable read is that it is several books in one. Of course it is Dershowitz’s autobiography. But he recounts his life in the law through his personal involvement with others. So in that sense it is also biographical of the people that he discusses – some clients and some not. And since these discussions generally center around legal issues, Taking the Stand is itself also a law book – but one that is infinitely more enjoyable than any case book I’ve ever read.

For example, there is no shortage of books and other writings on the subject of rape prosecutions. But to learn about it from Mike Tyson’s appellate lawyer, and hear the conversation that Dershowitz and Tyson had, in Tyson’s hotel room the night before his sentencing, is not the ordinary backdrop for such discussion.

These days murder investigations are as much about science as the work of gum shoes. Dershowitz touches on the scientific aspects in the context of his representations of Claus von Bulow and O.J. Simpson. This is far more interesting than a discussion of the subject without such context. Not to mention that Dershowitz reveals that, just as Johnnie Cochran was about to deliver his closing argument, Marcia Clark whispered to him: “When you’re up there, I want you [to] think of only one thing: I’m not wearing any underwear.”

Taking the Stand is a collection of dozens of stories of Dershowitz’s involvement in interesting cases (celebrities and otherwise) over a long career. These include cases (and causes) involving capital punishment, false confessions, obscenity, disclosure of government secrets, media and the law, terrorism, church and state, the Holocaust, defamation and privacy, Israel and so many more. Dershowitz never stays too long on any one topic, so there is never a chance for the discussion to get bogged down in tedium. To me, that’s what makes or breaks a non-fiction book.

The book also includes numerous short vignettes that generally describe Dershowitz’s experiences (jury duty, walking out on Warren Burger) or encounters with famous people – including some that he calls out for unacceptable behavior that such people probably thought they’d never see in writing (such as Leona Helmsey and Bobby Fisher). Much more positive experiences are described in vignettes about Gorbachev, Mitterrand and Justice Brennan.

It becomes clear throughout Taking the Stand that humor, especially Jewish humor, has played an important part of Dershowitz’s life. He says that he uses humor in the courtroom, classroom and every other aspect of his life. He describes joke telling as a youth as a “competitive sport” among friends. Perhaps there was something in the air as he grew up two houses down from Jackie Mason, Elliott Gould lived around the corner, Buddy Hackett was a few blocks away in his uncle’s building and Woody Allen, Mel Brooks and Larry David were in nearby neighborhoods. Dershowitz’s first job was as a deli guy in a kosher delicatessen on New York’s Lower East Side. A good Jewish deli is really just a comedy club where the comics wear white aprons. Dershowitz credits his work as a busboy in the Catskill Mountains, over the Jewish holidays, as a source of many of the jokes he knows.

Of course, being a stand-up comic myself, I had to ask Dershowitz about his love of Jewish humor and I even suggested that he give stand-up comedy a try. He told me that he thinks he knows every Jewish joke every invented by anyone. He says proudly that he has held his own with many of the best, including Larry David. Of course, Dershowitz notes, the pros write their own material and he admits to just telling other people’s jokes.

As for trying his hand at stand-up, his response was overwhelmingly enthusiastic: “Get me a gig! Get me a gig!” He told me that he almost tried stand-up comedy. A few years ago a fund raiser called Stand-up for Harvard was planned where various professors were to do stand-up routines. Dershowitz signed on but it never came to fruition. “I think they couldn’t find enough funny Harvard professors,” he suspects.

Obviously I had to find an insurance coverage angle for the discussion. Although as soon as I mentioned insurance Dershowitz was quick to tell me that he had something to say on the subject. He believes that insurance companies have far too much say whether criminal cases for fraud are brought. He feels that prosecutors defer to the expertise of the insurance company who they believe have handed them a case on a silver platter. By doing so the prosecutors do not do the hard work necessary to investigate the case themselves. This results is some weak cases being brought.

Insurance fraud is one thing, but there is no way that I was getting off the phone without some mention of insurance coverage. In Taking the Stand, Dershowitz is highly critical of those who use the well-known first amendment exception -- freedom of speech does not protect someone who falsely shouts fire in a theater -- as an analogy to support censorship in various contexts. He provides examples of how the analogy is not only inapt but even insulting.

Shouting fire in a theater may be, according to Dershowitz, the only jurisprudential argument to have achieved the status of a folk argument. The saying is attributed to Oliver Wendell Holmes. Although Dershowitz calls out Holmes for having borrowed the phrase, without attribution, from an obscure prosecutor.

Given that Dershowitz has been a long-time student and teacher of this famous phrase, I asked him if it is constitutionally protected free speech to stand in a movie theater, with a claim file, and shout: “Is this fire claim covered?” He laughed. And being a good sport he set out to answer. The question must be examined in context, he explained. It is constitutionally protected free speech as long as you don’t use fire as the central word and whisper all of the others.

|

| |

| |

|

| |

|

|

|

|

Vol. 3, Iss. 2

January 29, 2014

|

|

|

|

|

Coverage Opinions Caption Contest

Prizes Direct From Hollywood

Who doesn’t love a caption contest?

It’s simple. Send me an insurance-related caption, thought bubble or dialogue bubble for this cartoon. Feel free to send as many entries as you’d like.

The two best entries will win an autographed picture of Flo from the Progressive Insurance commercials. These were kindly provided to me by Odenkirk Provissiero Entertainment in Los Angeles – the management company for Stephanie Courtney, the actress and comic that plays Flo. |

| |

| |

|

| |

|

|

|

|

|

|

Vol. 3, Iss. 2

January 29, 2014

Randy Spencer’s Open Mic:

There Is No J In The Pollution Exclusion

|

|

|

|

|

|

Lately there have been a few decisions addressing whether hog manure qualifies as a pollutant under the pollution exclusion. This makes for an interesting debate – just not one to have at the dinner table. Riddle me this: Is bat guano a pollutant? This has also been answered by a few courts in recent years. The bat guano question had been right up there with many of the other great unsolved mysteries of the universe: How did the pyramids get built? What’s the meaning behind Stonehenge? How did those Easter Island fellows get there?

One of the reasons why the pollution exclusion is such an interesting issue, and the subject of so much commentary, is that the substances under consideration are so varied and sometimes quirky. Over the past three decades or so it seems that courts have addressed whether just about anything and everything is a pollutant for purposes of the exclusion. I’ve always known that to be the case from an anecdotal standpoint. But recently I saw actual evidence of it when I had the occasion to refer to Claudia Catalano’s A.L.R. article – which is more accurately described as a phonebook – on the pollution exclusion. Her piece -- “What Constitutes ‘Pollutant,’ ‘Contaminant,’ ‘Irritant,’ or ‘Waste’ Within Meaning of Absolute or Total Pollution Exclusion in Liability Insurance Policy” – contains an index of substances that have been presented to courts for their answer to this question. The index lists in the range of 260 entries.

Obviously that’s a lot of substances that have been the subject of pollution exclusion litigation. Indeed, so many in fact that upon closer review of the index I realized that every letter of the alphabet is represented -- except J. There is ammonia, benzene, carbon monoxide, dust, ethylene dibromide, fly ash, gasoline, hydrochloric acid, insecticides, kerosene, lead, manganese fumes, noise, odors, perc, quicklime, rubber, silica, toluene, underground storage tanks, vinyl chloride, wood ash, xylene, yellow jackets and zinc. [… next time won’t you sing with me.]

[OK, the yellow jackets case in fact involved pesticides to exterminate them. But when you are in the Ys sometimes you need to be creative.]

Surely there is a pollution exclusion case out there involving a substance that starts with the letter J? Someone find it and send it to Claudia Catalano. Not that her A.L.R. piece isn’t already complete, but it seems a pity that the index is just one short of the entire alphabet.

|

|

| |

|

|

|

|

|

|

Vol. 3, Iss. 2

January 29, 2014

Magic Johnson Follows Lakers Tradition And Enters Insurance World

But Does Not Respond To Coverage Opinions Request For Comment

|

|

|

The Chicago Tribune reported earlier this month that Los Angeles Lakers legend Earvin “Magic” Johnson has entered the insurance world. Magic is becoming a controlling shareholder in EquiTrust Life Insurance Co., which distributes fixed-rate and indexed annuities and life insurance through a national network of more than 14,500 independent agents.

The Tribune reported that the company is opening new offices in Illinois that will create 200 jobs in the coming year and could employ hundreds more in years to come. Illinois Governor Pat Quinn stated that he was excited to have Magic become a corporate citizen of the state.

Of course, Magic’s entry into the insurance world is nothing new for a Lakers legend. As readers of Coverage Opinions well know, long-time Los Angeles Lakers owner Jerry Buss was the man behind the California Supreme Court’s 1997 decision in Buss v. Transamerica Ins. Co. In general terms, California’s top court held in Buss that, in a so-called “mixed” action, in which some claims are potentially covered and others are not – thereby triggering a duty to defend the action in its entirety – an insurer may seek reimbursement of defense costs for claims that are not potentially covered. Also in general terms, as a practical matter, the Buss rule can be difficult to apply. The Buss court itself noted that the task of allocating defense costs solely to claims that are not even potentially covered is at best extremely difficult and may never be feasible. Buss gave rise to many other states addressing whether an insurer can obtain reimbursement of defense costs following a determination that it had no duty to defend. Courts nationally are generally split on the issue.

In February 2013 Jerry Buss passed away at age 80. Not one tribute or obituary that I read mentioned his California Supreme Court case. I brought this omission to the attention of Bill Dwyre, former Sports Editor for 25 years, and now columnist, for The Los Angeles Times. Dwyre himself wrote a wonderful tribute to Buss. He indicated that he passed my concern along to the business columnist folks. But nothing ever came of it. I couldn’t let Jerry Buss’s contribution to the world of insurance coverage go unnoticed. I wrote his “insurance obituary” in the February 27 issue of Coverage Opinions.

I reached out to Magic, through Magic Johnson Enterprises, and asked him if he was aware that, by taking a stake in EquiTrust Life, he was following in the footsteps of his former boss and continuing the Lakers’s tradition of playing a part in the insurance world. Unfortunately, he did not respond – perhaps because he had no clue whatsoever what I was talking about. Jerry Buss lost his famous case before the California Supreme Court. Hopefully for Magic his investment in EquiTrust Life won’t serve as the basis for his return to any courts.

|

|

| |

|

|

|

|

|

|

Vol. 3, Iss. 2

January 29, 2014

Appeals Court Provides Detailed Discussion Of Allocation Between Covered And Uncovered Claims

|

|

|

I have said this so many times. But given the huge importance of the issue, it is restated here. If you’ve read this before please forgive me.

You have just written the greatest reservation of rights letter ever. If Felix Unger handled claims, this is what his letter would look like. If there were a hall of fame for reservation of rights letters, you would soon get to see how you looked in bronze. Your letter compares the specific allegations in the complaint, to the policy language, and explains, with laser-like precision, why, despite the insured being provided with a defense, no coverage may be owed for any settlement or judgment. You mail the letter, put a copy in the file, take a deep breath of satisfaction, waste a few minutes reading a couple of meaningless articles on Yahoo, and then off you go to your next claim.

But the challenge with reservation of rights letters is not writing them. It is enforcing them. Because a reservation of rights letter is written in a sterile environment – at someone’s desk – it can easily spell out, in black and white terms, those claims and damages at issue in the underlying suit for which coverage may not be owed. The underlying litigation, on the other hand, is likely proceeding in a manner that is anything but as neat and tidy.

It will frequently be the case that the underlying litigation is simply not capable of producing an outcome that makes it possible for the insurer and insured to compare its results, with the reservation of rights letter, and easily decide which claims and damages are covered and which are not. To the contrary, the underlying litigation may result in a verdict that does not specify the extent to which it represents this or that type of damage or the claims on which the relief is based. In this situation, often-times referred to as a “general verdict,” the policyholder is likely to argue that, because the basis for the jury’s verdict cannot be determined, it must be presumed that the entirety of the jury award represents covered claims and damages. Adding to the difficulty for insurers is that it cannot ask appointed defense counsel to seek special jury interrogatories, which would go a long way toward solving this problem. [And similar problems may come from a settlement.]

Some courts have accepted the policyholder argument that, if the insurer created the problem of an inability to allocate between covered and uncovered claims, it must therefore bear the consequences. In other words, if it cannot be determined which portion of a verdict is covered and which is not, then all of the damages will be considered covered. Or the insurer may have a difficult burden to prove covered versus uncovered damages. In these situations, the fact that the insurer issued a world class reservation of rights letter, spelling out in detail its precise position on what is and what’s not covered, is no protection against failing to prevent a general verdict and the consequences that it causes.

At the heart of these decisions is the placing of blame on the insurer for being aware that the underlying litigation may result in a verdict that does not enable a determination to be made between covered and uncovered claims and/or damages, yet it took no steps to prevent such outcome. Indeed, these decisions sometimes speak in very harsh tones -- essentially blaming the insurer for being its own worst enemy.

The knotty issue of allocation between covered and uncovered claims was a subject of discussion, and in some detail, in World Harvest Church v. Grange Mutual Casualty Co., No. 13AP-290 (Ohio. Ct. App. Dec. 24, 2013). The issue arose as follows.

Michael and Lacey Faieta and their minor son, A.F., filed a complaint alleging that an employee of the prepatory school operated by World Harvest Church physically abused A.F. while the two and one-half-year-old boy was in the employee’s care in WHC’s daycare program. The Faietas raised claims of battery and intentional infliction of emotional distress against the employee and claims of negligent supervision and IIED against WHC. A after a seven-day trial, the jury returned general verdicts in favor of the Faietas against both the employee and WHC. The jury awarded the Faietas compensatory damages of $134,865 and punitive damages of $100,000 against the employee, and compensatory damages of $764,235 and punitive damages of $5,000,000 against WHC. The jury also found that the Faietas were entitled to attorney fees against WHC.

While Grange Mutual had defended WHC in the Faieta action, it refused to indemnify WHC for any portion of the judgment. WHC filed an action against Grange seeking a declaration that it was entitled to payment from Grange of all or some of the amount it paid to resolve the Faietas’ case.

Putting aside lots of issues, the trial court in the declaratory judgment action entered a judgment in favor of WHC and against Grange in the amount of $1.4 million. This included a compensatory award of $549,100. In addition to substantive coverage issues, the appeals court was required to address allocation between the potentially covered and uncovered causes of action that made up this compensatory award.

The trial court had found that “for the three causes of action on which the jury entered a general verdict in favor of the Faietas—battery, IIED, and negligent supervision—Grange ‘bears the burden of proof to demonstrate that coverage does not apply to each of the causes of action and will need to establish exclusions for the other portions of the award, if any,’ and that because ‘it is not possible to allocate the proportions of the general compensatory verdicts,’ ‘if [WHC] establishes coverage for any of the three causes of action, then [Grange] must indemnify [WHC] for the entire compensatory amount of the award.’”

The Ohio Court of Appeals addressed the burden of proof, but its decision was more nuanced and detailed.

Not surprisingly, the parties had diametrically opposing views on how to address the issue. Grange argued “that WHC should have the burden of proof as to the allocation of the verdict between [the employee’s] battery, WHC’s negligent supervision, and the IIED by [the employee] ‘and/or’ WHC, and that ‘[s]ince the verdict cannot be allocated, WHC’s action against Grange [for compensatory damages, attorney fees, and interest] must fail.’ WHC counters that Grange has the burden of allocating a general verdict to prove that some or all of the award represents damages for non-covered claims. WHC asserts that ‘[s]ince it is not possible to allocate the general compensatory verdicts, if WHC can establish coverage under any one of these three causes of action—battery, IIED, or negligent supervision—then Grange must indemnify WHC for the entire compensatory portion of the verdict.’” (emphasis in original).

The court determined that it would “apply what appears to be the general rule that an insured has the burden to prove entitlement to coverage, including the burden of allocating a prior general award into covered and noncovered claims, but that where an insurer has a duty to defend the insured and fails to seek an allocated verdict or advise the insured of the need for one, the burden shifts to the insurer.” (emphasis added).

Despite this general rule, Grange asserted that “the burden of proving allocation of the verdict did not shift from WHC to Grange because it sent a reservation of rights letter to WHC, WHC engaged its own private counsel in addition to the counsel that Grange provided to it in the personal-injury trial, Grange advised WHC of its divergence of interests, and WHC’s private counsel controlled the litigation.”

But this, the court concluded, was not sufficient to prevent the burden from shifting to the insurer. The court concluded that Grange provided WHC with only the most general and vague statements concerning their divergent interests. “Grange never advised WHC of the specific apportionment issue and of the need for special interrogatories allocating damages.”

The court concluded: “Under these circumstances, the presence of WHC’s independent counsel and Grange’s notification to WHC of its reservation of rights did not constitute a discharge of Grange’s duty to fully disclose the precise situation concerning the necessity of seeking an allocated verdict in the personal-injury case. If Grange truly believed that intervening in the case to submit special interrogatories would have compromised WHC and its employee’s ability to advance their agreed upon joint defense, Grange or its provided counsel could have still discharged any duty by precisely advising WHC of the need for an allocation of the damages and the consequences of not obtaining one. . . . Neither Grange’s reservation of rights nor the presence and participation of WHC’s independently retained counsel during the Faietas’ personal-injury case discharged Grange's duty.”

This is clearly a complex issue and one that must be addressed on a case by case basis. But there is an important overarching take-away. No matter how well-done you think your reservation of rights letter is, it is not going to enforce itself.

|

|

| |

|

|

|

|

|

|

Vol. 3, Iss. 2

January 29, 2014

Measuring The Bull’s-Eye On Target’s Back:

Lessons From The T.J. Maxx Data Breach Class Actions

"Simply put, the class action vehicle is broken."

-- Judge William Young, Overseeing The T.J. Maxx Data Breach Litigation

|

|

|

Once my wife believes something it is very difficult to change her mind. And if her mother agrees with her then look out. I could call in Socrates to speak with her and even he would walk away just shrugging his shoulders. Sorry man, I tried.

In a way this is the situation that Target Corp. is going to face when it defends the 70 or so putative class actions that have recently been filed against it – so far -- in various federal courts around the country for damages allegedly caused by a massive security breach of its customers’ personal and financial information. Yes, 70. You read that right.

At issue is the theft of the retailer’s customers’ personal information from the magnetic strips of their credit and debit cards. The theft allegedly occurred between November 27 and December 15 when customers’ cards were swiped through the retailer’s point-of-sale terminals. This was no small data breach. In general, it was initially announced that thieves stole credit and debit card information from 40 million customers. It later came to light that the same criminals acquired names, addresses and phone numbers from as many as 70 million accounts. However, given the no doubt overlap of these two groups, the number of affected individuals is not 110 million. Not that that’s much of a consolation for Target. And just as day follows night, after the breach was announced, the law suits began rolling in. Seven were filed on the same day that the breach was announced. For some plaintiffs’ lawyers this was the Black Friday door buster to end all others.

Despite the parade of horribles that the class action complaints allege that Target caused to its customers, Target’s website states that its guests (as the company refers to its customers) will have “zero liability for any charges that [they] didn’t make.” Target’s CEO, Gregg Steinhafel, in a CNBC interview that aired Monday, repeated that over and over and over. There’s no ambiguity there. No Target customer will be picking up any bar tabs in Nigeria.

But none of this will matter to the plaintiffs’ attorneys that have filed the class action suits. Just as my wife will never be convinced that taking Montgomery Avenue home from the King of Prussia Mall is just as good as Old Gulph Road, the plaintiffs’ attorneys will never believe that Target, no matter what it says or does to try to convince them, will adequately compensate its customers. [Actually, they probably do. But if they said so it would leave no compensation for themselves. So the class action suits will roll on.]

At least Target’s shareholders feel confident that the retailer will make all of this right. The company’s stock has held up well despite the onslaught of negative publicity and obvious fact that the data breach is going to cost Target shopping carts full of money. [Target’s revenue in 2013 was $73 billion. That’s more than the gross national product of over a hundred countries. So the company is unlikely to feel the hit as much as some would.]

Target is going to experience financial exposure on many fronts. Some of the obvious ones are the cost to investigate the data breach and upgrade its systems to prevent future breaches. There will be lost sales, which will translate to lost profits. Target has reported that it expects fourth quarter 2013 adjusted earnings per share of $1.20 to $1.30 compared with prior guidance of $1.50 to $1.60. Target will face claims from banks that suffered losses for fraudulent charges, as well as for the cost of banks to issue replacement cards. [A recent Wall Story Journal story addressed some issues surrounding that last point.] Target may be required to deal with shareholder suits against the company as well as settlements with state attorney’s general.

And, of course, Target will surely be required to compensate its customers for their alleged damages. These 70 or so class actions and counting are not going to be litigated in any court of law with a jury foreperson someday standing up and announcing a verdict in favor of Target. Of course not. These class actions will be settled. Target is much too reputation-dependant to not want to get these suits in the rear view mirror pronto.

So how might the Target class actions play out? That is impossible to gauge at this point. But for some guidance on that question consider the 25 class action complaints, filed in 2007, against retailer T.J. Maxx (and some sister stores), for damages allegedly caused by the theft of customers’ personal information.

But before getting to the TJX cases, and what they may foretell for Target, it is worthwhile to look at the Target class action complaints themselves and address whether Target has done what’s alleged and whether the plaintiffs have in fact suffered the damages they claim. Not that any of these details matter in the world of consumer class actions, but just indulge me.

The class action plaintiffs seek damages for their financial losses due to unauthorized charges on their credit and debit cards. But Target has made it abundantly clear that its customers will suffer no such losses. The class action plaintiffs also seek to be provided with credit monitoring services. That is usually one of the more tangible elements of damages sought in cases like this. Target has stated that it will offer free credit monitoring to its customers for one year. Details of this are spelled out on Target’s website. The company didn’t need to be forced by any court to offer this service.

Some class action plaintiffs seek damages for emotional distress. Really. I’m not making that up. My wife shopped at Target during the breach period. Thankfully she seems to be holding up just fine. But I am keeping a close eye on her for any changes in her behavior. Target’s Minneapolis headquarters is located not far from the Mayo Clinic in Rochester, Minnesota. Perhaps they can work out a deal to treat those suffering from such distress.

Some plaintiffs are seeking punitive damages from Target. Punitive damages are awarded for conduct that resembles criminal. They are saved for societal conduct that is the worst of the worst. It may turn out that Target did or didn’t do some things that allowed the data breach to take place. But it is inconceivable that anything it did could justify punitive damages. You don’t get to be the nation’s second largest retailer, with over 1,900 stores, by acting in any manner that comes within a hundred miles of conduct that could justify punitive damages.

The class action plaintiffs allege that Target breached various state consumer protection statutes. But these statutes are likely inapplicable to the circumstances here and/or Target did not act with the level of culpability required to have committed such a breach. The class action plaintiffs also allege that Target breached various state statutes that require timely notice of a data breach. Target announced the breach just four days after it was discovered. Further, these statutes generally do not include a private right of action.

Most reasonable people would stop shopping in any store that treated them as horribly as they alleged Target did. But I suspect that the class action plaintiffs have not seen the last of the inside of a Target store.

But despite the assurances and benefits that Target has offered voluntarily, without any court intervention, the class actions are still sure to settle -- and for some big numbers. Judge William Young, a Massachusetts federal judge, has stated: “Simply put, the class action vehicle is broken.” His Honor added that “there are surely plaintiffs’ lawyers who bring putative class action lawsuits without merit, assuming, correctly, that in many cases the defendant will settle the case to avoid a small probability of a substantial judgment.” That Judge Young made these statements, in the context of overseeing the T.J. Maxx data breach class actions, does not bode well for Target. See In Re TJX Companies Retail Security Breach Litigation, No. 07-10162 (D. Mass. Nov 3, 2008).

While the Target consumer class actions are bound to settle, what might that look like? Again, while it is impossible to know at this point, the settlement of the T.J. Maxx data breach class actions sheds some light on what may lie ahead for Target.

The T.J. Maxx data breach involved the theft of data related to over 45,000,000 credit and debit cards used at TJX Stores (T.J. Maxx, Marshalls, HomeGoods and a few others). However, banking associations that issued some of the affected cards asserted that hackers actually compromised the security of over 94,000,000 accounts. In any event, TJX announced in January 2007 that, going back as far as 2003, and in mid-May through December 2006, some customer financial information, as well as driver’s license numbers (which may be the same as social security numbers) were stolen from its systems.

The breach was announced in January 2007 and the settlement of 25 class actions came swiftly. The initial settlement was filed with the court on September 21, 2007. Putting aside other settlement-related activities, the settlement was put to bed in September 2008. Target is also likely to address the class actions with similar alacrity as TJX. In general, the settlement terms were as follows.

TJX offered three years of Equifax’s “Credit Watch Gold with 3-in-1 Credit Monitoring” (which includes $20,000 in identity theft insurance) to the approximately 455,000 class members whose name, address and driver’s license or military, tax or state identification number (which for some is the same as their social security number) may have been compromised. These are individuals who had previously returned merchandise to TJX without a receipt and, as part of that process, had provided such information to the retailer (the so-called “unreceipted return customers”). Such credit monitoring had a retail price of $390 for each class member. Thus, the cost to provide this service to 455,000 class members was $177,000,000.

But here’s the rub. According to the court’s opinion addressing attorney’s fees (approved to be $6.5 million; but subject to a very lengthy explanation from the court), only slightly more than 3% claimed the credit monitoring benefit.

Target is now offering its customers one year of Experian’s ProtectMyID credit monitoring, which includes $1,000,000 of identity theft insurance. According to Experian’s website, the retail price of this is $15.95 per month. Of course, Target is obviously not paying the rack rate. [If there’s an annual price for this service I could not find it as Experian’s website was not responding to certain links.]

It is not surprising that only slightly more than 3% of the eligible TJX class members sought credit monitoring. It was offered to them eons after the data breach took place. By the time it was offered those affected either forgot about the breach or knew by then that they were probably not in an jeopardy of identity theft.

Target’s offer of credit monitoring is world’s apart from TJX’s. Target is offering it to all of its customers and doing so when the incident is very fresh in their minds. Indeed, Target’s offer is coming while the data breach story is still front page news. There are exponentially more than 455,000 people eligible for credit monitoring and a lot more than 3% are going to take Target up on its offer. Consider that you aren’t even required to have shopped at Target during the breach period to sign up for credit monitoring. Target states that “[a]ll Target guests who shopped in U.S. stores can take advantage of one-year of free credit monitoring.” I didn’t shop at Target during the relevant period and I just signed up for it. The process was really easy.

Target is voluntarily taking on a huge credit monitoring expense. Target could do what TJX did and offer credit monitoring as part of a class action settlement long after this incident has been forgotten. This would dramatically reduce its credit monitoring liability. But that’s not the path it took. Nonetheless, despite voluntarily approaching credit monitoring in this manner, that likely won’t be enough for the class action plaintiffs’ attorneys.

The TJX settlement also included various cash payments and store vouchers for these unreceipted return customers. TJX reimbursed any costs incurred to replace their driver’s license. Those whose social security number was the same as their driver’s license, military, tax or state identification number could recover losses over $60 that occurred as a result of identity theft traceable to the breach. Customers were required to submit proof of loss and the aggregate amount payable for this category of damages was $1,000,000. As of the court’s November 3, 2008 opinion addressing attorney’s fees, almost 4,800 of such claims had been made. None were deemed valid and no payments had been made under this category.

Another category of benefits was offered to customers who certified that they made a purchase with a credit card, debit card, or check at TJX stores during the relevant time periods and incurred at least $5 in out-of-pocket expenses or lost time (valued at $10 an hour) as a result of the intrusion. Under this “self-certification” option, class members needed only to state, under penalty of perjury, that they had made a check or card purchase and that they had suffered the required loss. These individuals would receive, at their option, either a $15 check or a $30 voucher. The agreement imposed a $10,000,000 cap on claims made by self-certifying class members. Claims were valued at $30, whether for check or voucher. Class members who could provide documents that they both made a qualifying purchase (for example, a credit card statement) and suffered the requisite loss were eligible to receive a $30 check or $60 in vouchers. The agreement imposed no cap on the value of vouchers that class members could claim via this method but limited the payout made in check form to $7,000,000.

For lawyers who no doubt claimed that a data breach was a huge inconvenience for customers, they sure didn’t put a lot of value on their clients’ time or inconvenience when it came to reaching a settlement. Ironically, for most TJX customers, making a claim for compensation was probably a bigger inconvenience than the data breach itself ever caused them.

It is hard to imagine Target not voluntarily offering its customers some sort of coupons as an apology, for their inconvenience, as evidence of taking responsibility and a sign of good faith to win back their loyalty. Target already offered its customers a 10% discount the weekend after the breach was announced.

So what does all of this mean for Target. The simple answer is this. Even if no Target customer will have any liability for fraudulent charges; even if Target takes on a huge credit monitoring liability – and far greater than if it waited to be compelled to do so; even if the consumer protection and data breach notice claims have no merit; even if the TJX case shows that actual losses for identity theft from a date breach are rare; and even if Target voluntarily offers compensation for inconvenience, none of this is likely to be enough to escape also paying the class action piper. That’s just how it works. The plaintiffs’ attorneys are not going to look at Target’s voluntary compensation and drop their cases. OK, this looks good. We’re not needed here. Move along folks. Nothing to see. What Target can hope for is that all of its voluntary compensation serves to take some of the value out of the class action settlements.

Disclosure Statement: I do not own any shares of Target Corp. stock. White and Williams, LLP does not represent Target Corp. This article was originally published on January 15, 2014 as a supplement to Coverage Opinions, Vol. 3, Iss. 1 (Jan. 8, 2014).

|

|

| |

|

|

|

|

|

|

Vol. 3, Iss. 2

January 29, 2014

The Target Data Breach: Some Preliminary Thoughts On Coverage; The Great Connecticut Coincidence; And The Real Insurance Impact

|

|

|

So far the focus of the Target data breach has been on its scope, how it may have happened, Target’s response and the various types of financial havoc that it could cause for the nation’s second largest retailer. But no doubt it won’t be long before insurance coverage becomes a front and center issue. It would be hard to imagine insurance coverage not having a place at the table for such large scale and out of the blue losses. Think of insurance coverage as the tortoise in his race with the hare. After all the dust settles, insurance sometimes emerges as the most important issue.

What types of insurance does Target have and how much? Business Insurance reported that the company has at least $90 million of cyber insurance that sits over a self insured retention of $10 million. BI also reported that Target has $55 million of director’s and officer’s coverage that kicks in after a $10 million SIR. The sources for this report were well-placed in the industry who requested anonymity. It is not often that insurance news stories read in such cloak and dagger terms.

Target’s SEC filings indicate that, as you might suspect for a company of this type, it is self-insured for general liability insurance (and workers’ compensation) and then employs stop loss coverage. The amount of self-insurance for GL is not indicated. However, it appears to be a large number. A public filing indicates that workers compensation and general liability accrual was $627 million and $646 million at February 2, 2013 and January 28, 2012, respectively.

The coverage issues that arise under D&O insurance, for shareholder suits, are well tested. Much less is known about how any general liability and cyber coverage may respond to various claims filed against Target.

In general, when it comes to the potential for general liability coverage, for a data breach, the question is whether there has been “personal and advertising injury,” which is defined, in part, as the offense of an oral or written publication, in any manner, of material that violates a person’s right of privacy. Data breach + personal information being revealed = no surprise that attempts will be made to obtain coverage, for such losses, under a provision that addresses violation of the right of privacy. However, at some point this issue may be minimized as Insurance Services Office, Inc. does not believe that such cyber claims should be covered under a commercial general liability policy. To that end, ISO recently filed data breach exclusions for certain of its policies. Putting aside some different formats, a CGL exclusion (with a May 2014 date) has been filed titled “Exclusion – Access or Disclosure of Confidential or Personal Information and Data-Related Liability – with Limited Bodily Injury Exception.”

Coincidentally, right as the Target story was in full gear, a Connecticut appeals court issued an opinion that addressed the potential for general liability coverage for a loss of personal information. In Recall Total Info. Management, Inc. v. Federal Ins. Co., No. 34716 (Conn. App. Ct. Jan. 14, 2014) the court addressed whether a data breach case constituted a publication of material, that violates a person’s right to privacy, under the following wacky facts.

Recall entered into a records storage agreement with IBM. Recall agreed to transport and store various IBM electronic media and records. Recall subcontracted transportation services for the work to Ex Log. In February 2007, Ex Log dispatched a van to transport IBM computer tapes offsite from an IBM facility. During the transport, a cart containing the tapes fell out of the back of the van near a highway exit ramp. Before Ex Log realized what happened, approximately 130 of the tapes had been removed from the roadside by an unknown person and have never been recovered. The tapes contained personal identification information for approximately 500,000 past and present IBM employees, including social security numbers, birthdates and contact information. The tapes apparently were of such that they could not be read by personal computers or other machines accessible to the average person.

Putting aside how the claims arose, the court held: “On the basis of our review of the policy, we conclude that personal injury presupposes publication of the personal information contained on the tapes. Thus, the dispositive issue is not loss of the physical tapes themselves; rather, it is whether the information in them has been published. The plaintiffs contend that the mere loss of the tapes constitutes a publication, and has alleged that the information was published to a thief . . . . . As the complaint and affidavits are entirely devoid of facts suggesting that the personal information actually was accessed, there has been no publication.” (emphasis in the original).

What does the case mean? This is how my colleague Josh Mooney answered that question in his newsletter “The Coverage Inkwell,” which addresses emerging coverage issues in intellectual property, privacy and cyber liability:

“On the one hand, the holding in Recall Total is somewhat limited by its facts. Because there was no evidence that the information on the IBM tapes had been accessed, the court held that there was no ‘publication,’ no matter the meaning of the term. In most data breach cases, however, there is evidence that someone accessed the stolen data, either by means of hacking or with the assistance of an inside company employee. Thus, for many cases, Recall Total may be distinguished on its facts.

On the other hand, the case highlights problems with the meaning of publication. For instance, the trial court employed the meaning of publication as used in the tort of defamation. The ‘publication’ element in a right of privacy/publicity given to private life tort, however, is much more stringent. Most states, following the Restatement, require a dissemination of the information to the public at large or to so many people that it is substantially certain that the information will become generally known. The appellate court never seemed to consider such a stringent requirement; although, it did not have to because of the unique facts of the case.

Nevertheless, some may choose to characterize this case as one requiring a very low threshold for the ‘publication’ element of ‘personal and advertising injury’ in the context of a data breach claim. Given the paucity of published data breach coverage cases, this decision may get more attention that it merits.”

Not surprisingly, policyholder counsel see Recall Total as supporting general liability coverage for a data breach, despite the court’s actual decision in the case. Roberta Anderson of K&L Gates, writing in a client alert (that was picked up by The Wall Street Journal) described the decision like this: “Although the insureds in the Recall case did not hit the coverage bulls-eye, in contrast to the facts in that case, there is no doubt that there has been a ‘publication’ of the data of those individuals impacted by the Target data breach. Under Recall, therefore, and numerous other cases, the ‘personal injury’ coverage presumably would be triggered by the facts in connection with the Target breach. Where there has been a ‘publication’ (an undefined term in CGL policies that courts have construed broadly in favor of coverage), numerous courts have upheld coverage for data breaches and other privacy related claims.”

Cyber coverage is also a relatively untested area for a data breach. Target’s $90 million of such coverage may provide a test of how such policies (which are manuscript and differ widely in what’s offered and how they are drafted) respond.

But the biggest insurance story to come out of the Target situation is likely to be the insurance industry’s ability to use the Target data breach to demonstrate the need for companies to have cyber liability coverage. For the past few years some insurers have been placing a lot of emphasis on their cyber insurance policies. Has there been a big take-up rate? Nobody knows that for sure. However, The Wall Street Journal recently reported that only 31% of respondents to a research center’s survey had insurance to specifically protect against a data breach. [And that number seems high to me.] Insurers that have been marketing cyber policies can thank Target (and Nieman Marcus) for the immeasurable free advertising that the companies’ data breaches have provided to them in this effort. If the take-up rate for cyber policies is low, even after such well-publicized breaches, then perhaps there is not as wide of a market for the coverage as some believe (at least not yet).

|

|

| |

|

|

|

|

|

|

Vol. 3, Iss. 2

January 29, 2014

Asbestos: The Cal Ripken, Jr. Of Mass Torts

Read This Asbestos Case – Even You Do No Asbestos Work

|

|

|

Much has been written about asbestos and its role in the tort, bankruptcy and insurance systems. One aspect of the story has always been a perception of the dubious nature of some claims. Think of the mass medical screenings by doctors employed by lawyers.

But even when there is no dispute that a plaintiff was seriously injured, killed in fact, by exposure to asbestos, issues of causation and relative fault of the many defendants have often clouded the litigation. This issue was clearly on display in In re Garlock Sealing Technologies, LLC, No. 10–31607 (W.D.N.C. Bkrtcy. Ct. Jan. 10, 2014).

Even if you do no asbestos work, you are certainly involved, in some manner, with the civil justice system. The Garlock decision is a good lesson in how the system both works and doesn’t. Joe Nocera, long-time editorial page columnist for The New York Times, described the decision as “breathtaking.” It is.

Garlock produced and sold asbestos gaskets, sheet gasket material and packing used in pipes and valves that transported hot fluids in maritime, refinery and other industrial applications. The company was named as a defendant in countless asbestos suits. In 2010 Garlock Sealing Technologies, LLC and some affiliates filed a Chapter 11 petition. An Asbestos Claimants Committee (“ACC”) was appointed to represent existing asbestos disease claimants against the debtors. The members of the ACC are plaintiffs’ law firms representing those claimants. A Future Claimants Representative (“FCR”) was appointed to represent future asbestos disease claimants. At issue was the creation of a fund for resolution of present and future asbestos-related mesothelioma claims.

The parties had two distinct approaches to this estimation. Garlock offered a “legal liability” approach. This considered the merits of the claims in the aggregate based on the projected number of claimants and their likelihood of recovery. The ACC and FCR offered a “settlement approach.” This was based upon an extrapolation from Garlock’s history of resolving mesothelioma claims. These two approaches produced staggeringly different estimates. Garlock’s estimate was about $125 million and the ACC/FCR estimates were $1–1.3 billion.

The bankruptcy court concluded that Garlock’s aggregate liability for present and future mesothelioma claims was $125 million. How and why the court adopted Garlock’s (significantly) lower number is explained in detail in the court’s rather long opinion. The opinion sets forth the court’s decision following a hearing that took place over seventeen trial days that included 29 witnesses and hundreds of exhibits.

One aspect of the court’s decision comes under the category: “social science” evidence relating to practices in asbestos tort litigation. This is discussed here.

By the account of even an opposing expert, Garlock, as a gasket manufacturer, was not a significant asbestos defendant. “Nevertheless, Garlock was an active litigant in the tort system for thirty years—until its insurance ran out. During that time it tried to verdict a number of cases: it won defense verdicts in a very high percentage of those trials, but it suffered million-plus dollar judgments in a few cases. Garlock negotiated settlements in over 99% of the twenty thousand mesotlelioma cases in which it was a defendant. Garlock’s evidence at the present hearing demonstrated that the last ten years of its participation in the tort system was infected by the manipulation of exposure evidence by plaintiffs and their lawyers. That tactic, though not uniform, had a profound impact on a number of Garlock’s trials and many of its settlements such that the amounts recovered were inflated.”

How did it come to be that a company, that should have been a minor player in asbestos litigation, was subjected to such significant liability? The court provided a detailed explanation.

“One of Garlock’s primary defenses was to deflect responsibility to other co-defendants. Garlock’s contention was that its encapsulated chrysotile product did not cause injury. Evidence of the plaintiffs’ exposure to other co-defendants products was essential to its defense and its negotiating position.” But Garlock’s ability to lay off its responsibility to other defendants’ ended when bankruptcy removed such companies from the litigation. This was particularly pronounced when a wave of bankruptcies wiped out insulation manufacturers as co-defendants in its cases.

Adding to the problem for Garlock, the court explained, was that often the evidence of exposure to the insulation companies’ products also “disappeared.” This was a result of an effort by some plaintiffs and their lawyers to withhold evidence of exposure to other asbestos products and to delay filing claims against bankrupt defendants’ asbestos trusts until after obtaining recoveries from Garlock and other viable defendants.

For example, the court permitted Garlock to have full discovery in fifteen cases that it had settled for large sums. Garlock demonstrated that exposure evidence was withheld in every one of them. On average plaintiffs disclosed only about two exposures to bankruptcy companies’ products. Yet, after settling with Garlock, these plaintiffs made claims against about nineteen such companies’ trusts. Garlock identified 161 cases during the relevant period where it paid $250,000 or more. The limited discovery allowed by the court demonstrated that almost half of those cases involved misrepresentation of exposure evidence.

Now, compare those cases to ones where Garlock was able to obtain evidence of trust claims that had been filed and use such evidence in its defense at trial. In three such trials, Garlock won defense verdicts and in a fourth it was assigned only a 2% liability share.

Looking at all this evidence the court concluded that “withholding of exposure evidence by plaintiffs and their lawyers was significant and had the effect of unfairly inflating the recoveries against Garlock from 2000 through 2010. The court makes no determination of the propriety of that practice. The only thing that is important for this proceeding is that the practice was sufficiently widespread to render Garlock’s settlements unreliable as a predictor of its true liability. Consequently, Garlock’s settlement and verdict history during that period does not reflect its true liability for mesothelioma in the pending and future claimants.”

In re Garlock Sealing Technologies is a lengthy decision and there is more to it than just this. If you are involved in asbestos claims the full opinion is recommended reading. But even if you are not involved in asbestos per se, the decision is a good lesson in the civil justice system. The tort system failed Garlock. At least now the bankruptcy system is doing what it can to pick up some pieces.

|

|

| |

|

|

|

|

Vol. 3, Iss. 2

January 29, 2014

Federal Appeals Court Turns Uncovered “Disgorgement” Into Covered “Damages” -- Insurer Unable To Rely On Level 3

|

|

|

Insurers sometimes maintain that a loss is not covered because, well, it’s not covered. In other words, their position is that the loss is not covered because it is not a scenario that the policy was intended to cover. It is somewhat of a “we know a covered claim when we see one, and this one isn’t” situation.

But courts set out to resolve coverage questions by, first and foremost, interpreting the words of the insurance policy. [Whether they followed through with that promise is likely tied to whether you agree with the outcome.] Based on this, the policyholder’s response is likely “we also know a covered claim when we see one, and this one is because the policy language says so.”

While policy language is of course king, there are some fundamental principles that dictate insurance coverage that are not always based on the policy language. One of these is that an insured cannot obtain insurance coverage for having to return something that it was never entitled to keep in the first place. This issue arises frequently. But if there is no specific policy language to point to that says so, which is often the case, it can sometimes be more difficult to convince policyholders that no coverage is owed for this reason.

Despite a sometimes absence of specific policy language on this point, insurers have generally done well convincing courts of the soundness of this argument on account of it being a general principle of insurance law. While the insurer in Beaumont Hospital v. Federal Insurance Company, No. 13-1468 (6th Cir. Jan. 16, 2014) did not succeed in making this argument, its overall soundness is demonstrated by the court’s need to split hairs to reach its decision. Granted, the issue in Beaumont Hospital arose in the context of policy language – the definition of “loss” did not include “disgorgement.” Nonetheless the case has relevance to those situations where the issue is one of a fundamental principle.

At issue in Beaumont Hospital was a class action suit, brought by two registered nurses, neither of whom Beaumont employed, against eight Detroit-area hospital systems including Beaumont. The nurses claimed that the hospitals had violated certain antitrust laws by conspiring to depress wages of the nurses and exchanging information regarding the compensation of nurses, which had the effect of depressing their wages. In total, the nurses sought approximately $1.8 billion in damages.

To make a long story short, Beaumont settled and Federal Insurance paid approximately $9 million. However, Federal argued that the settlement constituted disgorgement and was not considered a Loss under the policy and thus was uninsurable. Federal made the payment under a reservation of rights and a coverage action would determine if coverage was in fact owed.

The policy at issue expressly provided coverage for antitrust claims. However, that does not affect the case’s relevance to other, more traditional, liability coverages.

Federal’s argument, that no coverage was owed, was exactly what you have expected to see: “[T]he nurses’ claims arose from Beaumont’s gaining of profit, remuneration, or advantage to which it was not entitled and the settlement was a disgorgement of that advantage. Federal argues that the advantage gained was nursing services at below-market compensation and that settlement is clearly disgorgement of the value of that advantage. Consequently, according to Federal, under the Policy, which expressly declines coverage of amounts constituting disgorgement, there is no coverage for what Beaumont’s nurses receive from the Underlying Lawsuit.”

This is the classic, and usually accepted, argument that an insured cannot obtain insurance coverage for having to return something that it was never entitled to keep in the first place. But the Beaumont Hospital court did not do so.

Federal relied on several cases, including, heavily, Level 3 Communications v. Federal Insurance, the Seventh Circuit’s 2001 opinion, authored by Judge Posner, that is the grand daddy case on this issue. The Level 3 court held that, when relief labeled as damages was “restitutionary in character,” it is uninsurable.

Beaumont argued that “money unlawfully retained is not the same in its legal character as money wrongfully acquired. Moreover, money paid to resolve a legal dispute is not necessarily a return of something to which the payor was not legally entitled in the first place.” (emphasis in original).

The court looked at definitions of disgorgement and damages and held that “the hospital never gained possession of (or obtained or acquired) the nurses’ wages illicitly, unlawfully, or unjustly. Rather, according to the nurses’ complaint, Beaumont retained the due, but unpaid, wages unlawfully. This is not mere semantics. Retaining or withholding differs from obtaining or acquiring. The hospital could not have taken money from the nurses because it was never in their hands in the first place. While the hospital’s alleged actions are still illicit, there is no way for the hospital to give up its ill-gotten gains if they were never obtained from the nurses. Therefore, the damages Beaumont paid in settlement of the claim does not constitute disgorgement.” (emphasis in original). The court was also influenced by the fact that the exclusion stated that only disgorgement was not a covered loss. However, because the policy used the term restitution elsewhere, Federal should have been aware of the difference between the two terms.

The court distinguished Level 3 and its progeny on the basis that such cases “all involve wrongfully acquiring something—such as stealing from pension funds, securities fraud, or unlawfully levied taxes. (citations omitted). Thus, the actors in these cases were subject to disgorgement because they retained funds unlawfully.”

Thus, the court held that the settlement did not constitute disgorgement under the policy and was therefore covered.

The court also rejected the argument that Michigan public policy precluded coverage -- no one should benefit from his own wrongdoing. Federal contended that if it had to insure Beaumont, the hospital will profit from its own wrongdoing and transfer the cost of returning money wrongfully withheld to the insurer. Federal further argued that providing coverage for the settlement would encourage moral hazards because it would incentivize wrongful behavior.

Rejecting the moral hazard argument, the court saw it this way: “Here, in addition to the damage to the reputation of Beaumont, the hospital also faced up to $1.8 billion in damages. The Policy limit for anti-trust claims is $25 million—far less than the threatened $1.8 billion which the plaintiffs sought jointly and severally from Beaumont. No insured is likely to bet on a gain of $25 million against a loss of $1.8 billion.”

The court got this decision wrong. There is no other way to say it. Call it what you want, but the settlement was for the hospital’s payment of wages for nursing services for which it benefitted. The correct payment of the nurses wages was simply delayed on account of their need to prove that the hospital short-changed them. In the end, Federal was forced make some of the hospital’s payroll.

|

|

| |

|

|

|

|

Vol. 3, Iss. 2

January 29, 2014

Court Provides A Detailed Discussion Of How To Achieve

"Additional Insured" Cost Sharing For Construction Defect

|

|

|

Anyone reading this knows that construction defect claims often involve a lot of parties. I was once involved in a California CD case, with so many parties, that when it came time for a mediation in Los Angeles it was necessary to rent the Kodak Theatre to accommodate all of the defense lawyers, coverage lawyers, claims professionals, party representatives and experts. And it’s not surprising that there were so many players. After all the case was about a defective door knob. [That was a joke. But because it is also so believable I thought it best to say so.]

The coverage issues surrounding construction defect can be, in and of themselves, complex and lacking consensus. But there is sometimes another layer of complexity that gets placed on top of an already vexing situation – how to resolve coverage owed to a general contractor when numerous of its subcontractors were obligated to afford it additional insured status. Then consider that some of the subcontractors did not acquire the promised insurance for the GC. And of those who did, they may not have obtained coverage for an equal period of time. This may all be workable when there are only one or two subcontractors sitting at the table next to the general contractor. But what about when there are many more than that – dozens even.

This Gordian Knot was addressed in detail in Travelers Indemnity Co. v. AAA Waterproofing, Inc., No. 10-2826 (D. Colo. Jan. 17, 2014). Given the thoroughness of the opinion it may become one that other courts, confronting this unwieldy situation, choose to follow.

The court in AAA Waterproofing did a good job of taking an obviously complex case and distilling it into simple terms. I’ll try to do the same. A homeowners association filed an action against D.R. Horton, the general contractor for the construction of a residential community, for alleged construction defects. DRH’s contracts with its various subcontractors required each of them to carry a commercial general liability policy naming DRH as an additional insured. Numerous third-party defendants were subcontractors that performed work or their insurers. Travelers insured some of D.R. Horton’s subcontractors.

The construction defect litigation was ultimately settled for $39.5 million. In the course of litigation, DRH incurred approximately $1.2 million in fees and costs. DRH attempted to negotiate with Travelers and other subcontractors’ insurers regarding the extent of their obligations for payment of DRH’s defense. DRH sought to recover the $200,000 deductible that it paid and the amount that DRH’s insurer paid in defense (DRH’s insurer assigned this claim to DRH).

DRH and Travelers settled their claims against each other. The court determined that Travelers’ obligation to defend DRH was joint and several. Thus, at issue was the extent that Travelers was entitled to recover from other subcontractors, and their insurers, for having paid more than its equitable share of DRH’s defense fees and costs in the construction defect litigation.

How to allocate DRH’s defense costs and fees incurred in the construction defect litigation was no small task when you consider that there were 54 subcontractors implicated by DRH in the underlying CD litigation (or their respective insurers), with only 23 subcontractors represented as parties or by their insurers in the allocation case.

The court looked at various approaches to allocation. First, while its discussion was brief, the court rejected allocating by respective liability for the underlying construction defects. The court considered this to be neither a workable nor reliable way to determine each subcontractor’s respective liability given the settlement in the underlying case.

The court also easily rejected a policy limits-based allocation method in this case. “[S]uch a system is not workable in this case, because numerous parties failed to obtain the requisite insurance policies, making them de facto self-insurers without policy limits upon which to base their allocation. The process of determining the allocation for such de facto insurers would require the Court either to adopt an arbitrary policy limit for them, or to hybridize its approach and assign a policy limit based on a time-on-the-risk determination of the scope of its de facto policy.”

Having rejected these approaches the court settled upon an “equal shares” method, concluding that it will result in the most equitable allocation under the circumstances. “While equal shares allocation has been applied in a minority of jurisdictions, the circumstances of this case—in which each subcontractor/insurer had a joint and several duty to provide a complete defense to DRH, and no reliable method exists to tie allocation to liability or policy limits—militates in favor of a holding that those subcontractors/insurers’ responsibility for equitable contribution to DRH’s defense costs should be apportioned evenly.”

Even though the court decided upon “equal shares,” there were still more issues to be addressed. For example, how should shares be assigned? One share per subcontractor or one share per policy? After looking at the competing arguments the court concluded that the most equitable allocation method was to divide the contribution amounts into equal shares per subcontractor. The court found persuasive Travelers’ argument that, “because each subcontractor (or its respective insurer) owed DRH a complete duty to defend only once, a subcontractor that held multiple policies should not be allocated multiple shares.”

Lastly, which subcontractors should be included in the allocation? The court rejected the subcontractors argument that allocation should be applied to all 54 subcontractors implicated by DRH in the construction defect litigation. Instead the court adopted Travelers’s approach that allocation should apply only to the subcontractors who were represented in the case, either directly or through their insurers.

While the court in AAA Waterproofing explained that its decision, to adopt equal shares, was justified by the circumstances of the case, those circumstances are not so unique when it comes to multi-party construction defect litigation -- each subcontractor/insurer has a joint and several duty to provide a complete defense to the general contractor, no reliable method exists to tie allocation to liability or policy limits, some subcontractors did not obtain insurance, some obtained more than others and not all subcontractors are before the court.

Again, given the thoroughness of AAA Waterproofing it may become a case that other courts, confronting this unwieldy cost sharing situation, choose to follow.

|

|

| |

|

|

|

| |

|

|

|

|

|

|

|

|

|

|