|

|

|

|

|

|

Vol. 7 - Issue 4

May 9, 2018

|

|

|

|

|

|

| |

A fifty Dollar fine and probation. That’s the sentence Judge Robert Braithwaite tells me, laughing, that he’d impose on Yogi Bear for stealing a picnic basket in Jellystone National Park. Braithwaite knows of what he speaks. He is a United States Magistrate Judge for the District of Utah, whose jurisdiction includes the state’s five immensely popular national parks.

Summer is upon us. Many will be headed to Zion, Bryce and Utah’s other spectacular national treasures. What better time to speak to Judge Braithwaite about his unique job, traveling the state, to hear the cases of alleged law-breakers on Utah’s federal lands. I know it’s going to be an entertaining conversation as I’ve heard some of these stories in Braithwaite’s book on the subject – Have Gavel Will Travel. My conversation with Judge Braithwaite was by phone. Misstep in a Utah national park -- and yours will be in person.

I had been under the impression that national parks are subject to all kinds of quirky laws designed to protect their majesty. They aren’t, I learn. No, I won’t go to jail for failing to yield the right of way to a squirrel, Braithwaite assures me. But while national parks may not have unique crimes, His Honor is clear that, in his courtroom, miscreants on this sacred land may have a higher price to pay.

|

| |

The Road To The National Parks

Before putting on a robe as a U.S. Magistrate, Judge Braithwaite, 67, native of Ithaca, New York, spent sixteen years on the Utah state bench. His docket was limitless. From parking tickets to sentencing a man to death and everything in between. He also sat three times by designation on the Utah Supreme Court – in one instance authoring a dissenting opinion. Bold move by a guest, for sure. I ask Braithwaite if they told him not to expect another invitation back. He laughs. “No, they were very friendly.”

But the years of hearing divorce, rape and murder cases, Brathwaite says, left him “worn down by the continual stream of problems and crimes.” “After so many cases with perpetrators and victims you start to get a little jaded in your view of humanity.”

Braithwaite left the state bench and took his current position in 2003. It was a return to the federal payroll, after having spent a summer in college as a Washington Monument elevator operator. As a Magistrate Judge, Braithwaite handles the “front end of felonies” and about 90% of the federal misdemeanors in Utah. “I’m the king of the misdemeanors,” he tells me.

|

|

|

|

|

It is a much different situation these days from Braithwaite’s constant tales of tragedy as a state court judge. While there can still be victims, he tells me, there is vastly less pressure. In a child custody case, “that five year old will suffer the consequences if you pick the wrong parent,” Braithwaite says. It is not the same in his current position: “If I find a speeder [guilty] or a camp fire violation, and I’m wrong, it’s not the same.” |

|

Riding The Circuit

In addition to Utah’s national parks, Judge Braithwaite’s jurisdiction includes the state’s other vast federal lands, such as that owned by the U.S. Forest Service, Bureau of Land Management and the popular Lake Powell. It’s a huge territory, covering 28,000 square miles. Plus he is responsible for federal crimes committed on state land, such as bank robbery and certain drug offenses. To mete out justice, Braithwaite “rides the circuit,” spending one day a month in four locations around the state. And these are not trips around the block. To get to Big Water, where he hears cases emanating from Lake Powell, Braithwaite travels 150 miles – “none of it freeway,” he points out. “I drive over a mountain range, down into a valley and then the second half I’m driving across the desert.” His drive to Moab to hear cases is 300 miles.

But a one day a month schedule is not suitable for defendants in custody. For this Braithwaite uses phone and email to make and convey decisions on their release. “I tell people that in the summer I never work a forty hour week,” but, he explains, “I almost always work seven days a week, even if it’s only for an hour. On a Sunday I’ll get a call from Lake Powell or Zion and I’ll deal with a drunk driver. And that’s fine.”

Utah’s federal lands have been in the news lately. In late 2017 President Trump signed executive orders shrinking two of Utah’s national monuments – Bears Ears (by 85%) and the Grand Staircase-Escalante (by half). As for the impact that this could have on Braithwaite’s job, he declines to speculate. |

| |

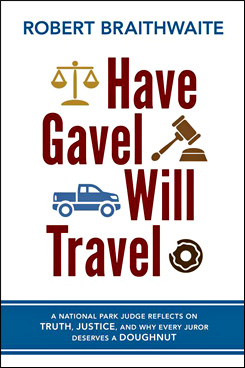

Have Gavel Will Travel

“You should write a book” is something that those with interesting jobs are frequently advised. Braithwaite heard that suggestion often. So he did. His 2015 Have Gavel Will Travel is a wonderfully entertaining, easy read, laugh out loud, look at his experiences on the bench.

Braithwaite recounts a hunter who had an ultra-light plane relay the GPS coordinates of a ram in Capitol Reef National Park, where hunting is illegal. The ram was killed. “This is hunting?,” Braithwaite asks. Then there’s the guide who forced a black bear up a tree in Dixie National Forest. The guide then called his client, who drove four hours from Las Vegas, to shoot the bear out of the tree. Braithwaite’s conclusion: “Contrary to what they may tell admirers of the bearskin rug spread out in their den, hunters like that have the cojones of BBs.”

The use of marijuana in national parks is illegal and will get you arrested. Some claim to have a defense. But waving your California medical marijuana prescription card won’t work. Braithwaite observes that “many a Californian has risen from his deathbed to smoke some pot while taking in the wonders of spectacular Southern Utah.”

|

|

|

|

|

There are many more stories of the law meets the national park in Have Gavel Will Travel. But Braithwaite can tell them better than me. Find it on Amazon. You won’t be disappointed.

But more than just anecdotes about interesting cases, Have Gavel Will Travel is also deeply personal. Writing in a self-deprecating manner, Braithwaite shares insecurities and angst that come with wearing a robe. The book makes you realize – sometimes easy to forget -- that judges are human too. |

| |

Don’t Spoil Someone Else’s Vacation

While national parks are not subject to unique federal laws, that does not mean that all federal law violators are the same. I pose this scenario to the judge. Littering is littering, but is there a difference between doing it in a national park versus leaving the same trash on the steps of a federal courthouse? “Not by the law; but there is in some instances with me,” Braithwaite tells me. Fines are often quoted as “up to” a certain amount. For a national park offense, Braithwaite says, “I might go on the higher end for something in a national park and toward the lower end on something that was not in a national park.”

“If people plan a trip and bring their families and stay in the campground at Zion National Park, it’s something that they look forward to all year.” If someone comes in and gets high on drugs, and ruins the vacation of people around them, “that calls for a stiffer penalty . . . then the same offense might get outside the national park. But that’s not written into the law, that’s just my philosophy.” |

| |

| |

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Vol. 7, Iss. 4

May 9, 2018

The New England Patriots Hater

And Insurance Coverage

|

|

|

|

|

| |

Sports fans’ passion for their teams often runs deep. Some fans will go to extreme measures to satisfy it, sometimes even filing a law suit. Litigation has arisen over such things as fans’ unhappiness with their season tickets, inability to get Super Bowl tickets, a belief that they did not get their money’s worth from the play on the field and a host of other situations.

But what happened in Connors v. Hamilton, No. 17-0224 (Mass. Super. Ct., Essex Cty., Nov. 17, 2017) is hard to believe, even in the world of sports -- and especially pro football -- fanaticism. Then, that this remarkable case gave way to a coverage decision, can only be described as an embarrassment of riches.

Elizabeth Connors and Ethel Hamilton were septuagenarian next door neighbors in Swampscott, Massachusetts. Connors was a long-time New England Patriots fan, going back to the days of Jim Nance. Fifteen feet away lived Ethel Hamilton, a life-long Atlanta Falcons fan, who liked to recount her time watching Claude Humphrey play.

Connors and Hamilton spent many years talking football and good-naturedly taking shots at each other’s team, as sports fans are wont to do. But innocent ribbing ended in February 2017, after Super Bowl LI. From that point on the two women stopped speaking to each other. As sports fans know, in Super Bowl LI, the New England Patriots came back from a 25 point deficit to beat the Atlanta Falcons, 34-28, in overtime. It is one of the greatest comebacks in sports history. For Falcons fans it caused unimaginable heartbreak.

Shortly after the Patriots epic win, Connors hung a Patriots flag on the 20 foot flag pole outside her home. The flag pole had been dormant for years but Connors decided that the time to resurrect its use had now come. Hamilton was incensed by Connors’s flag flying. She was grieving over the Falcons loss and Connors knew it. As Hamilton saw it, flying the Patriots flag was insensitive, a tremendous insult and, as she put it, “rubbing a salt mine in an open wound.” Connors, for her part, insisted that she meant no insult by the flag. It was simply a way to express her excitement for the greatest Patriots win of all time.

Hamilton asked Connors to take down the flag. Connors refused. So Hamilton did what aggrieved people -- even septuagenarians in Swampscott, Massachusetts – do. With her grandson serving as her lawyer, Hamilton filed suit against Connors, alleging trespass, and seeking damages for intentional and negligent infliction of emotional distress.

Hamilton’s theory was a novel one. While acknowledging that neither Connors, nor her flag or flag pole, physically encroached on Hamilton’s property, the offending flag cast a shadow on Hamilton’s front lawn at certain times of the day. Hamilton alleged that the shadow of the flag, which she knew contained the Patriots logo, even if the logo was not visible on the shadow, served as a trespass, being an intentional and unauthorized entry upon Hamilton’s property.

Connors sought coverage for “the crazy lawsuit,” as she called it, from her homeowner’s insurer -- Chowda Mutual Insurance Company. But Chowda disclaimed coverage, alleging that the suit did not seek damages because of “bodily injury,” “property damage” or “personal and advertising injury.” With no defense forthcoming from her insurance company, Connors turned to her grandson to represent her. So it was the battle of the grandsons, who grew up playing together at their respective grandparents’ homes.

Connors’s grandson filed an answer to the complaint and then a motion for summary judgment, arguing that, as a matter of law, a shadow cast on one’s property cannot qualify as a trespass. Hamilton’s grandson cross moved for summary judgment. The court denied Connor’s motion and granted Hamilton’s.

The court ordered Connors to remove the flag from the pole and, following a damages hearing, in which Hamilton’s psychiatrist testified to his patient’s emotional injuries caused by the flag, awarded Hamilton $37,500. In support of the damages award the court stated: “While the claim is certainly unusual, Connors must take the plaintiff as she found her. And Connors found this plaintiff as a devastated Falcons’ fan.”

Connors, upset with her grandson’s performance, retained another lawyer and filed suit against Chowda Mutual, seeking recovery of the defense costs paid to her grandson, $37,500 paid to Hamilton and a claim for violation of General Laws c. 93A.

The parties filed cross motions for summary judgment. Connors’s motion was granted and Chowda’s motion was denied. In finding that the Chowda Mutual policy provided coverage for defense and indemnity for the Hamilton suit, the court in Connors v. Chowda Mutual Insurance Company, No. 17-0412 (Mass. Super. Ct., Essex Cty., Apr. 27, 2018) looked to the policy’s Liability section, which provided coverage for “personal and advertising injury,” defined, in part, as “the wrongful eviction from, wrongful entry into, or invasion of the right of private occupancy of a room, dwelling or premises that a person occupies.”

The court held that the shadow cast upon Ethel Hamilton’s property, by Elizabeth Connors’s offending flag, unquestionably resulted in the invasion of the right of private occupancy of the dwelling or premises that Hamilton occupied.

As the court explained: “If the right of private occupancy means anything, it means that a Falcons’s fan has the right not to be subjected to the shadow of a New England Patriots flag, not to mention just days after Tom Brady’s performance for the ages, thereby solidifying Brady as the greatest quarterback of all-time, despite the ridiculous deflate-gate allegations, as well as the baseless claims of Patriots cheating.”

[Interestingly, this type of “personal and advertising injury” coverage, under an ISO commercial general liability policy, adds that the wrongful eviction from, wrongful entry into, or invasion of the right of private occupancy of a room, dwelling or premises that a person occupies, must be committed by or on behalf of the owner, landlord or lessor. That was not the case here. However, the liability section of a homeowner’s policy does not always contain the same language as an ISO CGL policy. In this situation, the difference in policy language created coverage under the Chowda homeowner’s policy that would not have existed under an ISO CGL policy.]

|

That’s my time. I’m Randy Spencer. Contact Randy Spencer at

Randy.Spencer@coverageopinions.info |

|

|

| |

|

|

|

|

Vol. 7, Iss.4

May 9, 2018

Gene Simmons, KISS And Insurance

|

|

|

|

Last month The Wall Street Journal had a front page story about Gene Simmons, legendary KISS rocker, and his willingness to be a pitch-man for just about anything. And, as the Journal put it, “experience is no obstacle.”

The Journal went on: “Mr. Simmons has been a pitchman for a vast array of products, including life insurance, translation software, the IndyCar race car league, a new line of soda called MoneyBag and a soon-to-be-launched monthly magazine called Mogul, targeting mom-and-pop investors with limited financial experience.”

Whoa! Hold the phone! Gene Simmons has pitched life insurance? I was reading the article at lunch and nearly choked on my turkey sandwich. Now MY tongue was hanging out. I had to know more.

Sure enough, lots of search results revealed that, in 2010, Simmons co-founded a company called Cool Springs Life that sells premium financed life insurance targeted at high net worth individuals.

|

|

|

|

| |

I don’t know if Simmons is still involved with Cool Springs Life. I couldn’t find his name anywhere on the firm’s website.

In any event, if Simmons is still in the life insurance business, I wrote a song that he can use for the company’s commercials. He can use it to remind people of their mortality and that life insurance cannot be ignored. It’s called “Death.”

Death I hear you calling

But I can’t stop breathing now

Me and my organs are staying

It’s not time for the ground

Just a few more years

And then I’ll give a tomb stone to you

I think I’ll hear you balling

Oh Death you’ll be so blue

Death you’ll be so blue

You say your life now feels so empty

In our house while I lay prone

I’m somewhere else

And you’re left there to groan

Just a few more years

And then I’ll give a tomb stone to you

I think I’ll hear you balling

Oh Death you’ll be so blue

Death you’ll be so blue

Death I know it’s lonely

While you’re still standing upright

Cause me and my organs have seen that bright light.

|

|

|

|

| |

|

Vol. 7, Iss. 4

May 9, 2018

900 New Cases (From 2014 to 2017):

Insurance Key Issues: What Makes The 4th Edition Different

|

|

|

|

|

| |

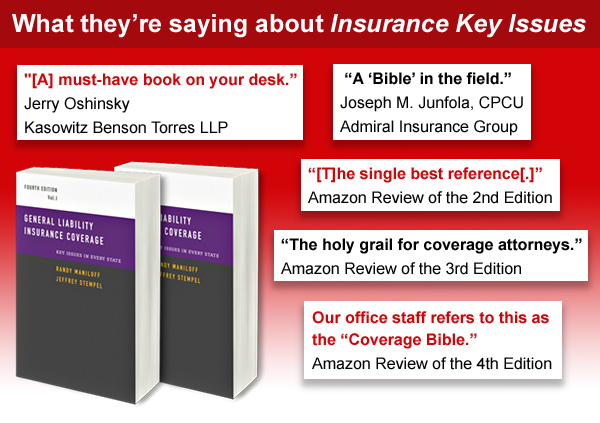

I’ve been getting this question – what’s the difference between the 3rd edition of Insurance Key Issues and the 4th?

The answer is simple. There was a three year gap between the 3rd and 4th editions. In the world of liability coverage, that’s a lifetime. The 4th edition adds over 900 new cases, as well as a chapter addressing the American Law Institute’s Restatement of the Law of Liability Insurance. The new addition also eliminates the chapter on Reasonable Expectations as it is adequately addressed in the 3rd edition.

Obviously some issues generate more new decisions than others. Here is the issue-by-issue breakdown of the new cases discussed in the 4th edition (virtually all decided between 2014 to 2017):

81 - Choice of Law for Coverage Disputes

63 - Late Notice (“Occurrence” Policies): Is Prejudice to the Insurer Required?

18 - Coverage for Pre-Tender Defense Costs

74 - Duty to Defend Standard: “Four Corners” or Extrinsic Evidence?

38 - Insured’s Right to Independent Counsel

27 - Insurer’s Right to Reimbursement of Defense Costs

45 - Prevailing Insured’s Right to Recover Attorney’s Fees in Coverage Litigation

26 - Number of Occurrences

37 - “Any” Insured vs. “The” Insured and the Severability of Interests Clause

22 - Is Emotional Injury “Bodily Injury”?

69 - Is Faulty Workmanship an “Occurrence?”

57 - Permissible Scope of Indemnification in Construction Contracts

14 - Qualified Pollution Exclusion

50 - Absolute Pollution Exclusion

17 - Trigger of Coverage for Latent Injury and Damage Claims

37 - Trigger of Coverage for Construction Defects

50 - Allocation of Latent Injury and Damage Claims

25 - Coverage For Privacy Claims and Cyber Risks

18 - Insurability of Punitive Damages

101 - First- and Third-Party Bad Faith Standards

[To the actuaries: I know. This add up to 869. But I added about 50 more cases after the state-by-state count was done and didn’t keep track of which issues they were. Long story. So many of these issues have a few more new cases.]

Visit the Insurance Key Issues website: http://insurancekeyissues.com

|

|

| |

|

|

|

|

Vol. 7, Iss. 4

May 9, 2018

Announcing The Winners Of The Longest Name Of A Party Contest

|

|

|

|

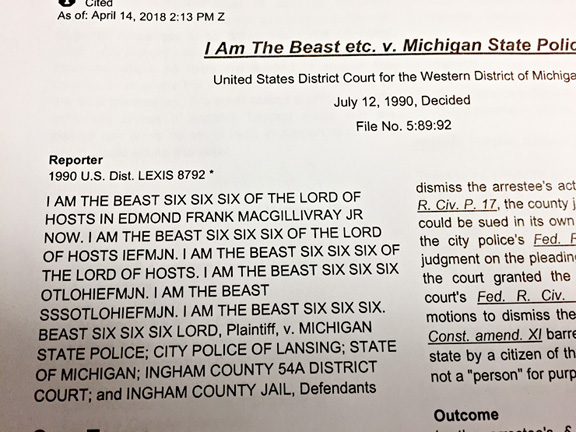

In mid-March the Northern District of California decided Polar-Mohr Maschinenvertriebsgesellschaft GMBH Co. KG v. Zurich, No. 17-1804 (N.D. Calif. March 15, 2018). Yes, that’s really the name of the insured.

As I discussed in the last issue of Coverage Opinions, that’s gotta be the longest name of an insured in the history of insurance. I declared the decision the Supercalifragilisticexpialidocious of insurance coverage.

I mentioned, kinda off the cuff, that I would send a complimentary copy of the 4th edition of Insurance Key Issues to the first person who could send me any case – insurance or not -- involving a party with a longer name. I was not expecting to hear from anyone. Lo, and behold, I heard from two CO readers who took me up on the challenge.

There was Andrew Zotos, of CNA in Princeton, New Jersey, who alerted me to this mouthful of a party name:

I Am The Beast Six Six Six Of The Lord Of Hosts In Edmond Frank Macgillivray Jr Now. I Am The Beast Six Six Six Of The Lord Of Hosts Iefmjn. I Am The Beast Six Six Six Of The Lord Of Hosts. I Am The Beast Six Six Six Otlohiefmjn. I Am The Beast Sssotlohiefmjn. I Am The Beast Six Six Six. Beast Six Six Six Lord.

The Plaintiff maintains that this is his actual name, having purportedly renounced his given name. In a footnote, the court mentioned that it would refer to plaintiff as “I am the beast.” Good idea.

You need proof of this? I understand. I would too. Here you go:

|

| |

|

| |

I also heard from Victor Lund, of The Mahoney Law Firm in Minneapolis, who brought to my attention John H. Krutsch, et al., Respondents, v. Walter H. Collin GmBh Verfahrenstechnik Und Maschinenfabric, 495 N.W.2d 208 (Minn. Ct. App. 1993).

But Victor went a step further. He didn’t just alert me to the case. No. He actually represented a party. And not just any party. He represemted Walter H Collin Gmbh VERFAHRENSTECHNIK UND MASCHINENFABRIC. Total show-off!

The CO Prize Patrol will be paying visits to Andrew and Victor to deliver copies of the 4th edition of Insurance Key Issues. Congratulations!

Visit the Insurance Key Issues website: http://insurancekeyissues.com |

|

|

| |

| |

|

|

|

|

Vol. 7, Iss. 4

May 9, 2018

Coverage Issues: So Just What Are The Majority Rules?

29 States Potentially Afford Independent Counsel For An ROR Defense

|

|

|

| |

|

| |

One of the comments I often hear from readers of Insurance Key Issues is that when they see a coverage issue, set out in a detailed 50 state survey, they realize that the majority rule is not what they thought it was. Or, they had the majority rule correct, but it is more of a majority, or less of one, than they thought.

Based on the 50 state surveys in the 4th edition of Insurance Key Issues, I calculated “scorecards” on the following issues:

Duty to Defend

33 states may look to extrinsic evidence to determine if an insurer is obligated to defend

Insurability of Punitive Damages

38 states potentially afford coverage for punitive damages

Insured’s Right to Independent Counsel

29 states potentially afford independent counsel to an insured being defended under an ROR

Prevailing Insured’s Right To Recover Attorney’s Fees:

45 states have the possibility of an insured recovering its DJ fees

Insurer’s Right to Reimbursement of Defense Costs

18 states support an insurer not being permitted to seek reimbursement of defense costs

(12 states have not addressed the issue)

Emotional Injury as “Bodily Injury”

27 states support a determination that emotional injury can qualify as “bodily injury”

Super Bowl LII

Eagles 41, Patriots 33

Is this what you thought the scores were?

To see a detailed, state by state, analysis of how these scores were calculated – and surveys of 14 more issues -- check out the 4th edition of Insurance Key Issues – Released as the #1 New Law Book On Amazon.

www.InsuranceKeyIssues.com

|

| |

|

|

|

|

Vol. 7, Iss. 4

May 9, 2018

I’m Going To Memphis: Recommendations Sought

Elvis Loves To Tender

|

|

|

|

My wife and I will be celebrating my wife’s 50th birthday in Memphis later this month. She knows we are going away, but doesn’t know where. But she doesn’t read Coverage Opinions so there is no chance that I’m ruining the surprise.

If any Memphis readers out there can kindly send me some recommendations for their favorite restaurants (barbecue for sure) and bars for music I’d really appreciate it. Also, any neat places to see that I wouldn’t know about just following the usual tourist plan. Thanks so much. I really appreciate it. |

| |

|

| |

| |

|

|

|

| |

|

Vol. 7, Iss. 4

May 9, 2018

ALI Vote On The Insurance Restatement At Hand

Lessons From Two Decisions On How The Restatement May Operate In Coverage Litigation

Early Decision: First Winner Of The Insurance Coverage Haiku Contest

|

|

|

|

On May 22, at the annual meeting of the American Law Institute in Washington, D.C., its members are set to vote on final approval of the eight-years-in-the-works Restatement of the Law of Liability Insurance. The RLLI had been scheduled for a final approval vote last May, but it was postponed to address issues raised in the run-up to it. After last year’s postponement, and certain changes made to the draft since then, all signs point to the RLLI being approved at this year’s meeting.

It is no secret that the insurance industry has been no fan of the RLLI and the policyholder-insurer debates over some of its provisions have been spirited. But after a near-decade, a bow is on its way to being tied on the RLLI.

But while one debate over the RLLI may soon be ending, a new one will just be getting underway. After the ALI’s final stamp of approval is put on the RLLI, expect to see it cited by some parties in coverage litigation, using it in an attempt to persuade courts to their side. This will likely result in disputes over the role that the RLLI should play in the court’s decision making.

Nobody can predict the role or impact that the RLLI may have in coverage litigation. But two federal court decisions that have addressed the RLLI – as a draft document – provide some reasonable illustrations.

The Restatement As A Consideration In The Absence Of Judicial Guidance

It is not unusual for a court to come upon a coverage issue of first impression in their state or one in which their law is not clear-cut. When searching for the answer to a coverage question, that otherwise has no answer, or a home-grown roadmap for finding one, courts frequently turn to out of state decisions and/or secondary sources for guidance. Of course these decisions and sources are not binding, but they are instructive to a court in need of an answer.

In the course of doing so, the RLLI may now be included in the list of sources that a court turns to for help in an unchartered territory situation. Knowing that Restatements are developed by learned individuals at the ALI, following a long and painstaking process, it would not be unreasonable that a court would look to what the RLLI has to say about the issue.

Selective Insurance Company of America v. Smiley Body Shop, Inc., 260 F. Supp. 3d 1023 (S.D. Ind. 2017) provides an excellent example of this scenario.

Here an Indiana federal court addressed an insurer’s right to reimbursement of defense costs. The court first noted that there was no Indiana authority that had addressed the issue. So, not surprisingly, the court looked to other decisions for guidance (3rd Circuit, 10th Circuit and Illinois Supreme Court) and noted that these courts found that an insurer did not have a right to recoup defense costs.

Then the court turned to the RLLI (even as a draft) for further guidance, stating: “Additionally, the Draft of Section 21 of the Restatement of the Law of Liability Insurance provides that ‘[u]nless otherwise stated in the insurance policy or otherwise agreed to by the insured, an insurer may not seek recoupment of defense costs from the insured, even when it is subsequently determined that the insurer did not have a duty to defend or pay defense costs.’ Restatement of the Law of Liability Insurance § 21 (Discussion Draft, to be considered by the members of the American Law Institute).”

In the end, the court was not required to answer the reimbursement of defense costs question. However, if it were, the court, using the RLLI for support, was seemingly poised to conclude that the insurer did not have such a right.

In the absence of precedent, or other required-to-be-considered cases, a court in need of an answer to a coverage question may now stir the RLLI into the mix.

Rejection Of The Restatement In The Face Of Judicial Guidance

But what about a court that is addressing a coverage issue that is the subject of precedent in its jurisdiction? Is there a place for the RLLI, in the court’s analysis, in this situation? In other words, will a court eschew its own precedent and instead opt to follow the RLLI if it differs? Based on the recent decision in Catlin Specialty Ins. Co. v. J.J. White, Inc., No. 14-1255 (E.D. Pa. Feb. 27, 2018), the answer is no.

Caitlin is a lengthy decision addressing coverage, under a pollution policy, for wrongful death allegedly caused by exposure to chemicals at a Sunoco refinery. New York law applied. One issue was whether the insurer breached its duty to defend. The court concluded that it did.

Having reached that decision, the court turned to whether the insurer could still contend that it did not have a duty to indemnify the insured. In essence, the court was addressing whether an insurer, that breaches the duty to defend, has waived the right to argue that, even if it owes a defense, it still may not owe coverage for indemnity.

In arguing in support of the so-called “waiver rule,” the insureds pointed to the March 28, 2017 draft of the RLLI, section 19, which provided that “an insurer that breaches the duty to defend without a reasonable basis for its conduct must provide coverage for the legal action for which the defense was sought, notwithstanding any grounds for contesting coverage.” The court also noted that a comment to section 19 stated that the rule “encourages insurers to fulfill their duty to defend by providing a consequence for a wrongful breach of that duty,” and that “[o]rdinary contract damages may not provide an adequate incentive for insurers to defend.”

The waiver rule was the RLLI provision that caused the most contention between insurers and policyholders during the drafting process.

Despite the insureds pointing to the RLLI (draft), in support of the waiver rule, the court did not go down that road. And, as the court saw it, why would it? After all, as the court noted, the waiver rule was rejected by the New York Court of Appeals in K2 v. American Guarantee (N.Y. 2014). J.J. White stands as a court unwilling to toss out its own precedent and follow the RLLI.

In a way, Smiley Body Shop and J.J. White are easy examples. When there is no in-state law on an issue, a court’s resort to the RLLI, in conjunction with other sources, seems likely in some cases. And when there is precedent available, it seems unlikely that a court would opt to adopt the RLLI if it were different. The hard cases regarding the impact and role of the RLLI will be the ones in the middle.

Early Decision: First Winner Of The Insurance Coverage Haiku Contest

The Insurance Coverage Haiku Contest is scheduled to end on May 15. However, with the final vote on the RLLI approaching, and with writing this piece, I couldn’t help but announce one early winner. [There will still be two more winners as originally advertised.]

I was very impressed by this entry from Lance D. Meyer of O’Meara Leer Wagner &Kohl, P.A., in Minneapolis:

At first, Principles.

But they’re aspirational.

Restatements change law.

I never imagined a haiku entry based on the RLLI, not to mention one that addresses the history of the project and the question over its impact. Really well done. Congratulations Lance. Because it’s spring, the CO Prize Patrol will deliver a copy of the 4th edition of Insurance Key Issues to your office. If it were winter you’d be waiting for it.

|

|

| |

| |

| |

|

|

|

|

Vol. 7, Iss. 4

May 9, 2018

Driverless Vehicles: This Is The Point I Was Making

|

|

|

|

In the last issue of Coverage Opinions I discussed certain liability and insurance issues associated with driverless cars. My main point was this:

No matter how much safer driverless cars turn out to be (let’s assume they do), they will not be foolproof. They can’t be. So, given the gargantuan number of auto accidents that take place in this country, there will still be a significant number of accidents, even when driverless cars are involved.

Right now, when there is an auto accident, it is rare to see the automobile manufacturer named as a defendant. Auto accidents are generally matters between the involved drivers. But when a self-driving automobile is involved, drivers will no longer be fighting over which one had the red light, but whose car is to blame.

In other words, if the car involved in the accident was designed not to have accidents, it is easy to see the automobile manufacturer, and the companies that made the component parts for the self-driving aspect, being named as a responsible party in lawsuits for countless automobile accidents. Accidents that are now simple, and quickly resolved, will become complex, drawn-out, technological fights between drivers and manufacturers over who’s to blame. Car crashes will go from one of the laws simpler problems to resolve to complex product liability litigation.

On account of this shift in focus, the financial exposure for automobile manufacturers, and the companies that made the relevant component parts -- or their insurers -- will be astronomical. Even if the manufacturers ultimately win the suits, and establish that their cars were not at fault, they will likely be looking at 7-figure legal fees in many cases. Congratulations GM, you won the case….

Well what do you know… This precise scenario is about to play out in California. In late March a driver was killed in Mountain View, California, when the Tesla he was driving crashed into a concrete highway median.

According to Tesla, “in the moments before the collision … Autopilot was engaged with the adaptive cruise control follow-distance set to minimum.” Tesla continued: “The driver had received several visual and one audible hands-on warning earlier in the drive and the driver’s hands were not detected on the wheel for six seconds prior to the collision.” Tesla has also stated that owners have driven the same stretch of highway with autopilot engaged “roughly 85,000 times... and there has never been an accident that we know of.”

The family of the driver killed retained legal counsel to explore its options. The law firm stated: “(Our) preliminary review indicates that the navigation system of the Tesla may have misread the lane lines on the roadway, failed to detect the concrete median, failed to brake the car, and drove the car into the median.”

So it sounds like Tesla, at least for now, sees this as a driver-error situation and the family of the driver is looking to blame Tesla’s technology.

In non-autonomous vehicle situations, when people hit highway medians, in single car accidents, they usually do not bring lawsuits. Who’s there to sue? [It could be a UM phantom vehicle insurance claim, but that’s a different issue.] But here, because the accident took place in an autonomous vehicle, what would have very likely been a no lawsuit situation, could now become one that takes years to resolve and costs Tesla (and/or its insurers) millions of dollars in defense costs. Ultimately Tesla may prove that its vehicle was not to blame and the accident was caused by driver error.

If so, congratulations Tesla, you won the case….

|

|

| |

|

|

|

|

Vol. 7, Iss. 4

May 9, 2018

I’ve Never Seen This Before: An “Extrinsic Evidence Endorsement”

|

|

|

|

I read a lot of coverage cases and insurance policies. You do too. So we’ve all seen some unusual and unique endorsements in our day. But the “Extrinsic Evidence Endorsement,” discussed in Developers Surety & Indemnity Co. v. Alis Homes, LLC, No. C17-0707 (W.D. Wash. Apr. 16, 2018) might be my new high water mark.

The case involves construction defect coverage and the central issue was whether there was compliance with an endorsement that requires the insured to secure such things as additional insured coverage from its subcontractors, as well as a hold harmless agreement from its subs. These endorsements, and coverage decisions addressing them, have become fairly common.

The court held that no coverage was owed, as the insured satisfied none of these subcontractor requirements. And, as the court put it, “the fact that [the insured] was ‘simply . . . unaware of the requirements’ because they ‘were buried in such a long insurance policy’ does not compel a different result.”

But the policy also contained this nugget of an endorsement: In determining whether the insurer owes a duty to defend or indemnify, the insurer “may look to extrinsic evidence outside of the allegations and/or facts pleaded by any claimant” and may “rely on extrinsic evidence to deny the defense and/or indemnity of a ‘suit.’” The endorsement cautions that it changes the policy and instructs the insured to read it carefully.

For various reasons, the court, sadly, was not required to address the enforceability of this endorsement. The court noted that it was an issue of first impression, a novel question and that the endorsement conflicts with Washington law, which does not permit an insurer to look to extrinsic evidence to disclaim a duty to defend.

Would an endorsement that is contrary to Washington Supreme Court precedent, and especially addressing an issue as important as the duty to defend standard, be enforceable? On one hand, there is freedom of contract, which could say yes. And the endorsement notes that it changes the policy.

But therein lies the problem. The endorsement, despite what it says, doesn’t change the policy. The policy obligates an insurer to defend, under certain circumstances, and does not address the role of extrinsic evidence in making that determination. The endorsement changes Washington law. I’m skeptical that the Washington Supreme Court would uphold an endorsement that flies in the face of a broad duty to defend standard that clearly benefits insureds. What do Woo think?

|

|

| |

|

|

|

|

Vol. 7 - Issue 4

May 9, 2018

|

|

|

|

|

|

|

When it comes to determining the number of occurrences, under a general liability policy, courts often start out by stating that they have the choice between two tests to guide their decision – the “cause test” and the “effect test.” The “cause test” is often associated with a finding of a single occurrence – and that’s usually how it is argued by insurers. And, as policyholders see it, the “effect test” should produce multiple occurrences. The cause test is the majority rule by a Reagan/Carter-size landslide.

But how often does the “cause test” in fact result in a finding of multiple occurrences? The answer – often. Based on a review of the Number of Occurrences chapter in the 4th edition of Insurance Key Issues, here is my scorecard on the issue: 15 states that have specifically identified themselves as applying the “cause test” have issued a decision finding multiple occurrences. So, when it comes to number of occurrences, labels do not always tell the entire story.

Case in point, Nevada refers to itself as a “cause test” state for purposes of number of occurrences. But that handy label hardly provided predictability, or a finding of a single occurrence, in Century Surety Co. v. United Specialty Ins. Co., No. 17-6589 (D. Nev. Apr. 18, 2018).

Century v. United was a classic number of occurrences dispute between a primary and excess insurer. You’ve seen this scenario. The primary insurer is arguing for a single occurrence and the excess insurer says its multiple occurrences. The reasons for these positions are obvious.

At issue was coverage for defective construction at the Palazzo Hotel in Las Vegas. [Incidentally, I saw Bob Anderson’s unreal Frank Sinatra impersonation show at the Palazzo a couple of years ago. Anderson’s talents are indescribable! Do not miss it if you ever get the chance.]

Ok, back to number of occurrences.

I’ll let the court describe the construction problems: “Approximately three years after the project was completed, maintenance personnel noticed corrosion of the steel support framing underneath the Palazzo’s pools and spas located on the third and fifth floors of the hotel. An investigation determined that water leaked into the unventilated crawl space beneath the pools creating a moist and humid environment that corroded the steel framing. That framing was also inconsistent with the project’s specifications, which called for cold-formed metal stud framing with G90 galvanization. Instead, the contractors used light-gauge steel finished with a primer that was not properly finished to prevent rusting. The corrosion was so significant that it reduced the load carrying capacity of the framing system, which required replacing the system.”

The Palazzo sued the contractor. An impediment to settlement was a dispute between Liberty Mutual, the primary insurer, and AIG, the excess insurer, over each insurer’s contribution. Liberty’s policy limit was $2 million per occurrence and $4 million general aggregate. Liberty tendered $2 million, contending that the property damage was the result of a single occurrence. AIG said not so fast. It contended that there were multiple occurrences, thus triggering Liberty’s $4 million limit. Litigation ensued and the number of occurrences issue came before the court.

As expected, the court started out by noting that there were two possible tests at issue: “Nevada follows the ‘causal approach’ to determine the number of occurrences. Under this approach, the inquiry focuses on ‘the cause or causes of the injury,’ not on the ‘number, magnitude or time of the injuries.’ Thus, ‘[a]s long as the injuries stem from one proximate cause there is a single occurrence.”

The court noted that, in making its evaluation, it considers factors such as how closely the events are linked in time and space and whether the events are interdependent. But the court added: “The test is more easily stated than applied, particularly in this case.”

The court’s note about the challenge in this particular case was tied to this observation: “This case is also complicated by the fact that numerous defects and negligent acts were identified but all affected only one area of the Palazzo: the steel framing beneath its pools and spas. Thus, this is unlike cases where a contractor engaged in negligent acts that caused damage to different parts of a project, resulting in multiple occurrences.”

The court look at each insurer’s position and concluded that both were too extreme:

“Liberty contends there is a single occurrence because there is only cause: ‘the negligent failure to follow design plans and thereby use proper materials.’ Liberty paints with too broad a brush. Such an interpretation in the context of a complex construction project would make almost all construction defects a single occurrence because the insurer could simply characterize them all as a failure to follow the design, a failure to exercise due care in construction, or a failure to adequately supervise subcontractors, regardless of the dissimilarities in time, space, impact to different parts of the project, or bases of liability. . . . Liberty's position is also too narrow. It does not address that more negligent acts were identified than selecting the wrong materials. Rather, there was faulty installation (including improper waterproofing and improper pipe and drainage installation), as well as contractors allegedly leaving trash in the crawlspaces that caused drains to clog.”

AIG’s position was also too extreme -- in the other direction, as the court explained: “AIG points to all the different types of defects that were discovered, including selection of the wrong steel, improperly sealed joints around the hatches, leaks in the drain pipes, faulty installation of drain pipes, faulty installation of waterproofing, clogged drains due to trash left by the contractors, and lack of adequate ventilation in the crawlspaces. But merely showing numerous acts of negligence is not enough to show multiple occurrences.”

In the face of these competing polar positons the court held that nobody was entitled to summary judgment: “While the parties have submitted two reports identifying numerous negligent acts in selection of materials, faulty installation of various aspects of the pool system, and failure to clean up, there is no opinion expressed about whether all of these defects together are the single proximate cause of the humid environment leading to the rusting, or whether there are multiple independent causes.”

As far as the court was concerned, number of occurrences came down to proximate cause: “Nevada defines proximate cause to mean a cause ‘without which the result would not have occurred. [I]f, for example, selection of faulty material combined with faulty waterproofing would have caused the rusting even in the absence of the other conditions, and faulty material combined with leaks also would have caused the rusting even in the absence of other conditions, then there is more than one proximate cause, and more than one occurrence.”

To summarize, Nevada is a “cause test” state, the Nevada Supreme Court has addressed number of occurrences, there are hundreds of number of occurrences cases available for guidance and both insurers were represented by fine lawyers. But, despite all this, the court couldn’t decide the number of occurrences at issue and rejected both insurers’ arguments. But this much is clear -- that Nevada is a “cause test” state did not lead to predictability nor dictate a single occurrence.

So, when it comes to number of occurrences, labels do not always tell the entire story.

|

| |

| |

|

|

|

|

Vol. 7, Iss. 4

May 9, 2018

Most Important Additional Insured Case I’ve Seen In A Long Time

|

|

|

|

As important as additional insured cases can be, I rarely report on them in Coverage Opinions. They are often policy language or fact specific or both. No matter how you slice it, additional insured decisions often-times do not offer easily discernable or wide-reaching lessons.

The recent New York Court of Appeals decision in Gilbane Building Co./TDX Construction Corp. v. St. Paul Fire and Marine Ins. Co., No. 22 (N.Y. Mar. 27, 2018) is an exception. The policy language at issue is widely used and the facts at issue arise with frequency. So I am pleased to discuss a rare AI decision in CO. [Incidentally, Gilbane Building is the King of Additional Insured decisions. A Lexis search of decisions, with the name “Gilbane” in the caption, and “additional insured” in the body, gets 18 hits.]

In Gilbane No. 18 the New York high court addressed the following additional insured scenario. As is often the case, when it comes to AI decisions, there are various parties and contracts at issue. It can be confusing to the reader. The players are as follows:

Dormitory Authority of the State of New York (DASNY) (Owner) contracted with Samson Construction Company, a general contractor, for construction of a new forensic laboratory for New York City.

“DASNY also contracted with a joint venture between Gilbane Building Company and TDX Construction Corporation (‘Gilbane JV’) for Gilbane JV to be the construction manager for the project.

DASNY’s contract with Samson provided that Samson would obtain general liability insurance for the job, with an endorsement naming as additional insureds: ‘DASNY, the State of NY, the Construction Manager [Gilbane JV] and other entities specified on the Sample Certificate of Insurance provided by DASNY.’”

Samson secured general liability coverage from Liberty Insurance Underwriters. The Sample Certificate of Insurance listed as “Additional Insureds under General Liability as respects this project: . . . Gilbane/TDX Construction Joint Venture.”

To clarify, Samson Construction Company, a general contractor, has a CGL policy that purports to provide additional insured coverage for Gilbane JV.

Next, DASNY sued Samson and Perkins Eastman, Architects, P.C., the project architect, alleging construction defects. Perkins commenced a third-party action against Gilbane JV. Gilbane JV sought defense and indemnity, as an additional insured, under the Liberty policy, for the Perkins suit. Liberty denied coverage and Gilbane JV filed suit against Liberty. Following trial court and appellate division decisions, the case made it to Albany.

The additional insured endorsement at issue provided as follows:

“WHO IS AN INSURED (Section II) is amended to include as an insured any person or organization with whom you have agreed to add as an additional insured by written contract but only with respect to liability arising out of your operations or premises owned by or rented to you.” (emphasis added).

So, any person or organization with whom Samson (being “you”) agreed to add as an additional insured, by written contract, is an additional insured (but only with respect to liability arising out of your operations or premises owned by or rented to you).

But here’s the rub – Gilbane JV has no contract with Samson. Rather, Samson had a contract with DASNY -- and that’s the source of Gilbane JV’s additional insured rights.

Gilbane JV did not see this as a problem, arguing: “[T]he phrase ‘by written contract’ modifies ‘to add,’ and argues that it refers to the act of the named insured, Samson, agreeing to add an additional insured. Put differently, Gilbane JV argues that ‘by written contract’ means only that any agreement by Samson to add an additional insured must be memorialized in a writing — not necessarily a writing between Samson and the purported additional insured. Thus, according to Gilbane JV, the contract between DASNY and Samson — under which Samson agreed in writing to procure a general liability insurance policy for the construction project and to name Gilbane JV as an additional insured — was sufficient to confer additional insured status upon Gilbane JV.”

But the New York high court agreed with Liberty that Gilbane JV was not entitled to additional insured coverage: “[T]he endorsement is facially clear and does not provide for coverage unless Gilbane JV is an organization ‘with whom’ Samson has a written contract.”

To be more specific, the court held that “the endorsement would have the meaning Gilbane JV desires if the word ‘with’ had been omitted. Omitting ‘with,’ the phrase would read: ‘. . . any person or organization whom you have agreed by written contract to add . . .’, and Gilbane JV’s position would have merit. But Samson and Liberty included that preposition in the contract between them, and we must give it its ordinary meaning. Here, the ‘with’ can only mean that the written contract must be ‘with’ the additional insured.”

The dissenting opinion reached the opposite conclusion by focusing on an alternative policy reading and concluding that the endorsement is ambiguous, or, at best, has two reasonable interpretations.

More importantly, the dissent argued, in vain, that Gilbane JV was an additional insured based on principles of risk transfer in the construction context: “Consistent with this risk transfer regime, a blanket additional insured endorsement generally provides coverage for any person or organization to whom or to which the named insured is obligated to name as an additional insured by virtue of a written contract or agreement. The point of such a blanket endorsement is to furnish a means of providing such coverage that is more efficient than requiring either a separate contract between each subcontractor and each additional insured (which the majority finds to be necessary here) or that the policy list the identity of each additional insured (a list that would have to be amended whenever the named insured undertakes an obligation to add a new upstream entity, consistent with standard commercial practice). In that regard, counsel for defendant conceded that underwriting considerations for a policy like the one before us are based, not on the number or identity of additional insureds that may be covered but, instead, on the nature of the insured's work. Thus, when Samson — a subcontractor on a major construction project, with a practical understanding of risk allocation in the construction industry — procured the policy here, it would reasonably expect that it had the right to add Gilbane JV, an upstream entity, as an additional insured without the approval of, or even so much as a notification to, defendant, so long as such coverage was required by a written contract. Seen through this lens, the interpretation proffered by Gilbane JV is consistent with the reasonable expectations of the average insured upon reading the policy and employing common speech.”

The additional insured endorsement at issue here is quite common. In addition, it is not usual for a construction contract to obligate a party to name an entity as an additional insured, but where such entity (the purported additional insured) is not a party to the contract. This happens often in contacts between general contractors and subcontractors where the sub is obligated to name the general contractor AND the owner as additional insureds – but the owner is not a party to the GC-sub contract.

Common policy language + frequently occurring scenario + important court + rejection of the obvious argument about risk transfer = an important additional insured decision.

|

|

| |

|

|

|

|

Vol. 7, Iss. 4

May 9, 2018

Defense Costs Inclusive Policy – But Insurer Pays Over Its Limit

|

|

|

|

It seems that when an insurer issues a defense cost inclusive policy, its objective is to limit its potential liability, soup to nuts, to the limit set out on the declarations page. But that was not the outcome for the insurer in Mora v. Lancet Indemnity Risk Retention Group, No. 16-960 (D. Md. Apr. 17, 2018).

At issue was coverage for a $996,000 state court judgment in a medical malpractice action. The policy at issue -- defense costs inclusive -- contained a $1,000,000 limit. The insured – or someone, I can’t tell; it’s technical but not important here – sought $996,840.50 (the policy limit less the defense costs incurred of $3,159.50; not sure how only $3,000 for defense; perhaps an SIR first). Also sought from the insurer was post-judgment interest.

The court addressed various procedural issues. Beyond that the court addressed the insurer’s argument that it’s maximum liability was $1,000,000 as the policy is “defense costs inclusive.” Thus, as the insurer saw it, it had no obligation for post-judgment interest that exceeds the policy’s $1,000,000 limit.

The court did not break a sweat in rejecting the insurer’s argument: “Although Lancet’s policy includes defense costs within the amount of a ‘claim,’ the policy also explicitly provides for post-judgment interest as a payment supplemental to a claim, rather than as a defense cost subject to the claim limit. Compare ECF No. 22-1 at 17 (defining defense costs) with ECF No. 22-1 at 39 (defining supplemental payments to include ‘[a]ll interest on the full amount of any judgment that accrues after the entry of judgment and before we have paid, offered to pay, or deposited in court the part of the judgment that is within the applicable Limits of Liability (emphases added by court)). Therefore, post-judgment interest is not a defense cost subject to the claim limit.”

The moral of the story, for insurers that write “defense costs inclusive” policies, for purposes of limiting their exposure to the amount on the Dec. page, is simple.

|

|

| |

|

|

|

|

Vol. 7, Iss. 4

May 9, 2018

Doobie-ous Decision: Marijuana House May Be One’s Principal Residence

|

|

|

|

The court’s decision in Weingarten v. Auto-Owners Insurance Co., No. 17-1401 (D. Colo. Apr. 17, 2018) will be of very little practical value for Coverage Opinions readers. It is a first-party property case, which is not what the vast majority of CO readers handle. And, even for those who do, the facts are really unique and have a low probability of arising again. Nonetheless it is a very interesting case. And CO article titles, with marijuana in the name, surely get read more than one’s announcing – click here to read about additional insureds.

Initially, a Colorado District Court granted summary judgment for an insurer in some sort of homeowner’s property case. The case I’m discussing here, a subsequent one, does not describe the nature of the property damage. It has something to do with virtually the entire use of the home for a marijuana grow operation. I could do a few minutes of research to find out more but it’s not important to cheech the lesson here. The court granted summary judgment on the basis that the policyholders were not able to demonstrate a disputed fact that their house was being used principally as a private residence, which was a requirement to secure coverage. The best the homeowners could do was offer a conclusory statement that people were living in the joint. This was not enough as the court saw it.

But the policyholders were not ready to roll over. They filed a motion for reconsideration, attempting to introduce previously unavailable photos and a video of the home (new evidence, previously unavailable, is a basis for a motion for reconsideration, the court noted).

Based on the photos and video, the court, describing it as a “very close call,” concluded that there was now a disputed issue of fact as to whether the individuals growing marijuana were principally using the house as their private residence (i.e., chief, primary or most important use for the property).

Here’s what the photos and video showed: “The pictures reveal that the individuals using the property paid for internet and received mail at the property. The video shows that the house contained a dining room table, photographs and art on the walls, a couch, a television, a washing machine and a bottle of detergent with clothes hanging nearby, and a pool table.”

The court concluded that “[t]hese aspects of the video demonstrate that individuals may have used the house for entertainment, daily meals, and regular chores, which is some indicia that the house was used principally as a private residence. Additionally, the video shows mattresses in two bedrooms; a desk, an office chair, and a night stand in one of the bedrooms; a bathroom with a toothbrush and mouthwash on the sink; clothes in one of the closets; and a coffee pot with coffee grounds in the kitchen.”

But the court was also quick to note that the video and photographs also supported the notion that the house was used principally as a marijuana grow operation.

The motion for reconsideration was granted.

Incidentally, why, you wonder, were the photos and video unavailable at the time that the court was addressing summary judgment? It was in the District Attorney’s file for the prosecution of the individuals allegedly growing marijuana at the property.

|

|

| |

|

|

|

|

Vol. 7, Iss. 4

May 9, 2018

Nuisance Claim Creates Coverage For Neighbors Sued For Being… A Nuisance

|

|

|

|

I love coverage cases involving disputes between neighbors. There is a voyeuristic aspect to seeing the various tactics that people take to cause annoyance to each other. Not Hatfield and McCoy-type stuff. More like getting under each other’s skin. That’s what’s at issue in American Reliable Ins. Co. v. Vlieland, No. 17-100 (D. Mont. Mar. 30, 2018), although there are some serious allegations here as well.

Randy Self and Tina Roberts live in Hungry Horse, Montana. They sued their neighbors, the Vlielands, alleging that they intentionally harassed, disrupted, and interfered with their enjoyment of life. Self and Roberts asserted claims for nuisance, intentional infliction of emotional distress and assault, alleging that “(1) the Vlielands played loud music and directed noise at [Self and Roberts’s] residence; (2) the Vlielands poisoned [Self and Roberts’s] dog; (3) Jeff Vlieland pointed a pistol at Randy Self; (4) Jeff Vlieland tried to run Tina Roberts off the road; (5) the Vlielands threw rocks at [Self and Roberts’s] residence; and (6) the Vlielands increased the height of their fence to block [Self and Roberts’s] view.”

The Vlielands turned to their homeowner’s insurer, American Reliance, for defense and indemnity. American Reliable defended under a reservation of rights and filed a coverage action. American Reliable argued that the policy precluded coverage because the conduct alleged does not qualify as an “occurrence,” i.e., accident. And, the insurer argued, if it does qualify as an “occurrence,” five policy exclusions further preclude coverage: 1. “Intentional Acts Exclusion”; 2. “Illegal Activities Exclusion”; 3. “Expected or Intended Acts Exclusion”; 4. “Assault and Emotional Abuse Exclusion”; and 5. “Punitive Damages Exclusion.”

Following a review of Montana law, the court stated that an “accident” “may include intentional acts if such acts resulted in unintended or unexpected consequences. Here, there are factual disputes to be resolved at trial regarding whether the Vlielands’ actions constituted negligent or intentional conduct. Though the acts are alleged as claims of intentional infliction of emotional distress and assault, they are also alleged in a claim of nuisance, which may be premised on negligent conduct. Additionally, it’s not plain from the face of the pleadings that the consequences of the Vlielands’ alleged acts were objectively intended or expected. Therefore, an issue of fact remains regarding whether the acts in the Underlying Complaint trigger an ‘occurrence’ under the Policy, which precludes summary judgment at this time.”

The court also held, for similar reasons, that summary judgment was not appropriate with respect to the various intentional-based exclusions, including the Intentional Acts exclusion, which precludes coverage for “bodily injury or property damage: a. Which is intended by, or which may reasonably be expected to result from any intentional act, or omission, of any person insured by this policy. . . . This exclusion applies even if: . . . (2) Such bodily injury or property damage is of a different kind or degree than intended or reasonably expected by any insured.”

Here the court explained that “the ‘Intentional Acts Exclusion’ and ‘Expected or Intended Exclusion’ do not preclude coverage if there is a possibility that the conduct had unintended and unexpected consequences to the victim. The parties dispute whether the Vlielands’ actions were negligent or intentional, which present factual issues to be resolved at trial in the Underlying Litigation. Because questions of fact exist regarding whether the Vlielands’ conduct was intentional or negligent, and if found intentional, whether the Vlielands’ could have expected or intended the consequences of that conduct, summary judgment is not proper on the ‘Intentional Acts Exclusion’ and ‘Expected or Intended Exclusion.’”

The take-away: The court here made it no easy task for an insurer, to disclaim coverage to an insured, for conduct – see above -- that could not have had anything other than expected or intended consequences.

|

|

| |

|

|

|

|

| |

|

|

One Of These Things Just Doesn’t Belong

In Ibrahim Sabbah v. Nationwide Mut. Ins. Co., No. 15-1772 (N.D. Ala. Apr. 18, 2017) the court noted that “[i]t is settled that the law in [Alabama] does not permit recovery for personal injury, inconvenience, annoyance or mental anguish and suffering in an action for breach of a contract of insurance.” But Alabama law does allow recovery of mental anguish damages, for breach of contract, under certain circumstances: “those concerning the plaintiff’s home [repair or construction], the burial of loved ones, a physician’s promises to deliver a child, or a new car warranty.”

Photocopies And “No Occurrence”

Are you tired of hearing if faulty workmanship is an occurrence? If so, here’s a different occurrence question: “In the Underlying Lawsuit, Caven alleges that Associa [condo management company] charged him and other owners an excessive fee in exchange for copies of condominium documents. The expected and reasonably foreseeable result of Associa’s act is that Caven and other owners would incur this fee. Thus, pursuant to Hawai’i law, the Court finds that Associa’s alleged act of charging Caven and other owners fees for copies of condominium documents was intentional, and not an accident. Accordingly, pursuant to Hawai’i law, Associa’s alleged act of charging excessive fees does not constitute an ‘occurrence’ under the Policy. The Court makes this finding regardless of whether Associa believed that its fees were excessive or in violation of Hawai’i law.” State Farm Fire & Casualty Co. v. Certified Management, No. 17-00056 (D. Haw. Apr. 27, 2018).

1973 ISO Filing: Notice-Prejudice Rule Applies To Claims Made Scenario

In Petrosantander United States v. HDI Global, No. 16-1320 (D. Kan. Apr. 9, 2018) a Kansas District Court predicted how the Texas Supreme Court would address a late notice issue under a Pollution Extension Endorsement with a claims made quality. [“Toto, I’ve a feeling we’re not in Kansas anymore.”] At issue was coverage under a Pollution Extension Endorsement contained in a commercial general liability policy. Putting aside several policy requirements, and another notice issue, and paraphrasing, the policy required that a “pollution incident” be reported to the insurer within 120 days after it first became known to the insured. The insured spilled salt water over rural land on August 10, 2014. The insurer did not receive notice until 141 days after the insured discovered it. Despite the claims made aspect to the Pollution Extension Endorsement, the court held that the insurer must prove prejudice, based on a 1973 Order of the Texas State Board of Insurance (following approval of an ISO filing), requiring that all general liability policies issued or delivered in Texas contain an endorsement stating: “As respects bodily injury liability coverage and property damage liability coverage, unless the company is prejudiced by the insured’s failure to comply with the requirement, any provision of this policy requiring the insured to give notice of action, occurrence or loss, or requiring the insured to forward demands, notices, summons or other legal process, shall not bar liability under this policy."

Mississippi High Court To Address Voluntary Payment and Right To Recovery

The 5th Circuit, in Colony Ins. Co. v. First Specialty Ins. Corp., No. 17-60094 (5th Cir. Apr. 16, 2018) certified the following questions to the Supreme Court of Mississippi: “Mississippi's voluntary payment doctrine does not bar an insurer from recovering a settlement payment made under ‘compulsion’ or as the result of a settlement-related ‘legal duty.’ 1. Does an insurer act under ‘compulsion’ if it takes the legal position that an entity purporting to be its insured is not covered by its policy, but nonetheless pays a settlement demand in good faith to avoid potentially greater liability that could arise from a future coverage determination? 2. Does an insurer satisfy the ‘legal duty’ standard if it makes a settlement payment on behalf of a purported insured whose defense it has assumed in good faith, but whose coverage under the policy has not been definitively resolved, even if the insurer maintains that the purported insured is not actually insured under the policy?”

|

|

| |

|

|

|

| |

|

|

|

|

|

|

|

|

|