It has now been about a month since the massive financial losses, on account of the Covid-19 pandemic, arrived at an inevitable door step -- the insurance industry’s.

There are various tall hurdles to the potential availability of business interruption coverage for Covid-19 losses. But history teaches that, in the face of wide-spread social problems, a place will be set at the table for insurance companies’ capital -- even if not deserving of an invitation.

If you are reading this, then you have read umpteen other articles, over the past few weeks, addressing the numerous issues associated with the potential availability of coverage for the pandemic. You know all of this: business interruption coverage requires that there be direct physical loss of or damage to property of some sort; many business interruption policies contain virus exclusions; at least five states have introduced legislation designed to eliminate the first two things I said; and several suits have already been filed by policyholders seeking a determination of coverage for their business interruption losses.

I believe that there are four principal takeaways, from the past month, concerning the pursuit of business interruption coverage for Covid-19 losses. One of them isn’t getting much attention. They are as follows:

- Policyholders will sometimes be asserting that insurers, that issued immediate denials for Covid-19 claims, did so in bad faith on account of an alleged failure to investigate the claim under applicable law

- One business interruption coverage theory in particular is getting attention from policyholders.

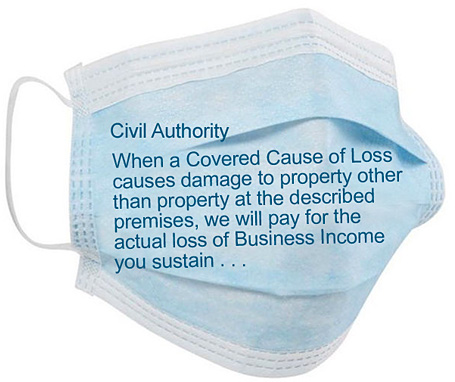

- Another business interruption coverage issue has not received a lot of attention. The biggest push for coverage has been for businesses that have been shut down by order of a civil authority. However, even if owed, such coverage is likely quite limited. Civil authority-based business interruption coverage, per policy language, is usually available for only up to four weeks.

- The restaurant industry is beating the loudest drum in the pursuit of business interruption coverage.

A closer look at each of these follows below.

Policyholders Assert Bad Faith For Insurers’ Alleged Failure To Investigate Claims

The first few declaratory judgment actions, seeking coverage for Covid-19 business interruption losses, were filed before the insurer disclaimed coverage. In other words, they were filed by policyholders in anticipation of being denied coverage. As a result, they did not include any insight into how policyholders may challenge insurer denials or position their cases. However, at least two declaratory judgment actions, filed after a coverage denial, do so.

In Big Onion Tavern Group, LLC, et al. v. Society Insurance, Inc., No. 1:20-cv-02005 (N.D. Ill. March 27, 2020), the insureds -- restaurants and movie theaters -- maintain that their insurer’s denial of business interruption coverage was wrongful, raising such issues as the absence of a virus exclusion in the policy and the argument that, “if a virus could never result in a ‘physical loss’ to property, there would be no need for such an exclusion.”

In addition to addressing the substantive coverage issues, the insureds also alleged that, upon receipt of the claims, the insurer “immediately denied the claims (either verbally or through cursory emails) without conducting any investigation, let alone a ‘reasonable investigation based on all available information’ as required under Illinois law.” The insureds seek damages for statutory bad faith.

Likewise, in Barbra Lane Snowden d/b/a Hair Goals Club v. Twin City Fire Insurance Company, No. 2020-106538 (Dist. Ct. Harris County, Tex. March 26, 2020), the policyholder – a wig store -- alleged that its insurer wrongfully denied coverage for Covid-19-caused business interruption losses. Here too the complaint included a bad faith claim for the insurer’s alleged failure to “adequately and reasonably investigate and evaluate plaintiff’s clams.”

Policyholders can be expected to assert similar claims if they believe that an insurer’s denial did not follow an adequate or reasonable investigation under applicable law.

The “Public Space” Theory For Civil Authority Coverage

Two principal challenges, to the potential availability of business interruption coverage for Covid-19 losses, are the requirement that there be direct physical loss of or damage to property at covered premises and many business interruption policies contain virus exclusions.

While we can expect to see policyholder challenges to the virus exclusion, it is certainly going to pose a serious obstacle to obtaining business interruption coverage.

The requirement for direct physical loss of or damage to property at covered premises presents another barrier to business interruption coverage. Businesses have been closed principally to foster social distancing and not on account of the presence of the virus inside a premises. And even if Covid-19 were present inside a covered premises, does that mean that there was direct physical loss of or damage to property? Many cases have been cited, in countless recent articles by insurer- and policyholder-side counsel, arguing both sides of this issue. But even if the presence of Covid-19 inside a premises is property damage, business closures for this reason are likely to be few and far between.

Facing this appreciated hurdle, a push is being made -- especially under non-virus exclusion policies – for civil authority coverage, based on what I call the “public space” theory. Civil authority coverage is usually included as part of business interruption.

The key to the argument is that, for purposes of civil authority coverage, there need not be direct physical loss of or damage to property at the covered premises. Rather, in general, business interruption coverage is potentially implicated if the action of a civil authority prohibits access to the covered premises -- on account of damage to other property, i.e., property not at the covered premises.

Seemingly because of the challenge of proving property damage at the covered premises, a civil authority-declaratory judgment complaint, recently filed in California state court, focuses its attention on proving property damage at other property. The other property is the public space.

In French Laundry Partners, LP dba The French Laundry, et al. v. Harford Fire Insurance Company, et al., the plaintiff alleges that access to restaurants has been prohibited by an order of civil authority as a direct result of a covered loss in the immediate area. In other words, the property damage was not at the restaurants.

Seeking to satisfy the “property damage at other property” requirement, the complaint argues that Covid-19 has physically impacted “public and private property, and physical spaces in cities around the world and in the United States.” To support this allegation, the complaint asserts that the virus “physically infects and stays on surfaces of objects or materials, ‘fomites,’ for up to twenty-eight days” and notes that “China, Italy, France and Spain have implemented the cleaning and fumigating of areas” before allowing those areas to re-opened to the public.” The complaint further asserts that the stay at home order states that it is being “issued based on evidence of physical damage to property.” [Certainly some civil authority orders seem to be attempting to “plead into coverage,” so to speak, by including such statements.]

This “public space” argument is also being pushed by the Business Interruption Group (“BIG”), an initiative recently formed by several high-profile chefs, to advocate for business interruption coverage for restaurants. More about BIG below. Its website makes the following “public space” argument:

“To avoid payments triggered by a Civil Authority Shutdown, the insurance industry is spreading deceptive propaganda indicating that the virus does not cause a dangerous condition to property. This is a lie. It is both factually and legally untrue. This disinformation campaign is intended to deceive policyholders about their coverage.

But mayors and governors around the country began Civil Authority Shutdowns, stating clearly in emergency executive orders that “the virus physically is property loss and damage.” Orders in New York City, New Orleans, Atlanta, Key West, Oakland Park, Pensacola, Napa, Panama City, Hillsborough County (FL), Broward County (FL), Harris County (TX), and the State of Colorado, also include the requisite language needed to trigger coverage. Despite these government proclamations, in order to avoid paying billions in property damage owed to restaurants, insurers have continued to deny that the novel Coronavirus attaches itself to physical property. They are purposefully misleading officials about the danger of Covid-19 in order to save themselves money.” (emphasis in original)

Necessity has always been the mother of creative arguments for coverage. Time will tell where this one goes.

The Overlooked “Civil Authority” Issue

So much has been written about the potential availability of business interruption coverage because of businesses being forced to close on account of a civil authority order.

Often overlooked in this discussion is the fact that, even if civil authority-based business interruption coverage were owed, such coverage is likely extremely limited. It is usually available for up to four weeks.

Policies vary, but this is generally a provision that you can expect to see in a civil authority coverage grant. [This is certainly the case in the policies that I have reviewed in assessing Covid-19 claims.]

For example, ISO’s standard Business Income form [CP 00 30 10 12] includes such a time limit for its civil authority grant of coverage. The policy form provides as follows:

“Civil Authority Coverage for Business Income will begin 72 hours after the time of the first action of civil authority that prohibits access to the described premises and will apply for a period of up to four consecutive weeks from the date on which such coverage began.”

Thus, even if policyholders can overcome a virus exclusion, and trigger civil authority-based business interruption coverage, in most cases the period for coverage will be up to four weeks. The way things are going now, this is far less than the time in which their businesses will be closed.

The Restaurant Industry And The Pursuit Of Coverage

The bulk of the early coverage actions, for Covid-19 business interruption losses, have been brought by restaurants and bars.

Another push for business interruption coverage for restaurants comes by way of the Business Interruption Group, an initiative formed by several high-profile chefs, to serve as a national legal, political and communications campaign to advocate for business interruption coverage.

In its April 1st press release, announcing its formation, BIG “demands immediate insurance payment for Civil Authority coverage that does not contain a virus exclusion, and supports a negotiated solution for federal subsidies for insurers who waive exclusions on policies.”

According to BIG, the restaurant industry employs more than 15.6 million Americans, making it the largest private sector employer in America.

BIG reports that the chefs had a call with President Trump, to introduce him to the campaign, and he was supportive, said he understands insurance and asked to see the policies to read them for himself.

BIG was launched in partnership with veteran New Orleans insurance attorney John W. Houghtaling II, of Gauthier, Murphy & Houghtaling, which led the Castano tobacco litigation that resulted in a $286 billion settlement. Mr. Houghtaling filed the first known coverage action for Covid-19 business interruption losses (involving Oceana Grill in NOLA’s French Quarter), as well as French Laundry Partners, discussed above.

Conclusion

So much remains unknown about the eventual impact of Covid-19 on health, the economy and just about every aspect of business and society. This includes insurance coverage.

|